SME Cash Flow Management: A Guide for MENA Businesses

You're probably familiar with this pattern. Payroll is due this week, a supplier wants payment before releasing the next shipment, and your biggest customer says the invoice will clear “soon”. On paper, the business is profitable. In the bank account, it doesn't feel that way.

That gap is where most SME stress lives. Not in the P&L. In timing.

In MENA, that timing problem is rarely a one-off issue. It's built into how many businesses trade. Buyers want longer terms. Suppliers want faster payment. Stock has to be bought before it's sold. Compliance checks add another layer of delay. Good SME cash flow management is what keeps that pressure from turning into disruption.

Why Cash Flow Is the Lifeblood of Your MENA Business

A business can show healthy sales and still run into trouble if cash arrives too slowly. That's why cash flow isn't an accounting side topic. It's the operating heartbeat of the company.

In the UAE, this pressure is widespread. A CICM study reported that 82% of SMEs had encountered cash-flow difficulties, and one in three SME leaders said they did not fully understand cash flow despite those problems, according to the CICM report on SME cash-flow difficulties. That tells you two things at once. First, this problem is common. Second, many owners are still managing it by instinct rather than by system.

Why timing matters more than profit

Most SME owners already know their gross margin. Fewer know exactly when cash will land, when major outflows hit, and which customers consistently pay late.

That's where businesses get caught. You pay rent, salaries, freight, customs, VAT-related obligations, and suppliers on real dates. Customers pay on expected dates, revised dates, or sometimes only after several reminders. The difference between those two calendars is your risk.

A few common examples make this clear:

- A distributor wins more orders but needs to buy inventory upfront, so growth creates strain instead of relief.

- A wholesaler offers generous buyer terms to stay competitive, then discovers collections are too slow to support the next purchase cycle.

- An automotive trader closes deals but has cash tied up in vehicles sitting in stock for months.

Practical rule: Profit tells you whether the business model works. Cash flow tells you whether the business can keep operating long enough to benefit from it.

Why monthly review isn't enough

Many SMEs still review cash at month-end. That's too slow for a business with weekly supplier demands and customer slippage.

Cash management works better when finance teams monitor inflows and outflows frequently, update forecasts often, and treat receivables discipline as an operating function, not a back-office chore. In this region, that isn't over-management. It's basic survival.

If your cash position feels unclear most of the time, that doesn't mean your business is weak. It usually means your visibility is weak. Fix that first, and better decisions follow.

