UAE Business Expansion to Saudi Arabia Finance

Saudi Arabia is usually the first market UAE owners look at once the home market starts feeling proven. The logic is obvious. Bigger buyer base, larger projects, stronger industrial demand, and a policy environment that is openly pushing private-sector growth.

The mistake is thinking expansion fails at the front end. It usually doesn't. Most UAE companies can generate interest in Saudi Arabia faster than they expect. What slows them down is finance. A business that is healthy in Dubai can feel strained the moment it starts shipping into Riyadh, Jeddah, or Dammam on longer terms, through new distributors, with different approval chains and a more formal operating setup.

That's why UAE business expansion to Saudi Arabia finance needs to be treated as an operating discipline, not an afterthought. If you structure collections, local setup, pricing, tax registration, and receivables strategy properly, the Saudi move can become profitable. If you don't, growth starts eating cash.

The Saudi Prize and Its Hidden Financial Hurdles

A familiar Saudi expansion story starts with a strong first order. A UAE company wins a customer in Riyadh, offers 60 to 90 day terms to secure the account, ships product, and records the sale. Revenue looks healthy. Cash gets tighter. Salaries, stock purchases, freight, VAT, and supplier obligations still need funding long before the customer pays.

That gap catches profitable companies off guard.

The actual strain is rarely demand. It is the time lag between spending cash and collecting it. In Saudi expansion, that lag often widens at the same moment operating costs rise. New registrations, local staffing, warehousing, distributor support, travel, and compliance work all arrive early. Customer cash usually does not.

The commercial prize is real, and the UAE-Saudi corridor is already substantial. What operators need to see clearly is that growth into the Kingdom often behaves like a working capital test before it becomes a profit story. Sales can improve while liquidity weakens.

I have seen this play out with wholesalers, service firms, and industrial suppliers alike. The pattern is consistent. The UAE parent business funds the Saudi push from its own balance sheet, assumes receivables will settle roughly in line with the UAE, then finds that approval chains, buyer onboarding, and payment processing stretch the cycle far longer than expected. A business can be right on strategy and still run into a cash squeeze.

Practical rule: Judge Saudi expansion by cash conversion speed, not pipeline volume.

The companies that handle this well usually get three things right early:

- They build a cash-flow model around slower collections. Sales forecasts alone are not enough.

- They separate one-off entry costs from ongoing trading pressure. Licence fees and setup costs hurt once. Receivables, inventory, and supplier terms shape the business every month.

- They put finance operations into the entry plan from day one. Banking access, invoicing discipline, credit control, and local payment processes need an owner before the first large order ships.

Saudi expansion rewards disciplined operators. The winners are not always the companies with the biggest budgets. They are usually the ones that treat expansion for what it is: a working capital exercise with a sales opportunity attached.

Understanding the KSA Financial Landscape

Saudi Arabia isn't just a larger version of the UAE. It's a different financial environment, with its own regulators, documentation culture, payment behaviour, and operating rhythm.

Saudi Arabia's SME agenda is openly expansionary. Industry commentary citing government planning says SMEs are targeted to reach 35% of GDP by the end of the decade under Vision 2030, as noted in this overview of the economy of Saudi Arabia. For a UAE company entering the kingdom, that target matters because it signals continued demand for structured trade terms, receivables tools, and practical support around commercial growth.

The regulators that shape daily finance

Two names matter quickly once you move from planning to execution.

SAMA sits at the centre of the banking and financial system. In practical terms, your treasury team feels its influence through banking processes, payment infrastructure, account opening expectations, and the seriousness around licensed activity.

ZATCA affects the tax and documentation side of the business. That touches invoicing, VAT treatment, import and customs interactions where relevant, and the records you need to keep if you want collections and accounting to run cleanly.

A UAE finance team that is used to fast commercial execution can get frustrated here. Saudi processes often expect more supporting paperwork and a more formal sequence.

Saudi isn't difficult because demand is weak. It's difficult because informal shortcuts that sometimes work elsewhere tend to break once tax, banking, and local registration start interacting.

What catches UAE finance teams off guard

The first issue is payment behaviour. Even when a buyer is good, internal approvals may move through procurement, finance, and business units in a way that stretches collection timing.

