Finance Manager Responsibilities: A Guide for UAE SMEs

If you're a finance manager at a UAE SME, the day usually starts before the rest of the business realises there's a problem. A key customer hasn't paid. Supplier due dates are close. Payroll is approaching. Sales says revenue is strong, but the bank balance tells a more complicated story.

That's why the best finance managers aren't just keeping books tidy. They're protecting the company's room to operate. They decide which payments move first, where risk is building, and whether growth is affordable or only looks good on paper.

Beyond Bookkeeping The Modern Finance Manager

A finance manager in a growing SME rarely has the luxury of treating finance as a month-end activity. Their primary work begins when receipts and payments stop lining up neatly. One overdue invoice can force awkward decisions about supplier timing, purchasing plans, or whether to delay a non-essential spend that another department assumed was already approved.

In practice, finance manager responsibilities sit at the centre of business continuity. The role covers reporting, controls, budgeting, receivables, payables, and the constant translation of raw transactions into decisions the leadership team can act on. If management wants to know whether it can hire, expand stock, negotiate better supplier terms, or absorb a slow-paying client, finance is the function that gives a usable answer.

That matters at a national level too. In the UAE, SMEs account for 63.5% of non-oil GDP and 96% of all companies, according to the UAE-focused finance manager overview on Indeed. In an economy with that much SME activity, finance discipline isn't just an internal admin function. It affects resilience, employment, and growth across the market.

What the role feels like on the ground

In a fast-moving company, the finance manager is often the person who sees trouble first. Sales may still be optimistic. Operations may still be buying. Leadership may still be focused on the next opportunity. Finance sees the mismatch between confidence and cash.

Practical rule: Profit can wait for the management accounts. Cash pressure shows up much earlier.

That's why modern finance leaders spend time building visibility, not just recording history. Good treasury habits, clear approval flows, and realistic short-term forecasts do more for stability than beautifully formatted reports delivered too late. If your team is still managing liquidity by scrolling through bank statements and scattered spreadsheets, it helps to understand stronger treasury management practices for SMEs.

