How Can MENA SMEs Master Working Capital?

Think of working capital as the lifeblood of your business. It's the cash you have on hand to run your day-to-day operations. In simple terms, it's the difference between your current assets (what you own that can quickly become cash) and your current liabilities (what you need to pay soon). Imagine it's the fuel in your car—no matter how powerful the engine, you're not going anywhere without it.

Understanding Your Operational Fuel

For any small or medium-sized enterprise (SME), getting a handle on working capital isn't just a financial chore; it's fundamental to survival and growth. This is the money that pays your staff, covers supplier invoices, and keeps the lights on.

If you have positive working capital, you're in a good spot—you have enough liquid assets to cover your immediate bills. But if that number dips into the negative, it’s a warning sign that cash flow problems could be just around the corner, even if your business is profitable on paper.

The Two Core Elements

At its core, the working capital calculation is straightforward. It boils down to two key parts of your business's financial health:

- Current Assets: This is everything your business owns that can be turned into cash within a year. Think of cash in the bank, accounts receivable (the money your customers owe you), and your inventory.

- Current Liabilities: These are your short-term debts and bills that need to be paid within a year. This typically includes accounts payable (the money you owe your suppliers), short-term debts, and other expenses like salaries and taxes.

The goal is to keep these two in a healthy balance, ensuring you always have enough easily accessible cash to handle your obligations without stress.

Effective working capital management gives you the freedom and financial stability to jump on growth opportunities, handle market shifts, and build a business that lasts.

More Than Just Numbers

Don't mistake working capital management for simple bookkeeping. It's a powerful strategic tool that can give you a real competitive edge. For instance, when you're just getting started, understanding the total cost of starting a business in Dubai is vital for estimating how much cash you'll need to keep things running smoothly from day one.

When you manage it well, your business doesn't just survive; it thrives. You'll have the cash to invest in new stock, get better deals from suppliers by paying them early, and steer clear of the cash flow emergencies that can stop a growing business in its tracks. In this guide, we'll show you exactly how to measure, manage, and perfect this crucial part of your company's financial health.

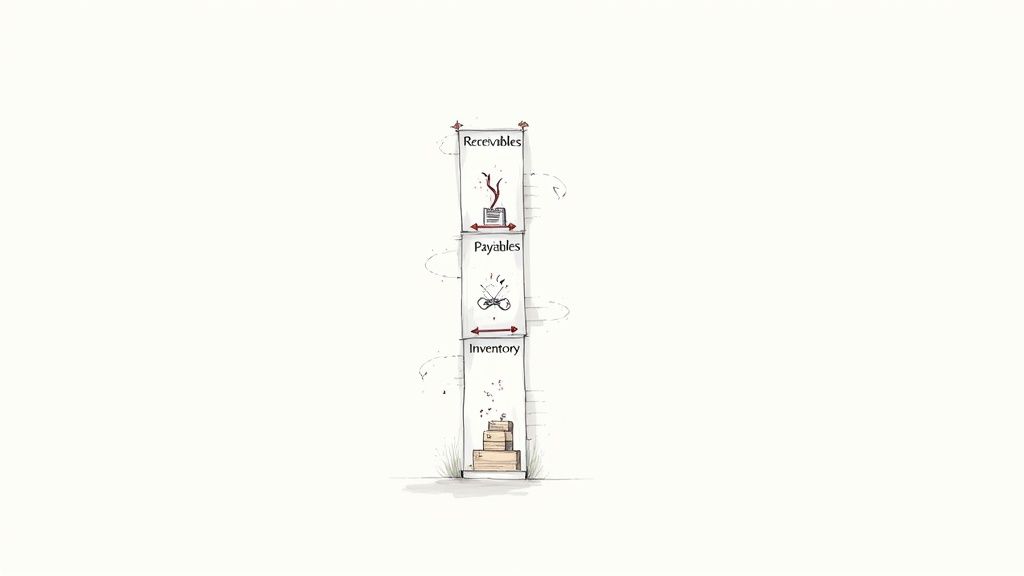

The Moving Parts of Working Capital

To get a real grip on your business’s financial health, you need to understand what actually makes up your working capital. It's less of a single number and more of a balancing act between three key areas. Get them working together, and your operations will run smoothly. But if one falls out of sync, it can throw your entire cash flow into chaos.