The second is banking culture. Local banking relationships are not just administrative. They support local payroll, supplier payments, receipts, and credibility with counterparties. If you try to run everything remotely from the UAE, friction builds fast.

The third is reporting discipline. Saudi counterparties often expect formal documents that match legal entity status, tax registration, and contractual terms. If your contract says one thing, your invoice says another, and your registration status is still pending, your receivable can get stuck for reasons that have nothing to do with customer intent.

The mindset shift that works

Use a Saudi-specific lens before you sell aggressively.

- Map the order-to-cash process: who approves, who receives goods, who validates invoices, and who releases payment.

- Check documentation early: contracts, tax details, entity names, and invoice formatting need to line up.

- Build local finance capability: even a lean setup needs someone accountable for collections, bank coordination, and compliance follow-through.

A UAE team that respects these differences usually adapts well. A team that assumes Saudi buyers will behave like UAE buyers often spends the first year fixing preventable cash problems.

Navigating Your Saudi Market Entry and Banking Setup

Saudi market entry works best when finance leads the sequence. If sales gets ahead of the legal and banking setup, the business can win orders it isn't yet structured to service properly.

The practical framework is clear. The most reliable method is to treat entry as a regulated operating model. The sequence is set out in Hawksford's guide to growing and expanding a UAE business into Saudi Arabia: establish a Saudi legal presence, secure Commercial Registration, obtain sector-specific licences, complete ZATCA tax and VAT registration, and set up local premises if needed.

What each step means financially

Legal presence first.

This determines how you contract, invoice, hire, and open accounts. Finance teams should confirm shareholder documents, constitutional documents, and signatory authority before anything else.

Commercial Registration next.

Without CR, too many downstream tasks stall. Vendors may hesitate, banks may not proceed, and local commercial credibility remains weak.

Licences after that.

If your activity touches regulated areas, delays here can affect launch timing more than expected. Don't treat licensing as a paperwork footnote.

Tax and VAT registration.

This changes how invoices are issued and how finance books local activity. The sooner this is aligned, the fewer clean-up exercises you'll face later.

Premises and employee setup.

Even a modest local footprint can matter because banks, regulators, and customers often want to see substance, not just intent.

Why local banking matters more than most firms expect

A Saudi bank account isn't just a convenience. It's part of the operating backbone.

It helps with:

- Collections efficiency: local buyers often pay more smoothly into local accounts.

- Payroll and supplier payments: cross-border workarounds become messy fast.

- Treasury visibility: you need to see Saudi cash movement as its own stream.

- Compliance confidence: counterparties take the setup more seriously when it's complete.

If your team is also reviewing how to structure banking for founders, executives, or incoming staff around the UAE side of operations, this guide to expat bank accounts in Dubai is a useful reference point for comparing practical account-opening considerations.

Common setup mistakes

The most expensive mistakes are rarely dramatic. They're usually sequencing errors.

- Selling before paperwork is aligned: revenue lands before the business can invoice and collect cleanly.

- Using UAE document assumptions: Saudi counterparties often ask for a deeper paper trail.

- Treating bank onboarding as quick admin: it can take coordination, clarification, and patience.

Open the entity and the account structure before you scale the pipeline. In Saudi, finance setup isn't support work. It's market access.

Funding Your Initial Expansion into the Kingdom

Initial expansion money and day-to-day trading cash are not the same thing. Many SMEs blend them together, and that's where pressure starts.

The first bucket is setup capital. That covers entity formation, registrations, licences, advisers, hiring, premises, systems, and launch costs. Traditional answers here are usually straightforward: shareholder equity, retained earnings, or a bank facility. Each can work, but each has trade-offs.

Equity gives breathing room, but owners may not want to dilute or tie up capital in admin-heavy setup spend. Bank lines can help, but they often move more slowly than commercial opportunities. They may also come with collateral expectations or covenant logic that doesn't fit a fast-moving expansion.

The second bucket is operating cash. That's the money tied up once trade begins. At this point, many plans become unrealistic, because the business funds market entry but forgets to fund the gap between shipment and payment.

An HSBC survey of UAE businesses planning Saudi investment found that 90% plan to increase investment in Saudi Arabia over the next five years, with project financing cited as the top attraction. The useful takeaway isn't just the level of interest. It's that companies need different forms of capital for different stages of expansion.

