Flexible Payment Plans: The Ultimate Method for B2B Sales Growth

Imagine turning a potential ‘no’ from a customer into a firm ‘yes’ just by changing how you ask for payment. That's the real power of flexible payment plans. Think of them as a bridge between your need for steady cash flow and your buyer’s need for a bit more time to pay. For B2B suppliers, this isn't just another option at checkout; it's a serious sales tool.

Why Flexible Payment Plans Are a Game Changer for B2B Sales

In the competitive B2B market, offering payment flexibility is no longer a nice-to-have—it’s a necessity. Many businesses, especially small and medium-sized enterprises (SMEs) in the UAE and MENA region, are in a constant balancing act. On one hand, you need cash coming in to cover operational costs, restock inventory, and invest in growth. On the other, your business customers often need payment terms to manage their own budgets, which delays your revenue.

This is where a modern approach to payments makes a huge difference. Instead of waiting 30, 60, or even 90 days for an invoice to be paid, you can offer these terms to your buyers while getting paid almost instantly yourself. It solves the fundamental conflict between your cash needs and your customers' expectations.

Unlocking Growth and Building Loyalty

Offering flexible payment plans goes way beyond simplifying transactions; it's a powerful engine for business growth. When buyers aren't constrained by huge upfront costs, they're much more likely to place larger orders and buy more often. This has a direct, positive impact on your average order value and overall sales volume.

A flexible payment structure transforms the sales conversation from, "Can you afford this?" to, "How can we make this work for you?" This shift in focus builds stronger, more loyal customer relationships and sets you apart from competitors who stick to rigid payment policies.

What's more, this flexibility makes your business far more attractive to new customers who might have been unable to meet strict payment requirements before. By removing this barrier, you open up entirely new market segments. You can learn more about how to structure these deals by exploring modern trends in B2B payments and their impact on day-to-day operations. By adapting your payment strategy, you'll be able to close more deals and build a more resilient, thriving business.

Understanding Your Options for Flexible Payments

When you're navigating the B2B world, it's easy to see that not all payment solutions are built the same. Offering flexible payment plans is a game-changer, but the real secret is knowing which tool to pull out of the toolbox for the right job. It's about matching the solution to the situation to get the biggest impact.

Let’s break down the main types of flexible payments you can use as an SME in the MENA region. We'll ditch the jargon and get straight to how each one works in the real world, so you can figure out what makes the most sense for your business and your customers.

Invoice Discounting for Immediate Cash Flow

Picture this: you've just delivered a huge order to a major client. The invoice is sitting there, but the payment terms are a painful 60 days out. In the meantime, you’ve got your own suppliers to pay and stock to reorder. This classic cash flow crunch is exactly where invoice discounting steps in as a lifesaver.

Invoice discounting lets you cash in on your outstanding invoices right away. Instead of waiting weeks (or even months) for your customer to pay, a partner like Comfi can advance you a huge chunk of that invoice's value, often within 24 hours. You get the cash you need to keep things running, no delays.

This isn’t about taking on debt. It’s about unlocking funds that are already yours but are temporarily locked up in your accounts receivable. Clients who use this method have been able to unlock their working capital, which is the perfect way to bridge those short-term cash gaps, letting you pay your bills on time and jump on new opportunities without a second thought.

No matter which path you take, creating a clear schedule of payments is the foundation of any good agreement. It keeps things transparent for you and your customer.

B2B Buy Now Pay Later to Drive Sales

Now, let's flip the script and look at it from your customer’s side. A retailer wants to stock up on your products for a big season like Ramadan or the end-of-year rush. But paying for that massive order all at once would put a serious strain on their cash flow. This is where B2B Buy Now, Pay Later (BNPL) becomes your ultimate sales tool.

With B2B BNPL, you give your buyers the breathing room of paying in 30, 60, or even 90 days. Here’s the brilliant part: you don't wait a single day for your money. A platform like Comfi pays you the full invoice amount upfront, while they handle collecting the payments from your customer over time. You can learn more about how B2B BNPL solutions work and slot into your sales process.

By offering BNPL, you remove the biggest obstacle for your buyer—the upfront cost. This empowers them to increase their order size, leading to a higher average order value (AOV) for your business.

This approach brilliantly separates your sales cycle from your cash flow cycle. You get all the benefits of offering attractive terms without shouldering any of the risk or the long wait for payment.