Let's unpack these three components with some practical insights for small and medium-sized businesses in the UAE and across MENA. These aren't just dry accounting terms; they're the actual levers you can pull to make your company more stable and ready for growth.

Accounts Receivable: The Cash Locked Up in Your Invoices

First up is accounts receivable. This is simply the money your customers owe you for products or services they've already received. It's cash that belongs to you, but it's not in your bank account yet. For many businesses, this is the single biggest and most frustrating cash flow headache.

Picture this: you run a wholesale food distribution company in Dubai. You’ve just delivered a huge order to a major supermarket chain, worth thousands of dirhams. The sale is done and the profit is on the books, but the client’s payment terms are 90 days.

While you're waiting those three months, the bills don't stop. Your own suppliers need paying, your warehouse team needs their salaries, and your delivery trucks need fuel. That gap between doing the work and getting paid is where so many SMEs get stuck. Their working capital is tied up, completely unavailable for the day-to-day running of the business.

Accounts Payable: A Smart Way to Manage Your Cash Outflow

On the flip side, you have accounts payable. This is the money you owe your suppliers. It’s technically a debt, but savvy business owners see it as more than just a pile of bills.

Think of managing your payables as a strategic way to control your cash outflow. It’s a powerful method for holding onto your cash for as long as you can without damaging relationships with your suppliers.

Let's say a boutique electronics shop in Riyadh needs to bring in the latest smartphones. Instead of paying for all that stock upfront, they negotiate payment terms of 60 days with their distributor. This simple move achieves a few things:

- Holds onto Cash: Their money stays in the bank, ready for unexpected expenses or a last-minute marketing push.

- Boosts Cash Flow: They can sell some of the new phones to customers before the supplier's bill is even due, essentially using customer money to pay their own invoice.

- Strengthens Relationships: As long as they pay reliably within those 60 days, they build trust. That trust can lead to even better deals or more flexible terms down the road.

The trick is to find that sweet spot—stretching payments just enough to help your cash flow, while always paying on time to remain a partner people want to do business with.

Inventory: Walking the Tightrope Between ‘Ready’ and ‘Risky’

The last piece of the puzzle is inventory. This covers everything from the raw materials you use to the finished products waiting to be sold. For any business selling physical goods, whether it's construction supplies or designer clothes—managing inventory is a constant balancing act.

You absolutely need enough stock on hand to meet customer demand and not lose out on sales. But every item sitting on a shelf represents cash that's tied up. That's money that could be paying salaries, covering rent, or funding an expansion.

Imagine a UAE-based furniture maker gearing up for the winter season, which is always a busy time for home goods. If they produce too much and overestimate demand, they’ll be stuck with a warehouse full of unsold sofas—a massive drain on their working capital. But if they don't produce enough, they'll miss out on sales and send customers straight to their competitors. Effective inventory management is all about using good data and smart forecasting to walk this tightrope, making sure your cash is working for you, not just collecting dust.

Key Metrics to Measure Your Working Capital Health

Knowing what working capital is is one thing; actually managing it is another. To do that, you need to measure it. Think of these key metrics as the dashboard on your car—they give you a real-time view of your business's financial engine, telling you how efficiently you're running and if you're about to stall.

For any business owner in the MENA region, getting a handle on a few key numbers can turn financial management from a guessing game into a clear strategy. These aren't just for accountants; they're practical tools that tell a story about your company’s stability and operational rhythm.

The Current Ratio: A Basic Health Check

The Current Ratio is the quickest and most straightforward health check for your business. It answers a simple but vital question: "Do I have enough short-term assets to cover my short-term debts?"