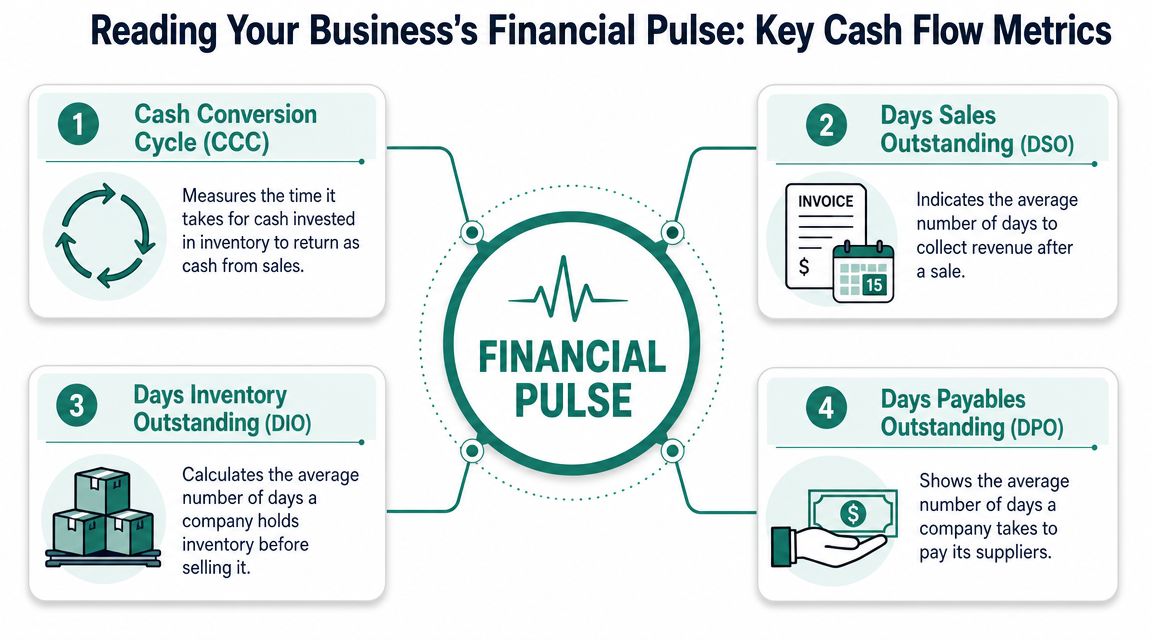

How to Read Your Business's Financial Pulse

If you want to improve cash flow, stop looking only at the bank balance. A bank balance is a snapshot. You need the moving parts behind it.

Four metrics tell most of the story. You don't need a finance degree to use them. You just need to know what each one reveals.

Cash Conversion Cycle

Cash Conversion Cycle, or CCC, measures how long cash stays tied up in operations before it returns through customer payments.

Simple formula: DIO + DSO - DPO

Think of it as the full trip your cash takes. You buy stock, hold it, sell it, invoice the customer, wait for payment, and only then get your cash back. The longer that cycle, the more pressure the business carries.

A long CCC usually points to one of three problems:

- Inventory is sitting too long

- Customers are paying too slowly

- Suppliers are being paid too quickly

Days Sales Outstanding

Days Sales Outstanding, or DSO, tells you how long your money is tied up with customers after you make a sale.

Simple formula: Accounts receivable divided by credit sales, multiplied over the period

This is one of the most useful metrics in SME cash flow management. High-performing finance teams in the UAE focus on shortening DSO because every extra day traps more capital in receivables and reduces liquidity, as discussed in this paper on cash flow management in SMEs during economic uncertainty.

If your DSO keeps drifting up, don't treat that as a reporting issue. It's an operating issue.

Issue invoices immediately. Then follow payment terms with the same discipline you use for supplier deadlines.

Days Inventory Outstanding

Days Inventory Outstanding, or DIO, shows how long inventory sits before it is sold.

Simple formula: Average inventory divided by cost of goods sold, multiplied over the period

For stock-heavy businesses, this number matters as much as sales. A warehouse can look like strength from the outside and behave like a cash trap on the inside.

Watch DIO closely if you sell vehicles, electronics, spare parts, consumer goods, or seasonal items. If stock sits too long, the business ends up carrying the cost long before it sees the cash.

Days Payables Outstanding and burn rate

Days Payables Outstanding, or DPO, measures how long you take to pay suppliers.

Simple formula: Accounts payable divided by supplier purchases, multiplied over the period

A longer DPO can support liquidity, but only if supplier relationships stay healthy. Stretching payables without agreement usually creates more damage later.

Burn rate is simpler. It tells you how fast the business is consuming cash. For profitable SMEs, this still matters when collections slow or stock buying rises.

Simple formula: Cash outflows minus cash inflows over a period

Use these metrics together, not separately:

- High DSO means collections are slow

- High DIO means stock is absorbing cash

- Low DPO may mean you're paying suppliers before customers pay you

- Negative burn trend means your buffer is shrinking

When owners say, “Cash disappears even though sales are fine,” one of these metrics usually explains why.

Forecasting Your Cash Flow Without a Crystal Ball

Many owners avoid forecasting because they assume it requires a complicated model. It doesn't. For most SMEs, a simple direct cash forecast is more useful than a polished spreadsheet no one updates.

The easiest way to think about it is this. A direct forecast works like a household budget. You list expected cash in and expected cash out by week. An indirect forecast is more like tracking how your overall financial position changes through accounting adjustments. Both have value, but the direct method is usually the better operating tool for an SME.

Use the direct method first

A direct forecast answers practical questions fast:

- What cash is expected to come in this week?

- What must go out this week?

- Where is the shortfall likely to appear?

- Can the business delay, accelerate, or restructure anything before that date?

