Deferred Payment for Business Purchases UAE: A Guide 2026

You're ready to place a larger order. Your customer wants stock now. Your supplier wants payment on normal terms. Your cash is stuck in receivables, VAT obligations, payroll, or inventory that hasn't turned yet.

That's where many UAE SMEs get stuck. The sale is there, demand is real, but timing gets in the way.

Deferred payment for business purchases UAE businesses use today isn't just about “pay later”. It's about matching money out with money in, without letting growth stall because cash arrives on the wrong day. For wholesalers, distributors, auto dealers, and electronics traders, that timing issue can decide whether you restock confidently or keep saying, “next month”.

Why Deferred Payments Are a Growth Engine in the UAE

A common UAE scenario looks like this. A distributor gets a strong purchase opportunity before peak demand. The buyer is serious, the margin works, and the supplier can fulfil. But there's a problem. Paying upfront would tighten cash too much, especially when other invoices are still waiting to be settled.

In practice, that's why deferred payment has become so normal in local trade. According to Atradius on UAE payment practices, 50% of all B2B sales in the UAE are transacted on credit, with average payment terms of 47 days. The same report says 58% of these B2B sales are overdue, which shows the other side of the story. Credit supports sales, but delays can put real pressure on liquidity.

That matters because deferred payment is no longer a niche commercial favour between long-time partners. It's part of how many UAE businesses operate.

Why owners feel both interest and caution

A business owner usually sees the upside immediately. If you can spread payments, you can buy more stock, preserve cash, and avoid turning away orders.

The hesitation comes later. Who carries the risk? What happens if the customer pays late? Will your finance team end up chasing invoices manually?

Practical rule: Deferred payment works best when it's treated as a sales and cash-flow tool together, not as a loose promise between buyer and supplier.

That's why more SMEs are moving away from informal WhatsApp agreements and ad hoc extensions toward structured plans, digital approvals, and clearer repayment terms. If you want a simple introduction to how flexible terms shape buying behaviour, this guide to flexible payment plans is a useful starting point.

Understanding Deferred Payment in a B2B Context

Deferred payment means the buyer receives goods now and pays later, either on a set date or through agreed instalments. The sale happens today. The cash arrives later.

That sounds straightforward, but many UAE SMEs use the same phrase for three very different setups. One is basic trade credit, such as net 30 or net 60. Another is a scheduled instalment plan with fixed repayment dates. A third uses a financing partner that pays the supplier first and then collects from the buyer under agreed terms.

The distinction matters because each model shifts pressure to a different place. Sometimes the supplier carries the receivable on its own books. Sometimes the buyer takes on fees in exchange for more breathing room. Sometimes a third party handles settlement and collections, which changes how sales, finance, and credit control work day to day. For businesses reviewing B2B buy now, pay later options for larger purchases, that difference is often the starting point.

What it means in day-to-day trade

In practice, deferred payment in the UAE is usually set up in one of two ways. The supplier gives credit for a fixed period, or the purchase is broken into scheduled payments. The commercial question is simple. Who is waiting for the money, and what does that wait cost?

For a buyer, the benefit is timing. You can bring in stock before your own receivables land. That is especially useful if you sell products that sit in the warehouse before they turn into cash.

For a supplier, the benefit is conversion. Better terms can help close a larger order or win a buyer who would otherwise reduce quantity. But someone still needs to track due dates, match invoices, follow up on late accounts, and decide what happens if a payment is missed.

Where confusion usually starts

Problems begin when businesses treat deferred payment like a favour instead of a system.

An informal extension sounds harmless. A buyer asks for another month. The supplier agrees by email or WhatsApp. The goods have already moved, but the paperwork, approval trail, and follow-up process stay vague.

A structured deferred payment setup works differently. Terms are documented before the sale closes. Payment dates are fixed. The invoice and delivery records match. Responsibility for reminders, collections, and credit exposure is clear.

