Top Payment Gateway UAE Solutions for Your Business in 2026

If you're running an SME in the UAE, there's a fair chance your finance team is still spending too much time on payment admin. One customer pays by bank transfer. Another asks for a card link. A third wants instalments at checkout. Meanwhile, your team is matching receipts, chasing remittances, and holding shipments because cash hasn't landed where it should.

That friction looks small when viewed line by line in a spreadsheet. In practice, it slows stock turns, delays supplier payments, and weakens visibility over what cash is available today.

A proper payment setup fixes part of that problem. The more important point is this. A payment gateway in the UAE shouldn't be treated as a checkout plug-in alone. It should be treated as the first layer of a broader cash flow system that helps you collect faster, operate with less manual work, and remove bottlenecks that hold back growth.

Beyond the Spreadsheet The Real Cost of Manual Payments

A familiar pattern shows up in growing UAE businesses. Sales are healthy, customer demand is real, but cash still feels tight. The issue often isn't revenue. It's the gap between selling, collecting, reconciling, and then using that cash to place the next order.

A wholesaler might send invoices in the morning, receive partial bank transfers through the week, and ask the finance team to confirm every payment before releasing stock. An online seller may still carry cash-on-delivery because some customers expect it, while card payments, wallet payments, and refund requests all sit in different systems. None of that looks dramatic on its own. Together, it creates delay.

Where the hidden cost shows up

Manual payment handling usually hurts in four places:

- Collections slow down: Customers who can't pay quickly often pay later than promised.

- Operations get blocked: Dispatch, delivery, and account management teams wait for finance confirmation.

- Reconciliation consumes staff time: Teams spend hours matching payment references, bank entries, and invoices.

- Decisions get weaker: Cash forecasting becomes guesswork when incoming funds aren't centralised.

Practical rule: If your team needs to check email, bank statements, and WhatsApp messages to confirm one payment, your process is too expensive.

The cost isn't only labour. Manual flows also create avoidable mistakes. Payments get misallocated. Orders are released against the wrong account. Refunds take too long. Customers lose confidence when they have to prove they already paid.

Why old habits stop scaling

Many owners accept these delays because that's how the business started. Bank transfers were manageable at low volume. Cash-on-delivery helped early sales. Offline approvals felt safe. But once order volume rises, those same habits start restricting growth.

A finance function should help the business move faster, not act as a checkpoint between sale and fulfilment. That's where modern payment infrastructure changes the conversation. Instead of treating payment collection as an admin task, strong operators treat it as a lever for cleaner cash flow, lower friction, and better control.

