Financial Planning for SMEs: A MENA Growth Framework 2026

Revenue is rising. Orders are coming in. Your team is busy. Yet you still pause before saying yes to a new supplier deal, a larger inventory purchase, or a new market push.

That tension is common across SMEs in MENA. Profit on paper doesn't always mean cash in the bank. A business can look healthy from the outside while the owner spends every week juggling supplier due dates, customer payment delays, payroll timing, and stock decisions.

That's where financial planning becomes practical. Not academic. Not just for large corporates. It's the discipline that helps you decide what you can afford, when to move, where the pressure points sit, and how to keep growth from turning into strain.

The Hidden Brake on Your Business Growth

A wholesaler in Dubai closes a strong month. Sales look good. New buyers are asking for larger orders. A promising supplier offers better pricing if the business can commit to more volume.

But there's a problem. Several customer invoices still haven't been paid. Cash is tied up in stock. Rent, salaries, and supplier obligations won't wait. So the owner does what many founders do. He delays the growth decision, chases collections, and hopes timing works out.

That pattern emerges in many SMEs. The issue isn't always weak demand. Often, it's the gap between revenue and usable cash.

Why intention isn't enough

Many business owners know they need a proper plan. They've felt the pain of reacting too late. They've seen how one delayed payment can distort an entire month.

That gap between knowing and doing is familiar more broadly too. According to the 2017 Savings Index by National Bonds Corporation, more than 41% of UAE residents and savers had planned to begin proper financial planning, yet a significant portion delayed action until their mid-thirties (National Bonds reference). The lesson applies to businesses as much as individuals. Good intentions don't create resilience. Systems do.

Practical rule: If your decisions depend on checking the bank balance first, you don't yet have a financial plan. You have a cash reaction habit.

What the real brake looks like

For SMEs, the hidden brake usually shows up in familiar ways:

- Late customer payments: Sales are booked, but operating cash arrives too slowly.

- Inventory drag: Money sits in products instead of funding the next opportunity.

- Poor timing visibility: You know annual targets, but not next month's pressure points.

- Reactive decisions: You buy, hire, or discount based on urgency rather than strategy.

Financial planning fixes that by turning finance into a forward-looking management tool. It helps you map upcoming obligations, expected inflows, likely shortfalls, and growth capacity before stress appears.

A founder who plans properly doesn't stop problems from happening. They spot them earlier, rank them better, and respond with options instead of panic.