The formula is as simple as it gets:

Current Ratio = Current Assets / Current Liabilities

Generally, a ratio above 1.0 is a good sign, meaning you have more assets than liabilities. A ratio of 2.0, for instance, shows you have two dirhams of current assets for every one dirham of debt you owe. Be careful, though. A ratio that's too high might mean you aren't using your assets efficiently—perhaps too much cash is just sitting there, not working for you.

The Quick Ratio: A Financial Stress Test

Next up is the Quick Ratio, sometimes called the Acid-Test Ratio. This one is a tougher, more conservative measure. It asks a more pointed question: "If I had to pay all my short-term bills right now, could I do it without selling a single piece of inventory?"

This is a critical stress test because, let's be honest, inventory can be hard to sell quickly without offering a steep discount.

Here’s the formula:

Quick Ratio = (Current Assets - Inventory) / Current Liabilities

A quick ratio of 1.0 or higher is what you want to see. It signals that you can meet your immediate financial obligations without a fire sale on your stock, which points to strong liquidity and a solid financial footing.

The Cash Conversion Cycle: An Efficiency Gauge

While the first two ratios provide a snapshot of your liquidity, the Cash Conversion Cycle (CCC) measures efficiency over time. It tells you exactly how long it takes (in days) for your business to turn its investments in inventory back into cash from sales.

A shorter CCC is always better. It means your money isn't stuck in products on a shelf or in unpaid customer invoices. Instead, it's flowing back to you faster, ready to be reinvested for growth.

Figuring out your CCC involves three parts:

- Days Sales Outstanding (DSO): How many days does it take to get paid after you make a sale?

- Days Inventory Outstanding (DIO): How long does your inventory sit before it's sold?

- Days Payables Outstanding (DPO): How many days do you take to pay your own suppliers?

The final calculation brings it all together: CCC = DSO + DIO - DPO

For example, say it takes you 45 days to collect from customers (DSO) and 60 days to sell your stock (DIO), but you pay your suppliers in 30 days (DPO). Your CCC would be 75 days (45 + 60 - 30). That’s two and a half months where your cash is tied up in each cycle. The goal is to shrink that number.

On that front, there's good news. In 2024, companies across the Middle East saw a 5.6% improvement in optimising their working capital, effectively shaving six days off their net working capital cycle.

Of course, to measure any of this accurately, you need a solid foundation in your financial record-keeping. This guide to UAE Business Accounting is a great place to start. When your books are in order, calculating these ratios becomes straightforward, and using the right tools can make all the difference. Check out our guide on the best accounting software in the UAE to see how technology can help.

Common Working Capital Headaches for MENA SMEs

Knowing your financial metrics is one thing, but living the day-to-day reality of running a small or medium-sized business in the MENA region is another. Many profitable companies find themselves wrestling with cash flow problems that turn good numbers on a spreadsheet into real-world operational nightmares. Getting to grips with these common pain points is the first step to solving them.

It's a classic story: sales are strong, but the bank account is empty. The biggest hurdle for many isn't a lack of business, but the long, frustrating wait to get paid, especially when working with large corporate or government clients who have their own lengthy payment procedures.

The Long Wait for Payments

Waiting 60, 90, or even 120 days for an invoice to be settled can be agonizing for a small business. This creates a huge cash flow gap and sends your Days Sales Outstanding (DSO) metric through the roof.

Picture a construction subcontractor in the UAE who has just wrapped up a big project for a property developer. The job is done, the invoice is sent, but the payment terms mean the money won't land for another three months. In the meantime, they have workers to pay, materials to buy for the next job, and rent to cover. That long wait puts a massive strain on their working capital and puts their growth plans on hold.

The Inventory Balancing Act

Another common headache is getting inventory right. Between unpredictable supply chains and fluctuating customer demand, it’s incredibly tough to keep just the right amount of stock on hand. Get it wrong, and you end up with a high Days Inventory Outstanding (DIO).

