Cash Flow Forecasting: A Practical SME Playbook for 2026

Sales are up. Margins look healthy. The P&L says the business is doing fine. Then payroll week arrives, two customers push payment, a supplier wants settlement before releasing the next order, and the bank balance tells a very different story.

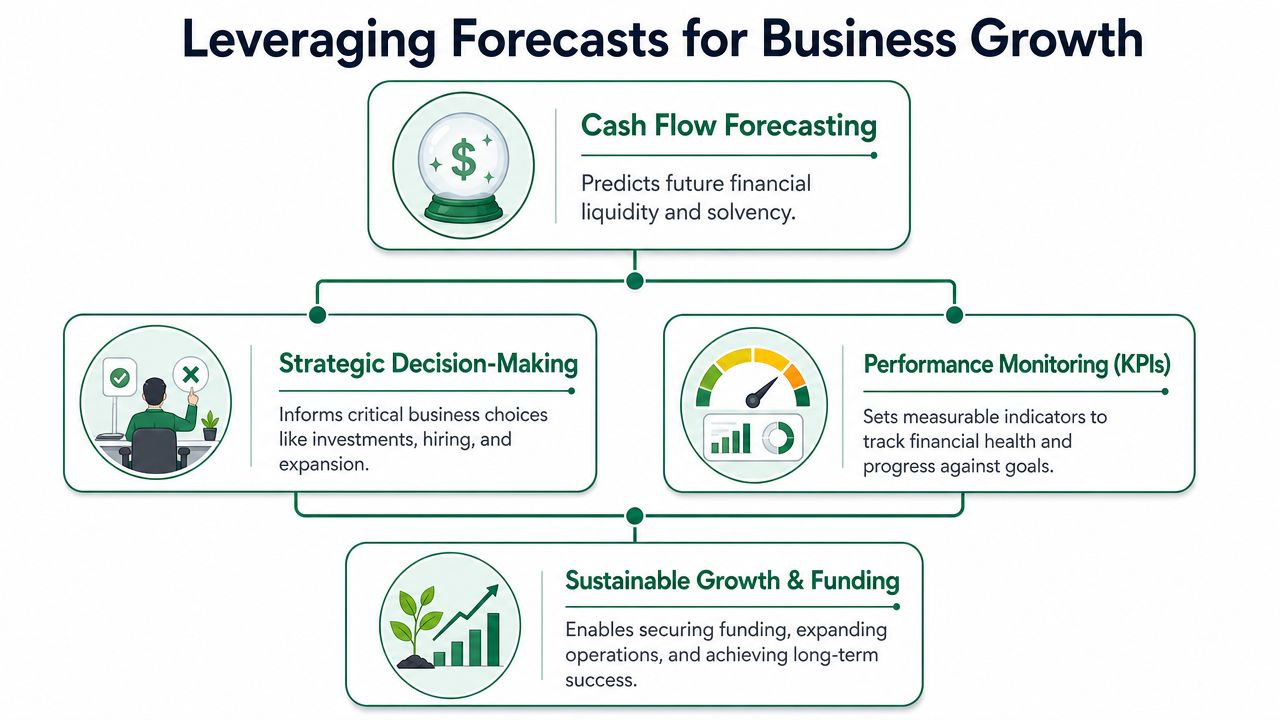

That's the moment most SME owners and finance managers in the UAE start taking cash flow forecasting seriously. Not because it's a finance best practice, but because the gap between revenue and cash can get uncomfortable very quickly in this market. A forecast gives you something more useful than optimism. It gives you timing, pressure points, and room to act before the problem reaches the bank account.

Why Profitable Businesses Still Run Out of Cash

A profitable business can still become illiquid. That isn't a contradiction. It's a timing problem.

Take a common SME pattern in the region. You invoice a good month of sales, book the revenue, and assume the pressure is easing. But rent, salaries, supplier payments, freight, and tax obligations don't wait for your customers to pay. In the UAE, that mismatch is structural. A 2024 payment survey referenced by Insightsoftware found that the average B2B invoice was paid in 54 days, and 36% of all B2B sales became overdue.

That gap is where profitable businesses get squeezed.

Profit doesn't pay this week's bills

Accounting profit records performance. Cash pays obligations. Those are related, but they don't move on the same timetable.