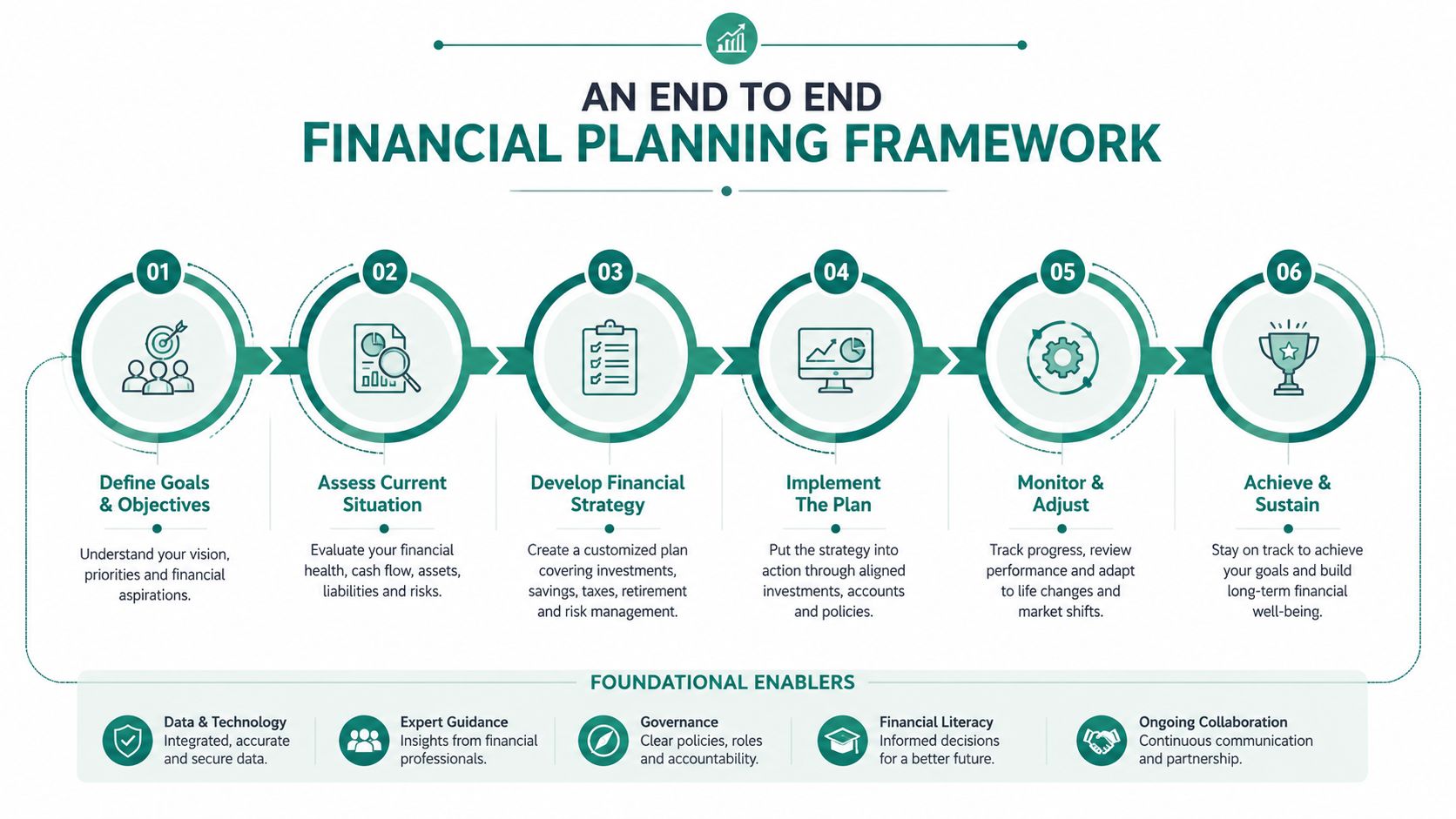

What Financial Planning Really Means for an SME

For an SME, financial planning is less like bookkeeping and more like a GPS for a business journey. Bookkeeping tells you where you've been. Financial planning helps you decide where you're going, how much fuel you need, and what route still works if traffic changes.

That distinction matters. Many owners confuse finance with record-keeping. Records matter, but they don't tell you whether you can add headcount, extend buyer terms, increase stock, or survive a slow quarter.

A useful plan connects daily operations to future choices.

The four pillars that make a plan useful

Think of your financial plan as the blueprint before construction starts. Without it, teams still work, but they often build in the wrong order.

Strategic forecasting

This is your forward view. You estimate likely sales, expenses, cash inflows, and cash outflows over the coming months. The aim isn't perfection. The aim is visibility.

A forecast answers questions like:

- Can we afford a bigger order next month

- Will receivables cover supplier payments on time

- What happens if a major client pays late

- How much cash buffer do we need

Operational budgeting

A budget translates strategy into operating limits. It tells each part of the business what level of spending fits current goals.

Good budgeting isn't about cutting everything. It's about choosing deliberately.

- Sales budget: How much commercial activity you expect to fund

- Procurement budget: What inventory or materials levels are realistic

- People budget: Whether hiring fits current capacity

- Overhead budget: What fixed costs the business can carry safely

Risk management

Every SME faces shocks. A customer delay, a supply interruption, a seasonal drop, or a cost increase can ripple through the whole company.

Risk management means identifying where one disruption could create a chain reaction. It also means deciding in advance what action you'll take if that happens.

The strongest plans don't assume smooth conditions. They assume reality.

Capital management

Capital management is a key area where many SMEs struggle most, focusing on how cash moves through the business and how quickly it returns after being committed.

It covers receivables, payables, stock, payment terms, and timing gaps. It also includes the tools you use to keep operations moving without freezing growth. If you want a stronger foundation for understanding how historical numbers support these decisions, this guide to financial reporting for SMEs is a useful companion.

A proper plan pulls all four pillars together. When one is missing, the business usually feels it somewhere else.