What the main funding routes actually solve

- Shareholder funds: good for launch control, but they can get consumed by setup and initial stock.

- Bank facilities: useful when documentation, collateral, and timing all line up.

- Strategic partners or investors: potentially helpful, but not always suitable for ordinary trading needs.

That's why finance teams should separate one-time launch spend from recurring cash-cycle pressure.

The gap most SMEs need to plan for

A Saudi expansion usually strains cash after the first orders arrive, not before. You've already paid to source, ship, and service the account, but the receivable hasn't converted into cash yet.

That's the point where agile, transaction-linked tools start making more sense than broad corporate funding alone. If you're assessing different ways to structure that capital stack, this guide on how to get finance for business is a useful starting point.

The practical test is simple. Ask whether a funding option helps you enter Saudi Arabia, or whether it helps you trade sustainably once you're there. Those are two different jobs.

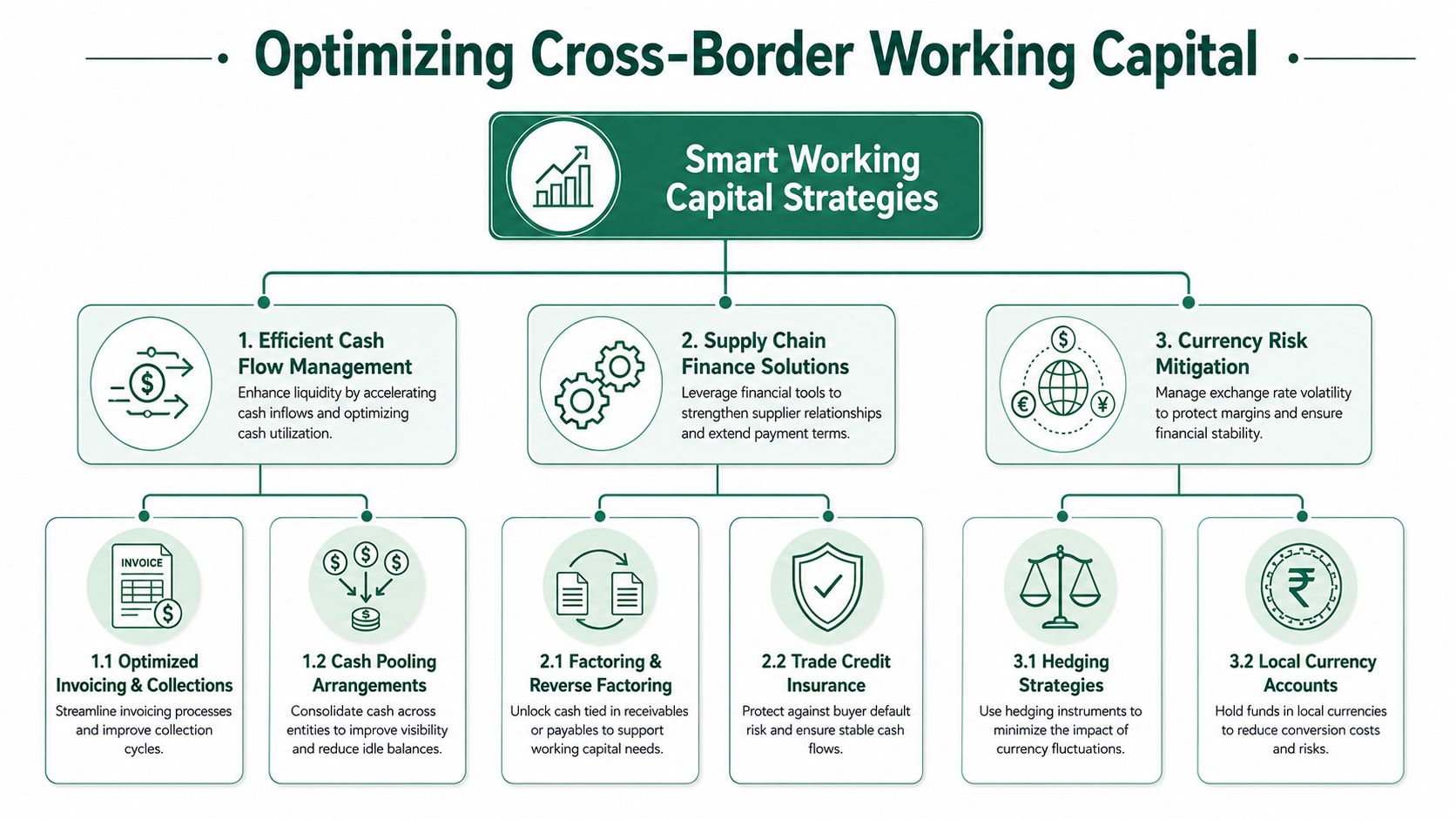

Smart Working Capital Strategies for Cross-Border Growth

Profitable expansion is often won or lost based on these considerations. Sales into Saudi Arabia can grow quickly, but receivables, inventory, and payment terms often grow faster than cash.

Think of working capital like oxygen in a warehouse. You don't notice it when there's enough. The moment it tightens, everything slows at once. Purchase orders become harder to fulfil, supplier relationships strain, and the sales team starts avoiding good deals because the business can't carry the terms.

Invoice discounting for long receivable cycles

Invoice discounting is one of the cleanest tools for cross-border trade when the sale is good but the payment clock is slow.

The logic is simple. Instead of waiting for the full customer payment cycle to end, the business frees up cash from approved invoices and recycles it into fresh stock, payroll, and fulfilment.

This works especially well when:

- The buyer is solid but pays on extended terms

- The supplier needs to restock before the invoice matures

- The expansion plan depends on repeating orders, not one-off transactions

Done properly, invoice discounting turns receivables from a blocked asset into a usable operating resource.

B2B BNPL for commercial flexibility

Sometimes the issue isn't your own payment timing. It's the buyer's.

A Saudi buyer may want stock now but may also need 30, 60, or 90 day terms to fit internal procurement or resale cycles. If the UAE supplier carries that burden directly, cash gets squeezed. If the supplier refuses terms, the deal may stall.