If your finance team is only reviewing margin, sales growth, and month-end reports, it can miss actual operational risk. Cash pressure often starts in accounts receivable, not in declining demand. One delayed customer can throw off supplier timing, inventory planning, and management decisions for the next few weeks.

Practical rule: If collections behaviour is volatile, your forecast should be treated as an operating tool, not a reporting file.

A lot of owners look for profitability advice first, which is fair. Resources like Everglow Prosperity's guide on business profitability are useful for improving margins and commercial discipline. But higher profit alone won't fix a collections lag. You still need visibility into when cash lands.

The trap most SMEs fall into

The usual sequence looks like this:

- Revenue is booked early: The sale is real, the invoice is issued, and the team feels secure.

- Cash leaves on fixed dates: Payroll, rent, utilities, logistics, and suppliers still need paying on schedule.

- Collections slip: A key account pays late, pays partially, or disputes part of the invoice.

- Management reacts too late: By the time the issue is obvious, the only choices left are delay, scramble, or cut.

That's why a practical forecast matters more than a polished one. It should tell you what happens if receipts arrive later than planned, not just whether annual revenue targets look achievable.

If your team is still trying to fix liquidity after the shortfall appears, start with a more disciplined view of timing and collections. A straightforward guide on how to improve cash flow can help frame the operational changes, but the foundation is still the same. Know when cash is expected, know what must be paid, and know the gap before it becomes urgent.

Choosing Your Forecasting Method and Horizon

Most SMEs don't need a complex model first. They need the right method for the job.

The mistake I see most often is using one forecast for everything. Teams try to manage next week's cash risk with a budget-style model, or they try to make long-range planning decisions from a highly detailed daily cash sheet. Both approaches create noise.

Direct versus indirect

The easiest way to think about it is this. The direct method asks, “What cash will come in and go out?” The indirect method asks, “Starting from expected profit, what does that imply for cash over time?”

Here's how the trade-off works in practice:

- Direct method: Better when you need visibility into actual receipts and payments. This is the method finance teams use to manage liquidity, supplier timing, payroll readiness, and near-term risk.

- Indirect method: Better when you're planning at a higher level. It's useful for annual planning, board discussions, and understanding whether the business is structurally cash generative over a longer period.

For most SMEs in the region, the practical choice is clear. A rolling 13-week direct forecast is the most useful baseline. Numeric notes that this horizon is short enough to manage immediate liquidity risk and long enough to support medium-term decisions, and it recommends updating the forecast weekly using integrated data feeds.

Why the 13-week horizon works

A 13-week view forces discipline without pretending you can predict the full year with precision. It's long enough to surface upcoming strain around payroll cycles, supplier settlements, seasonal buying, and delayed collections. It's short enough that the underlying assumptions still mean something.

That's why I prefer weekly buckets for this horizon. Daily detail over a longer window often creates false precision. Monthly buckets, on the other hand, can hide a liquidity problem until it's already close.

The best SME cash flow forecasting model is usually not the most detailed one. It's the one your team can refresh every week without breaking it.

A simple way to choose

Use this decision lens:

- Use direct forecasting when: You need to answer whether cash will be available to meet obligations on time.

- Use indirect forecasting when: You need to connect operating plans, budgets, and financial statements to longer-term cash expectations.

- Use both when the business is growing: One model manages survival and timing. The other supports strategy.

If your team is trying to tighten the connection between receivables, payables, and inventory timing, it also helps to understand the cash conversion cycle. That metric doesn't replace a forecast, but it explains why some businesses feel permanent pressure even when sales remain steady.

Building Your First Reliable Forecast Model

You don't need specialist software to start. You need clean inputs, clear categories, and a weekly rhythm.

Most unreliable forecasts fail before modelling even begins. The opening cash balance is wrong, receivables are stale, payables are incomplete, and someone is still copying figures from multiple spreadsheets. If the starting point is off, the forecast will only give you false confidence.

Start with reconciled data

Build the model from sources that reflect actual cash movement:

- Bank balances: Use reconciled balances, not rough figures from memory or screenshots.

- Accounts receivable: Work from invoice-level data, expected payment dates, and any known disputes or promised delays.

- Accounts payable: Include due dates, agreed terms, and any supplier arrangements that may shift.

- Payroll and fixed overheads: Salaries, rent, utilities, software, and recurring service costs should already be scheduled.

- Operational commitments: Freight, customs, marketing campaigns, inventory purchases, and one-off project costs need to be visible.