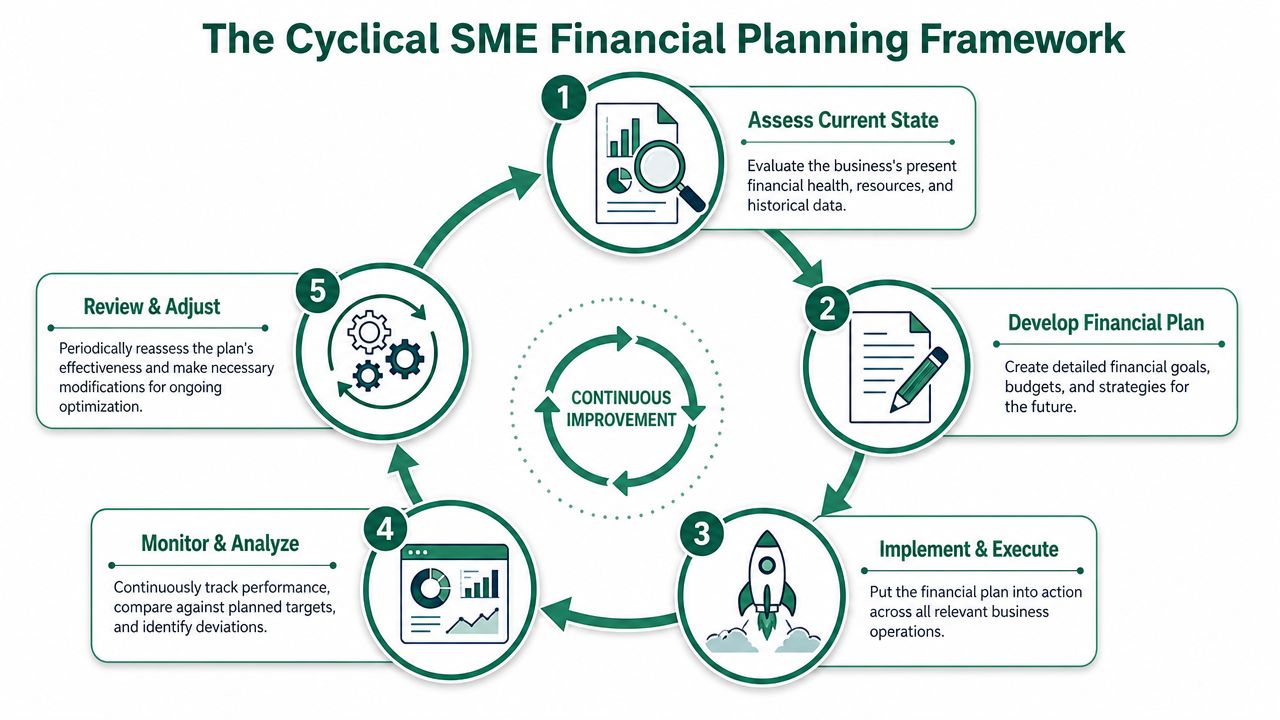

An End to End Financial Planning Framework

A strong financial plan isn't a document you write once and forget. It's a loop. You set direction, test assumptions, run the business, measure reality, and adjust.

That matters because SMEs don't operate in stable conditions for long. Customer demand shifts. Supplier timelines move. Costs change. The plan has to move with them.

Step one, define growth oriented goals

Start with decisions, not spreadsheets.

Don't write “grow revenue” and stop there. Tie the goal to an operational reality. For example, you might want to expand into a new emirate, increase average order size, shorten collection cycles, or carry more inventory before peak demand.

Useful goals tend to be specific in business terms:

- Sales expansion: Add a new buyer segment or widen product mix

- Cash discipline: Reduce dependence on last-minute collection chasing

- Operational scale: Support more orders without breaking supplier relationships

- Margin protection: Improve planning around discounting and procurement timing

Step two, forecast your financial future

Once goals are clear, build a simple forecast. Start with expected sales by month, then map when cash arrives. After that, list your expected outgoing cash, including suppliers, salaries, rent, logistics, software, and tax-related obligations.

Many owners fall into a common trap. They forecast revenue, but not timing. A good sales month can still create a cash squeeze if collections lag.

Include assumptions in plain words. If a buyer usually pays slowly, model that reality. If demand is seasonal, reflect that shape rather than using a flat monthly average.

Step three, build your operational budget

Your budget gives boundaries to each function. It tells operations how far they can commit, sales what type of deal still fits cash capacity, and leadership when spending should pause.