What a Payment Gateway Is and How It Works

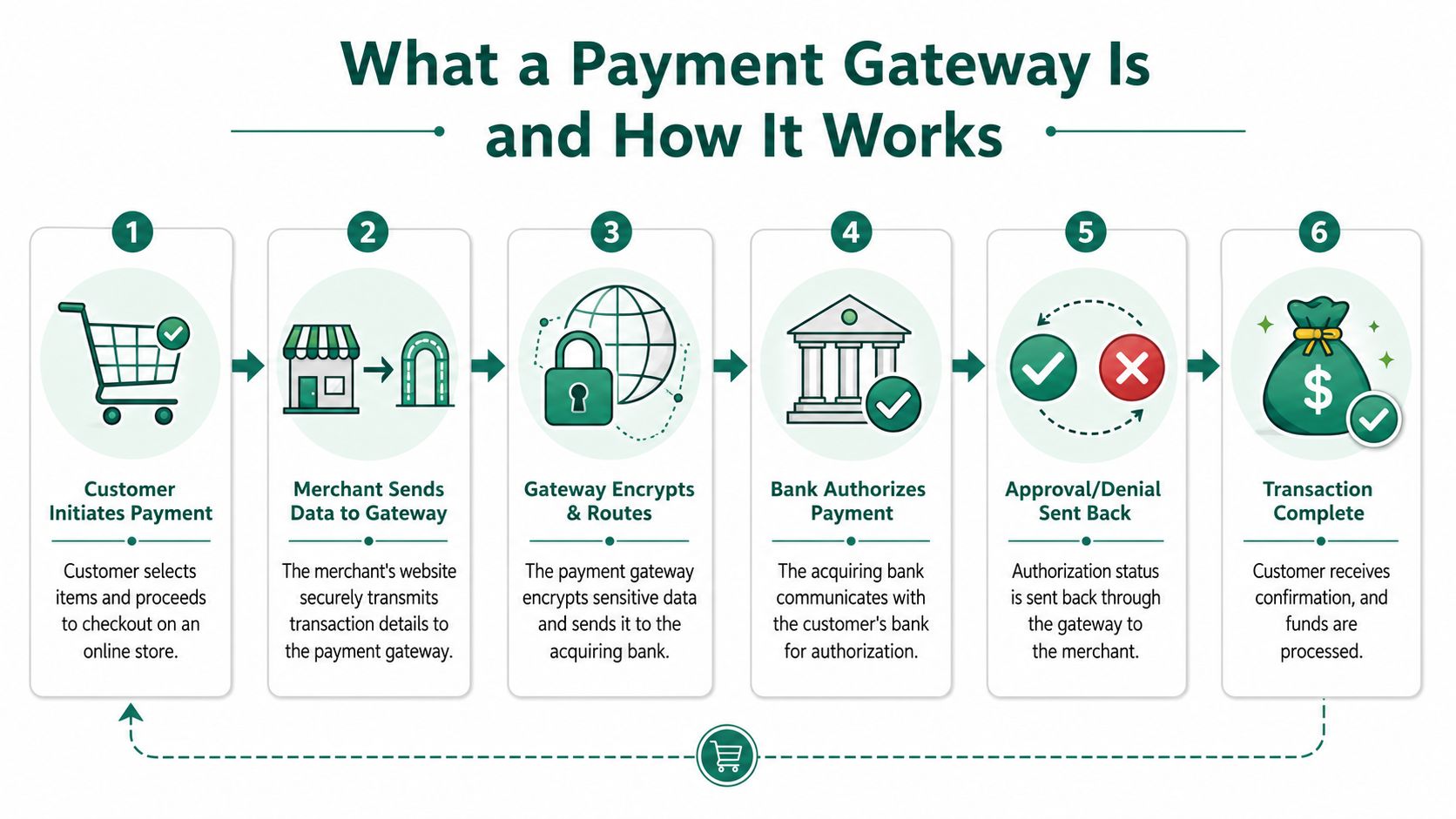

A payment gateway is easiest to understand as your digital cashier, security guard, and messenger in one service. It takes payment details from the customer, sends them through the right banking channels, checks whether the transaction should be approved, and returns the result to your website or invoicing system.

For a business owner, the point isn't the technology stack. The point is automation. A good gateway replaces manual checking with a controlled process that works the same way every time.

The basic flow

Here is what happens in practical terms:

- The customer starts the payment

- They choose card, wallet, or another method at checkout.

- Your business sends the payment request

- Your website, app, or payment link passes the transaction details securely to the gateway.

- The gateway protects and routes the data

- The gateway encrypts the information and sends it to the acquiring bank.

- Banks check whether the payment can go through

- The acquiring bank contacts the customer's issuing bank for approval or rejection.

- The answer comes back

- The gateway passes that response back to your system in real time.

- You and the customer get a result

- The order is confirmed, declined, or flagged for further authentication.

Why this matters to finance teams

Without a gateway, digital collection becomes fragmented. Someone has to create links manually, verify receipts manually, and track failed attempts manually. With a gateway, those checks become part of the transaction flow itself.

That matters even more once you connect payments to your back office. Linking the gateway to your ERP closes the gap between sale, payment status, and reconciliation. If you're reviewing that layer, this note on ERP integration for finance operations is useful because it focuses on workflow rather than code.

A gateway doesn't just accept money. It standardises the way your business receives, verifies, and records money.

What to ask before you sign

Business owners don't need to become payments engineers, but they should ask direct questions:

- Can it support your channels: online checkout, payment links, invoices, or recurring billing?