- Tax schedules: Corporate tax can no longer sit outside the liquidity conversation.

Structure the model around cash, not accounting categories

Keep the first version plain. Each period should show:

- Opening cash

- Expected inflows

- Expected outflows

- Net movement

- Closing cash

That sounds basic because it is. The discipline comes from how you classify and time each line.

Inflows should be based on when money is likely to be collected, not when the invoice was issued. Outflows should be based on when money must leave the account, not when the expense is recognised in the books.

Don't forget corporate tax

Many UAE SMEs must now adjust old habits. The UAE corporate tax framework referenced by TreviPay applies 0% to taxable income up to AED 375,000 and 9% above that threshold. Since the tax came into effect from 1 June 2023, profitable businesses need to forecast tax-related cash outflows alongside operations.

That changes the role of forecasting. It's no longer just about business visibility. It's part of compliance-linked planning. A business can show healthy profitability and still hit a tight cash position if tax falls due while receivables are still outstanding.

What works in practice: Build tax as a planned cash event in the forecast, not as an afterthought after month-end reporting.

If you're trying to improve financial discipline more broadly, this breakdown of how to improve financial planning and control is a useful complement to the forecasting process. It pairs well with stronger cash routines because planning improves when treasury, accounting, and operations are working from the same assumptions.

Keep the process lightweight

A workable first model should answer a few questions quickly:

- Can we meet every committed payment on time?

- Which receipts are carrying too much weight in the next few weeks?

- What happens if one major customer slips?

- Are there large non-routine outflows approaching?

If you're formalising this process across the finance function, a stronger treasury management setup will help. The forecast should sit inside a wider operating rhythm that includes reconciliations, approvals, payment timing, and variance review.

When collections uncertainty is the largest source of forecast error, some SMEs simplify the problem at its source. Comfi’s invoice discounting allows businesses to convert outstanding receivables into cash within hours, effectively replacing an unpredictable inflow line with a confirmed one. That kind of adjustment does not eliminate the need for forecasting, but it does narrow the range of outcomes the model needs to handle, and it makes the weekly refresh far more reliable.

Using Scenarios to Stress-Test Your Business

One forecast is just one version of the future. It's useful, but it isn't enough.

The finance teams that get real value from cash flow forecasting don't stop at a baseline. They build scenarios around the risks that hit the business. In MENA, that usually means collection timing, supplier disruption, and inventory delays much more than abstract “best case” and “worst case” revenue assumptions.

Focus on the risks that move cash

A lot of generic guidance tells you to model sales up, sales flat, and sales down. That can help at a strategic level, but it often misses the immediate issue. For many SMEs, the bigger danger is that sales happen and cash still arrives late. As Sage notes in its cash flow forecasting guidance, the primary risk for many MENA businesses is payment timing, and effective forecasting should be built around collections scenarios.

That's a better lens because it reflects how liquidity pressure usually appears in practice.

Scenarios worth building first

Start with a small set of scenarios your team can maintain:

- Delayed key customer payment: Move a major receivable out and see what happens to payroll, supplier plans, and minimum cash.

- Partial collection: Assume only part of a promised inflow lands this period.

- Supplier acceleration: Model a vendor requiring earlier payment before releasing goods.

- Inventory hold-up: Push expected stock arrival and test the effect on sales conversion and downstream receipts.

- Tax and one-off overlap: Check what happens when a scheduled tax payment lands in the same period as another large outflow.

Each one should lead to a management decision. If a customer delay creates a shortfall, who escalates collections? If inventory slips, do you defer another spend? If a supplier compresses terms, which purchase gets priority?

Good scenario design isn't about drama. It's about making predictable stress visible early enough to respond.

Build scenarios around behaviours, not hopes

What usually fails is a scenario file built once and ignored. Or a “base case” that assumes everything goes to plan.

A better approach is to tie scenarios to known behaviours:

- customers who regularly pay late

- suppliers who won't release stock without settlement

- inventory lines that convert slowly

- months where operating costs bunch together

- commercial deals that improve revenue but extend collection timing

That last point matters. Growth can increase pressure before it improves liquidity. More orders often mean more stock, more supplier commitments, and more exposure to receivables timing.

If your forecast doesn't test those pressures, it's not helping management make better decisions. It's just recording a preferred outcome.

From Forecasting to Funding Your Growth

A forecast should trigger decisions. If it only produces a weekly file that no one acts on, it's wasted effort.