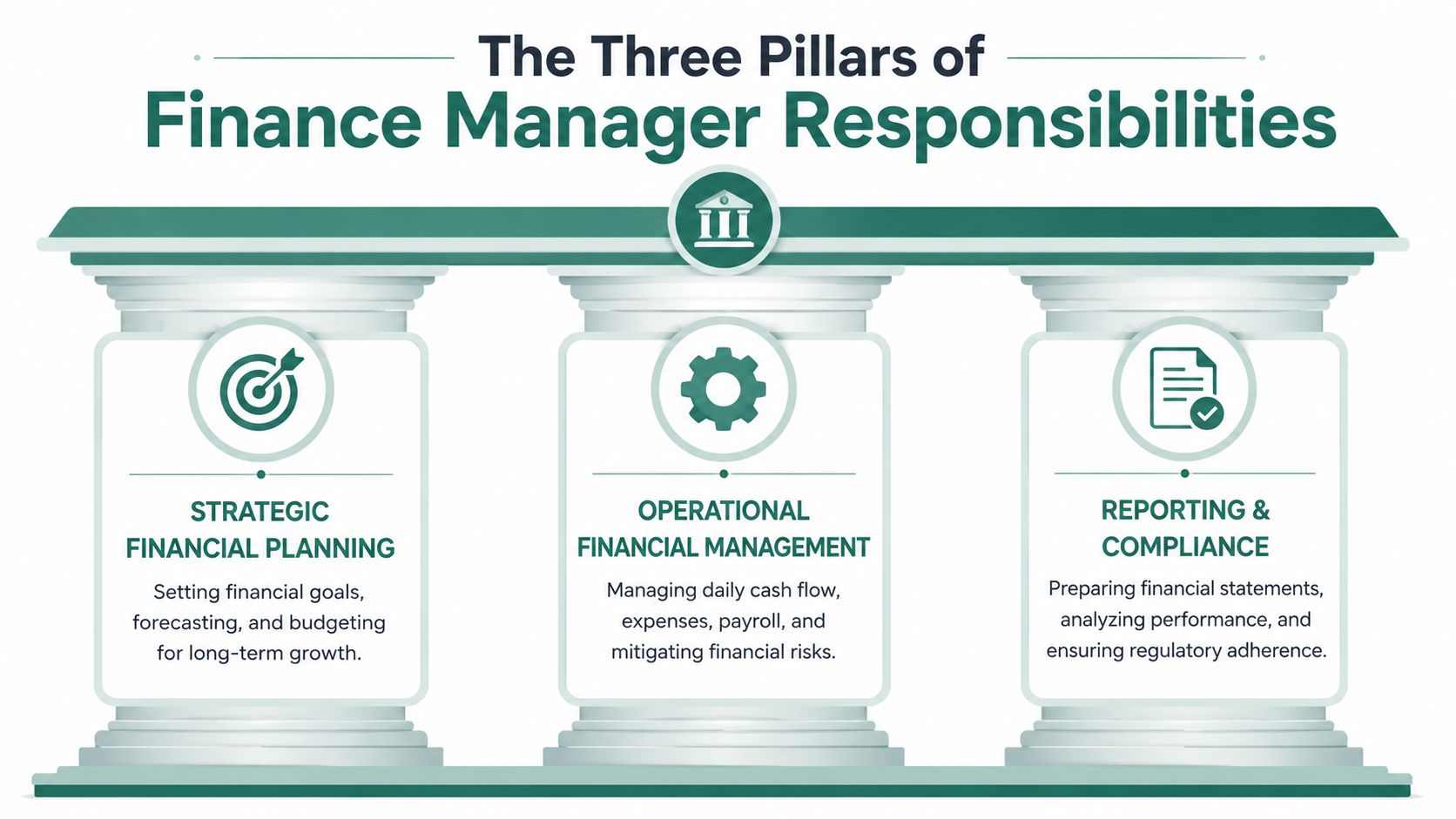

The Three Pillars of Finance Manager Responsibilities

The easiest way to understand finance manager responsibilities is to group them into three pillars. Most businesses focus heavily on the first pillar, appreciate the second, and underestimate the third. In UAE SMEs, that third pillar often decides whether the company feels stable or constantly under pressure.

Financial guardianship

This is the foundation. The finance manager owns the integrity of the numbers and the discipline around them. That includes making sure transactions are recorded properly, reconciliations are completed, payables and receivables are controlled, and reports are reliable enough for management, auditors, and regulators.

Without this pillar, every later decision gets weaker. Budgeting becomes guesswork. Forecasting becomes political. Leadership starts debating whose spreadsheet is right instead of debating what to do next.

Key responsibilities here usually include:

- Accurate reporting: Monthly, quarterly, and annual reporting that reflects commercial reality rather than rough estimates.

- Internal controls: Approval rules, segregation of duties where possible, and clear ownership over payments, expenses, and journal entries.

- Compliance discipline: VAT, payroll processes, audit readiness, and documentation standards that can stand up to review.

- Balance sheet control: Reconciliations that catch hidden issues early, especially in receivables, accruals, inventory, and intercompany balances.

Strategic partnership

A weak finance function reports what happened. A strong one helps leadership choose what to do next. That means the finance manager has to move beyond scorekeeping and become a decision partner.

The practical side of this pillar is often underappreciated. A good finance manager doesn't solely produce a budget. They challenge assumptions inside it. They ask whether projected sales are collectible, whether inventory buys are timed correctly, and whether margin assumptions survive after freight, discounts, and customer payment terms are considered.

A forecast isn't useful because it looks precise. It's useful because it forces the business to confront trade-offs early.

This pillar usually shows up in work such as scenario planning, budget reviews with department heads, variance analysis, and explaining performance in plain language to non-finance leaders. If operations wants to add headcount, finance should show the cash effect, not just the annual cost. If sales wants to offer longer terms, finance should model what that does to collections pressure.

Liquidity management

The role becomes operationally decisive as, in UAE practice, finance manager responsibilities extend beyond reporting into cash conversion control, including end-to-end finance operations, cash-flow forecasting, and daily liquidity management, as reflected in regional finance manager role expectations from Michael Page.

That sounds technical, but the question is simple: how quickly does the business turn commercial activity into available cash?

This pillar covers:

- Cash-flow forecasting: Looking ahead far enough to spot pressure before it turns into urgency.

- Working-capital control: Managing invoice timing, collection follow-up, supplier terms, and inventory decisions together rather than in silos.

- Payment prioritisation: Knowing what must be paid now, what can be negotiated, and what should never be delayed.

- Liquidity buffers: Keeping enough flexibility for ordinary disruption, because disruption is ordinary.

What doesn't work is treating cash flow as a by-product of accounting. By the time month-end reports confirm there was a problem, the business has already felt it.

