What Is Accounts Receivable: Your 2026 Guide for UAE SMEs

With credit sales accounting for over 50% of B2B transactions in the Middle East, accounts receivable is indeed the lifeblood for any B2B business. It's the money your business has already earned, for goods or services delivered on credit, and it sits on your balance sheet as a current asset because you expect to turn it into cash within 12 months.

You can see why this matters if your sales look healthy but your bank balance doesn't. A wholesaler in Dubai might deliver stock this week, issue an invoice on 30, 60, or 90-day terms, and still struggle to pay suppliers before the customer settles. That gap between booked revenue and actual cash is where many SMEs get squeezed.

What Is Accounts Receivable and Why It Matters for SMEs

A simple way to answer the question what is accounts receivable is this. It's money customers owe your business after you've already delivered the product or completed the service.

If you sell on credit, you are effectively giving your customer time to pay. Until the money arrives, that invoice becomes part of your accounts receivable, often shortened to AR.

The sales versus cash problem

This confuses many business owners at first. They think, “We made the sale, so why are we short on cash?” The answer is timing.

Revenue can be recorded today. Cash may arrive much later.

That's why AR isn't just an accounting label. For SMEs in the MENA region, it's often one of the biggest moving parts in day-to-day liquidity. If too much cash is stuck in unpaid invoices, you may delay payroll, slow restocking, or turn down growth opportunities.

Practical rule: A sale on credit is not the same as cash in the bank.

Why SME owners should care

AR matters because it tells you how much of your near-term cash is still trapped with customers. The healthier your receivables process, the more predictable your business becomes.

A few examples make this clearer:

- A distributor ships stock to a retail chain: The goods are gone from the warehouse, but the cash hasn't arrived yet.

- A service firm completes a project: The team has done the work, but the invoice is still waiting in the customer's approval flow.

- An automotive supplier delivers parts on agreed terms: Sales rise, yet usable cash stays tight until collections catch up.

If you want a broader view of how collections and cash timing interact, this guide on payments and receivables helps connect AR to the rest of your cash cycle.

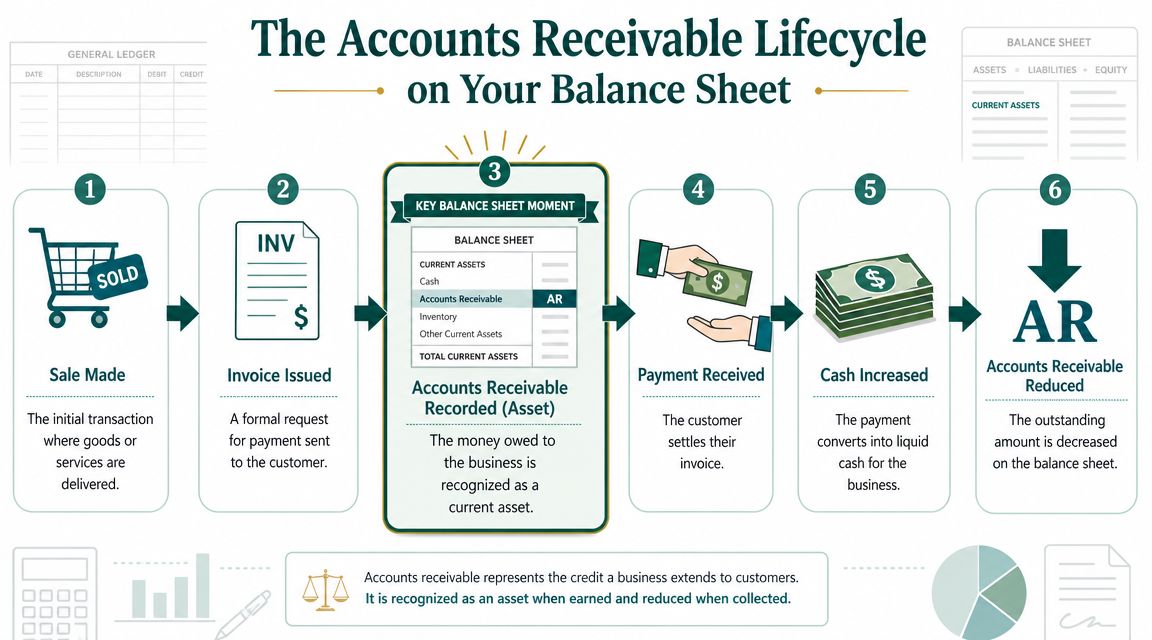

How Accounts Receivable Works on Your Balance Sheet

When you send an invoice after delivering goods or services, your business records an asset. Not cash yet, but a legal claim to cash.