If your team cannot explain who pays on which date, who follows up, and what happens after a delay, the business does not have a payment process. It has credit exposure with loose administration.

Why inventory-heavy sectors need a tighter definition

This matters more in automotive, electronics, and other inventory-led sectors than it does in many service businesses. A consultant may defer payment on one project invoice. A distributor may defer payment across containers, spare parts, devices, or fast-moving SKUs that must be reordered before the first batch is fully paid for.

That changes the goal. Deferred payment is not only about making a purchase easier. It is about keeping stock moving without draining working capital at the wrong moment.

A useful way to see it is to compare it with shelf space. If cash is tied up in inventory for too long, your warehouse may be full while your bank balance is tight. Well-structured deferred terms give that stock more time to sell before the payment obligation falls due. Poorly structured terms do the opposite. They create a gap between when you must pay and when the inventory turns into cash.

For inventory businesses, that timing gap is the whole issue. The right deferred payment structure helps match outgoing payments to the sales cycle of the goods being purchased.

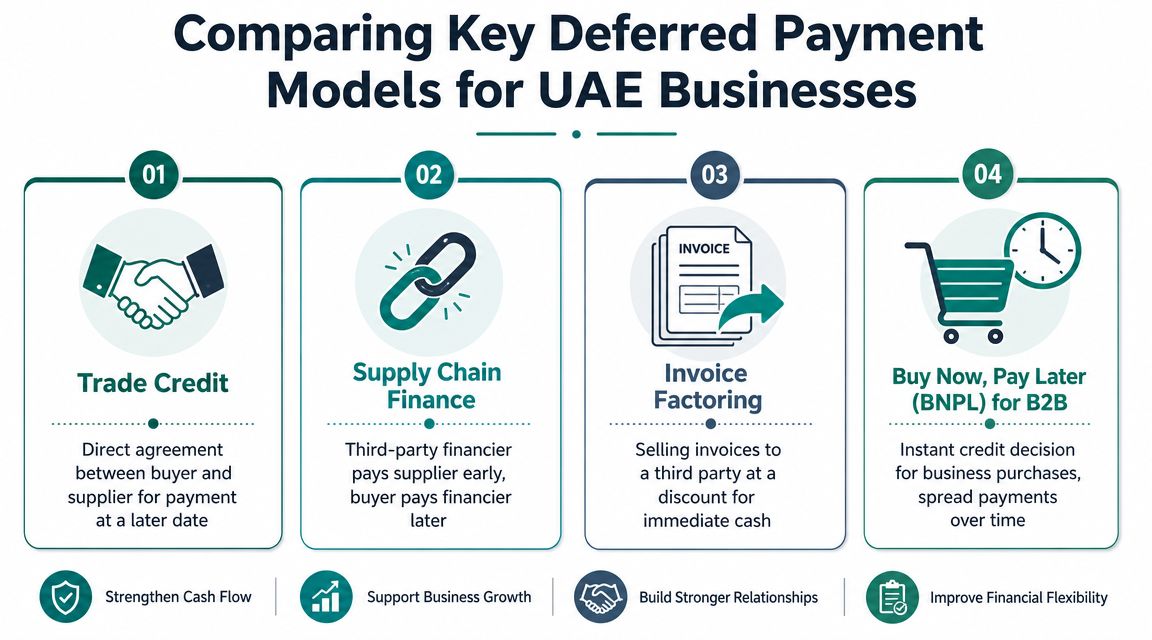

Comparing Key Deferred Payment Models for UAE Businesses

Not every deferred payment setup solves the same problem. Some help buyers complete a purchase more easily. Others help suppliers get paid earlier. Some are especially useful when money is tied up in stock for long periods.

Trade credit

This is the oldest model and still the most familiar. The supplier ships goods now and gives the buyer time to pay later.