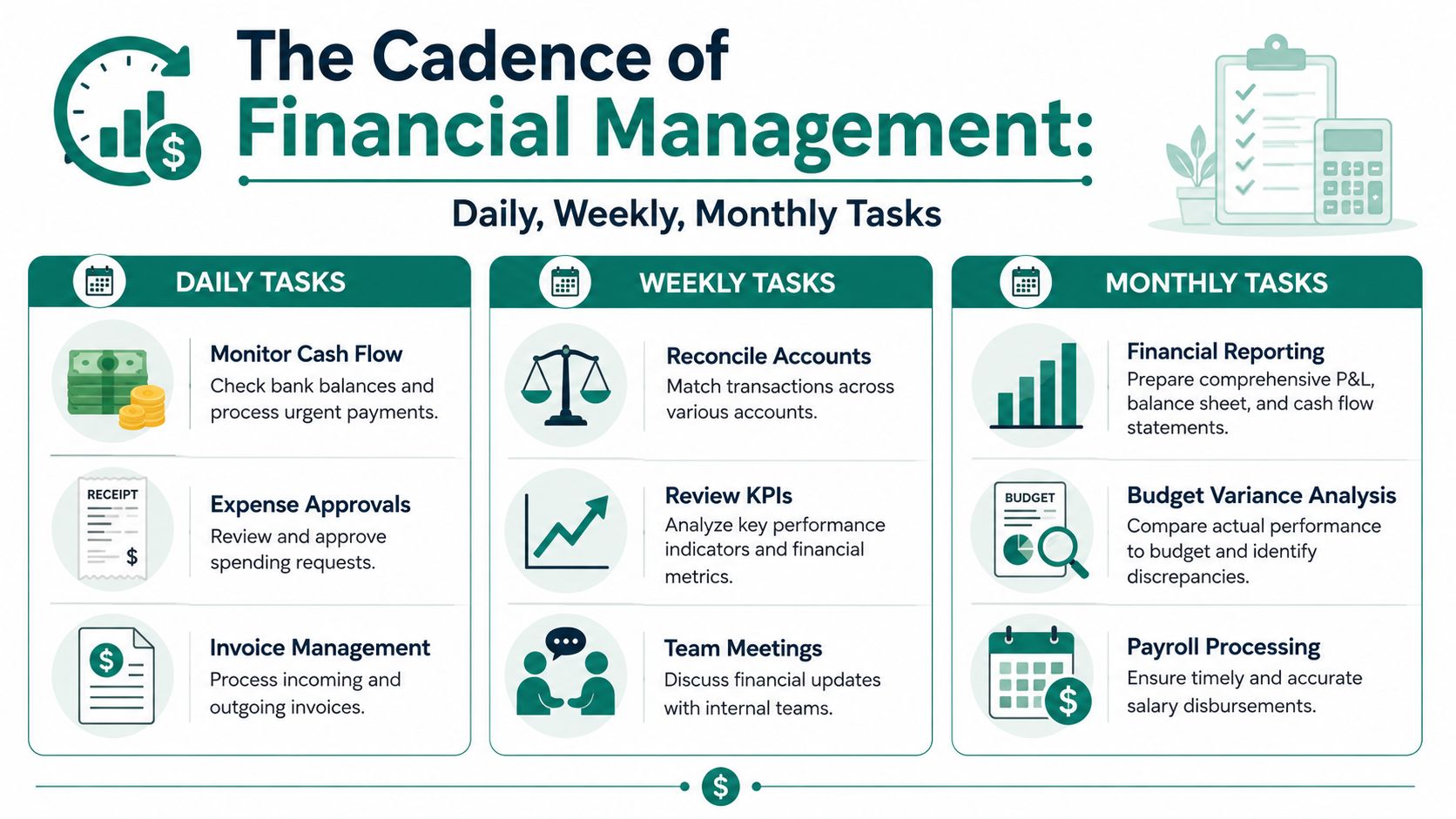

The Cadence of Financial Management Daily Weekly Monthly Tasks

Outside the realm of finance, the role is often imagined in broad terms: reports, budgets, controls. However, the work is more rhythmic. Strong finance managers run on cadence. They know which issues need same-day attention, which need weekly review, and which only become clear when the month closes.

Daily priorities

Daily work is about staying close to cash and exceptions. This isn't glamorous, but it prevents surprises.

- Check cash position early: Review bank balances, expected inflows, urgent payment requests, and any same-day obligations.