If tax timing affects your budgeting decisions, this practical guide to 2026 tax planning for business owners can help frame how owners think about obligations alongside growth planning.

Step four, choose the KPIs that matter

You don't need dozens of metrics. You need a short list that exposes stress early.

Focus on indicators that answer these questions:

- How quickly do we turn sales into cash

- How long is money trapped in stock

- Are we funding growth safely or stretching too far

- Which customers or products create timing risk

Step five, review and adapt continuously

Set a monthly review rhythm. Compare forecast to actuals. Look for misses that repeat. If receivables come in later than planned three months in a row, that's no longer a one-off issue. It's a structural input that belongs in the next forecast.

Decision habit: Review variances with your leadership team while there's still time to act, not after the month is already lost.

A plan becomes powerful when it changes decisions in real time. That's when finance stops being a record of what happened and starts becoming an operating system for what to do next.

Essential KPIs and Templates for Your Plan

Most SME plans break down for one reason. The owner can't see pressure building until cash gets tight.

KPIs solve that problem when they're tied to action. The point isn't to collect metrics for a board slide. The point is to spot friction in receivables, stock, margins, and customer quality before it damages operations.

The KPIs worth watching closely

Cash conversion cycle

This shows how long cash stays tied up between paying suppliers and collecting from customers. A longer cycle usually means more pressure on day-to-day operations.

If you want a practical breakdown of how this applies in practice, this guide to cash flow forecasting for growing businesses helps connect timing assumptions to actual planning decisions.

Days sales outstanding

DSO tells you how long customers take to pay. If DSO rises, cash arrives later even if revenue looks strong. That's often the earliest warning sign in a growing SME.

Working capital ratio

This gives a quick view of short-term financial health. It won't tell you everything, but it helps you judge whether current assets are comfortably covering current obligations.

Gross margin by product or customer segment

Not all sales improve the business equally. Some products move quickly and pay well. Others create hidden pressure through slower payment cycles, discounting, or return issues.

Inventory days

This matters most for trading businesses, distributors, and dealers. Slow-moving stock can tie up cash that the business needs elsewhere.

For subscription or account-growth businesses, planning should also connect customer retention to revenue durability. Teams working on recurring revenue may find this piece on boosting net revenue retention useful because it frames how expansion, churn, and account quality influence long-term financial planning.

Two simple templates every SME should maintain

A spreadsheet is enough if the structure is sound.

Cash flow projection

- Opening cash balance: What cash is available at the start of the period

- Expected collections: Customer payments by likely receipt date

- Supplier payments: Outgoings matched to actual due dates

- Payroll and fixed costs: Salaries, rent, software, utilities, transport

- Variable spending: Marketing, freight, seasonal procurement, project costs

- Closing cash balance: What remains after inflows and outflows

Basic profit and loss view

- Revenue line: Sales by category or channel

- Direct costs: Product or service delivery costs

- Gross profit: The amount left after direct costs

- Operating expenses: Team, office, systems, fulfilment, selling costs

- Operating result: Whether the core business is generating a healthy return

Track KPIs monthly, but investigate exceptions weekly. Waiting for month-end often means waiting too long.