- Can your team reconcile easily: clean reporting matters as much as acceptance.

- Can it handle your customer mix: local and international cards, wallets, and common checkout behaviours.

- Can it scale cleanly: today's workaround often becomes tomorrow's reporting problem.

If you want a plain-language view of how providers structure secure online payment solutions, that guide is a useful companion reading before vendor discussions.

The Payment Gateway UAE Landscape for SMEs

A typical UAE SME feels the payment issue before it sees it in a dashboard. Orders come in, customers ask to pay by card or wallet, the team sends a bank transfer request instead, then finance waits for proof of payment and chases reconciliation later. That delay slows fulfilment, ties up staff time, and creates pressure on cash flow.

The market has already moved past that model. The UAE's payment gateway market is expanding quickly, and digital payments now account for the majority of e-commerce transactions, according to this UAE payments market analysis. For SMEs, the point is straightforward. Digital collection is no longer a channel upgrade. It is a baseline operating requirement.

What UAE customers expect at checkout

Customer expectations in the UAE are shaped by a mixed buyer base. Residents, expatriates, tourists, and cross-border buyers do not all want to pay the same way. A gateway has to support that reality. Card acceptance matters. Wallet support matters. Multi-currency support matters if the business sells beyond a narrow local customer segment.

Reliability matters too. A provider that accepts the right payment methods but creates settlement confusion or frequent support delays will still cause operational drag. In practice, SMEs should judge a gateway less by its sales pitch and more by how clearly it handles approval rates, settlement timing, refunds, and reporting.

Regulation affects finance outcomes

Regulation is not just a legal check box. It affects risk, approval confidence, and the amount of internal control the finance team needs to build around collections.

In the UAE, serious providers are expected to meet the Central Bank's requirements and established security standards such as PCI DSS and 3D Secure authentication. That reduces exposure to fraud and chargeback disputes, but it also does something more practical. It gives management confidence that the payment process can scale without creating a control problem later.

Choosing for the next bottleneck, not just today's checkout

Many SMEs make a narrow decision. They choose a gateway to collect money online, then discover three months later that their real constraint is working capital.

A good gateway should fit the business you are building, not just the transactions you are processing this week. If settlements are slow, supplier payments still need funding. If customers want instalment options, conversion may depend on BNPL. If invoices are paid on long terms, invoice discounting can matter more to liquidity than the gateway itself. The gateway is the entry point. The bigger gain comes from connecting collections to modern cash flow tools that remove pressure from day-to-day operations.

For SMEs reviewing providers, I would focus on four questions:

- How clear is settlement reporting: Finance needs a clean view of fees, reversals, refunds, and payout timing.

- Does the currency setup match your buyer mix: International cards and non-AED billing can affect conversion and reconciliation.

- Can support resolve payment issues quickly: A failed transaction during a busy sales period becomes a revenue issue fast.

- Will the setup support international selling: SelfServe's guide for international payments is a practical reference for merchants planning multi-currency and cross-border checkout options.

The strongest SMEs in the UAE do not treat a payment gateway as the full payments strategy. They use it as the first layer in a tighter system for collection, reconciliation, and cash flow control.

How Gateways Improve Operational Performance

A familiar UAE SME pattern looks like this. Sales closes the order today. Finance waits for a transfer slip on WhatsApp, someone checks the bank portal, customer service holds the order, and the stock sits in the warehouse for another day. The sale exists, but the cash process is still manual.

That delay shows up everywhere. Teams spend time chasing proof of payment, resolving mismatched amounts, and answering avoidable order queries. For a finance lead, the question is simple. Does the gateway shorten the path from sale to usable cash and reduce operating effort at the same time?

A well-set gateway improves operating rhythm across the business, not only at checkout.

When payment confirmation is automated, sales can collect faster, fulfilment can release orders sooner, and finance can reconcile against a cleaner record. Staff stop stitching together screenshots, bank entries, and invoice notes just to confirm what was paid.