- Approve or hold spend: Separate essential payments from spending that can wait without damaging operations.

- Track invoice movement: Make sure outgoing invoices are issued correctly and incoming invoices are coded, approved, and queued properly.

- Watch for anomalies: Failed collections, duplicate requests, unusual expense claims, or unexpected debit activity need quick review.

A finance manager who skips this daily discipline usually ends up firefighting. A short morning review often avoids a much larger afternoon problem.

Weekly operating cycle

Weekly tasks are where finance starts pulling patterns out of the noise. This is the level at which collection delays, supplier pressure, or poor internal processes become visible enough to act on.

Typical weekly work includes:

- Receivables review: Identify overdue balances, assign follow-up actions, and escalate where customer promises are slipping.

- Payables planning: Group upcoming supplier commitments and decide which payments support continuity, influence, or negotiation.

- Payroll preparation: Confirm inputs, approvals, and timing so there are no avoidable errors or last-minute scrambles.

- Management check-ins: Meet sales, operations, procurement, or founders to align financial reality with operational plans.

On the ground: The week usually turns on one question. Are we using cash intentionally, or are we reacting to whoever shouts loudest?

Weekly forecasting becomes far more useful when it's tied to actual invoice behaviour, not just budget lines. Teams that want better visibility usually benefit from a more disciplined cash flow forecasting approach for SMEs.

Monthly management cycle

Month-end is still important, but it shouldn't be where finance first discovers the truth. The monthly cycle is where the team consolidates what daily and weekly discipline has already revealed.

A solid monthly rhythm usually includes:

- Close the books properly: Reconcile balances, review accruals, clear suspense items, and check that reported numbers reflect commercial substance.

- Prepare management reporting: Deliver a clean profit and loss view, balance sheet review, and cash commentary that leaders can use.

- Run variance analysis: Compare actuals to budget and forecast, then explain what changed and why it matters.

- Reset the next period: Update assumptions for collections, supplier outflows, stock plans, and overhead commitments.

What works is consistency. What fails is heroic month-end effort built on weak transaction hygiene and late information.

Essential Skills and KPIs for the Modern Finance Manager

The role demands more than accounting knowledge. A finance manager can be technically correct and still ineffective if they can't influence decisions, challenge assumptions, or keep the business focused on cash reality. The strongest people in the role combine technical skill with commercial judgement.

Hard skills that actually matter

Financial reporting and reconciliation are baseline requirements, not differentiators. The more valuable hard skills are the ones that help the finance manager convert messy business activity into a decision.

That usually includes:

- Forecasting skill: Building short-term and medium-term views that reflect collection timing, supplier behaviour, seasonality, and known risks.

- Management reporting: Producing packs that explain movement clearly instead of overwhelming stakeholders with ledger detail.

- Systems fluency: Working confidently across ERP platforms, accounting software, banking portals, and approval workflows.

- Balance sheet control: Understanding how errors in receivables, payables, prepayments, inventory, and accruals distort the picture.

- Process design: Setting approval paths, reporting deadlines, and documentation standards that people follow.

A practical finance manager doesn't chase perfect models if the inputs are weak. It's better to have a live forecast built on current customer and supplier facts than a complex workbook nobody updates properly.

Soft skills that separate average from strong

For many finance hires, career progression hinges on their approach to these responsibilities. The business doesn't need a walking rulebook. It needs someone who can hold a line when necessary and still help teams move.

Useful soft skills include:

- Clarity: Explaining financial consequences in plain language to sales, operations, and founders.

- Judgement: Knowing when to enforce process strictly and when to escalate a commercially sensible exception.

- Negotiation: Handling supplier conversations, payment plans, customer disputes, and internal spending challenges without turning every issue into conflict.

- Credibility: Delivering numbers that people trust and advice that proves reliable over time.

- Composure: Staying calm when collections slip, approvals bottleneck, or competing priorities all look urgent.

The best finance managers don't just say no. They explain the cost of each option and help the business choose deliberately.

KPIs worth tracking

Not every useful KPI belongs on a dashboard. A finance manager should track measures that show whether the company is becoming easier or harder to operate.

Good examples include:

- Days Sales Outstanding: A practical signal of how quickly receivables convert into cash.

- Cash conversion cycle: A broad view of how inventory, receivables, and payables interact.

- Budget versus actual variance: Helpful only when paired with explanation and action.

- Overdue receivables ageing: More revealing than top-line sales when collections discipline weakens.