Think about a retailer in Saudi Arabia gearing up for a huge shopping festival. They buy a massive amount of stock, expecting a sales boom. But if that boom doesn't quite materialize, they're left with a warehouse full of unsold products. That inventory is literally cash tied up on a shelf—money that could have been spent on marketing or hiring new staff. Every day it sits there, it’s choking their working capital.

The real struggle for most MENA SMEs is a simple timing mismatch: they have to pay their own bills quickly, but their customers pay them slowly. This is the heart of most working capital problems.

Pressure from the Supply Chain

Finally, there’s the pressure from the other side: suppliers. Keeping them happy often means paying them on time, which leads to a short Days Payables Outstanding (DPO). And while a good relationship with your suppliers is vital, paying them too fast can drain your cash before your own customers have paid you.

This forces a tricky balancing act. You might want to ask for longer payment terms to give yourself some breathing room, but you risk losing a great supplier to a competitor who can pay faster. It’s a classic squeeze, forcing businesses to pay out quickly while they wait patiently for money to come in.

These challenges don't exist in a vacuum. Broader economic trends can make things even tougher. When regional growth slows, it can put an extra squeeze on businesses already struggling with these internal cycles. As economic forecasts change, a company's ability to get funding and innovate becomes directly linked to how well it manages its cash. You can get a deeper look at these regional trends in reports from the World Bank on the MENA economy.

How to Optimize Your Working Capital

Once you've spotted the common pain points putting a squeeze on your cash flow, it's time to take back control. The good news is that smart working capital management isn't about making drastic, overnight changes. It's all about making small, consistent tweaks across the three pillars of your business: how you collect your money, how you pay your bills, and how you manage your stock.

Focusing on these areas helps you build a much more resilient and efficient financial engine. Let's dig into some practical, real-world strategies any SME owner can start using today to unlock that trapped cash and get back to growing.

Optimize Your Accounts Receivable

The single fastest way to improve your working capital is to get paid faster. Every day you can shave off your Days Sales Outstanding (DSO) is another day you have cash in the bank, not on someone else's balance sheet.

It all starts with clear communication and solid processes. If your invoices are vague or your follow-up is relaxed, you’re unintentionally sending the message that getting paid isn’t a top priority.

Here are a few tactics to bring that cash in sooner:

- Issue Clear and Prompt Invoices: Don’t let invoices sit on your desk. Send them the moment a job is finished or a product is delivered. Make sure the due date, payment options, and contact info are crystal clear.

- Offer Early Payment Incentives: A small discount, maybe 1-2% for paying within 10 days, can work wonders. It encourages clients to settle up long before the standard 30 or 60-day deadline hits. The small hit might be well worth the boost to your cash flow.

- Establish a Follow-Up System: Don’t leave collections to chance. Set up a simple, professional follow-up schedule. This could be an automated email a week before the due date, a polite call on the day it's due, and a consistent process for any overdue accounts.

Strategically Manage Your Accounts Payable

On the flip side, while you want to collect cash fast, you should aim to pay your own suppliers as slowly as your agreements allow—without burning any bridges, of course. Stretching out your Days Payables Outstanding (DPO) keeps cash in your business longer, where you can put it to work.

This is a bit of a balancing act. You need to protect your reputation as a reliable customer while using payment terms to your benefit.

The goal isn't to avoid paying your bills. It's about timing your cash outflows to better match your cash inflows. This strategic delay can prevent that all-too-common cash crunch where your own bills are due before your customers have even paid you.

One great way to manage this is to talk to your key suppliers. If you’ve been a good customer with a history of on-time payments, they might be open to extending your terms from 30 days to 45 or even 60. B2B Buy Now, Pay Later platforms can also formalize these extended terms, giving you the breathing room you need. You can see exactly how BNPL solutions enhance cash flow for UAE businesses in our detailed guide.