If your team already has sales invoices, supplier due dates, payroll dates, rent, loan repayments, and tax-related payment dates, you have enough to start.

Build it for 13 weeks if possible, but don't get stuck on format. The discipline matters more than the template.

What to include in a usable forecast

A useful weekly forecast should include:

- Confirmed inflows: Cash you reasonably expect from issued invoices and recurring revenue

- Likely inflows: Payments that may arrive, but need a probability check based on customer history

- Fixed outflows: Salaries, rent, utilities, committed supplier payments

- Variable outflows: Inventory purchases, marketing spend, logistics, discretionary expenses

- One-off items: Annual fees, deposits, equipment purchases, exceptional payments

The best forecasts are built from actual history, then updated as reality changes. If one customer always pays late, don't place their invoice in the “best case” column and hope for the best. Forecast behaviour, not intention.

Forecast decisions, not just numbers

A forecast is useful only if it changes behaviour. When you can see a tight week coming, you have options. You can bring collections forward, delay a non-essential purchase, split a supplier payment, reduce a stock order, or look at tools that accelerate cash conversion.

If you want a clearer handle on the operating mechanics behind that timing gap, this guide to cash conversion cycle management is worth reading alongside your forecast work.

A forecast should feel slightly uncomfortable. If it always looks smooth, the assumptions are probably too optimistic.

Practical Strategies to Unlock Trapped Working Capital

Most cash flow problems in SMEs come from cash getting stuck in three places. Receivables. Payables. Inventory. If you improve those three levers, cash starts moving again.

For SMEs in the MENA region, a major pressure point is bridging the gap between paying suppliers and collecting from buyers. Industry guidance notes that liquidity improves when accounts receivable are settled before accounts payable are due, and that extending supplier terms and improving collections can materially improve working capital, as outlined in this SME cash flow management guide.

Tighten receivables without annoying good customers

Receivables usually offer the fastest operational fix. Most SMEs don't have a sales problem here. They have a follow-up problem.

Start with the basics:

- Invoice immediately: Don't wait until week-end or month-end. Delayed invoicing delays collection.

- Set payment terms clearly: Put due dates, bank details, and reference instructions on every invoice.

- Automate reminders: Use scheduled reminders before due date, on due date, and after due date.

- Segment customers: Treat a reliable payer differently from a chronic late payer.

- Escalate early: If an invoice slips, act before it becomes an ageing report issue.

A small commercial change can also help. If buyers ask for longer terms, price that term into the deal instead of absorbing the cash cost.

Use payables as a planning tool

Payables are often mishandled in one of two ways. Some SMEs pay too early out of habit. Others pay too late and damage supplier trust.

The better approach is deliberate negotiation.

- Ask for matched terms: If buyers pay on longer cycles, align supplier terms where possible.

- Prioritise strategic suppliers: Protect the relationships that protect your stock flow.

- Split large payments when needed: Many suppliers will accept staged payments if you ask before the due date.

- Avoid surprise delays: Silence hurts credibility more than a structured conversation.

If you need a plain-English refresher on understanding working capital for businesses, that overview is useful for owners who want the operational view rather than an academic definition.

Attack excess inventory directly

Inventory ties up more cash than many owners realise. Sales teams often want “more stock for flexibility”. Finance teams know old stock behaves like frozen cash.

Control starts with visibility:

- Review SKU movement: Separate fast-moving items from slow movers.

- Set reorder points by actual sell-through: Don't reorder based on gut feel.

- Reduce vanity stock: If an item rarely moves, challenge why you're still carrying it.

- Link purchases to turnover thresholds: Restock when movement justifies it, not when the warehouse feels empty.

Slow-moving stock doesn't just occupy shelf space. It occupies tomorrow's supplier payment.

The businesses that manage working capital well usually aren't doing one heroic thing. They're making dozens of small, disciplined decisions that shorten the time between cash out and cash back in.

How MENA Fintech Tools Can Accelerate Your Cash Flow

Traditional cash flow advice often stops at “invoice faster” and “negotiate better terms”. That helps, but it doesn't fully solve the UAE and MENA reality of long B2B payment cycles, stock-heavy trade, and admin-heavy processes.