- Close timeliness and accuracy: The month-end process should be reliable, not chaotic.

- Forecast accuracy: Not to punish the team, but to improve assumptions and spot recurring blind spots.

What doesn't help is tracking too many metrics with no owner. A useful KPI changes behaviour. A decorative KPI just fills a slide.

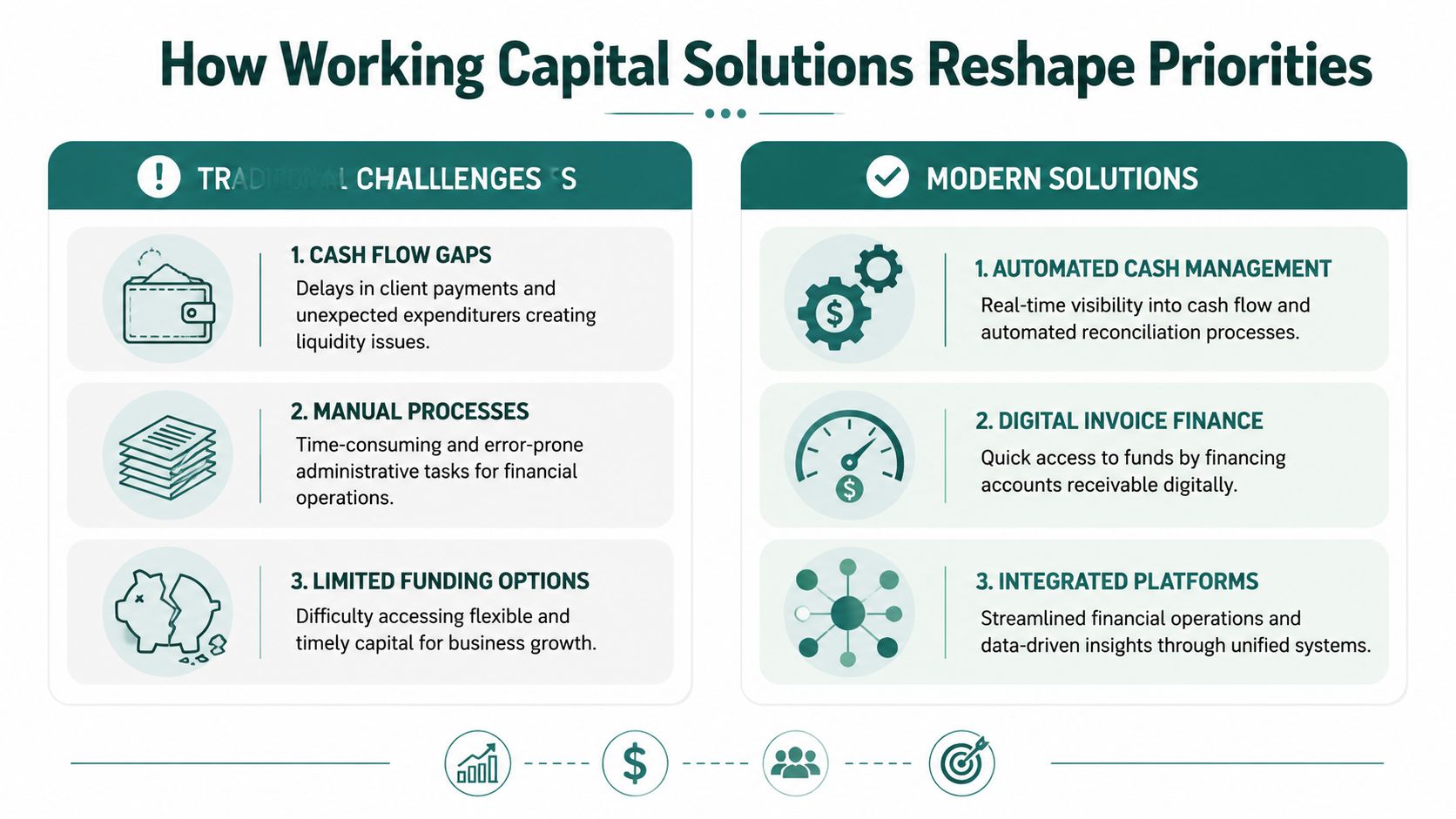

How Working Capital Solutions Reshape Priorities

The job changes materially when the business has better tools for working capital. Without them, the finance manager spends too much time bridging gaps manually. They chase receivables, delay payables, rework forecasts, and negotiate around constraints that keep repeating.