That's why AR appears on the balance sheet as a current asset. In the UAE and GCC context, it's treated this way because it's expected to convert into cash within 12 months, as explained in SAP's guide to accounts receivable as a current asset.

Think of AR as frozen cash

The easiest analogy is frozen cash. The value is real, but you can't use it yet.

If your customer is reliable and pays on time, AR becomes cash later. If payment is delayed, disputed, or never collected, the asset becomes less useful than it first appeared.

Here's the lifecycle in plain language:

- You deliver goods or services

- You issue the invoice

- The invoice is recorded as accounts receivable

- The customer pays

- Cash increases

- Accounts receivable decreases

That sequence matters because your financial statements can look strong while cash remains tight. A large AR balance may reflect healthy sales. It may also signal that too much money is locked up outside your bank account.

Why balance sheet treatment matters in real life

Business owners often hear “asset” and assume “good”. That's only partly true.

AR supports working capital only when it is collectible. If customers delay payment, the number on the balance sheet overstates the cash you can deploy.

Sage describes AR as money a company expects to collect for goods or services already delivered but not yet paid for, and notes that this improves liquidity only if the receivables are collectible, as outlined in Sage's explanation of accounts receivable and collectibility.

A profitable month can still create stress if most of the profit is sitting inside unpaid invoices.

Accounts receivable versus accounts payable

Many owners mix up accounts receivable and accounts payable.

Use this shortcut:

- Accounts receivable: Money customers owe you

- Accounts payable: Money you owe suppliers

One is an incoming claim. The other is an outgoing obligation.

That difference shapes your cash planning. If receivables arrive after payables fall due, the timing mismatch creates pressure even when the business is technically profitable. That's one reason finance teams watch AR so closely in wholesale, distribution, and trade businesses.