Modern fintech tools matter because they change timing. They help businesses free up cash already sitting inside invoices, purchase cycles, or inventory.

When invoices are the bottleneck

Consider a supplier that has delivered goods to a large buyer on agreed terms. The sale is real. The invoice is approved. The problem is waiting.

In that case, invoice discounting can convert that approved invoice into usable cash sooner. Instead of waiting through the full payment cycle, the supplier gets liquidity earlier and can keep buying stock, paying vendors, or covering operating costs without squeezing the business elsewhere.

This works best when the business is healthy but collections timing keeps creating strain. It's not a substitute for receivables discipline. It's a way to stop good sales from becoming bad cash flow.

When buyers need more time but suppliers need payment now

Now take a wholesaler selling to retailers that want flexibility on settlement. If the wholesaler insists on immediate payment, some orders may not happen. If it gives long terms to everyone without structure, cash flow suffers.

That's where B2B Buy Now, Pay Later can help. Buyers get time to pay. Suppliers can still move goods without waiting through the full cycle. Used properly, this supports order flow while reducing the tension between sales growth and liquidity.

One option in this market is Comfi, which supports products such as Invoice Discounting, Buy Now, Pay Later terms, and dealer-focused solutions through a digital workflow. For owners tracking how these tools fit into the wider market, this overview of fintech for modern business cash management gives helpful context.

When inventory is the real constraint

This is especially relevant in automotive and other inventory-heavy sectors. In the UAE, cash conversion can be constrained by stock that stays tied up for months. Operationally, businesses often address this with asset-backed or inventory-linked structures that release cash from in-stock vehicles so they can restock faster and avoid cash-flow pressure, as described in this article on small business cash flow management for inventory-heavy firms.

A dealer, for example, may have profitable vehicles sitting in the yard but limited room to acquire the next batch. The issue isn't lack of demand. It's that too much cash is immobilised in current stock.

The practical lesson is simple. If your bottleneck sits inside invoices or inventory, generic budgeting advice won't fully fix it. You need tools that accelerate conversion, not just reports that describe the delay.

Building a Resilient Cash Management System

One-off fixes help for a month or a quarter. A system keeps the business stable when buyer behaviour changes, costs rise, or stock cycles lengthen.

Resilient SME cash flow management rests on three things. Process, technology, and review discipline. If one is missing, the whole setup weakens.

Build process before software

Start with rules your team can realistically follow:

- Credit policy: Decide who gets terms, how much, and under what conditions.

- Invoice policy: Set a rule that invoices go out immediately after delivery or milestone completion.

- Collections policy: Define when reminders go out and who escalates overdue accounts.

- Purchasing policy: Require inventory and procurement decisions to reflect current cash position, not just sales ambition.

Many niche sectors need specialized routines. If you want a sector-specific example, this article on how to manage jewelry business cash flow is useful because it shows how stock discipline and purchasing decisions shape liquidity in a product-led business.

Use technology to reduce lag

Technology should remove delay, not add dashboards nobody uses.

The most useful stack usually includes invoicing, collections reminders, bank visibility, and weekly cash forecasting in one operating rhythm. If your team is still pulling figures from separate systems and reconciling by hand, cash decisions will always lag behind reality.

A broader look at treasury management for growing businesses can help finance leaders connect day-to-day cash control with a more structured operating model.

The strongest cash system is the one your team updates every week without fail.

Review weekly, not only monthly

A monthly finance meeting won't catch a customer delay that threatens next Tuesday's supplier payment.

Set a short weekly review. Look at cash on hand, expected receipts, upcoming outflows, ageing receivables, and any stock purchases that need approval. Keep it operational. This isn't a board presentation. It's a control routine.

Owners who do this consistently usually spot pressure earlier, negotiate better, and make fewer rushed decisions.

