Invoice Finance for Small Business: A 2026 MENA Guide

A strong month can still feel stressful when cash is trapped in unpaid invoices.

You deliver the order. The client accepts it. The invoice goes out. Then the wait starts. For many SMEs in the UAE and wider MENA region, that wait is the primary problem, not a lack of sales.

If your customers buy on trade terms, your business can look healthy on paper while still feeling squeezed day to day. You may need to pay suppliers now, cover salaries now, or buy stock now, even though your customer won't settle for weeks. That's where invoice finance for small business becomes useful. It helps you access cash tied up in invoices you've already issued, instead of sitting still and waiting for payment to land.

Your Business Is Growing But Cash Is Tight

Growth often creates a strange kind of pressure. The more orders you win, the more cash you need upfront to fulfil them. If one large customer takes a long time to pay, that single invoice can slow the rest of the business.

A common example in the UAE is a supplier who lands a valuable B2B order from a retailer, contractor, distributor, or corporate buyer. It's good business, but the buyer wants payment terms. Those terms might be routine for them, yet for a smaller company they can lock up cash at exactly the wrong time.

That gap between delivering the work and receiving the money is where invoice finance fits.

With invoice finance, a business can release up to 80% to 90% of an unpaid invoice's value within 24 hours, according to the British Business Bank's guide to invoice finance. Instead of waiting for the full payment cycle to finish, you get access to most of the invoice value much earlier.

Why that matters in practice

That cash can help you do ordinary but critical things:

- Pay suppliers on time so production or purchasing doesn't stall

- Cover payroll and overheads without juggling payments

- Take on new orders rather than turning work away

- Buy inventory earlier when demand is rising

This is one reason invoice finance is often described as a revolving facility. As the British Business Bank notes in its guide, the available funding typically replenishes as invoices are issued and settled. In plain language, your access can move with your sales rather than stay fixed.

Practical rule: If your biggest problem is timing, not demand, invoice finance may be worth examining.

It's also worth knowing what this tool is and isn't. It isn't built for every company. Traditional invoice finance is generally more relevant to established SMEs than very small firms, and the British Business Bank notes it is generally not suitable for businesses with annual turnover below £300,000 in its UK context.

For MENA business owners, the principle is the same. If your business sells to other businesses on delayed payment terms, invoice finance can act like a bridge between delivery and payment.