It works well when:

- Relationships are established and both sides know each other's payment habits

- Order values are manageable enough for the supplier to carry the receivable

- Terms are simple such as net 30, net 60, or net 90

Trade credit can be effective, but it often becomes messy when the supplier's finance team is carrying too much exposure. If overdue invoices start piling up, sales growth can create cash pressure instead of relieving it.

Supply chain finance or third-party settlement

In this setup, a third party pays the supplier earlier, while the buyer settles later according to agreed terms. The structure changes the operational burden. The supplier is less exposed to delayed collections, and the buyer still gets breathing room.

This model suits:

- Wholesale and distribution businesses that need terms to close deals

- Suppliers with growing order volumes who don't want receivables to balloon

- Cross-functional teams that want a more controlled approval and settlement flow

A business considering embedded options can review solutions like B2B buy now pay later for merchant checkout as one structured path among several available approaches in the market.

Invoice discounting

Invoice discounting starts from a different point. The sale has already happened. The supplier has issued the invoice, but cash hasn't arrived yet.

That makes it useful when:

- You already have receivables on your books

- Your buyer terms are standard, but the wait is creating pressure

- You want to access cash from completed sales, not redesign checkout

This model helps smooth cash conversion. It doesn't usually change the buyer's purchasing experience directly. It helps the supplier avoid waiting the full term before using the value already sitting in issued invoices.

Dealer financing and stock-linked models

Generic advice often breaks down at this juncture.

Inventory-heavy sectors don't live on the same rhythm as ordinary trade credit. In automotive, money can sit in vehicles on the lot long before a sale happens. According to Atradius on UAE B2B payment practices and inventory cycles, capital can be tied up for up to 180 days before a vehicle sells. In that context, deferred payment isn't mainly about convenience. It's about releasing value trapped in stock.

The same logic applies in parts of electronics and consumer goods distribution where products are bought in volume, turn rates vary, and cash is locked between procurement and final sale.

Dealer-style structures are usually a better fit when:

- Inventory is expensive and slow-moving

- Restocking speed matters more than extending payables alone

- The business needs liquidity against stock position, not just against invoices

- Management wants financing logic that reflects stock rotation, not a flat net term

A net 60 term can help a fast-turning business. It may do very little for a dealer whose inventory sits much longer.

How to choose between them

A simple way to think about it:

- Use trade credit when the relationship is strong and the supplier can comfortably carry the timing gap.

- Use invoice discounting when sales are already made and you need earlier access to cash from invoices.

- Use third-party deferred payment models when you want buyers to have terms without pushing collection risk back onto the supplier.

- Use dealer or stock-linked structures when inventory itself is the bottleneck.

The right answer depends less on what sounds flexible and more on where your cash is getting trapped.

The Benefits and Risks for Suppliers and Buyers

A Dubai electronics distributor brings in a container of fast-moving accessories and slower premium devices before a sales period. The stock is on the shelf, but the cash has already left the business. If payment to the supplier can wait until more of that stock converts into sales, the deal supports growth. If the timing, pricing, and controls are weak, the same deal can squeeze both sides a month later.

Deferred payment changes who carries the timing gap between delivery and cash. In inventory-heavy sectors such as automotive parts, vehicles, consumer electronics, and white goods, that timing gap is often the primary commercial issue. The product has value, but the value is trapped in stock until the buyer sells through.

For suppliers

Suppliers usually introduce deferred terms to remove friction at the point of purchase. A buyer who cannot pay in full today may still be a strong customer if given terms that match how stock turns. That often leads to larger orders, faster replenishment decisions, and better conversion against competing offers.

For a supplier in automotive or electronics distribution, the upside is not only higher sales volume. It can also mean better sell-in across a wider product range. A dealer may take more SKUs, more accessories, or higher-ticket models if payment dates line up with expected sell-through rather than shipment date.

The commercial benefits are clear:

- Higher order values when buyers are not forced to preserve all cash up front

- Stronger account retention because payment terms become part of the service, not just the price

- Better stock movement when buyers can reorder before cash from the previous batch is fully collected

The risk sits in the receivable.

