Mastering The Cash Conversion Cycle For SME Growth

Think of your business's cash flow as its circulatory system. Money needs to move constantly to keep things healthy and growing. The cash conversion cycle (CCC) is a key performance indicator that measures the speed of that circulation.

Simply put, it’s the number of days it takes for the money you spend on inventory to make its way back into your pocket as cash from a sale. A shorter cycle is a sign of a fit, efficient business. A longer one? That's a red flag that your cash is getting stuck somewhere.

What The Cash Conversion Cycle Really Means For Your Business

Let's use a practical example. Imagine you own a small electronics shop. Your CCC is the time that passes between you paying your supplier for a batch of new headphones and the moment a customer pays you for a pair. It’s the life cycle of your cash.

A short CCC means your money is always working for you, quickly turning back into usable cash that can fund the next order, pay salaries, or fuel expansion. But when that cycle stretches out, your cash is tied up—either sitting on a shelf as unsold inventory or waiting in a customer's bank account as an unpaid invoice.

For any small or medium-sized business in the MENA region, this isn't just accounting jargon. It's a direct measure of your operational health and your ability to stay nimble. A tight grip on your CCC is a true strategic advantage, giving you the liquidity to run your daily operations and jump on new opportunities without hesitation.

The Three Pillars of Your Cash Flow

To truly understand your CCC, you need to look at the three levers that control it. Each one is a stage where your cash can either flow smoothly or get bogged down.

- Inventory: How long do your products sit on the shelf before they sell? The longer they're there, the longer your cash is locked up in physical goods.

- Receivables: After you make a sale, how long does it take for your customers to actually pay you? Every day an invoice is outstanding is a day that cash isn't in your bank account.

- Payables: This is the other side of the coin—how long do you have to pay your suppliers? Smartly extending this period gives you more time to use your cash before it goes out the door.

A lower CCC means you're turning inventory and invoices into cash—fast. This not only helps you meet your own financial obligations with ease but also puts you in a much stronger position when you need to improve your cash flow. Businesses with a strong CCC often find it easier to unlock their working capital.

Getting these three pillars in balance is the secret to a shorter cash conversion cycle and a more resilient business. Understanding what the CCC means is the first step, but it's part of a bigger picture. To get a wider view, it's worth mastering financial analysis techniques for total control. As we cover in our guide to improving cash flow for small businesses, these metrics are absolutely fundamental to your success.

Breaking Down The Cash Conversion Cycle Formula

At first glance, the formula for the cash conversion cycle might look like something straight out of an accounting textbook. But it’s actually telling a very simple story about your company's cash. The formula is: CCC = DIO + DSO - DPO.

Think of it this way: each part of that equation is a chapter in the story of your working capital. It tracks the exact number of days your money is tied up in the process of doing business, from spending cash to getting it back. Getting a handle on this formula is the first step to truly mastering your company's liquidity.

The goal is to shrink the time between cash going out and cash coming in. That’s what optimizing your CCC is all about. Let's pull apart each piece to see how it works.

DIO: Days Inventory Outstanding

Days Inventory Outstanding (DIO) is the average number of days your products sit on the shelf before they're sold. It’s a direct measure of how long your cash is locked up in physical stock. The higher the DIO, the more money you have just sitting in a warehouse, not earning a thing.

For example, a MENA-based auto parts distributor has a high DIO if a shipment of filters and brake pads sits on their shelves for months. Every single day those parts go unsold, the cash used to buy them is trapped.

A lower DIO is almost always a good sign. It means you're moving products efficiently and turning your inventory back into cash quickly.

DSO: Days Sales Outstanding

Days Sales Outstanding (DSO) tracks the average time it takes you to get paid after you’ve made a sale. It’s the gap between issuing an invoice and seeing the money actually hit your bank account. This metric puts a spotlight on how effective your collections process really is.

Imagine a software company in Riyadh that sells yearly subscriptions. Their DSO is the number of days they have to wait for a corporate client to pay up after the service is already running. A high DSO can choke a business, creating huge cash flow problems even if you're technically profitable on paper.

Bringing down your DSO is one of the fastest ways to inject cash back into your business and improve your CCC.

DPO: Days Payables Outstanding

Days Payables Outstanding (DPO) measures how long your company takes to pay its own bills to suppliers. Now, this one is different. Unlike DIO and DSO, a higher DPO is often a good thing for your cash flow because it means you're holding onto your cash for longer.