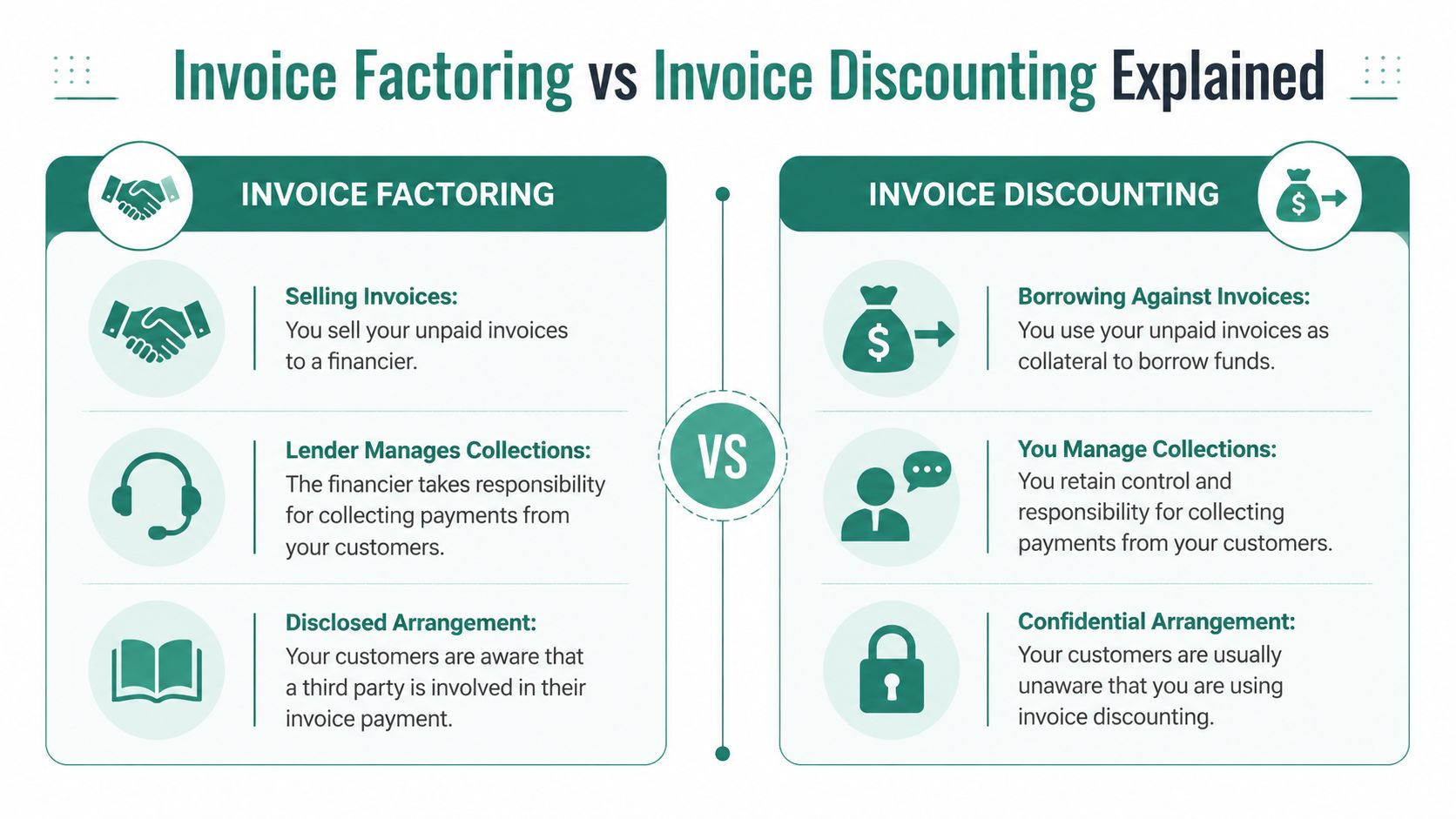

Invoice Factoring vs Invoice Discounting Explained

Both options sit under the same umbrella. Both use unpaid invoices to access cash sooner. The big difference is who deals with the customer payment process.

A simple way to think about it is this. One option is more hands-on for the provider. The other leaves more control with you.

Invoice factoring

With invoice factoring, the provider usually takes a more visible role after the invoice is issued. They often handle collections and follow up with the customer for payment.

That can suit a small business that wants administrative help, especially if chasing receivables takes too much owner time. If your team is lean and your sales ledger is growing quickly, outsourcing part of that process can remove friction.

Factoring may work well if:

- Your team is stretched and collections are consuming time

- You want support with ledger management instead of running it all internally

- You don't mind customer awareness that a third party is involved

Invoice discounting

With invoice discounting, you typically stay in charge of the customer relationship and the collection process. The provider advances cash against the invoice, but your customer relationship usually remains more direct.

That often appeals to businesses that want tighter control over communications, especially if account management is sensitive or relationship-led. Many wholesalers, distributors, and service firms prefer this route because it feels closer to their normal receivables workflow.

You may prefer discounting if:

- You want to keep customer communication in-house

- Your finance team already manages collections well

- You care about confidentiality and control

If your customer relationships are carefully managed by your team, invoice discounting often feels more natural than factoring.

The operational choice matters more than many founders expect. A facility can be commercially useful but still be a poor fit if it changes how customers experience your business.

If you're trying to improve receivables handling before choosing a structure, it also helps to build invoice-to-cash workflows so invoice creation, payment tracking, and follow-up are more organised from the start.

For a deeper side-by-side breakdown of how these models differ, this guide on invoice discounting vs factoring is a useful follow-on read.

How the Invoice Finance Process Works

The mechanics are usually simpler than people expect. In most cases, the provider wants to answer one core question first. Is this a genuine B2B invoice that is likely to be paid?

That's why the process tends to move in a short sequence rather than a long banking-style application.

Step 1 Apply with business and buyer details

You start by sharing basic information about your company, your invoices, and the customers behind those invoices. Providers usually want to know who owes the money, what was delivered, and whether the invoice is already due or still within normal payment terms.

This stage is less about storytelling and more about clarity. Clean records matter.

Step 2 Submit the invoice

Once you're onboarded, you upload the invoice or invoices you want reviewed. These are usually B2B invoices, not consumer receivables.

The product is designed around trade credit. Standard payment delays of 30, 60, or 90 days are exactly the kind of gap invoice finance is built to address, as explained in the Swoop Funding guide to invoice finance.

Step 3 The provider verifies the invoice

Verification is where providers check that the invoice is valid, undisputed, and tied to a real business transaction. They may also review supporting documents such as purchase orders, delivery notes, or proof that the goods or services were accepted.

This is the part that often confuses smaller businesses. The provider isn't just looking at your company. They're also checking whether the invoice itself stands up to scrutiny.