The gains are practical:

- Sales confirms orders faster: Reps can send links and collect payment without waiting for manual bank verification.

- Finance spends less time on exceptions: Transaction records, refunds, and failed attempts sit in one system instead of scattered across emails and spreadsheets.

- Operations releases orders with less friction: Approved payments move into fulfilment with fewer internal checks.

- Customer service handles fewer status disputes: Customers receive clearer confirmation and have fewer reasons to ask whether payment went through.

I have seen this matter more than any feature checklist. If finance is still acting as a payment control desk, headcount gets pulled into low-value work instead of cash planning and supplier management.

Payment choice also affects operating performance because it changes how many orders complete on the first attempt. In the UAE market, card-only checkout often leaves money behind, especially on mobile and higher-ticket purchases. A sensible mix usually includes cards, wallets, and, where order values justify it, BNPL.

The trade-off needs judgment. More payment methods can improve completion rates, but too many plug-ins can create reporting problems and support issues. SMEs usually get better results from a smaller set of payment methods that finance can track cleanly than from adding every option available.

For most businesses, the operating standard is straightforward:

- Keep cards as the base layer: They still cover the broadest range of customer payments.

- Add digital wallets where mobile usage is high: They reduce input friction and speed up checkout.

- Use BNPL selectively: It can help conversion, but it matters more when it supports basket size and cash collection in a controlled way.

- Keep cash on delivery only if the margin supports it: If returns, failed deliveries, and collection delays erode profit, remove it.

The common failure points are usually internal, not technical.

One business runs a gateway, a separate wallet app, manual invoice collection, and three different reporting exports. Another adds payment methods without assigning anyone in finance to monitor settlement timing, refund leakage, and fees. A third improves checkout but leaves the post-payment workflow unchanged, so staff still intervene order by order.

A payment gateway should reduce admin, tighten control, and shorten the time between invoice and cash receipt. That is the operational win. The bigger advantage comes after that, when the payment layer connects to tools that solve the cash timing pressure behind the sale.

Drive Growth with Smart Cash Flow Tools

A finance team in the UAE can fix checkout, speed up payment acceptance, and still run short on working capital by the end of the month. The pressure usually shows up elsewhere. Supplier payments fall due before customer invoices are collected, stock has to be replenished before earlier sales convert into cash, and larger orders create strain instead of relief.

A payment gateway improves collection at the point of sale. Growth usually comes from connecting that payment layer to funding tools that deal with timing across the full order cycle. If you want a practical framework, this guide on payments and receivables for finance teams explains how those pieces work together.

Where cash flow still gets stuck

The pattern is familiar across SMEs:

- Customer terms run longer than supplier terms: Cash leaves the business before it comes back in.

- Inventory ties up liquidity: Restocking decisions compete with payroll, rent, and supplier commitments.

- Larger deals increase pressure: Revenue rises on paper while usable cash stays delayed.

That is why finance should treat the gateway as the collection layer, not the whole answer.

For B2B sellers, invoice discounting can release cash from approved invoices that would otherwise sit in receivables until the due date. For merchants selling to business buyers or higher-ticket customers, Buy Now, Pay Later can support order flow while improving collection timing for the seller, provided the terms, fees, and approval logic are controlled properly.

One operating model, with fewer cash surprises

The stronger setup is a connected one. The gateway accepts payment. The cash flow tool addresses timing. Finance gets a clearer view of receivables, expected settlement, and upcoming payable pressure because those items are no longer scattered across separate systems and manual follow-ups.

One example in the UAE market is Comfi, which supports invoice discounting, Buy Now, Pay Later terms, and dealer financing through a digital workflow. Used well, that kind of setup helps suppliers access working capital tied up in invoices and gives buyers more flexible payment timing without pushing the operational burden back onto the seller's internal team.

Faster collection helps. Better control over cash timing across purchasing, invoicing, and settlement is where the biggest business benefit sits.