If the supplier keeps that receivable on its own books, finance teams must carry delayed cash inflow, monitor overdue balances, and absorb any slippage in payment behaviour. That can work with a small number of disciplined buyers. It gets harder when multiple accounts ask for terms at once, especially if the supplier is also funding imports, warehousing, or local distribution costs.

Common supplier risks include:

- Cash-flow pressure when settlement is delayed across several large accounts

- More collections work if installments or due dates are tracked manually

- Lower margins when the cost of delay, default, or admin effort was not built into pricing

- Concentration risk if too much exposure sits with a few major dealers or resellers

A useful rule is simple. Sales teams see the order. Finance teams must see the waiting period behind the order.

For buyers

Buyers usually feel the benefit faster because the relief is immediate. The business gets stock now and pays later, which helps preserve cash for payroll, marketing, transport, or the next purchase cycle.

In inventory-heavy businesses, that matters more than the term length alone suggests. A net 30 or staged-payment plan works best when it matches the speed at which stock turns into revenue. For an electronics reseller, that might mean paying after a campaign period. For an automotive dealer, it may mean aligning repayment with vehicle sales rather than with the delivery date.

Deferred payment works like breathing room between buying and selling. Used well, it lets a business carry the stock it needs without starving the rest of the operation.

Buyer benefits often include:

- Better working capital control because cash is spread across the period in which goods are sold

- Stronger buying power on larger or more varied inventory orders

- Fewer missed sales opportunities when the business can stock ahead of demand

- More flexibility in seasonal sectors where revenue arrives in uneven waves

But buyers can also create problems for themselves. Lighter upfront pressure can make a purchase look affordable even when the full repayment schedule is unrealistic. That is common when procurement, sales, and finance are not looking at the same cash-flow forecast.

The buyer-side risks usually look like this:

- Overcommitting on inventory based on expected sales that arrive later than planned

- Underestimating total cost if fees, markups, or penalties were not reviewed carefully

- Poor visibility when several payment plans sit across branches, product teams, or departments

- Repayment mismatches when stock moves slower than the agreed payment schedule

That last point matters a lot in automotive and electronics. If premium units sit longer than expected, the buyer still owes instalments on time. Stock may be valuable, but it does not pay the bill until it sells.

The practical balance

Deferred payment works best when both sides solve the same timing problem, but from different angles. The supplier wants sales without weakening cash collection. The buyer wants stock without draining operating cash too early.

A good arrangement makes that trade visible. Who carries credit risk. What triggers payment. How late payment is handled. What happens if stock turns slower than forecast. Those questions matter more than the headline term.

In practice, the strongest setups are boring in the best way. The commercial team can explain them in one minute, and the finance team can track them without spreadsheets multiplying in the background.

Navigating UAE Regulatory and Tax Rules

A deferred payment arrangement can look commercially neat and still fail operationally if the paperwork is weak. In the UAE, the contract details and payment data matter more than many SMEs expect.

What needs to be clear in the contract

UAE deferred-payment contracts should include detailed payment schedules, assignment rights, and clear metadata for bank transfers, according to this UAE deferred-payment contract guidance.

That matters because vague wording creates avoidable disputes. If the agreement doesn't clearly state instalment dates, transfer instructions, rights to assign receivables, and remedies when payment slips, your finance team is left interpreting the deal after the problem starts.

A practical contract should spell out:

- Payment schedule with exact dates or trigger events

- Assignment rights if another regulated party may handle settlement or collections

- Goods and invoice references so payments can be matched cleanly

- Force majeure and longer-tenor wording where the arrangement runs over a longer period

- Sharia-compliance language if the structure is intended to be Sharia-compliant

Why bank transfer data can delay payment

A lot of payment friction doesn't come from refusal to pay. It comes from poor data.

UAE AML rules require complete originator and beneficiary information. If transfer details are missing or unclear, banks may pause or reject the payment. That means your invoice number, buyer and supplier identifiers, and payment purpose should be accurate and consistent from onboarding through settlement.

