How to Get Finance for Business in the UAE

For businesses in the UAE, growth often comes down to one simple thing: accessing cash when you need it. The quickest way to get finance for business isn't always through old-school banks. Fintech solutions like invoice discounting or B2B Buy Now, Pay Later (BNPL) can provide access to funds in as little as 24 hours. These modern options cut through the red tape, offering a much smarter way to manage your cash flow.

The Shifting Sands of Business Finance in the UAE

For any small or medium-sized enterprise (SME) in the UAE and the wider MENA region, securing business finance in a timely manner can be a constant challenge. SMEs are the engine room of the economy, but their access to traditional funding hasn't kept up with their massive contribution. This disconnect is a major roadblock for agile businesses in sectors like wholesale, distribution, and automotive that depend heavily on consistent cash flow.

Approaching a conventional bank often means getting stuck in a slow, bureaucratic process that doesn't work for a business that needs to move fast. The mountains of paperwork, rigid collateral demands, and painfully long approval times can bring growth to a grinding halt, leaving you unable to stock up on inventory or say yes to that big customer order.

The Real Story of the SME Funding Gap

This gap between what SMEs need and what traditional banks offer isn't just anecdotal; it’s a deep-seated issue in the region's financial setup. SMEs in the UAE are a huge deal, yet they have historically received a disproportionately small slice of formal credit.

Let's look at the numbers. By mid-2022, there were roughly 557,000 SMEs in the UAE, powering around 63.5% of the non-oil GDP. Despite this massive economic footprint, studies show that SMEs across the MENA region receive only 8% of total bank lending. Compare that to the 22% in high-income economies, and you see the problem. This imbalance creates a huge credit gap, forcing countless suppliers and dealers to dip into personal savings or rely on unstable trade credit instead of proper institutional capital. You can get more background on the SME ecosystem from the official UAE government portal.

For a B2B business operating on 30, 60, or even 90-day invoice terms, this funding gap isn't just a number. It means slower order cycles, insufficient stock on the shelves, and missing out on golden opportunities to grow.

The Rise of Fintech Solutions

This is exactly where modern, fintech-driven alternatives have stepped in. Solutions like invoice discounting and B2B BNPL were built from the ground up to address this funding gap.

- Invoice Discounting: This lets you get a cash advance against your unpaid invoices, freeing up capital that would otherwise be locked away for weeks or months.

- B2B Buy Now, Pay Later (BNPL): This gives your buyers the flexible payment terms they want, encouraging bigger orders while ensuring you get paid right away.

These tools offer a practical, no-nonsense way for businesses to take control of their cash flow, without the delays and headaches associated with traditional methods. For any finance leader looking to fuel growth efficiently, they represent a clear path forward.

Comparing Your Business Finance Options

When you need to get finance for your business, the path you take can seriously impact your company’s agility and growth. The decision is no longer just about securing a bank loan. Today’s market is full of different options, each built for different business needs, timelines, and situations.

Figuring out the core differences between modern fintech solutions and old-school banking methods is the first step to making a smart choice. The right move really depends on your specific circumstances—are you trying to plug an immediate cash flow gap, or are you planning a major long-term investment?

This decision tree gives you a simple way to start thinking about your options, based on your most urgent need: cash flow.

The takeaway here is straightforward: if accessing working capital right now is the priority, fintech is designed for speed. But if you’re funding a planned, long-term project, the traditional route is often a better fit.

Fintech Solutions for Immediate Needs

Fintech platforms have completely changed the game by focusing on speed and accessibility. They use technology to make applications simpler and approvals faster, which is perfect for businesses in fast-moving industries like wholesale and distribution. Two of the most powerful tools are invoice discounting and B2B Buy Now, Pay Later (BNPL).

- Invoice Discounting: This is a lifeline for businesses with solid sales but slow-paying customers. Instead of waiting 30, 60, or even 90 days for an invoice to be paid, you can get an advance on that money, often within 24-48 hours. It directly solves cash flow problems, letting you pay suppliers, cover payroll, or jump on new opportunities without waiting. The whole process is digital and requires significantly less paperwork than a bank would ask for.