Why this matters in automotive and distribution

This issue is especially visible in sectors where order values are high and stock has to keep moving. A dealer with cash tied up in vehicles delays restocking. An electronics distributor with receivables outstanding may miss the next purchase cycle. A wholesaler can win new business and still feel constrained because customer terms stretch beyond what the balance sheet can absorb.

In those cases, the gateway does one job well. It gets money flowing through the right channel. Cash flow tools make that money usable at the point the business needs it. That is what improves purchasing power, protects supplier relationships, and gives finance more control over growth.

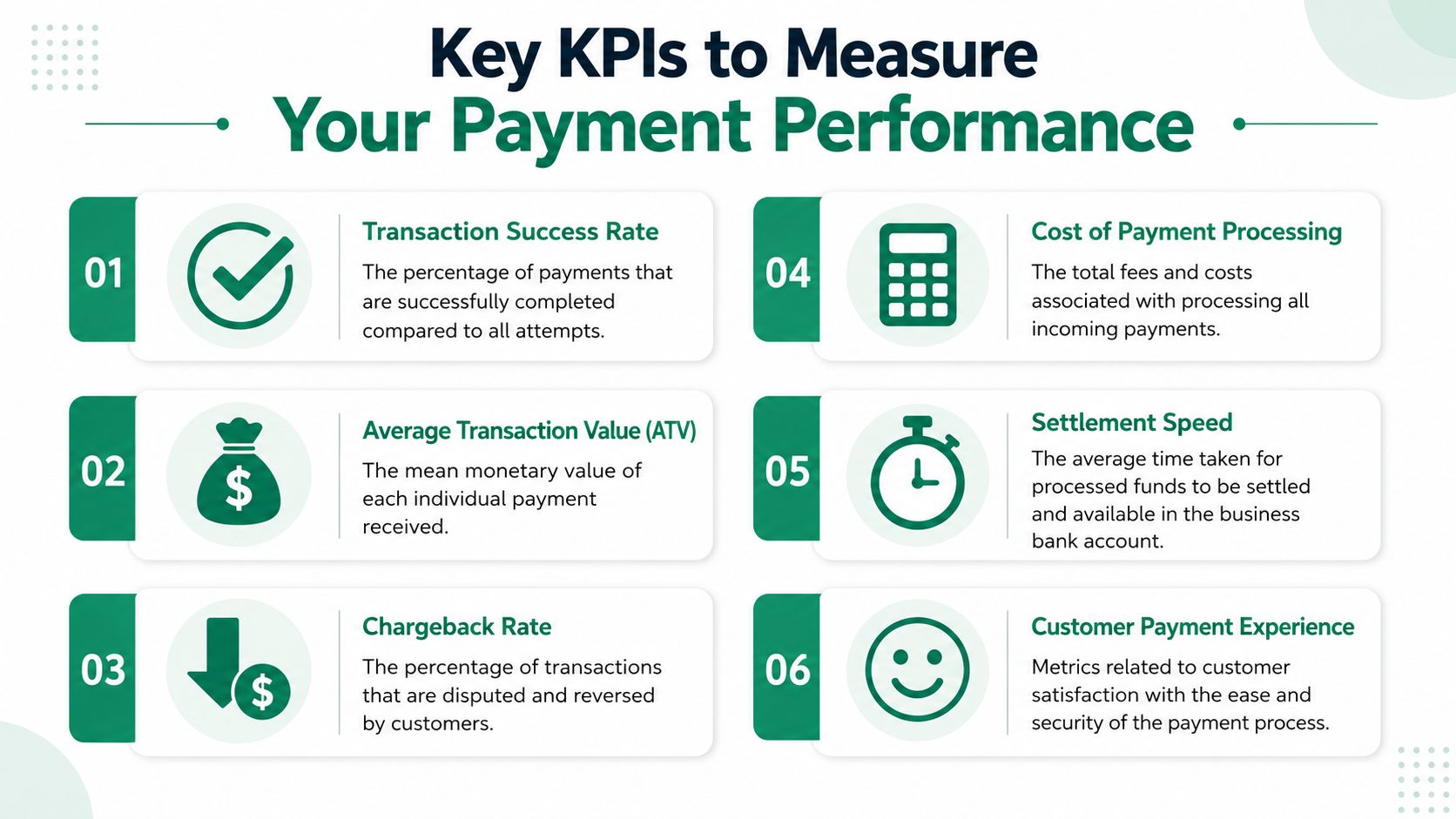

Key KPIs to Measure Your Payment Performance

Too many businesses install a gateway and then stop measuring. That's a mistake. Payment infrastructure should be monitored the same way you monitor gross margin, stock turns, or debtor ageing.