The best finance teams use forecasting to decide when to slow spending, when to push collections, when to delay a purchase, and when to use external tools that smooth the cash gap between commitment and receipt. That's where forecasting becomes commercial, not just administrative.

Set triggers before you need them

You don't want to invent your response in the middle of a tight week. Set clear internal triggers in advance.

Examples that work well:

- Minimum cash threshold: The point where management review becomes mandatory.

- Collections concentration alert: A warning when too much of the next period depends on one or two receipts.

- Inventory ageing review: A regular check for stock that's absorbing too much cash for too long.

- Supplier pressure flag: A sign that terms are tightening or settlement requests are moving forward.

These don't need to be complicated. They just need to be visible and linked to action.

Match the tool to the cash problem

Different cash pressures call for different responses.

If the issue sits in receivables, some businesses model the effect of invoice discounting to pull cash forward. If the issue sits in buyer conversion, some teams model Buy Now, Pay Later terms to support demand while protecting internal cash planning. If the issue sits in stock-heavy trading, the forecast should test what happens when inventory liquidity improves and capital tied up in stock is released.

That last point matters a lot in automotive and other asset-heavy sectors. Generic forecasting advice usually stops at “include inventory”. It doesn't go far enough. As Pathward's guide notes, dealer-style businesses can have cash tied up in inventory for up to 180 days, which means the real question isn't only next month's balance. It's how much capital is trapped in ageing stock, and when that starts limiting growth.

Use the forecast to compare choices

Once the model is stable, it becomes a decision engine.

You can ask:

- what happens if we take a larger order with longer payment terms

- whether accelerating stock turnover changes the next quarter's cash position

- how supplier terms affect buying decisions

- whether a receivables-based solution closes the projected gap cleanly

- how much headroom exists before expansion becomes risky

That's the point where forecasting supports growth, not just control.

For founders and operators thinking more broadly about how businesses raise non-dilutive capital in 2026, it helps to evaluate those options inside a forecast rather than in isolation. The right choice isn't the one that sounds flexible on paper. It's the one that improves timing, preserves operating room, and fits how cash moves through your business.

Your Implementation Checklist and Common Pitfalls

If your team is starting from scratch, keep it simple and repeatable. A useful cash flow forecasting process is better than an elegant model no one updates.

Implementation checklist

- Choose one operating horizon: Start with a rolling short-term view that management can review every week.

- Use reconciled opening cash: Don't build on estimated balances.

- Pull the right source data: Bank, AR, AP, payroll, recurring overheads, tax, and major one-off commitments.

- Classify by timing: Record when cash is expected to move, not when revenue or expense is recognised.

- Review variances weekly: Compare forecast versus actual and fix assumptions quickly.

- Escalate exceptions early: Flag overdue collections, compressed supplier terms, and unusual outflows before they become urgent.

The mistakes that cause most forecast failures

Some problems are almost universal.

- Confusing profit with liquidity: A healthy P&L can hide a weak cash position.

- Treating all receivables as equal: Some customers pay on time. Some don't. Your model should reflect that.

- Ignoring tax and one-off items: These are exactly the cash events that create surprises.

- Relying on stale spreadsheets: Manual copying introduces lag and errors.

- Building once and forgetting it: Forecasts drift quickly if they aren't refreshed.

There's also a technology point worth taking seriously. Resolve's summary of predictive cash forecasting notes that AI-driven forecasting can reduce errors by 20% to 50% compared with traditional spreadsheet methods. That doesn't mean every SME needs a complex system on day one. It does mean manual forecasting has limits, especially when payment behaviour is irregular.

A forecast should get more accurate because your team learns from it every week. If the same surprises keep happening, the process isn't doing its job.

The practical standard is straightforward. Keep the model grounded in real cash data, update it on a fixed cadence, and use it to drive decisions before cash becomes tight.

If your forecast consistently highlights cash pressure from receivables timing, inventory lock-up, or supplier payment windows, the most valuable next step is mapping a practical response before the shortfall arrives. Comfi gives UAE and MENA SMEs access to Invoice Discounting, B2B Buy Now Pay Later, and Automotive Dealer Financing, so the finance team can act on a forecasted gap rather than scramble to react to one. The businesses that forecast well and plan their liquidity tools in advance are the ones that turn cash visibility into a genuine competitive advantage.