- B2B Buy Now, Pay Later (BNPL): We all know BNPL from online shopping, but its B2B version is a game-changer for suppliers. You can offer your business customers flexible payment terms—letting them pay over 30, 60, or 90 days—which helps you close more sales and attract new buyers. The best part? You, the supplier, get paid the full amount upfront by the BNPL provider, who also handles the payment collection. It removes both credit risk and administrative headaches from your plate.

The SME financing market in the UAE is quickly shifting towards these kinds of flexible models. In a market worth around USD 30 billion, there's a clear move away from traditional bank overdrafts. Over USD 1.5 billion has been poured into GCC-based fintech platforms to help close the SME funding gap, with a huge chunk of that coming from the UAE. For many business owners, "getting finance" now means working with platforms that use real-time transaction data to make decisions, leading to more approvals for SMEs that banks used to overlook.

Traditional Methods for Long-Term Growth

While fintech is great for speed, traditional financing still plays a crucial role, especially for big, strategic investments. These options are usually slower and require more hoops to jump through, but they can provide larger amounts of capital for major business milestones.

- Bank Loans: A standard business loan is often the first thing people think of when they need to finance their business. It’s best for huge expenses like buying property, acquiring heavy machinery, or funding a massive expansion. The application process can be extensive, demanding detailed business plans, years of financial statements, and hefty collateral. Approval can take weeks or even months, but the interest rates might be lower for established businesses with a strong credit history. For a detailed look at funding equipment, check out this a comprehensive guide to restaurant equipment financing options.

- Equity Funding: This means selling a piece of your company to investors in exchange for cash. It’s not a loan, so there’s nothing to pay back. The catch? You’re giving up a share of your ownership and some control. This path is usually for high-growth startups and scale-ups with the potential for massive returns. It's a long, complicated process of pitching to venture capitalists or angel investors and is designed to fund ambitious, long-term growth, not manage day-to-day cash flow.

The core difference comes down to purpose and speed. Fintech provides short-term liquidity to keep operations running. Traditional methods provide the foundational, long-term capital needed for transformative growth.

Making the right choice means being honest about your immediate needs and future goals. If you need to unlock cash tied up in unpaid invoices or want to boost sales with flexible payment options, fintech is your best friend. But for those planning a major, multi-year expansion, the slower, more deliberate pace of traditional options might be the better fit. To get a better handle on the details, have a look at our guide on navigating small business lending.

Quick Comparison of Business Finance Options

To help you see the differences at a glance, here’s a straightforward comparison between modern fintech and traditional financing. This information cuts through the noise and highlights the key factors that matter most when you're deciding where to get funding.

Fintech (Invoice Discounting, BNPL)

- Best For: Solving immediate cash flow gaps, boosting sales, covering operational costs.

- Approval Speed: 24-48 hours.

- Typical Cost Structure: Discount fee on invoice value or a small transaction fee.

- Collateral Required: Usually unsecured; the invoice itself acts as the asset.

Traditional (Bank Loans, Equity)

- Best For: Large capital projects, long-term expansion, property or heavy equipment purchases.

- Approval Speed: Weeks to months.

- Typical Cost Structure: Annual interest rate (APR) on the loan amount or giving up company equity.

- Collateral Required: Almost always requires significant collateral like property or assets.

Ultimately, the best option depends entirely on your situation. Fintech offers a quick, flexible solution for the day-to-day financial realities of running a business. Traditional finance, on the other hand, provides the heavy-duty capital needed for foundational growth. Knowing which one to use, and when, is key to building a resilient business.