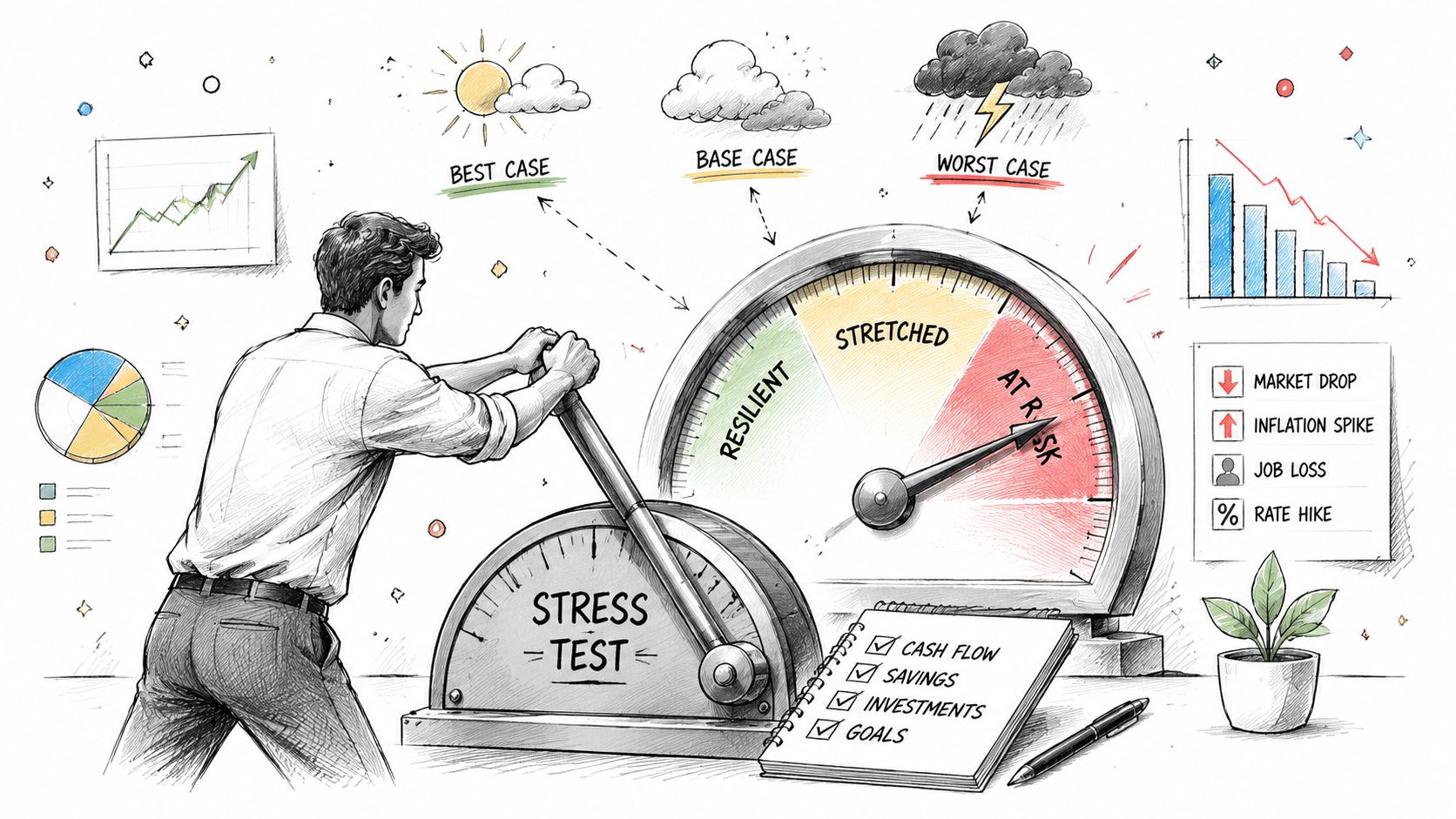

Stress Testing Your Financial Scenarios

A plan only proves itself when conditions stop being ideal.

Many SMEs create a forecast using expected demand and expected payment timing. Then reality interferes. A major client pays late. Shipping costs rise without warning. Seasonal demand softens just when inventory arrives.

Stress testing means running those “what if” situations before they happen, then deciding what response makes sense.

Scenario one, a major client pays late

A finance manager in Riyadh expects a large customer payment this month. That receipt is meant to cover supplier settlements and a restocking order.

Now remove that cash from the forecast and push it back by a full quarter. The first question isn't whether the client will eventually pay. The real question is what breaks in the meantime.

Look at:

- Supplier due dates: Which commitments become hard to meet

- Payroll timing: Whether operating cash stays protected

- Stock decisions: Whether replenishment needs to shrink or shift

- Sales impact: Whether delivery capacity falls because inventory can't be replaced

Scenario two, input or shipping costs rise suddenly

A distributor may still sell the same volume, yet margins and cash needs can deteriorate together if landed costs increase.

Model the higher cost into the months ahead. Then test two responses. First, hold prices steady and see how much margin disappears. Second, adjust pricing and estimate whether sales velocity changes.

This exercise helps you answer a painful but necessary question. Are you underpricing risk in order to preserve short-term volume?

Scenario three, seasonal demand drops below expectation

A retailer or dealer often enters a season with stock already committed. If demand dips, cash remains trapped while overhead continues.

Run a lower-demand version of your forecast and focus on timing:

- How long stock remains unsold

- How much working cash stays trapped

- Which discretionary costs can pause

- When you would need to renegotiate purchasing pace

A resilient financial plan includes a trigger point. If cash, collections, or inventory cross that line, management acts immediately.