A food and beverage wholesaler in Dubai, for instance, might negotiate 60-day payment terms with its produce suppliers. That DPO gives them two full months to sell the goods and collect from their restaurant customers before their own bill is due.

The core idea is simple: CCC = (Time to Sell) + (Time to Collect) - (Time to Pay). It's a clear measure of your operational efficiency and a vital sign of your company's financial health.

Getting this cycle right isn't just an academic exercise. Across the MENA region, the connection between a shorter cash conversion cycle and better business performance is well-documented. Research clearly shows that companies that successfully reduce their CCC see a direct increase in profitability. For finance managers, this proves that every single day shaved off the cycle boosts liquidity and your return on assets.

Why a Shorter Cash Conversion Cycle Gives You a Real Edge

Lowering your company's cash conversion cycle isn't just some abstract financial goal—it's about building a smarter, stronger, and more nimble business. When you get this right, a simple metric transforms into a serious competitive advantage out in the real world.

Think about it: when your cash moves faster, your entire operation becomes more responsive. With better liquidity, you have the freedom to jump on opportunities as they pop up, without constantly stressing about making payroll or paying your suppliers. For any small or medium-sized business, that kind of financial breathing room is a total game-changer.

From Metric to Momentum

A business with a tight CCC is light on its feet, ready to pivot or sprint when needed. In contrast, a competitor with a long, sluggish cycle is bogged down, slow to react when the market shifts. The difference is night and day, and it quickly separates the winners from the losers.

Imagine a UAE-based electronics retailer. With a short CCC, they can spot a hot new gadget, place a big order, and have it on their shelves before anyone else. That speed lets them grab market share while their rivals are still stuck waiting for cash from last month's sales to come in.

It works the same way for an F&B distributor. If you’re known for paying your suppliers quickly, you can often get better prices and more flexible terms. A reputation for being financially solid, backed by a low CCC, opens doors to better partnerships and a more reliable supply chain.

An optimized cash conversion cycle stops being a number on a spreadsheet and becomes a core part of your growth strategy. It frees you up to invest in marketing, add new products, and handle economic curveballs with a healthy cash buffer.

The impact isn't just theoretical. It touches every part of your business, giving you the power to make proactive decisions instead of just reacting to problems.

The Real-World Payoffs of a Shorter CCC

Let’s get specific. Here’s exactly how a lower cash conversion cycle strengthens your business and your position in the market.

- Better Liquidity and Cash Flow: This is the most obvious win. A shorter cycle means cash gets back into your bank account faster. That money is the lifeblood for daily operations, covering everything from rent to marketing spend. You can finally breathe a little easier.

- More Operational Flexibility: When you have cash readily available, you can say "yes" to time-sensitive opportunities. Maybe that’s buying inventory at a bulk discount, investing in new equipment to work more efficiently, or launching a quick promotion to get ahead of the competition.

- Stronger Supplier Relationships: Paying suppliers on time—or even early—builds incredible trust. This can lead to better terms, priority service, and a supply chain you can count on, which is a massive advantage no matter what industry you're in.

- Higher Profitability: A shorter CCC can directly fatten your bottom line. By needing less outside money to fill cash gaps, you save a bundle on interest payments. Plus, turning over inventory faster means you spend less on storage, insurance, and other holding costs.

This focus on efficiency is catching on. Companies across the Middle East recently improved their net working capital efficiency by 5.6%, which cut a full six days from their average cycle. This shift, driven by smarter inventory and receivables management, is freeing up billions in cash that SMEs can now pour back into growth. To see the full picture of these regional shifts, you can learn more about working capital improvements in the Middle East.