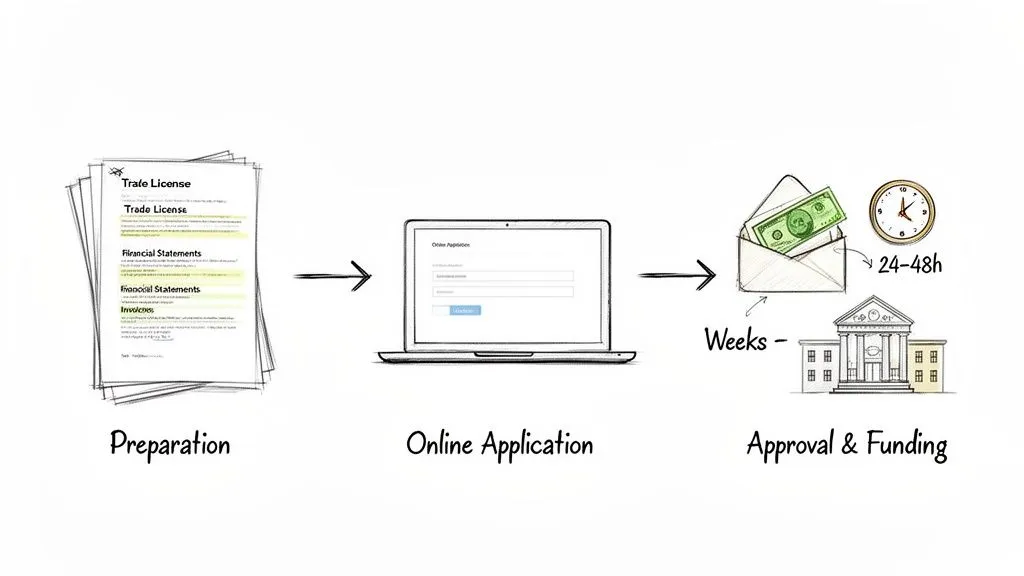

A Practical Guide to the Application Process

Trying to secure business finance can feel like a maze, but it helps to know the layout. Whether you’re dealing with a slick fintech platform or a traditional bank, the journey breaks down into three core phases: getting your house in order, submitting the application, and getting the decision. Your success often comes down to that first step—a well-organised application is half the battle won.

It’s also crucial to understand the difference between the two main paths. The fintech route is all about speed and simplicity, using digital data to make quick calls. Banks, on the other hand, follow a more traditional, paper-heavy trail that digs deep into your business history and assets. Knowing what each provider is looking for will help you manage your time and expectations.

Stage 1: Assembling Your Documents

Before you even think about filling out a form, getting your paperwork together is the most important thing you can do. A complete, organised set of documents signals that you run a serious, professional operation. While the exact list varies, most providers will ask for a standard set of files to confirm your business's identity, legal status, and financial health.

For most applications in the UAE, you’ll need these essentials ready to go:

- Valid Trade Licence: This is non-negotiable. It’s the official proof that your business is legally registered and allowed to operate.

- Memorandum of Association (MOA): This document lays out the company’s internal rules and, crucially, who owns it.

- Passport and Emirates ID Copies: Required for all owners and key signatories to verify their identities.

- Bank Statements: Usually for the last 6-12 months, these give a clear, unfiltered look at your company’s cash flow and financial stability.

- Invoices (for invoice discounting): If you're looking to get cash from your receivables, you’ll need copies of the specific invoices you want to draw against.

If you're going down the traditional bank route, the list gets a lot longer. Expect to provide audited financial statements for the last 2-3 years, detailed business plans, and proof of any collateral you’re offering up.

Stage 2: The Application Experience

This is where you’ll really feel the difference between fintech and old-school banking. Fintech platforms like Comfi have built their application process to be entirely digital and painless, cutting out all the usual friction. You can typically get the whole thing done online in just a few minutes.

The digital application journey usually looks something like this:

- Online Registration: Setting up an account on the platform.

- Document Upload: Submitting digital copies of the papers you’ve already gathered.

- Connecting Accounts: Securely linking your business bank account or accounting software, which allows for real-time data analysis.

Applying through a traditional bank is a much more hands-on and drawn-out affair. It often involves multiple trips to the branch, stacks of paperwork, and long conversations with a relationship manager. The bank’s focus is on historical performance and physical assets, not your live transactional data.