Step 4 You receive an advance

If the invoice is approved, the provider releases an agreed portion of its value upfront. According to Swoop Funding, invoice finance typically advances up to 100% of the invoice total and often does so within 1 to 2 days.

For a business managing payroll, stock purchases, or freight costs, speed matters almost as much as the amount.

The real value isn't only early cash. It's being able to keep trading while customers follow their normal payment cycle.

Step 5 The customer pays on the agreed terms

What happens next depends on the structure you chose earlier.

- In a factoring setup, the customer often pays the provider directly.

- In a discounting setup, payment collection usually remains with your business.

Either way, your customer still pays on the original commercial terms. Invoice finance changes the timing of your access to cash. It doesn't usually change the buyer's agreed payment window.

Step 6 Final settlement takes place

After the customer pays the invoice in full, the remaining balance is released to you after fees and any agreed deductions are accounted for.

Owners sometimes realise they should have asked better questions upfront. The gross invoice amount and the final amount you receive aren't the same thing, so you need to understand the fee structure before relying on the facility.

What tends to improve approval odds

Providers usually look for a few basics:

- Clear B2B invoices issued to established business customers

- Good documentation showing the sale is complete and accepted

- Low dispute risk because contested invoices are harder to fund

- Reliable payer behaviour from the buyer

If your receivables process is messy, fix that before applying. An AR guide for operations leaders can help tighten invoicing, collections, and handoff processes so funding decisions move more smoothly.

Costs Risks and Benefits for MENA Businesses

This is the question most owners really want answered. Not “What is invoice finance?” but “Will it make financial sense for my business?”

That's the right question.

The headline promise of invoice finance is straightforward. You access cash sooner. But affordability depends on what happens after the advance, not just before it.

The core benefit is timing

For many MENA SMEs, the immediate benefit is operational breathing room. Earlier cash access can help a business stay consistent during long receivables cycles, especially when supplier payments and salary obligations don't move just because a customer is slow.

This can improve decision-making in ordinary situations:

- A distributor can restock sooner instead of waiting for a large invoice to clear

- A service firm can meet payroll calmly while enterprise clients follow internal approval cycles

- A wholesaler can accept larger orders without freezing cash in one transaction

That kind of flexibility matters most in businesses where sales are healthy but collections are slow.

What drives approval and pricing

A key point many founders miss is that providers often focus heavily on the buyer's credit quality, not only on your own financials. Drip Capital explains that approval and risk are shaped by confidence that the invoice is valid and that the buyer is creditworthy and likely to pay, in its article on benefits of invoice financing.

That changes the conversation. If your customer is large, reputable, and reliable, your invoice may be more attractive than your balance sheet alone would suggest.

The affordability question is rarely answered well

Generic explainers for UAE businesses often fall short. They tell you that funds can be released quickly. They rarely help you judge whether the facility is worth the cost once all deductions, conditions, and timing issues are included.

Stripe's small-business guidance highlights that invoice financing can advance “up to 90%” of invoice value in 1 to 2 days, and it also notes an important UAE market context: the UAE Ministry of Economy has repeatedly stated that SMEs account for around 94% of companies operating in the country, as discussed in Stripe's article on invoice financing for small businesses. That makes pricing clarity especially important because a huge share of the market can be affected by unclear terms.

Worth checking first: Don't evaluate invoice finance on the advance alone. Evaluate it on the cash you keep after fees, holdbacks, disputes, and timing issues.

What can make it more expensive than expected

The true cost can rise when practical issues appear in the transaction itself.

Watch for points like these:

- Holdbacks and reserves

The provider may keep back part of the invoice value until final settlement. That affects how much usable cash lands in your account. - Disputes or deductions

If the customer challenges the invoice, delays acceptance, or applies deductions, your access to the remaining balance can shrink or slow down. - Recourse terms

In a recourse structure, your business may still carry responsibility if the customer doesn't pay. That shifts more risk back to you. - Early-payment discounts with buyers

If your customer negotiates settlement adjustments, your net proceeds may change even though the face value of the invoice looked attractive at the start.

A practical break-even way to think about it

You don't need a complex model to make a first judgement. You need a sensible commercial test.

Ask:

- What problem am I solving? Is it payroll pressure, inventory timing, or the ability to take the next order?

- What margin sits behind this invoice? Thin-margin trades need more caution.

- What happens if I don't use it? Lost sales, supplier strain, and stockouts all have a cost too.

- Is my customer low-risk and low-dispute? Cleaner invoices tend to be easier to work with.