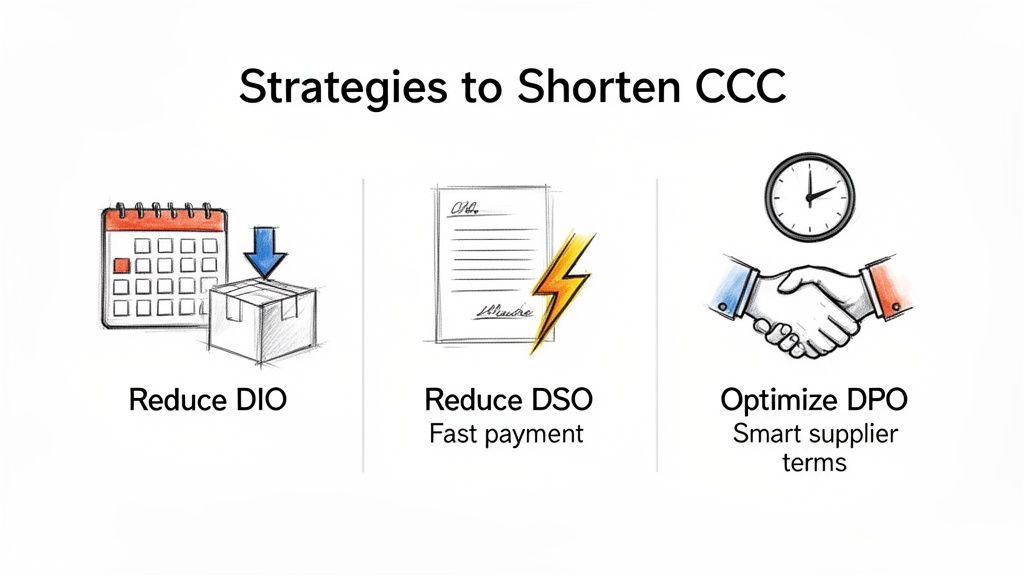

Actionable Strategies To Shorten Your Cash Conversion Cycle

Knowing the theory behind the cash conversion cycle is one thing, but actually putting that knowledge to work is where the magic happens for business growth. The real shift from theory to action comes down to focusing on the three pillars of your CCC: your inventory, your receivables, and your payables.

By making smart, targeted tweaks in each of these areas, you can systematically shrink your cash cycle and free up the working capital that’s currently stuck in your operations. The trick is to see each component not as a siloed problem but as an interconnected part of your overall cash flow engine.

Let's break down the practical, no-jargon strategies you can start using today to make your business more financially nimble.

Tactic 1: Reduce Your Inventory Days (DIO)

Every item sitting in your warehouse is cash that isn't working for you. The longer it sits there, the higher your DIO climbs and the more drawn-out your cash conversion cycle becomes. The goal is simple: move stock faster and smarter.

Start by getting better at demand forecasting. Dive into your historical sales data and keep an eye on market trends to get a clearer picture of what your customers will want, and when. This simple step helps you avoid tying up cash in slow-moving products while ensuring you're never out of your bestsellers.

Another powerful move is to adopt a just-in-time (JIT) inventory model. This means timing your orders so that goods arrive from suppliers right when you need them for production or sale, slashing the time they spend gathering dust in your warehouse.

A lower DIO doesn't just shorten your cash cycle; it also cuts down on storage, insurance, and obsolescence costs, directly boosting your profitability. It's about having the right amount of stock at exactly the right time.

Here are a few more ways to improve your DIO:

- Analyze Slow-Moving Stock: Regularly pinpoint products that aren’t selling. Create promotions or bundle deals to clear them out and recoup your cash.

- Strengthen Supplier Relationships: Partner with suppliers who offer quicker, more reliable deliveries. This allows you to hold less safety stock with confidence.

- Use Technology: Good inventory management software gives you real-time visibility into stock levels, sales velocity, and reorder points.

Tactic 2: Shrink Your Sales Days (DSO)

Your Days Sales Outstanding (DSO) is simply the time it takes for you to get paid after you make a sale. For most SMEs, this is often the area ripe for the quickest and most significant cash cycle improvements. Faster collections mean faster access to your own money.

A critical first step is to tighten up your credit policies. Before you extend credit to a new customer, do your homework. A quick check on their payment history and financial stability can save you major headaches down the road. Setting clear, firm payment terms from the get-go also prevents any confusion.

Offering small incentives for early payment can work wonders. A small discount, like 2% off if an invoice is paid within 10 days instead of 30, can be just the nudge many clients need to pay sooner. That small hit is often well worth the benefit of having cash in hand.

Of course, the most direct approach is to make paying you as easy as possible. This is where modern payment solutions can be a game-changer. For instance, exploring options like invoice discounting solutions can show you how to get cash from your invoices almost immediately, instead of waiting weeks or even months for your customers to pay.

To really shorten your CCC, you have to focus on the sales-to-cash process. Putting some essential accounts receivable best practices into place will help you collect what you're owed, faster.

Tactic 3: Optimize Your Payable Days (DPO)

The final lever you can pull is your Days Payables Outstanding (DPO)—how long you take to pay your own suppliers. Now, unlike DIO and DSO, the goal here is to stretch this period out, but—and this is a big but—without torching those crucial supplier relationships.

The most straightforward way to optimize DPO is through good old-fashioned negotiation. When you're a reliable, consistent customer, you have some leverage. Have a frank conversation with your key suppliers about extending your payment terms from 30 days to 45 or even 60.