Streamlined Dealer Payments for Supply Chains

Finally, let's look at industries built on complex networks of distributors and dealers. Think electronics, auto parts, or fast-moving consumer goods. In these supply chains, payments can become a slow, clunky process, creating frustrating bottlenecks for everyone involved.

Streamlined dealer payments are custom-built to fix this. The system creates a much slicker payment flow between a main distributor and their entire network of smaller dealers and retailers. It makes sure payments are processed fast and reliably, so distributors get paid sooner and dealers can manage their stock and cash flow better.

This is a highly specialized solution for the unique headaches of multi-layered distribution. By smoothing out the entire payment journey, it strengthens relationships between distributors and their partners, helping the whole supply chain run more efficiently—and more profitably—for everyone.

What’s the Real Business Impact of Payment Flexibility?

Moving this conversation from theory to your actual balance sheet is where things get interesting. Offering flexible payment plans isn't just another operational tweak or a nice-to-have feature. It's a strategic investment in growth. The impact shows up directly on your bottom line, changing how you attract customers, close deals, and manage your own money.

It’s not just about being convenient; it’s about building a more resilient and profitable business. When you lift the immediate financial burden from your buyers, you fundamentally change their behaviour. Suddenly, that big, intimidating upfront cost becomes a series of manageable instalments. This simple shift empowers customers to commit to larger orders and buy more often, which is a direct path to boosting your revenue.

Drive a Serious Uplift in Sales

One of the first things you'll notice is a real, measurable jump in sales. By letting customers buy now and pay over time, you remove the single biggest hurdle that makes them hesitate or walk away: the upfront cost. This is especially true for B2B buyers who are constantly juggling their own cash flow to manage inventory and day-to-day operations.

This approach immediately widens your customer base, making your products accessible to businesses that previously couldn’t swing a large initial outlay. The result is a powerful one-two punch:

- Higher Average Order Value (AOV): Customers are far more willing to add more to their order or upgrade to premium options when they can spread out the cost.

- Increased Conversion Rates: Potential buyers who were sitting on the fence are converted into paying customers, turning lost opportunities into closed deals.

Strengthen Customer Loyalty and Acquisition

In a crowded market, customer experience is what sets you apart. Offering flexible payment plans sends a clear message that you understand your customers' financial pressures and you’re willing to be a partner, not just a vendor. This builds trust and fosters a much stronger, more loyal relationship that lasts well beyond a single transaction.

Offering payment flexibility is a clear signal to the market that you are a modern, customer-centric business. This not only retains existing clients but also serves as a powerful magnet for attracting new ones who are actively seeking more accommodating partners.

A smooth payment experience encourages repeat business and turns happy customers into your best salespeople. This word-of-mouth marketing is priceless, driving down your Customer Acquisition Cost (CAC) as new clients seek you out because of your reputation for being easy to work with.

Achieve Healthier, More Predictable Cash Flow

This might be the most critical impact of all—the effect on your own financial stability. Traditionally, offering payment terms meant your business had to wait 30, 60, or even 90 days to get paid. This created painful cash flow gaps that could easily kill growth. Modern flexible payment solutions flip this broken model on its head.

Here’s where the distinction is crucial. You offer your buyers the 30, 60, or 90-day terms they need, but through a platform like Comfi, you get paid upfront. Your sales cycle is successfully disconnected from your cash collection cycle. The huge growth in the UAE's Buy Now, Pay Later (BNPL) market, which hit USD 2.45 billion in a single year, shows just how much demand there is for these terms. You can learn more about the growth of flexible payments in the UAE.

Imagine an SME unlocking its own funds that were previously trapped in unpaid invoices. That capital can be immediately reinvested into a vital marketing campaign, buying new inventory for a busy season, or expanding a product line—actions that fuel real growth that would have otherwise been impossible. This is the true power of predictable cash flow.

How to Implement Flexible Payments in Your Business

Adopting flexible payment plans is a powerful strategic move, but let's be honest—getting started can feel a bit overwhelming. The good news? Modern fintech has made the whole process surprisingly straightforward. Forget about a massive, complex technical overhaul. It’s more like a clear, step-by-step checklist.

The key is simply to approach it with a plan. By breaking it down into manageable chunks—from deciding who gets payment terms to making sure you're compliant—you can slot this new capability right into your existing operations and start seeing the benefits almost immediately.

Step 1: Define Clear Buyer Eligibility Criteria

Before you start offering flexible terms to everyone, you need to decide who qualifies. This isn't about excluding customers; it’s about smart risk management to ensure the programme is sustainable for your business. Setting clear, consistent eligibility criteria is the first and most important step.