That's where B2B Buy Now, Pay Later can help. It allows the seller to offer attractive terms without forcing the entire cash burden onto the balance sheet.

One option in this category is Comfi, which supports Invoice Discounting, Buy Now, Pay Later, and Automotive Dealer Financing for SMEs across MENA. In practice, tools like these are useful when a business needs to obtain cash from invoices, offer structured buyer terms, or keep inventory moving without tying up operating liquidity. For a broader framework on regional planning, this guide on GCC expansion working capital for UAE businesses is worth reviewing.

Field note: The best use of payment-term tools isn't to rescue weak deals. It's to support good customers whose buying cycle is longer than your cash cycle.

Dealer financing for inventory-heavy sectors

Automotive, electronics, appliances, and other inventory-led sectors have a specific problem. Cash sits in stock before it sits in receivables.

Dealer financing helps businesses free up capital tied up in inventory so they can keep rotating stock instead of watching it absorb balance-sheet capacity. This matters a lot in sectors where missed replenishment means missed margin.

A distributor entering Saudi Arabia should ask two questions early:

- How much cash will sit in inventory before sale?

- How quickly can that stock be converted back into usable funds?

If the answer to the second question is “not quickly”, inventory needs as much attention as receivables.

A simple cross-border working capital playbook

Good practice here is usually operational, not theoretical.

- Match tools to bottlenecks: use receivables solutions for invoice delay, inventory solutions for stock-heavy models, and term solutions when buyers need flexibility.

- Underwrite around the operational trade cycle: not just the nominal invoice date. Look at delivery, acceptance, invoice approval, and payment release.

- Build collections discipline early: cash flow improves when finance teams chase documentation issues before invoices age.

- Keep treasury close to sales: commercial teams often offer terms quickly. Finance needs to shape what “acceptable terms” means in practice.

For teams trying to quantify how staffing structures and outsourced support affect liquidity management, PEO Metrics' working capital analysis is a useful external reference.

The broad principle is simple. Don't let growth get trapped in receivables and stock. If Saudi expansion is working commercially, your finance model should help that growth circulate, not sit still.