Frame it as a win-win. Explain that better terms for you mean a healthier cash flow, which allows you to place larger, more consistent orders with them.

You can also use B2B payment tools to your advantage. Some platforms allow you to pay your suppliers right away (keeping them happy) while giving you extended terms to pay the platform back. This gives your business valuable breathing room. It’s all about finding that sweet spot that supports your cash flow without putting your supply chain at risk.

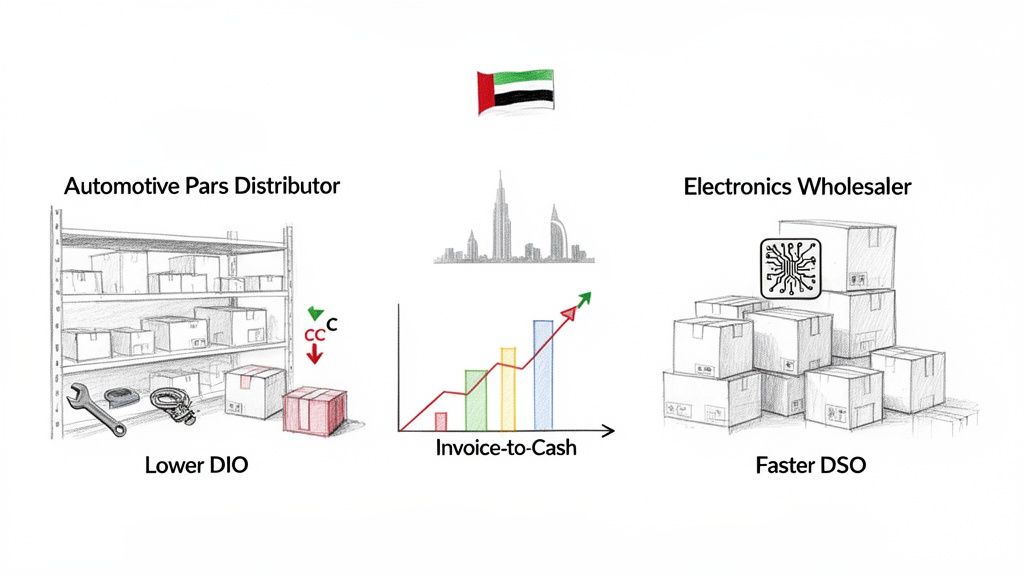

How UAE Businesses Are Winning With CCC Optimization

It’s one thing to talk about strategies in theory, but seeing them in action is where the power of optimizing the cash conversion cycle really comes alive. All across the UAE, businesses are turning these concepts into real-world success stories, proving that smart cash flow management is a potent engine for growth.

Let's dive into a couple of real-life examples of local businesses that transformed their operations simply by getting a handle on their CCC. These stories show that with the right approach and the right tools, any business can unlock its trapped working capital.

Case Study: An Automotive Parts Distributor

Picture an automotive parts distributor in Dubai facing a classic CCC squeeze. Their warehouse was packed with expensive inventory (a high DIO), and on top of that, they were often waiting up to 90 days for payments from workshops and dealers (a high DSO). This created a constant cash crunch, making it tough to restock popular items or even pay their own suppliers.

Their first move was to tackle the inventory beast. By digging into their sales data, they figured out which parts were flying off the shelves and which were just gathering dust. They immediately adjusted their ordering to focus on high-demand items and cut back on slower-moving products. Just like that, their DIO started to drop, freeing up cash.

Next, they went after their long payment cycles. Instead of just chasing late payments, they started offering their dealers more flexible payment options through a fintech platform. This was a win-win: workshops could get the parts they needed right away, and the distributor got paid much, much faster.

The results were impressive:

- Reduced DIO: Better forecasting and stock management cut down how long parts sat on shelves.

- Lowered DSO: Offering flexible payment terms through a partner drastically shortened the invoice-to-cash window.

- Increased Sales: With their own cash flow less strained, workshops started placing larger and more frequent orders.

By shortening their cash conversion cycle, the distributor didn't just solve an immediate cash flow headache; they actually fueled significant sales growth.

Case Study: An Electronics Wholesaler

Now, let's look at an electronics wholesaler supplying major retail chains. Business was booming, but their success was creating a new kind of problem. The big retailers they supplied had long payment terms, sometimes stretching out to a painful 120 days. This created a huge cash flow gap, making it nearly impossible to fund the massive purchase orders needed to keep up with demand.