You might set rules based on factors like:

- Business Registration: Requiring buyers to have a valid trade licence and be in good standing.

- Order History: Offering terms to repeat customers with a solid track record of paying on time.

- Order Size: Setting a minimum order value to qualify for extended payment terms.

The goal is to create a fair system that protects your business while making your products more accessible.

Step 2: Choose the Right Integration Method

So, how will you actually offer these plans at checkout or on your invoices? The right method depends entirely on your current workflow and tech setup. Luckily, you don't need a team of developers to get this done.

Modern platforms offer a few different features to fit any business:

- Web Dashboard: This is the simplest way in. You can manually create payment links or process orders through an easy-to-use online portal. It's perfect if you handle a lower volume of B2B transactions.

- Low-Code Plugins: If you run an e-commerce store or use certain accounting software, pre-built plugins can bolt flexible payment options directly onto your existing systems with minimal fuss.

- Full API Integration: For larger businesses with custom-built platforms, a full API integration creates the smoothest experience for everyone, embedding payment options directly into your checkout flow.

The best choice is always the one that causes the least disruption to your current operations while giving your customers a slick experience.

The real power of a modern fintech partnership lies in its ability to handle the heavy lifting. Instead of building a complex system from scratch, you can plug into a ready-made infrastructure designed for speed and security.

Step 3: Understand Credit Risk Management

One of the biggest worries for any business offering deferred payments is the risk of a buyer not paying. This is where partnering with a specialised platform like Comfi becomes a genuine game-changer. Instead of shouldering the burden of vetting customers and chasing payments yourself, the right partner takes on the entire risk process for you.

When a buyer chooses a flexible payment plan, the platform runs instant, paperless checks to assess their eligibility. The decision is fast and data-driven, often coming back in moments. If approved, the platform assumes the risk. This means you get paid upfront and are completely protected, even if your buyer pays late or defaults.

Step 4: Establish Transparent Terms and Pricing

Clarity is everything when it comes to building trust. Your flexible payment plans must have transparent terms, conditions, and any associated costs laid out clearly from the start. Hiding fees or using confusing jargon will only lead to disputes and hurt your reputation. A critical part of this is ensuring your checkout process is optimized; learn more about creating order forms that convert to build this transparency into your sales process from day one.

Work with your payment partner to define a straightforward structure. This should include the exact payment schedule, the total amount due, and any service charges. By being upfront, you position the payment plan as a valuable service, not a hidden cost.

Step 5: Navigate Local Compliance

Finally, you have to make sure your payment offerings comply with all local regulations. In the UAE and the wider MENA region, financial rules are well-defined and strictly enforced.

Working with a locally-based fintech partner gives you a massive advantage here, as they already have a deep understanding of the legal landscape. They ensure that every part of the process—from customer onboarding to data handling—adheres to the requirements of authorities like the UAE Central Bank. It gives you complete peace of mind.

Measuring the Success of Your New Payment Strategy

So, you've launched your flexible payment plans. Great. But gut feelings don't pay the bills. To really know if they're working, you need a solid way to measure their impact. This is where a clear KPI framework comes in, showing you the real-world effects on customer behaviour and, most importantly, your cash flow.

Simply tracking top-line revenue won't give you the full story. For instance, looking at your average order value alongside your conversion rate can uncover patterns a single metric would completely miss. This deeper view helps you spot subtle shifts in how your customers are buying and lets you react quickly.