For finance teams, this leads to a simple operating rule:

- Use regulated payment channels

- Keep invoice metadata clean

- Match buyer, supplier, and payment-purpose details carefully

- Check transfer information before funds are sent

Clean contract terms reduce legal disputes. Clean payment data reduces bank friction. You need both.

A practical note on VAT and documentation

Deferred payment changes when cash is paid. It doesn't remove the need for proper VAT-compliant invoicing. Finance teams should make sure invoices, tax details, and supporting records are prepared correctly at issuance, not treated as an afterthought because cash will come later.

That's where many SMEs slip. They focus on negotiating terms, then realise later that the supporting documents aren't consistent across sales, tax, and banking records.

If you want deferred payment for business purchases UAE operations can handle cleanly, documentation has to be built into the process from day one.

How to Implement a Deferred Payment System

Rolling out deferred payment isn't just a finance project. Sales, operations, credit control, and customer support all end up touching it. The businesses that get it right usually start with process discipline, not software first.

Start with your actual cash cycle

Before choosing any provider or model, map the timing inside your business.

Ask questions like:

- When do you pay suppliers now

- When do your customers usually pay

- Which stock categories turn quickly, and which sit longer

- Where does growth stall because cash is tied up

This step sounds basic, but it stops expensive mistakes. A fast-turning wholesale line may only need simple net terms. A vehicle dealer or electronics importer may need a stock-linked structure because the cash blockage sits in inventory, not at checkout.

Choose a model that matches your use case

The UAE's deferred-payment environment is becoming more embedded in everyday purchasing. ResearchAndMarkets projects the UAE BNPL market will reach US$3.92 billion by 2031, as reported in this ResearchAndMarkets market outlook. For B2B merchants, that means buyers increasingly expect smoother payment options at the point of purchase.

When assessing options, look at:

- Approval logic that fits SME buyers rather than only large corporates

- Integration method, whether dashboard-based or API-led

- Collection handling so your team isn't manually managing every overdue account

- Industry fit, especially if you operate in automotive, electronics, wholesale, or marketplace trade

If you're comparing ways suppliers negotiate and operationalize longer terms, this guide to getting extended payment terms from suppliers in the UAE gives useful commercial context.

Keep implementation practical

Most SMEs don't need a large digital transformation project. They need a controlled rollout.

A sensible implementation path looks like this:

- Pilot with one customer segment

Start where order patterns are predictable and your team already understands the buying cycle. - Define approval rules early

Decide who can offer terms, on what order sizes, and under what documentation requirements. - Connect the data flow

Make sure invoices, due dates, buyer details, and settlement status can be tracked in one place. - Train sales and finance together

Sales should know how to present the option. Finance should know how repayments, disputes, and exceptions are handled. - Review performance monthly

Check whether the model is helping order flow, reducing friction, or creating new bottlenecks.

One example of a structured implementation option

Some providers support rollout through a digital dashboard for invoice upload, while others offer low-code plugins or API integration for a more embedded experience. Comfi, for example, supports B2B buy now pay later, invoice discounting, and dealer financing with supplier-side digital workflows and buyer payment terms structured around business purchases.

That matters less as branding and more as operating design. The right setup is the one your sales team can explain easily, your finance team can reconcile without manual chaos, and your customers can use without confusion.