The real difference is how they look at risk. Fintechs use live data to see how healthy your business is right now, which allows for lightning-fast decisions. Banks rely on a historical, collateral-based model that, by its very nature, takes a lot more time and scrutiny.

Stage 3: Approval and Accessing Funds

The final step is getting the decision and, hopefully, the money. The timelines here are worlds apart. With fintech solutions like invoice discounting, speed is the whole point. Once your application is in and your invoices are checked, you can often see the funds in your account within 24 to 48 hours. That kind of speed is a game-changer when you have urgent working capital needs.

In the world of traditional banking, you’ll need to be patient. The approval process for a business loan can take anywhere from several weeks to a few months. It has to go through multiple layers of review, from a credit analyst all the way up to a final committee. Even after you get the "yes," it can take more time to sort out legal documents before the money is actually released.

This makes bank loans a good fit for planned, long-term investments, but completely impractical for plugging unexpected cash flow gaps. No matter which path you choose, putting together a strong application from the start is the best way to get finance for your business with minimal delays.

Real-World Scenarios: Picking the Right Finance When It Counts

Understanding the theory behind business finance is one thing. Knowing exactly which tool to grab when you’re in a real-world crunch is something else entirely. The best financing option isn’t a one-size-fits-all product; it’s a specific solution for a specific problem.

Let’s move from theory to practice. Here are a few common situations that wholesalers, distributors, and e-commerce businesses face every day. See if any of these sound familiar—connecting these examples to your own challenges is the first step to building a smarter, more resilient financial strategy.

The Unexpectedly Large Order

Picture this: you're an electronics wholesaler in Dubai, and a major retailer suddenly drops a purchase order that's double your usual volume. It’s a massive opportunity, but you need cash now to pay your own suppliers. The problem? All your capital is tied up in outstanding invoices with 60-day payment terms.

Waiting two months for that cash to land means kissing this huge sale goodbye. Applying for a traditional bank loan would take weeks, and by then, the opportunity will have vanished.

Recommended Solution: Invoice Discounting

This is the classic use case for invoice discounting. Instead of waiting, you can get an immediate cash advance against those existing unpaid invoices. This helps unlock the working capital you’ve already earned—often within 24-48 hours—giving you the funds to buy the stock you need and fulfil that large order without missing a beat.

Gearing Up for a High-Sales Season

Now, imagine you’re an automotive dealer in Abu Dhabi preparing for the peak Ramadan sales season. To capture all that demand, you need to pack your showroom with popular models. That requires a huge upfront investment, and tying up so much capital in stock for weeks could put a serious strain on your day-to-day operations.

You need a way to fund your inventory that’s directly linked to your sales cycle, freeing up capital as soon as a vehicle is sold.

Recommended Solution: Dealer-Focused Solutions

Specialised dealer financing solutions were built for exactly this scenario. It lets you stock up on inventory without the immediate cash hit. The repayment is typically tied to the sale of the vehicles, creating a smooth flow of capital that perfectly matches your business rhythm. It's a strategic way to load up on inventory without choking your cash flow.

The key takeaway here is that modern finance solutions aren’t generic. They are specialised tools designed to solve specific operational bottlenecks, whether it’s managing receivables or stocking up on inventory. Choosing the right one is about matching the solution to the problem at hand.

Supercharging Sales on a B2B Platform

Let’s say you run a B2B e-commerce platform for office supplies. You’ve noticed that your business customers are hesitant to place larger orders because it ties up their own cash. Your goal is simple: increase the average order value and attract bigger clients.

Offering better payment terms seems like the obvious answer. But the thought of managing the credit risk and administrative nightmare of chasing payments from hundreds of different buyers is enough to keep you up at night.

Recommended Solution: B2B Buy Now, Pay Later (BNPL)

By integrating a B2B BNPL option at checkout, you can offer your buyers flexible 30, 60, or 90-day payment terms. This empowers them to buy more without feeling the immediate financial pinch. And the best part? You get paid the full invoice amount upfront from the BNPL provider, who takes on the task of collecting the payment. You boost sales, eliminate credit risk, and improve your own cash flow all at once. For more on this, check out our insights on optimising your cash conversion cycle.