Managing Currency, Payments, and Financial Risks

A Saudi expansion doesn't stay healthy just because sales are rising. It stays healthy because finance keeps the model disciplined after launch.

The most common operational error is importing UAE assumptions into Saudi trading. That shows up in pricing, margin expectations, collection timing, channel incentives, and even the cost of serving the account. Demand may be strong and the expansion can still disappoint if the commercial model is wrong.

That risk is called out directly in Meaccurate's work on Saudi market pricing and entry strategy. Their core point is blunt: a Saudi expansion can fail even when demand exists if the product is priced on UAE assumptions, and the recommended approach is to combine market research, stakeholder interviews, competitor analysis, operational assessment, and commercial modelling before capital is committed.

Where the financial model usually breaks

Pricing logic.

A margin that works in the UAE may not survive Saudi distributor expectations, local tender behaviour, or added service costs.

Payment design.

Cross-border collections need a clear process. Who receives payment, into which account, under which contract, and how disputes are handled should all be settled before volume builds.

Currency handling.

Even where AED and SAR exposure feels manageable, finance teams still need a policy. The issue is rarely dramatic FX speculation. It's routine slippage from poor account structure, mismatched settlements, and inconsistent treasury practice.

A practical risk routine

Build a monthly review around a few operating questions:

- Are Saudi deals meeting planned gross margin after local costs?

- Are payment terms drifting beyond what the original model assumed?

- Are distributor or channel expectations changing actual profitability?

- Do collections delays come from customer behaviour or internal process gaps?

This is also where payment operations matter. A clean receivables process reduces friction long before an invoice becomes overdue. Teams that need to tighten their process design should review practical approaches to payments and receivables management.

Good expansion finance is less about forecasting heroics and more about keeping small leaks from becoming permanent margin loss.

The Saudi market rewards businesses that adapt their financial model locally. It doesn't reward companies that assume a UAE template will travel unchanged.

Your Financial Checklist for Saudi Expansion

A typical UAE SME reaches the same moment a few months into Saudi expansion. Sales are coming in, but cash is not arriving in the pattern the original model assumed. Inventory is sitting longer than planned. Customer approvals take extra rounds. Payroll, VAT, customs, and supplier payments still need to go out on time.

That is why a Saudi launch needs a finance checklist built around cash movement, not just entity setup.

Start by checking whether the operating model can survive a slow first collection cycle. A business can be legally ready and still be financially exposed if receivables, stock, and local payment obligations are out of sync. I have seen profitable Saudi revenue create pressure on the UAE parent because no one mapped the actual timing gap between invoice issue and cash receipt.

Readiness checks worth using

- Cash-flow realism: Have you modelled delayed collections, internal customer approval steps, and replenishment timing using conservative assumptions?

- Pricing discipline: Have you rebuilt pricing around Saudi channel margins, delivery costs, and support overhead instead of copying UAE pricing?

- Receivables ownership: Is one person clearly responsible for invoice submission, acceptance follow-up, dispute handling, and payment release tracking?

- Inventory exposure: If stock must sit locally before sale, have you set limits on how much working capital can be tied up at one time?

- Tax and compliance alignment: Are ZATCA-related invoicing, document retention, and control processes ready before transaction volume increases?

- Treasury setup: Is there a defined process for local payments, intercompany funding, and account-level control over who can approve and release cash?

- Stress test: If collections arrive 30 to 60 days later than plan, can the Saudi operation still cover payroll, rent, and supplier commitments without emergency funding?

The strongest finance teams use this checklist before revenue ramps, then review it monthly during the first year. That matters because early underperformance rarely starts with one dramatic mistake. It usually starts with small timing gaps. A late customer approval here. Extra stock there. A pricing exception for one account. Together, those gaps drain cash faster than the P&L suggests.

Saudi opportunity rewards businesses that stay disciplined after market entry. The winners usually treat working capital as a daily operating issue, not a quarterly finance report.

If your business is expanding from the UAE into Saudi Arabia and you need a cleaner way to access cash from invoices, offer buyer payment terms, or keep inventory moving without slowing growth, Comfi is one option to explore as it enables UAE businesses to unlock capital from outstanding invoices within 24 hours, helping free up liquidity to support expansion into the Saudi market.