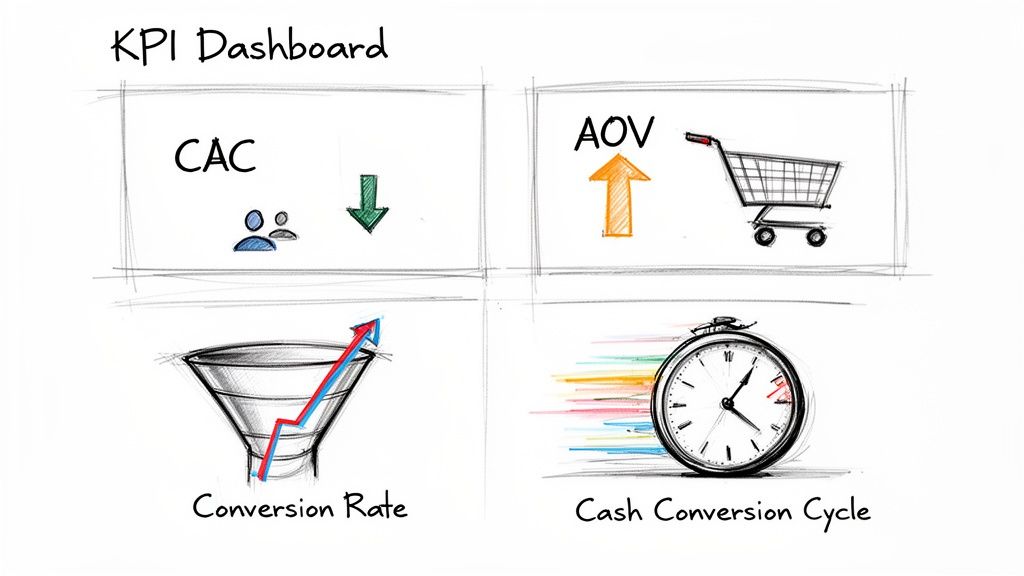

Key Metrics to Track

To get a true sense of how these new payment options are driving growth, focus on these four core metrics. They work together to paint a complete picture.

- Lower Customer Acquisition Cost (CAC): How much does it really cost you to bring a new buyer on board? Offering flexible terms often makes your pitch far more compelling, especially for customers who are sensitive to upfront costs, which can bring your CAC down.

- Higher Average Order Value (AOV): This tracks the average amount spent in a single transaction. It’s simple logic: when customers have the breathing room to pay over time, they’re often willing to buy more in one go.

- Improved Sales Conversion Rate: What percentage of prospects actually become paying customers? By removing the immediate budget headache, instalment options can give hesitant buyers the final nudge they need to click "purchase."

- Faster Cash Conversion Cycle: This is a big one. It measures how quickly a sale turns into actual cash in your bank account. Platforms that pay you upfront while your customer pays later are a game-changer for shortening this cycle.

By watching these numbers as a group, you can uncover opportunities you might have otherwise missed. A dip in your conversion rate while your AOV holds steady could be a signal to tweak your payment term lengths or rethink your approval criteria.

“Measuring the right KPIs can reveal a direct 25% uplift in ROI and guide smarter financial decisions.”

Building Your KPI Dashboard

You don't need a complicated setup to get started. Begin with a simple dashboard tool that connects to the data you already have—even a well-organised spreadsheet will do the trick before you upgrade to a dedicated BI platform.

- Pull in sales data from your CRM or payment gateway.

- Assign each KPI to a simple visual chart or gauge.

- Set up alerts to notify you when you hit important thresholds, like your CAC creeping above your target.

As you get more comfortable, you can automate these data feeds to cut down on manual work and get more accurate, real-time insights. This kind of visibility allows your team to jump on trends without any delay.

Tips for Data-Driven Adjustments

Let the data guide how you refine your payment strategy over time. Consistent monitoring creates a powerful feedback loop for continuous improvement.

- Glance at your metrics weekly. It helps you catch any strange dips or spikes early on.

- Slice and dice the data. Compare performance across different customer segments to see what's resonating.

- Don't be afraid to experiment with different payment terms. See how a 30-day plan performs against a 60-day one.

For a deeper analysis, it's worth learning how to improve your accounts receivable turnover ratio to really get your cash flow optimised.

Creating a Continuous Improvement Loop

Think of your strategy as a living thing that you constantly refine. Cycle through these steps to keep making it better:

- Analyze: Review trends monthly and set fresh targets.

- Test: Run A/B tests on different payment terms and ask for customer feedback.

- Iterate: Adjust your plan structures based on how customers are actually using them.

These regular review cycles ensure you’re always adapting your pricing and terms based on what's actually happening in the real world. By combining clear metrics with a structured dashboard, you can easily prove the ROI of your flexible payment strategy and keep pushing for better results.

Ultimately, tracking these KPIs is what allows you to fine-tune your payment offerings, boost your cash flow, and keep the business running smoothly month after month.

Common Mistakes to Avoid When Offering Payment Plans

Offering flexible payment plans can feel like a game-changer for boosting sales and bringing in new customers. But diving in without a clear strategy can create more headaches than it solves. It’s easy to get tangled in the operational side of things if you’re not careful.

The goal is to offer your customers the flexibility they need without putting your own financial stability on the line. Getting this balance right is everything.

A classic rookie mistake is trying to run the whole show in-house. It might seem like the cheapest option at first, but it can quickly spiral into an operational nightmare. You suddenly find your team spending all their time manually tracking different payment schedules, sending out reminders, and chasing down late invoices. That’s valuable time and energy that should be going into growing the business, not playing bill collector.