In the UAE, that pressure is not theoretical. 39% of businesses experienced delayed payments in Q1 2025, according to this UAE-focused discussion of finance manager duties and payment delays. When late payment risk is common, finance manager responsibilities naturally shift toward invoice timing, receivables discipline, supplier terms, and liquidity protection.

From chasing cash to orchestrating timing

Traditional SME finance teams often work in a reactive loop. A customer pays late. Finance slows supplier payments. Procurement gets frustrated. Sales asks for flexibility on another account. The forecast changes again. Nothing is technically broken, but everything feels tight.

Modern working-capital tools change the sequence of decisions. They give the finance manager more choice over timing, which is what liquidity management is really about.

For example:

- Invoice-based solutions: These can help teams release cash tied up in approved receivables, which reduces the need to wait passively for settlement.

- Extended payment workflows: These can create breathing room on the payables side when purchasing needs to move ahead before collections catch up.

- Digitised approval and reconciliation tools: These reduce manual lag and improve visibility, which matters because delayed information often creates delayed action.

The most important change is mental, not technical. The finance manager stops asking only, “How do we survive this month's gap?” and starts asking, “Which timing decision best supports margin, supplier relationships, and continuity?”

What improves in day-to-day work

When working-capital options are available and integrated into the finance workflow, the daily role becomes less about emergency response and more about prioritisation.

A finance manager can spend more time on:

- Selecting which receivables to act on: Not every invoice needs the same treatment.

- Protecting supplier relationships: Paying strategically is different from paying late by default.

- Supporting larger purchasing opportunities: Operations can move faster when finance sees a path to maintain liquidity.

- Reducing manual collections stress: The team gains time to manage exceptions, not every single transaction.

Strong working-capital management doesn't remove discipline. It makes discipline more effective because the team has better choices.

This is especially visible in sectors with heavy stock requirements or long sales cycles. In automotive, for instance, inventory can tie up significant cash while vehicles wait to sell. In distribution, one large order can improve revenue and strain liquidity at the same time. In both cases, finance needs tools that align commercial timing with cash timing.

The new priority set for finance leaders

Once better working-capital infrastructure is in place, the role becomes more strategic in very practical ways. The finance manager starts focusing less on transaction friction and more on capital allocation.

That usually means a shift towards:

- Scenario planning: Which customer, stock, or supplier decisions create the healthiest cash path?

- Commercial support: Which deals are good business after payment timing is considered?

- System visibility: Where are the delays, and are they operational, contractual, or behavioural?

- Policy design: Which approvals and limits preserve flexibility without creating leakage?

If you're reviewing the wider discipline behind these decisions, it helps to look at working capital as an operating system rather than a reporting line. A practical overview of that mindset sits in this guide to working capital management for growing businesses.

Conclusion From Cost Center to Growth Partner

A finance manager who only reports history will always be seen as overhead. A finance manager who protects cash, improves decision quality, and keeps the company operational becomes a growth partner.

That shift matters because SMEs don't fail only from weak sales or poor products. They also struggle when timing gets ignored. Revenue arrives later than expected. Inventory sits longer than planned. Supplier obligations don't move. Costs become real before collections do. Finance sits in the middle of all of it.

What the role should be judged on

The most useful view of finance manager responsibilities is simple. Can this person keep the books reliable, help leadership decide with confidence, and maintain enough liquidity for the business to move? If the answer is yes, the role is doing far more than administration.

Business owners should hire for that breadth. Finance professionals should build for it. The role now rewards people who understand accounting, but it increasingly depends on those who can also shape process, influence behaviour, and organise working capital with intent.

A wider operational lens

There's also value in looking outside the finance department itself. Workforce structure, payroll setup, and outsourced employment models can all affect timing, controls, and cash planning. For a useful operational perspective, this breakdown of how PEOs affect financial operations is worth reading.

The finance manager who thrives in a UAE SME isn't sitting at the back of the business waiting for month-end. They're close to customers, suppliers, inventory, payroll, and leadership decisions. They know that good reporting matters, but they also know that timing is what keeps a growing company steady.

That's the evolution of the role. Not from accountant to strategist in theory, but from scorekeeper to operator in practice.

If your business wants more control over invoice timing, supplier payments, and day-to-day liquidity, Comfi helps SMEs access working capital through invoice discounting, Buy Now, Pay Later terms, and automotive dealer financing. It's built for businesses that need faster cash movement without adding more manual friction to the finance team.