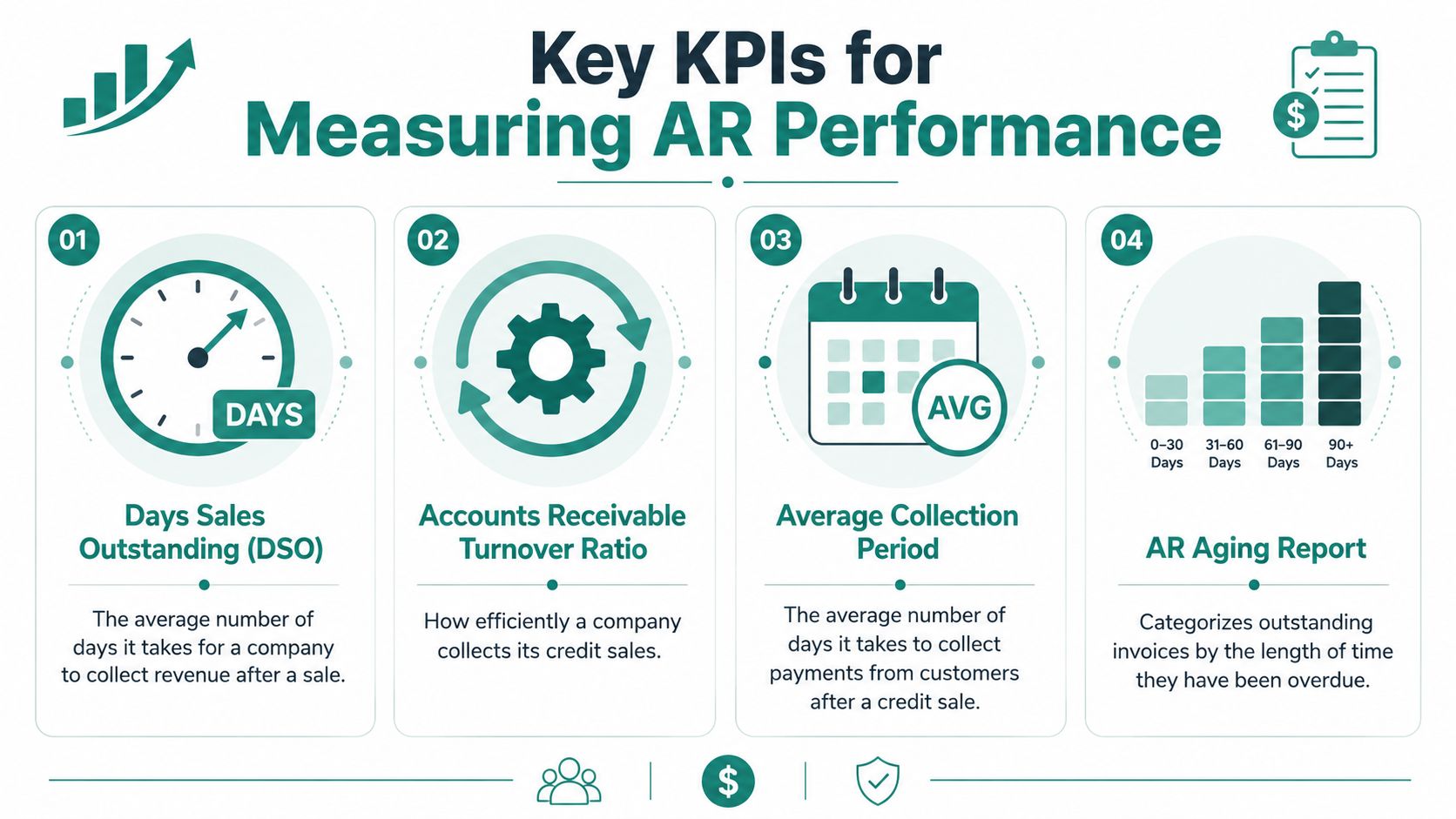

Measuring AR Performance with Key KPIs

You can't manage receivables by instinct alone. You need a small set of measures that tell you whether invoices are moving, stalling, or turning risky.

Start with your ageing report

An AR ageing report groups invoices by how long they've been outstanding. Typical buckets follow the logic of current, then progressively older overdue balances.

You don't need to be an accountant to use it well. You're looking for patterns.

- Current invoices: These are not yet due, or only recently issued.

- Recently overdue invoices: These need prompt follow-up before they become a habit.

- Older overdue invoices: These often signal a dispute, approval bottleneck, or customer stress.

- Repeated slow payers: These customers may need different terms or closer credit control.

If one major customer keeps appearing in the older buckets, that's not just an admin issue. It's a cash-flow warning.

DSO tells you how fast sales become cash

Days Sales Outstanding, or DSO, is one of the most useful AR metrics because it answers a practical question. On average, how long does it take you to collect after a sale?

PDCflow defines the formula as (AR ÷ Total Credit Sales) × Number of Days in its explanation of Days Sales Outstanding in AR management.

That formula matters because DSO turns a vague feeling into a timing measure. If DSO rises, more cash stays trapped in receivables for longer. For SMEs, even small increases can make payroll, supplier payments, and inventory purchases harder to fund.

A useful way to interpret DSO:

- Lower and stable: Collections are broadly keeping pace with sales.

- Rising gradually: Billing may be slow, terms may be too loose, or follow-up may be inconsistent.

- Spiking suddenly: Look for disputes, customer concentration, or operational errors.

If you want a deeper look at one efficiency metric related to collection performance, this explainer on the accounts receivable turnover ratio is a useful companion.

If your sales team celebrates growth while DSO quietly climbs, finance will feel the problem before anyone else does.

Don't ignore doubtful accounts

Some receivables won't turn into cash in full. That's why finance teams maintain an allowance for doubtful accounts.

This is a cautious estimate of invoices that may never be collected. SAP notes that net accounts receivable is the amount expected after deducting doubtful-account allowances, returns, and discounts. That idea is important because gross AR can look healthy while net AR gives a more realistic picture of expected cash.

For a business owner, the lesson is straightforward:

- Gross AR shows what customers owe on paper

- Net AR shows what you realistically expect to collect

That difference matters when you're planning purchases, hiring, or expansion. If you budget against gross receivables and collections disappoint, the shortfall hits fast.