Streamline Your Inventory Management

Remember, every single item sitting on your warehouse shelves is cash tied up. Reducing your Days Inventory Outstanding (DIO) by getting smarter with your stock levels can free up a huge amount of working capital.

The trick is to find that sweet spot between overstocking (which traps cash) and understocking (which costs you sales). This isn’t about guesswork; it requires a bit of a data-driven mindset.

Here are a few ways to get more efficient with your inventory:

- Embrace Just-In-Time (JIT) Principles: You don't need a massive, complex system. The core idea is simple: order stock closer to when you actually need it. This immediately cuts down on storage costs and the risk of getting stuck with things you can't sell.

- Use Data for Better Forecasting: Look at your past sales data to spot trends and seasonal patterns. When you can more accurately predict demand, you can order the right amount of stock at the right time. No more shortages, no more gluts.

- Identify and Clear Slow-Moving Stock: Make it a habit to review your inventory and pinpoint items that are just collecting dust. A well-timed sale or a promotional bundle can quickly turn that dead stock back into valuable cash.

Tapping into Financial Solutions to Free Up Your Cash

So, you've optimised your internal processes, but cash is still tight. What's next? It might be time to look outside your business for a solution. Thankfully, the MENA market has a growing number of options designed specifically to help SMEs like yours unlock the cash that’s tied up on the balance sheet.

Think of it as turning tomorrow's revenue into today's working capital. But not all solutions are created equal. Getting to grips with how each one works is key to picking the right fit for your business, your industry, and your specific cash flow challenges.

A Closer Look at Your Options

Invoice Discounting

At its core, invoice discounting is a simple concept: why wait 30, 60, or even 90 days for a customer to pay when you can get most of that cash right now? This solution lets you sell your unpaid invoices to a third party for an immediate cash advance.

You get a large chunk of the invoice value upfront, which can be a game-changer for covering payroll, buying supplies, or jumping on a new opportunity. The trade-off is a small fee, and you’re usually still the one who has to chase your customer for the final payment. It’s a direct and powerful way to inject liquidity into your business when you need it most.

Want to dig deeper? You can get a clearer picture by exploring the fundamentals of how invoice discounting works for SMEs.

B2B Buy Now, Pay Later (BNPL)

You've probably seen BNPL for consumer shopping, but it’s becoming a powerful tool in the B2B world, too. It lets your business customers buy from you today but spread their payments over time. A BNPL provider typically pays you, the supplier, upfront and then handles collecting the instalments from your buyer.

The big win here is that it can seriously boost your sales. By making it easier for customers to buy, you can encourage bigger, more frequent orders. You also get to offload the credit risk and the hassle of collections. The main thing to watch is the transaction fees, as they'll eat into your profit margins if you don't account for them in your pricing.

Dealer Financing

If you’re in an industry like automotive, you know that holding inventory is a massive cash drain. Dealer financing or dealer network platforms tackle this head-on. They create a financial bridge between manufacturers, distributors, and dealers, allowing businesses to stock up on inventory without paying for it all upfront.

This is a huge advantage. It means a car dealership or electronics retailer can have a fully stocked showroom, ready to make sales, without tying up all their working capital in inventory.

This approach directly fuels sales and strengthens the entire supply chain. However, these platforms are often highly specialized and might not be as flexible as other options. The terms can also get complicated, so it’s important to read the fine print.

Traditional Bank Overdrafts

The bank overdraft is the classic safety net. It’s a pre-agreed limit that lets you spend more than you have in your business account, giving you a buffer for those unexpected short-term cash crunches.

The beauty of an overdraft is its flexibility—you only use it when you need it and only pay interest on the amount you’ve actually used. The catch? You’ll need a solid credit history and may have to put up collateral to get one. The interest rates can also be steep, and banks have the right to change the terms or even recall the facility, sometimes with very little warning.

Comparing Your Choices

To make the right decision, it helps to see these options side-by-side. Each has its place, but the best one for you depends entirely on your business model and immediate needs. Here is a breakdown of the key considerations for each.