The right KPIs tell you whether your setup is improving collections or moving the same problems into a digital interface.

The metrics worth reviewing every month

- Transaction success rate: Track approved payments against total attempts. If this drops, sales may be leaking before you even see the order.

- Cart abandonment rate: If customers start checkout and don't finish, your payment flow may be too complex or poorly matched to customer preference.

- Average transaction value: Useful for seeing whether payment flexibility is supporting larger baskets or order sizes.

- Chargeback rate: Disputes affect margin, staff workload, and provider relationships.

- Settlement speed: Finance should know how quickly processed payments become usable cash.

- Cost of payment processing: Review transaction fees, fixed gateway fees, and operational overhead together, not separately.

What improves these numbers

In the UAE, fraud control and customer experience have to work together. Payment gateways must employ 3D Secure authentication and machine learning-based fraud detection to combat fraud and cart abandonment, while multilingual support in Arabic and English is critical for improving transaction success rates and customer retention, according to Stripe's overview of payments in the United Arab Emirates.

That should shape your KPI review. If approval rates are weak, don't assume fraud settings should be loosened. Check whether authentication flow is working properly, whether language support matches your customer base, and whether a specific payment method is underperforming.

Build one reporting routine

A simple monthly review is enough for most SMEs if it includes both finance and commercial input.

- Finance reviews: fees, settlements, failed payments, refund timing.

- Sales or e-commerce reviews: checkout drop-off, payment method usage, customer complaints.

- Operations reviews: release delays tied to payment confirmation.

For teams trying to tighten that discipline, this guide on payments and receivables processes is a practical starting point because it focuses on how collection data connects to working capital management.

The best payment dashboard isn't the one with the most charts. It's the one that tells you why cash is late, why approvals fail, and where margin is leaking.

Your Gateway to Sustainable Business Growth

A payment gateway is now basic business infrastructure in the UAE. But treating it as a checkout feature alone undersells its role. Its full value comes when payment collection, reconciliation, and cash timing work as one system.

For SME owners and finance leaders, that changes the conversation. You're no longer asking only how to accept cards online. You're asking how to reduce payment friction, shorten the path from sale to cash, and stop receivables or inventory from constraining the next stage of growth.

What a sound setup looks like

A durable approach usually includes three parts:

- A compliant gateway foundation: To operate a payment gateway, entities need a Payment Service Provider licence from the Central Bank of UAE, with minimum capital of AED 1M–10M and UAE-hosted servers for data localisation, as explained in this summary of UAE gateway requirements.

- A payment mix that fits customer behaviour: Cards, wallets, and selective flexible payment options.

- A cash flow layer behind the gateway: So the business can use incoming demand without waiting for every invoice cycle to end.

The businesses that benefit most from a modern payment gateway UAE strategy are usually the ones that tie payments back to commercial execution. They restock faster. They spend less time reconciling. They make fewer decisions based on incomplete cash data.

If you're revisiting your broader payment model, it's worth also reviewing how B2B payments workflows affect collections, supplier relationships, and order velocity across the business.

A cleaner payment process won't solve every finance problem. It will, however, remove one of the most common operational drags that keeps otherwise strong UAE SMEs from growing at the pace their market allows.

If your business is collecting digitally but still feeling pressure from invoice delays, stock constraints, or uneven cash timing, Comfi is worth reviewing as part of the wider setup. It supports invoice discounting, Buy Now, Pay Later terms, and dealer financing through a digital workflow that helps businesses access working capital tied up in invoices and inventory while keeping operations moving.