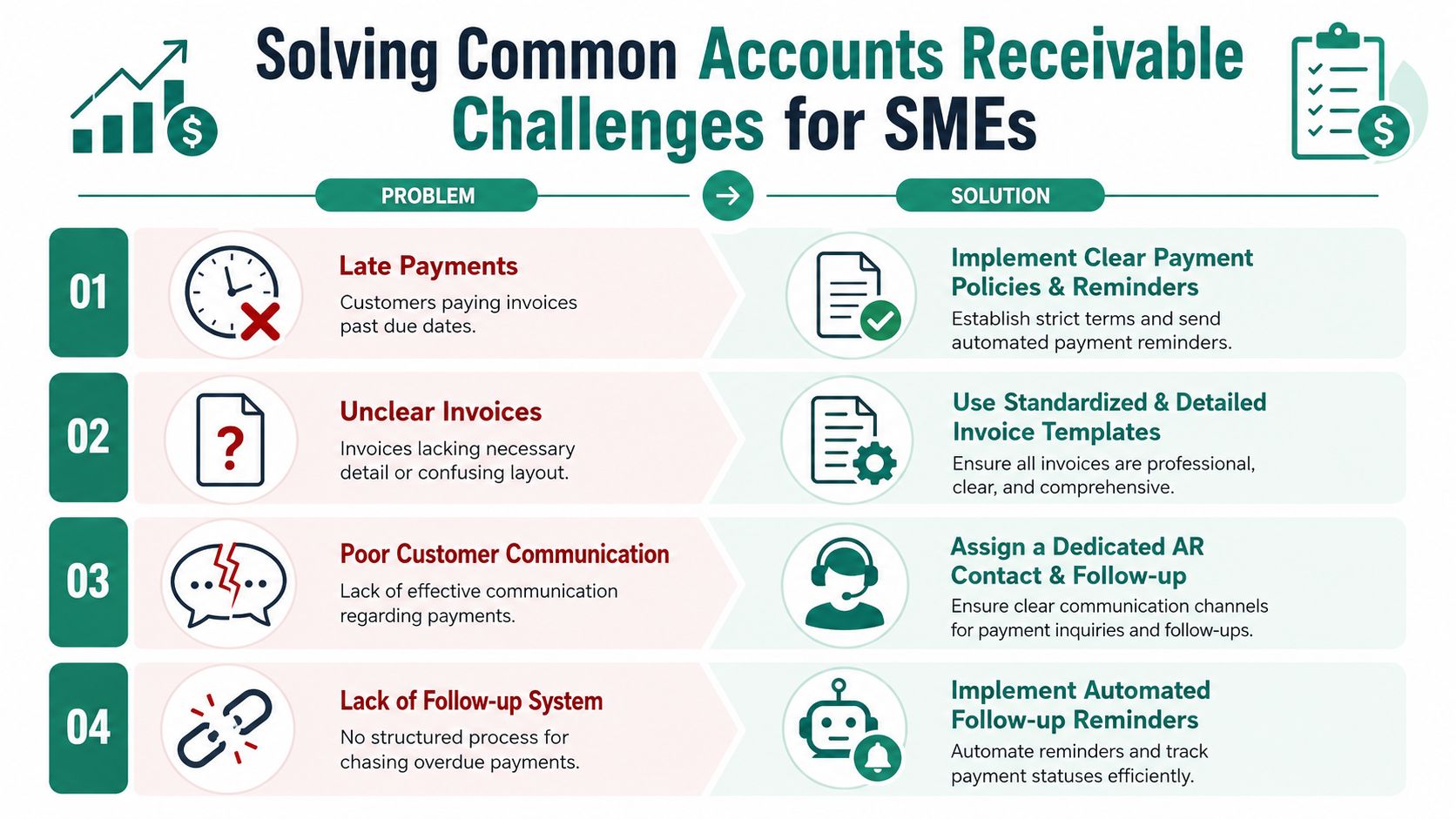

Solving Common Accounts Receivable Challenges

Most AR problems aren't mysterious. They usually come from a small set of repeated issues. Weak terms, poor invoice quality, inconsistent follow-up, and slow dispute handling cause more damage than most owners realise.

For UAE SMEs, this is especially practical. The US Chamber's discussion of UAE payment practices notes that delayed payments are a persistent challenge and that many firms carry overdue receivables, which is why AR becomes less about definition and more about trapped cash, as described in this piece on UAE payment practices and accounts receivable pressure.

Late payments

This is the most visible AR headache. The invoice is approved, the customer relationship looks fine, but payment drifts beyond the due date.

The fix is usually operational, not dramatic.

- Set terms clearly: Put payment terms, due dates, and required reference details on every quotation, contract, and invoice.

- Invoice immediately: Don't wait until week-end or month-end if the goods are already delivered.

- Follow up consistently: A reminder schedule works better than ad hoc chasing.

Unclear or disputed invoices

A customer won't pay quickly if the invoice is missing a purchase order number, has the wrong quantity, or doesn't match what was delivered.

This slows collections because finance teams at your customer's side often stop the invoice until someone clarifies it.

Try this checklist:

- Use standard templates: Keep line items, tax details, due dates, and contact details consistent.

- Match commercial documents: Ensure the invoice aligns with the PO, delivery note, and agreed pricing.

- Resolve disputes fast: Assign ownership so issues don't sit between sales, operations, and finance.

Clean invoicing shortens collection time before collections even begin.

Manual tracking and weak communication

Some businesses still track receivables with scattered spreadsheets, inboxes, and informal WhatsApp follow-ups. That works for a while, then breaks when invoice volume grows.

A stronger process usually includes:

- One AR owner: Customers should know exactly who to contact about balances and remittances.