Stress testing doesn't make a business pessimistic. It makes leadership calmer. When a disruption arrives, the team already knows the likely effect, the first actions to take, and which decisions must wait.

Integrating Working Capital Solutions for Growth

Traditional financial planning often assumes two familiar answers to a cash gap. Borrow from a bank or dilute ownership through equity. For many SMEs, neither is a good operational fit.

Banks can be slow, documentation-heavy, or restrictive. Equity may solve capital pressure, but it changes ownership and usually doesn't match short-term working cycles. That's why more SME finance leaders are building modern tools directly into their financial planning process.

One useful background read on the mechanics behind this is managing business finances effectively, especially if you want to connect day-to-day cash discipline with broader growth planning.

Use tools that match the problem

Different cash flow problems need different solutions. If you treat them all the same, you can end up solving the wrong bottleneck.

Invoice discounting for slow collections

When your business has completed the sale but cash is still waiting inside receivables, invoice discounting can help realize value from issued invoices. That makes it useful when late customer payment is the main constraint.

This tool fits businesses that are operationally healthy but collection timing creates strain. It can support supplier payments, stock replenishment, and smoother operating cycles without waiting for every invoice to mature.

B2B Buy Now Pay Later for order growth

Sometimes the issue isn't receivables. It's buyer hesitation. A customer wants to place a larger order but needs more breathing room on payment terms.

In those cases, Buy Now, Pay Later structures can support stronger purchasing behaviour while helping the seller maintain momentum. In the verified business context provided for this market, businesses using Comfi's capital solutions report up to 30% sales uplift and 20% new-customer growth (research context). The practical point isn't the brand. It's the planning lesson. Flexible payment structures can influence sales capacity, customer acquisition, and order size.

Dealer financing for inventory heavy businesses

Some sectors face a more physical form of cash lock-up. Automotive is one of the clearest examples.

In the UAE auto market, dealers face inventory holding periods of up to 180 days before vehicles sell, which ties up capital and slows restocking. When cash sits inside unsold vehicles for that long, the business can struggle to buy fresh inventory even when demand exists.

That matters in a market where the UAE auto finance market reached a valuation of AED 55 billion in 2023 (UAE auto finance market data). It also matters because smaller dealers may find institutional access uneven. Many UAE banks require a minimum car value of Dh 25,000 to qualify for auto financing, as they typically finance only 80% of the vehicle's value (auto finance eligibility context). Add the cost of used car funding, where typical interest rates are approximately 4.79% for 12 to 36 month terms and 5.29% for 37 to 60 month terms (used car financing market context), and it becomes clear why inventory liquidity needs its own planning response.

If automotive is part of your operation, it helps to understand how inventory timing affects your cash conversion cycle in practice.

The planning shift that matters

The main shift is strategic. Don't treat these tools as emergency patches. Build them into your plan as options for specific conditions.

- Use invoice-based tools when receivables timing is the pressure point

- Use flexible buyer terms when sales expansion is limited by payment friction

- Use inventory-linked structures when stock absorbs cash for too long

That approach turns financial planning into a growth framework rather than a survival exercise.

Turn Your Financial Plan into Decisive Action

Most SME owners don't need more finance jargon. They need a clear way to make better decisions under pressure.

That starts by seeing financial planning for what it really is. It's not a yearly admin task. It's the discipline that connects growth goals, realistic forecasting, operating budgets, meaningful KPIs, scenario testing, and cash flow tools that match the problem in front of you.

A good plan gives you timing visibility. A better plan gives you decision confidence. You know when to push, when to pause, and when to protect cash before strain spreads through the business.

If your business is growing but still feels financially tight, that's your signal. Don't wait for the next delayed payment, stock bottleneck, or seasonal dip to force action. Build the planning rhythm now. Review it monthly. Stress test it rigorously. Use modern solutions where they fit. Then let the plan guide your next move.

Financial freedom in an SME rarely comes from one big breakthrough. It comes from organised decisions made early, repeatedly, and with better visibility than the market around you.

If you want to turn planning into faster action, Comfi helps SMEs across MENA release cash tied up in invoices, offer flexible payment terms, and free up value from inventory so growth doesn't stall when cash flow gets tight.