This forward-thinking approach is catching on fast. Recent data shows that UAE SMEs are actively looking for capital to expand and digitise. According to Mastercard’s 2025 SME Confidence Index, a staggering 70% of small businesses in the UAE plan to seek access to funds in 2025, mostly to scale their operations. This ambition, combined with strong government support like the USD 8.7 billion "Projects of the 50" initiative, proves that getting finance is all about choosing the smartest, fastest option on the table. You can learn more about these trends in the SME Confidence Index report.

How Comfi Helps Businesses Unlock Cash Flow

Navigating the world of business finance really boils down to one thing: accessing cash when you need it most. For any business in the UAE juggling delayed payments or trying to supercharge sales, the right financial tools can be a complete game-changer. This is where modern digital platforms come in, designed specifically to cut through the old-school hurdles and solve cash flow problems fast.

This is exactly where Comfi shines. We offer practical, straightforward solutions built for the realities that suppliers, wholesalers, and dealers face every day. Our focus is on speed and simplicity, helping you unlock the capital you need to grow, manage your day-to-day, and grab new opportunities without getting bogged down.

Turning Unpaid Invoices into Immediate Capital

One of the biggest growth killers for any B2B company is the cash trapped in unpaid invoices. That painful wait for 30, 60, or even 90 days creates a predictable bottleneck, stalling everything from buying new stock to running daily operations. Comfi’s invoice discounting product is the direct answer to this problem.

Instead of sitting around waiting for your customers to pay up, you can simply upload your outstanding invoices to our platform and get a huge chunk of their value almost instantly. Our clients have been able to get funds in their accounts within 24 hours. It’s a powerful way to turn future revenue into the working capital you need today, without the endless waits or mountains of paperwork from traditional financial institutions.

The advantages are crystal clear:

- Rapid Access to Funds: Get cash in your account in as little as one business day.

- No Collateral Needed: Your invoice is the asset, so you don’t have to pledge property or equipment.

- Simple Digital Process: The entire experience, from setup to funding, is handled online through a clean, intuitive dashboard.

The core benefit here is control. When you unlock cash from your receivables, you're back in command of your financial timeline. You can pay your own suppliers, cover payroll, and invest in growth without missing a beat.

Empowering Sales with Flexible Buyer Terms

In a market this competitive, offering attractive payment terms can be the one thing that makes a buyer choose you over someone else. The problem is, extending credit yourself means taking on risk and a whole lot of admin. Comfi’s B2B Buy Now, Pay Later (BNPL) solution completely solves this dilemma, letting you offer flexible terms while you get paid upfront.

This model gives your buyers the freedom to pay over 30, 60, or 90 days, which encourages them to place bigger, more frequent orders. But for you, the supplier, the benefit is immediate. Comfi pays you the full invoice amount straight away and we handle the collections process. This takes both the credit risk and the operational headache of chasing payments completely off your plate.

Our clients see real, measurable results from this:

- Up to a 30% uplift in sales from existing customers.

- A 20% increase in new customer acquisition thanks to more appealing terms.

- Larger average order sizes as buyers find they have more purchasing power.

It creates a true win-win. Your buyers get the flexibility they want, and you get the immediate cash flow you need to scale your operations. Of course, pairing a great tool with solid internal practices is key. To really get a grip on your company’s financial health, it’s worth exploring effective cash flow management strategies. By combining smart internal habits with external tools, you can build a resilient financial foundation that supports real, sustainable growth. If you're looking for more details, you can learn more about invoice discounting with Comfi here.

Common Questions About Business Finance in the UAE

When you’re looking for business finance, a lot of questions come up. The landscape is packed with different options, each with its own rules, timelines, and real-world benefits. To help you cut through the noise and make a decision you feel good about, we’ve pulled together some of the most common questions SMEs in the UAE ask on their funding journey.

What Is the Fastest Way to Get Business Finance?