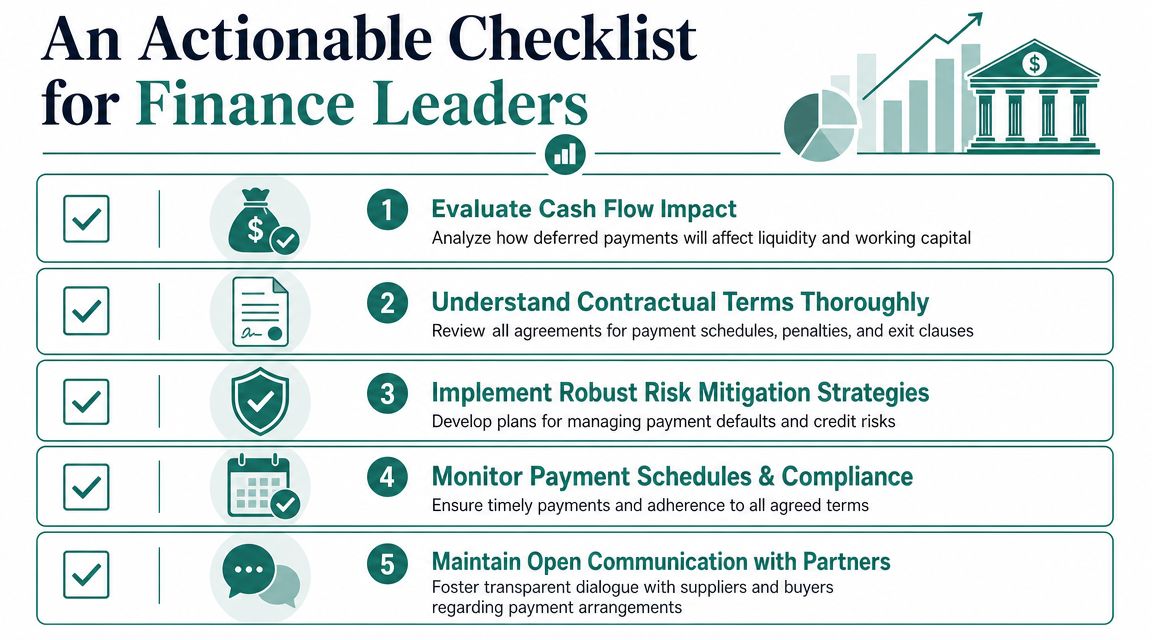

An Actionable Checklist for Finance Leaders

A good deferred payment setup should make your cash position easier to manage, not harder to understand. For finance leaders, the goal isn't only to extend terms. It's to decide where those terms create commercial value and where they create hidden exposure.

Use this checklist before launching or expanding any deferred payment for business purchases UAE programme:

- Map the cash gap clearly

Identify whether the pressure sits in payables, receivables, or unsold inventory. Don't solve an invoice problem with a stock tool, or a stock problem with a generic net term. - Separate buyer convenience from supplier risk

A smoother checkout or purchase flow is useful, but only if the repayment structure and collection responsibilities are equally clear. - Stress-test inventory cycles

If your sector carries stock for long periods, use a structure that reflects rotation timing instead of assuming ordinary trade terms will be enough. - Review contract language properly

Payment schedules, assignment rights, and transfer details shouldn't be buried in generic supplier paperwork. - Make invoice and transfer data audit-ready

Clean metadata prevents operational headaches later with matching, settlement, and bank review. - Choose a system your teams will use

If sales can't explain it or finance can't reconcile it quickly, adoption will fall apart.

The strongest deferred-payment programme is the one that sales can offer confidently and finance can monitor without surprises.

- Track outcomes that matter

Watch order size, stock availability, overdue behaviour, and collection workload. If the structure helps growth but creates admin drag, it still needs redesign.

If you're evaluating deferred payment options for UAE business purchases, Comfi is one platform to review. It supports models such as B2B Buy Now, Pay Later, Invoice Discounting, and Dealer Financing, which can help suppliers offer payment flexibility while keeping operational control over invoice workflows and repayment visibility.

Related Reading

- How Comfi’s B2B Buy Now Pay Later Solution Enhances Cash Flow for Businesses in the UAE

- Software Reseller Payment Terms UAE: A Practical Guide

- Optimize Your Hospital Suppliers Payment Terms UAE

- A Supplier’s Guide to Navigating Supermarket Payment Terms in the UAE (2026)

Ready to improve your business cash flow? Get started with Comfi today.