Invoice Discounting

- How It Works: Selling your unpaid customer invoices to a third party for an immediate cash advance.

- Best For: Businesses with long payment cycles and reliable B2B customers.

- Key Advantage: Quick injection of cash to improve immediate liquidity.

- Consideration: Incurs a fee and you often remain responsible for collections.

B2B BNPL

- How It Works: A third party pays you upfront for a sale, while your business customer pays them back in instalments.

- Best For: Suppliers looking to increase sales volume and average order value.

- Key Advantage: Boosts sales by removing payment barriers for your customers.

- Consideration: Transaction fees can reduce profit margins on each sale.

Dealer Financing

- How It Works: A platform facilitates financing so dealers can acquire inventory without paying for it upfront.

- Best For: Retailers/dealers in inventory-heavy sectors (e.g., auto, electronics).

- Key Advantage: Solves the massive challenge of inventory financing.

- Consideration: Often industry-specific and can have complex terms.

Bank Overdraft

- How It Works: A pre-approved line of credit from your bank that you can draw on as needed for short-term gaps.

- Best For: Businesses needing a flexible safety net for unpredictable cash flow.

- Key Advantage: Highly flexible; you only pay for what you use.

- Consideration: Requires strong credit, potential collateral, and can have high-interest rates.

Choosing the right partner can make all the difference in turning a cash flow challenge into a growth opportunity.

The scale of this issue in our region is massive. A 2024 analysis from PwC found that a staggering US$54.7 billion is trapped on the balance sheets of publicly listed companies in the Middle East alone. This highlights a huge, untapped potential for businesses to release cash and reinvest it back into their operations. You can read more of these insights on the regional working capital landscape from PwC. While a platform like Comfi doesn't directly provide financial services, many of our clients have successfully used our payment management tools to get their own financial house in order, which allowed them to unlock the working capital they needed to grow.

Got Questions About Working Capital? We’ve Got Answers

Even with a solid plan in place, it’s normal to have questions pop up about the day-to-day reality of managing your business’s cash flow. Let's tackle some of the most common ones we hear from business owners.

Can a Business Be Profitable but Still Run Out of Cash?

It’s a surprisingly common trap, and the answer is a definite yes. Profitability is what’s on your income statement, but cash is what’s in your bank account. You can be racking up profitable sales, but if your clients are taking months to pay their invoices, that profit is just a number on a page.

Think of it this way: if all your cash is tied up in unsold inventory or outstanding invoices, you can’t pay your suppliers, staff, or rent. This is exactly why obsessing over working capital is just as important as chasing profits.

I Want to Improve My Working Capital. Where Do I Even Start?

The best place to begin is by understanding your cash conversion cycle. It sounds technical, but it’s really about figuring out how long it takes for the money you spend on inventory and operations to come back into your business as cash from sales.

You'll want to calculate three key numbers: Days Sales Outstanding (DSO), Days Inventory Outstanding (DIO), and Days Payables Outstanding (DPO). This exercise acts like a diagnostic test, showing you precisely where your cash is getting stuck. For many businesses, the fastest win is to work on getting paid quicker, which means bringing that DSO number down.

Getting a handle on these three metrics is non-negotiable. They give you a clear map to spot the bottlenecks and free up the cash you need to run and grow your business.

How Often Should I Be Looking at My Working Capital?

This isn’t something you can just set and forget. For most SMEs, sitting down for a proper review once a month is a good habit. It keeps you connected to the financial pulse of your business.

That said, if you’re in a fast-paced industry or your business is growing quickly, you’ll want to check in weekly. Keeping a regular eye on your cash flow, who owes you money, and who you need to pay helps you spot trouble long before it becomes a crisis.

Ready to take control of your payments and build a healthier cash flow? Comfi gives you the tools to manage your payment cycles effectively, helping clients unlock the working capital they need to grow. See how it works at https://comfi.ai/get-started.