- A shared system: Use accounting software or an ERP view that shows invoice status, due dates, and notes in one place.

- Documented follow-up: Keep a record of promises to pay, dispute reasons, and next actions.

There's also a basic but often missed operational risk here. Payment reminders, invoice approvals, and remittance advice often move through email. If those messages are spoofed, blocked, or misdirected, collections slow down and fraud risk rises. Teams reviewing their receivables process should also look at top email protection solutions to reduce avoidable payment communication issues.

No structured escalation path

Many SMEs chase overdue payments the same way whether an invoice is one day late or seriously overdue. That creates confusion internally and sends mixed signals externally.

A better approach is to define stages:

- Pre-due reminder

- Due-date confirmation

- First overdue follow-up

- Escalation to account manager or finance lead

- Credit hold or reviszed terms for repeat cases

That structure doesn't have to be aggressive. It just needs to be clear and repeatable.

How to Turn Your Invoices into Immediate Cash

Waiting for customers to pay is common. It isn't your only option.

In the UAE, AR management is moving beyond manual collection alone. HighRadius notes that digital invoice workflows, ERP integration, and alternative tools such as invoice financing are becoming more important for businesses that want to reduce DSO and free up cash without adding traditional bank debt, as discussed in this overview of digitized accounts receivable and alternative cash-flow tools.

Option one is invoice discounting

Invoice discounting allows a business to release cash tied up in approved invoices instead of waiting for the full customer payment cycle to run its course.

This is useful when:

- You sell on extended terms: Common in wholesale, trade, and distribution.

- You need to restock quickly: Cash arrives sooner, so purchasing decisions don't wait on collections.

- You want smoother forecasting: Receipts become less dependent on exact customer payment timing.

If you want a practical look at how this works in market context, this guide to invoice discounting in the UAE explains the mechanics in more detail.

Another route is offering flexible buyer terms

Some businesses improve cash flow by letting buyers pay over time while the seller receives payment earlier through a third-party structure. In B2B, this can support larger orders and reduce friction at the point of sale.

It's especially relevant when customers ask for 30, 60, or 90-day terms but suppliers can't afford to wait.

The business benefit is simple:

- The buyer gets breathing room

- The seller avoids long collection delays

- Operations become easier to plan

Automotive businesses have a related challenge

In automotive trade, cash is often tied up not only in invoices but also in stock. Dealers may hold vehicles while waiting for the right buyer and settlement timing.

That's why inventory-linked solutions can matter alongside receivables tools. The goal is the same in practical terms. Turn an illiquid business asset into usable cash sooner so you can keep moving.

Where digital tools fit

The old model of AR depended heavily on manual reminders and reactive chasing. The newer model combines process discipline with digital workflows.

A strong setup usually includes:

- Fast invoice issuance

- System visibility into due dates and approvals

- Automated reminders

- Clear records of customer responses

- An option to access cash from eligible invoices

One example in this space is Comfi, which offers tools including invoice discounting, Buy Now, Pay Later terms, and automotive dealer solutions designed to help businesses free up cash tied up in invoices or stock. The practical attraction for SMEs is speed and predictability, especially when long customer terms would otherwise slow reinvestment.

The real shift is mental. AR doesn't have to be a waiting room. It can be managed as an active cash-flow lever.

Taking Control of Your Business Cash Flow

Once you understand what accounts receivable really is, the question changes. It's no longer “Why is this on my balance sheet?” It becomes “How quickly can I turn this into usable cash?”

That's the difference between accounting awareness and financial control.

A simple plan to act on

Start with three moves.

- Measure the position: Review your ageing report, overdue balances, and DSO trend.

- Fix the process: Tighten invoicing, clarify terms, and create a consistent collection rhythm.

- Reduce the waiting: Where it makes sense, use digital tools or invoice-based solutions to make cash available sooner.

For many SMEs in MENA, AR is one of the largest assets on paper and one of the biggest sources of stress in practice. When you manage it actively, it stops being a static line item and starts supporting day-to-day decisions.

Good AR management doesn't just protect cash. It gives you options. You can restock earlier, negotiate from a stronger position, and take on growth without being held back by payment delays.

If unpaid invoices are slowing your business, Comfi's invoice discounting is one option to explore. It helps SMEs in MENA access cash tied up in invoices within hours through a seamless digital process, so businesses can shorten the wait between making a sale and using the proceeds to operate and grow.

Related Reading

- 8 Best Accounts Receivable Software for SMEs in 2026

- Inventory Financing vs Invoice Discounting for UAE SMEs

- A Guide to Food and Beverage Invoice Financing in the Middle East for 2026

Ready to improve your business cash flow? Get started with Comfi today.