Assuming All the Risk Yourself

This is probably the single biggest—and most dangerous—mistake you can make: taking on 100% of the risk. When you offer payment terms directly to a buyer, you're the one left holding the bag if they don't pay up. It only takes one large customer to default to trigger a serious cash flow crisis, completely wiping out all the benefits you were hoping to gain.

This approach effectively turns your sales department into a collections agency, a job that very few teams are cut out for. The stress and distraction of pursuing unpaid debts can be immense, pulling you away from the core activities that actually make you money.

The smartest way to offer flexible payment plans is to transfer the risk. Partnering with a specialized fintech platform means you get paid upfront, while they handle buyer vetting and assume the risk of non-payment. This protects your cash flow completely.

Straining Your Own Cash Flow

Another common pitfall is underestimating the hit your own liquidity will take. When you let your buyers pay later, you're essentially letting your own funds sit in their bank account instead of yours. Your sales figures might look fantastic on paper, but your actual cash-on-hand can dip to dangerously low levels.

This creates a painful squeeze where you've made the sales but don't have the cash to pay your own suppliers, restock inventory, or even cover payroll. Waiting 30, 60, or 90 days to get paid can bring your growth to a grinding halt.

A successful payment plan strategy has to separate your sales cycle from your cash collection cycle. The solution is to work with a service that pays you for your invoices right away, letting you offer competitive terms without creating a cash flow gap for your own business.

This setup gives you the best of both worlds:

- Your buyers get the flexibility they need. This helps you close bigger deals, more often.

- You receive your funds almost instantly. This ensures you have the capital to run and grow your business without any interruptions.

By sidestepping these common mistakes—getting buried in operations, taking on all the risk, and draining your cash flow—you can build a flexible payment strategy that’s not just profitable, but sustainable for the long haul.

Your Questions About Flexible Payments, Answered

Alright, so the benefits are clear, but you probably still have a few practical questions about how this all works on a day-to-day basis. Let's tackle some of the most common ones we hear from business owners and finance managers just like you.

How Quickly Can I Actually Get Started?

Much faster than you'd expect. With modern platforms, the entire setup is digital. Forget about mountains of paperwork. You can usually get your business registered, link up your bank account, and be ready to offer flexible payment plans in just a couple of days—all without needing your tech team to get involved.

What Happens if a Buyer Doesn't Pay? Who Takes the Hit?

This is the big one, and the answer is simple: you don't. When you partner with a service like Comfi, we take on 100% of the risk. We handle the buyer vetting, and once a deal is approved, you get paid upfront. If the buyer defaults down the line, that’s on us to manage. Your cash flow is completely protected.

Will This Work with My Current Software?

Yes, that's the whole point. A good flexible payments provider should fit into your world, not force you to change how you work. There are usually a few different ways to get connected:

- A Simple Web Dashboard: Perfect if you want to manually create payment links or manage invoices without any tech setup.

- Low-Code Plugins: These are great for e-commerce sites and accounting software. They slot right into your existing checkout or invoicing process.

- Full API Integration: For businesses with custom-built systems, a full API lets you embed the payment options so seamlessly your buyers won't even know they've left your site.

The goal of a good payment partner is to adapt to your workflow, not force you to change it. The best solutions offer a range of integration options that minimize disruption and maximize efficiency for your team.

How Does This Work in the UAE Market Specifically?

The UAE is the perfect place for this. The digital payment scene here is incredibly mature, with point-of-sale (POS) transactions making up over 80% of the market. Options like Buy Now, Pay Later (BNPL) are already second nature to consumers and businesses.

This high level of trust means everyone is comfortable with modern payment solutions. The UAE’s payment market is valued at over USD 213 billion, proving that offering flexible terms isn't just a nice-to-have; it's essential to stay competitive. You can dig into more of the numbers on the UAE payments market to see the full picture.

Ready to offer flexible payment plans and unlock your business’s growth potential? With Comfi, you can get paid upfront, eliminate risk, and empower your customers with the payment terms they need. Visit Comfi to get started today.

Related Reading

- How Comfi’s B2B Buy Now Pay Later Solution Enhances Cash Flow for Businesses in the UAE

- Deferred Payment for Business Purchases UAE: A Guide 2026

- Software Reseller Payment Terms UAE: A Practical Guide

- Unlock Cash Flow: How to Get Extended Payment Terms From Suppliers in the UAE

Ready to improve your business cash flow? Get started with Comfi today.