If the facility helps you preserve supplier relationships, avoid turning away profitable business, or keep operations steady during long payment cycles, it may be worthwhile even if the fee isn't cheap in absolute terms.

If you want to think more carefully about exposure on the buyer side, this piece on payment risk is a useful companion.

How to Choose a Provider and Apply

The right provider should make the process clearer, not more complicated. If the pricing is hard to understand or the workflow feels clumsy, that usually becomes a problem later when cash is tight and time matters.

For SMEs in MENA, provider choice often comes down to three practical questions. Can they explain their terms plainly? Can they move at the speed your business needs? Do they understand the type of buyers and receivables you deal with?

What to compare before you sign

Don't start with branding. Start with execution.

- Fee transparency

Ask for a plain-English explanation of every fee, reserve, and condition that affects final settlement. - Funding speed

Fast approval only matters if funds are released when promised. - Invoice eligibility rules

Some providers are comfortable with certain sectors, customer profiles, or invoice types. Others are much narrower. - Digital workflow

A clean dashboard, easy document upload, and clear status tracking save time for your finance team. - Collections approach

If the provider interacts with your customers, make sure their style fits your relationship model.

A provider can look affordable at first glance and still be awkward in day-to-day use. Process quality matters.

A simple application checklist

Most businesses can prepare in advance by gathering a small set of documents and answers:

- Business records such as trade licence details and company information

- Customer information for the buyer linked to the invoice

- Invoice copies for the receivables you want reviewed

- Supporting proof like purchase orders, delivery records, or accepted work confirmation

- Banking and payout details so funds can be settled smoothly

One MENA-focused option in this category is Comfi's invoice discounting product, which lets businesses upload approved invoices through a digital workflow and receive early payment after approval. It's one example of the kind of fully digital process many SMEs now expect.

Questions worth asking on the first call

Some questions reveal more than a sales deck ever will:

- What happens if my customer pays late?

- How do you handle disputed invoices?

- Can I choose specific invoices or is the facility broader?

- Who speaks to my customer, and when?

- What reduces the amount I receive at final settlement?

A good provider won't dodge those questions.

Real Examples of Invoice Finance in Action

The value of invoice finance usually becomes obvious when you look at actual trading situations rather than definitions.

A Dubai electronics distributor

A distributor supplies a major retail chain with a seasonal shipment of devices and accessories. The retailer accepts the goods, but payment is due later under standard trade terms. That leaves the distributor in a difficult spot. Sales look strong, yet cash is tied up in one large receivable just as the next buying window opens.

The business uses invoice discounting on that approved invoice. Cash is released early, and the company uses it to place new stock orders while demand is still active. The key benefit isn't theoretical. It's the ability to restock without waiting for the first invoice to clear.

A Riyadh B2B services firm

A marketing agency works with several corporate clients that pay on longer approval cycles. The agency has recurring project work, but monthly collections are uneven. Some months look comfortable, while others feel tight because client payments bunch together later than expected.

The firm uses invoice finance selectively on approved client invoices during heavier payroll periods. That gives the owner a steadier operating rhythm. Staff are paid on time, software subscriptions stay current, and the agency doesn't need to pause growth because client finance teams move slowly.

These examples show the same pattern. The problem isn't always lack of revenue. Often it's the delay between earning money and receiving it.

Frequently Asked Questions about Invoice Finance

Will my customers know I'm using invoice finance

Sometimes yes, sometimes no.

In many factoring arrangements, the customer is aware because the provider may handle collections or receive payment directly. In invoice discounting, the arrangement is often more discreet and your team may continue handling customer communication as usual.

If confidentiality matters to you, ask the provider exactly how payments are routed and how customer contact is handled before you sign.

What if my customer pays late or doesn't pay at all

That depends on the agreement.

Some facilities are recourse-based, which means your business may remain responsible if the customer doesn't settle. Others place more of that risk with the provider, but the terms are usually stricter and the pricing may differ. You need to know which model you're agreeing to, especially if you deal with buyers who have long approval chains or a history of disputes.

Do I have to use all my invoices

Not always.

Some arrangements let businesses finance selected invoices when needed. Others are broader and may involve a larger share of your receivables book. The right setup depends on whether your funding need is occasional, seasonal, or ongoing.

If you only want flexibility for certain buyers or specific large invoices, ask whether selective use is possible. That can make invoice finance much more practical for a smaller business.

If your business sells on B2B terms and cash gets stuck between delivery and payment, Comfi is one option to explore. It offers digital invoice discounting workflows for SMEs in MENA, helping businesses access cash from approved invoices without waiting for the full customer payment cycle.