Their DSO was so high it was putting the entire operation at risk, even though the company was profitable on paper. They desperately needed a way to bridge the gap between shipping the goods and actually getting paid.

The solution? Invoice discounting. By partnering with a platform like Comfi, they could upload their approved invoices from the big retailers and get the cash almost instantly. It completely transformed their cash flow overnight.

Instead of waiting months for their money, the wholesaler could now access their revenue within 24 hours. This allowed them to immediately reinvest in new inventory, pay their international suppliers on time, and confidently say "yes" to even the largest orders from retailers.

This strategic move was a game-changer. It allowed them to unlock their working capital, take on new retail clients without fearing a cash shortage, and totally simplify their collections process. By zeroing in on just one piece of their cash conversion cycle—the DSO—they stabilized their finances and paved the way for serious growth. Many businesses are now exploring similar tactics, and you can learn more about how Comfi’s B2B Buy Now, Pay Later solution enhances cash flow for businesses in the UAE.

The Road to Smarter Growth is Paved with Cash

Mastering your cash conversion cycle isn't a destination; it's a journey of constant learning and tweaking. We've seen that the CCC is much more than a number on a spreadsheet. Think of it as the pulse of your business—a vital sign that tells you how efficiently you're turning your investments into cash you can actually use.

By getting a handle on the formula, appreciating why a shorter cycle is better, and putting the strategies we've talked about into practice, you can grab the wheel of your company's financial health. The most important thing to remember is that you have the power to make your cash work smarter for you.

It’s All About Continuous Improvement

Optimizing your cash conversion cycle isn't a one-and-done project. It’s a commitment to being smarter about how your money moves. Keeping a close eye on your DIO, DSO, and DPO means you can catch small hiccups before they turn into full-blown cash flow emergencies. This kind of forward-thinking is what separates a fragile business from a resilient one.

The real prize here is building a business where cash flow is a reliable asset, not a constant source of anxiety. A shorter CCC gives you the breathing room to invest, innovate, and handle whatever the market throws at you.

For business owners across the MENA region, the way forward is clear. By embracing modern processes and using the right fintech tools, you can free up the working capital that’s currently locked away in your day-to-day operations.

Here are your final steps on this path to growth:

- Measure Religiously: Make calculating your CCC a standard part of your financial check-ups.

- Act with Confidence: Use what you learn to make sharp decisions about your inventory, how you collect payments, and when you pay your own bills.

- Embrace Modern Tools: Look into platforms that can automate and speed up your cash flow, getting rid of manual headaches and accelerating your entire cycle.

Taking these principles to heart will help you build a stronger, more agile, and ultimately more successful company.

Your Top Questions About The Cash Conversion Cycle, Answered

Let's tackle some of the most common questions that business owners and finance managers ask about the cash conversion cycle. I’ll give you the straight, practical answers you need.

What’s A Good Cash Conversion Cycle For A Small Business?

Honestly, there’s no single magic number. What’s considered “good” really depends on your industry. A neighborhood grocery store selling produce daily will have a completely different target CCC than a B2B company that builds custom machinery.

The real goal here is continuous improvement. If you can consistently shorten your CCC, you're winning. That's the best sign that your operations are getting leaner and more efficient.

Can My Cash Conversion Cycle Be Negative?

Absolutely, and it's an incredible position to be in. A negative CCC means you're getting paid by customers before you have to pay your own suppliers.

You see this a lot in e-commerce or subscription-based businesses where customers pay upfront.

When you achieve a negative CCC, your suppliers are essentially funding your day-to-day operations and growth. It's a massive competitive advantage.

How Often Should I Be Calculating My CCC?

For most businesses, calculating your CCC at least quarterly is a solid practice. It lines up perfectly with your regular financial reporting and gives you a consistent check-up on your cash flow health.

But if you're in a fast-paced industry or your business is growing quickly, switching to a monthly calculation is a smart move. It gives you sharper, more immediate insights. Calculating it regularly helps you catch trends and spot small issues before they snowball into major problems. Staying on top of this number is all about keeping a healthy financial rhythm.

By getting a handle on your cash conversion cycle, you can unlock serious growth potential. Comfi helps businesses do exactly that by making payments smoother and freeing up cash flow. Find out how we can help at https://comfi.ai.

Related Reading

- How Can MENA SMEs Master Working Capital?

- Staffing Agency Payroll Financing UAE: Boost Cash Flow 2026

- SME Cash Flow Management: A Guide for MENA Businesses

- Improve Working Capital for UAE IT Services Business

Ready to improve your business cash flow? Get started with Comfi today.