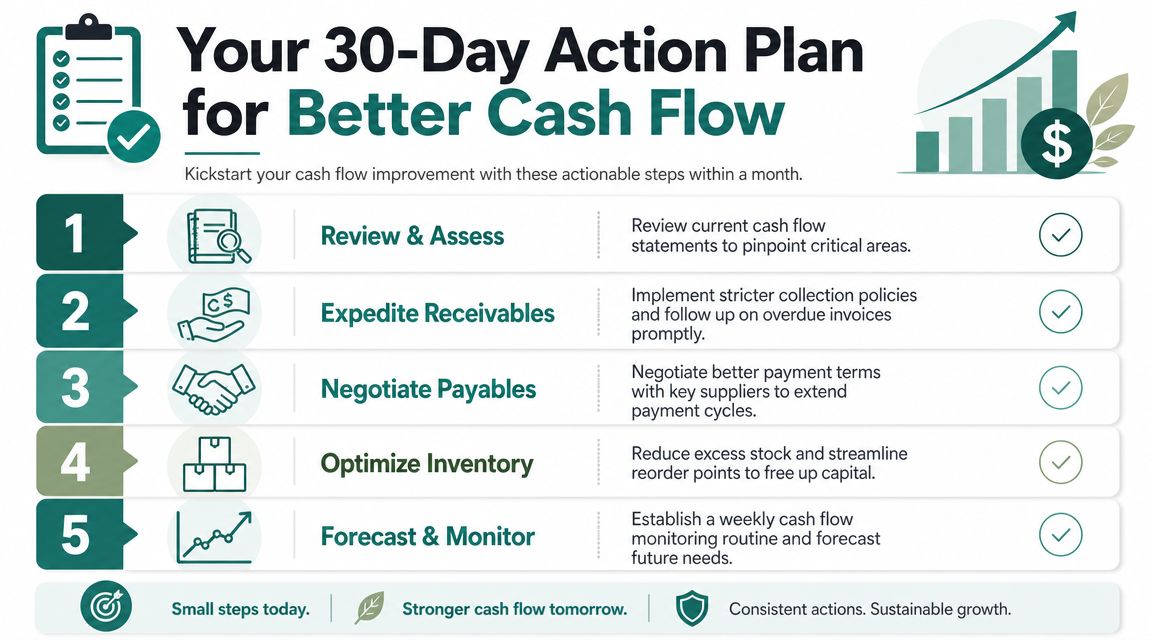

Your Action Plan for Better Cash Flow in 30 Days

You don't need to rebuild the whole finance function this month. You need a short list of actions that improve visibility and speed.

Week 1

- Calculate your key metrics: Work out DSO, DIO, DPO, and your cash conversion cycle.

- List all major cash dates: Include payroll, rent, supplier deadlines, and expected customer receipts.

- Identify your top problem area: Decide whether receivables, inventory, or payables is creating the biggest squeeze.

Week 2

- Build a weekly direct cash forecast: Use actual expected inflows and outflows, not optimistic guesses.

- Invoice faster: Remove any delay between delivery and billing.

- Set reminder rules: Schedule follow-ups before and after due dates.

Week 3

- Review customer terms: Tighten terms for slow payers and confirm disputes early.

- Review supplier terms: Ask key suppliers whether terms can be aligned more closely to your collection cycle.

- Check stock line by line: Flag slow-moving inventory and pause unnecessary replenishment.

Week 4

- Test a cash acceleration option: If approved invoices or inventory are tying up liquidity, assess whether a suitable digital tool can shorten the wait.

- Set a weekly cash meeting: Keep it short and focused on decisions.

- Write down your rules: Credit, invoicing, collections, and purchasing should not live only in your head.

Small changes done consistently usually beat big plans that never leave the spreadsheet.

If long payment cycles are slowing your business, Comfi is one option to explore for releasing cash tied up in invoices, buyer terms, or inventory through digital workflows designed for SMEs in MENA. The useful next step isn't to chase more sales blindly. It's to make sure the sales you already have convert into cash at the speed your business needs.

Related Reading

- How Can MENA SMEs Master Working Capital?

- Staffing Agency Payroll Financing UAE: Boost Cash Flow 2026

- Mastering SaaS Company Cash Flow UAE: 2026 Guide

- Improve Working Capital for UAE IT Services Business

Looking to improve your cash flow? Explore Comfi's Invoice Discounting solutions. Get started today.