For businesses that need capital right now, fintech solutions are, without a doubt, the fastest way to go. A traditional bank loan can take weeks, sometimes even months, to get approved. That kind of timeline just doesn’t work when you have an urgent need, like paying for a huge new order or making payroll.

On the other hand, platforms offering invoice discounting can often get funds into your account within 24 to 48 hours. The whole process is digital, from uploading a few documents to seeing the cash land. This speed is possible because the decision isn't based on years of your financial history; it's based on the quality of your invoices and the reliability of your customers.

How Do I Know if My Business Is Eligible?

Eligibility is one of the biggest differences between old-school financial institutions and modern fintech platforms. Banks usually have a long, strict checklist that can be a real hurdle for many SMEs.

- Traditional Banks often require: A long trading history (usually 2-3 years), a track record of profitability, high annual turnover, and physical assets you can offer up as collateral.

- Fintech Platforms focus on: Your recent business performance and day-to-day transactions. For something like invoice discounting, what really matters is the value of your outstanding invoices and your B2B customers' payment history. This data-first approach means even newer or asset-light businesses can qualify.

Is Invoice Discounting the Same as a Loan?

No, and it's a really important distinction. A loan is debt. You borrow a lump sum of money that you have to pay back over time with interest. It shows up as a liability on your balance sheet and often requires you to put company or personal assets on the line as security.

Invoice discounting isn't a loan. It’s a financial transaction where you sell your unpaid invoices to a third party for a fee. You’re essentially getting paid early on money that is already yours. This means you aren’t adding debt to your books, and it doesn't affect your ability to borrow later if you need to.

The key difference is what you're using to get the cash. A loan uses your future ability to repay as its foundation. Invoice discounting uses an asset you already own—the money your customers owe you.

What Are the Main Costs Involved?

Getting a clear picture of the costs is crucial when you get finance for business. The way you pay for funding is fundamentally different across the options and suits different financial strategies.

With a traditional bank loan, your main cost is the Annual Percentage Rate (APR), which wraps up the interest rate and any other fees. You pay this back over the life of the loan.

For invoice discounting, the cost is typically a simple discount fee—a small percentage of the invoice's value. That’s the fee for the service of getting your cash upfront. In a similar way, B2B BNPL solutions usually involve a small transaction fee, which the supplier pays to get paid immediately while giving their buyer flexible terms.

Can I Get Finance Without Providing Collateral?

Yes, absolutely. It's entirely possible to get business finance without having to pledge physical collateral like property or equipment. This is one of the biggest game-changers that modern fintech solutions have brought to the market.

- Invoice Discounting: This is a type of unsecured finance. The invoices themselves act as the asset, so there’s no need for traditional collateral. This is a huge advantage for service-based businesses or any company that doesn’t own a lot of physical assets.

- B2B Buy Now, Pay Later: This is also unsecured for the supplier. The provider takes on the risk of assessing the buyer's creditworthiness, so the supplier doesn't need to put up any assets to offer better payment terms.

This move away from collateral-based lending is a major reason why non-bank financial institutions have gained significant market share globally. They’re more interested in a business’s operational health and cash flow than its fixed assets.

How Does Technology Simplify the Process?

Technology is what makes modern finance so fast and accessible. Digital platforms have automated all the slow, manual steps that used to define the old banking experience.

Here are a few of the key tech advantages:

- Digital Onboarding: You can sign up and verify your business completely online, no need for trips to a bank branch.

- Seamless Document Submission: Securely upload essentials like your trade licence and bank statements in just a few minutes.

- Real-Time Data Analysis: By connecting to your accounting software or bank accounts, platforms can analyse your financial health almost instantly, leading to much faster decisions.

- Intuitive Dashboards: Manage your applications, keep an eye on your invoices, and see your available funding all in one simple online portal.

This tech-first approach doesn’t just speed things up; it also gives you far more transparency and control over your company's finances, making it easier than ever to get the capital you need to grow.

Ready to unlock your business's growth potential without the wait? With Comfi, you can turn your unpaid invoices into working capital in as little as 24 hours. Explore our solutions and see how we can help you grow.