Unlock Business Credit for UAE Professional Services Firms

A UAE professional services firm can look healthy on paper and still feel cash-starved in practice. You finish the client work, send the invoice, and then wait. Salaries don’t wait. Software subscriptions don’t wait. Office costs, visas, VAT filings, and subcontractor bills certainly don’t wait.

That gap between “earned” and “collected” is where most owners get stuck. Consultants, agencies, legal practices, accounting firms, and IT service providers usually don’t have warehouses, vehicles, or equipment-heavy balance sheets. Their value sits in people, contracts, expertise, and billed time. Traditional credit products often struggle with that model.

Business credit for UAE professional services firms works best when it matches how these firms earn money. That means understanding why banks often hesitate, what alternatives fit better, and how to prepare your firm so credit decisions become easier, faster, and less frustrating.

Why Cash Flow is King for UAE Professional Services

A consultancy in Dubai can have a full pipeline, respected clients, and solid margins, yet still spend too much time watching the bank balance. That sounds contradictory until you look at the payment cycle. The work is delivered today, but the cash may land much later.

A typical pattern looks like this. You win a project, assign staff, pay monthly overheads, and issue an invoice after a milestone or delivery. If the client pays slowly, your firm carries the cost of delivery while waiting for money you’ve already earned. That’s manageable once or twice. It becomes painful when several invoices age at the same time.

Where the pressure shows up first

For service firms, cash flow pressure usually appears in a few predictable places:

- Payroll and contractors: Your team expects to be paid on time, even if your client is still in an approval cycle.

- Growth decisions: Hiring one more consultant or account manager may be commercially sensible, but it can feel risky when receivables are stretched.

- Tax and compliance costs: VAT, licence renewals, audit costs, and admin fees arrive on schedule.

- Client concentration: One delayed payment from a large account can affect the rest of the month.

Cash flow problems in services rarely start with lack of demand. They usually start with timing.

That’s why the right credit setup matters. If your business runs on invoices, then your funding approach should respect that reality. The strongest solution isn’t always the largest facility. It’s usually the one that fits the cadence of your receivables and doesn’t force an asset-light business into an asset-heavy lending model.

Why Traditional Bank Loans Often Miss the Mark

Banks aren’t irrational when they ask for collateral, lengthy documentation, and a clear borrowing history. They’re trying to reduce risk using tools they know well. The problem is that those tools often suit traders, manufacturers, or property-backed businesses better than professional services firms.

The mismatch shows up clearly in UAE data. In a Central Bank of the UAE MSME survey, 73% of UAE MSMEs felt financially constrained, and among those that applied for bank credit, 53% were rejected. The main reasons were weak business performance (70%), insufficient credit history (22%), and inadequate collateral (14%).

The bank sees a different risk profile

A bank officer often asks questions that make perfect sense for a business with stock, machinery, or property. What asset secures the facility? What can be pledged? What resale value exists if things go wrong?

A professional services owner answers differently. The firm’s real assets are client relationships, recurring mandates, staff capability, reputation, and signed contracts. Those are valuable, but they’re harder to package into a conventional secured lending file.

That’s why many otherwise viable firms hear some version of the same message: come back with more history, stronger financials, better collateral, or more documentation.

What doesn’t work well for service firms

Traditional bank facilities often miss the mark when your business has these traits:

- Intangible value: The firm’s strength is expertise, not equipment.

- Irregular billing cycles: Revenue may be lumpy even when the annual book is strong.

- Young operating history: Newer firms may be profitable but thin on formal credit records.

- Large receivables exposure: A few major invoices can dominate the balance sheet.

Practical rule: If your strongest asset is a signed invoice or a client contract, a facility built around hard collateral is usually the wrong tool.

The hidden cost of slow approvals

Even when an approval is possible, the process can still be a poor fit. A long credit review may work for an office expansion or a major capex decision. It doesn’t work as well when you need to smooth the gap between invoicing and collection.

That’s the key distinction many owners miss. The issue often isn’t that the business is weak. It’s that the product being requested was designed for a different commercial model.

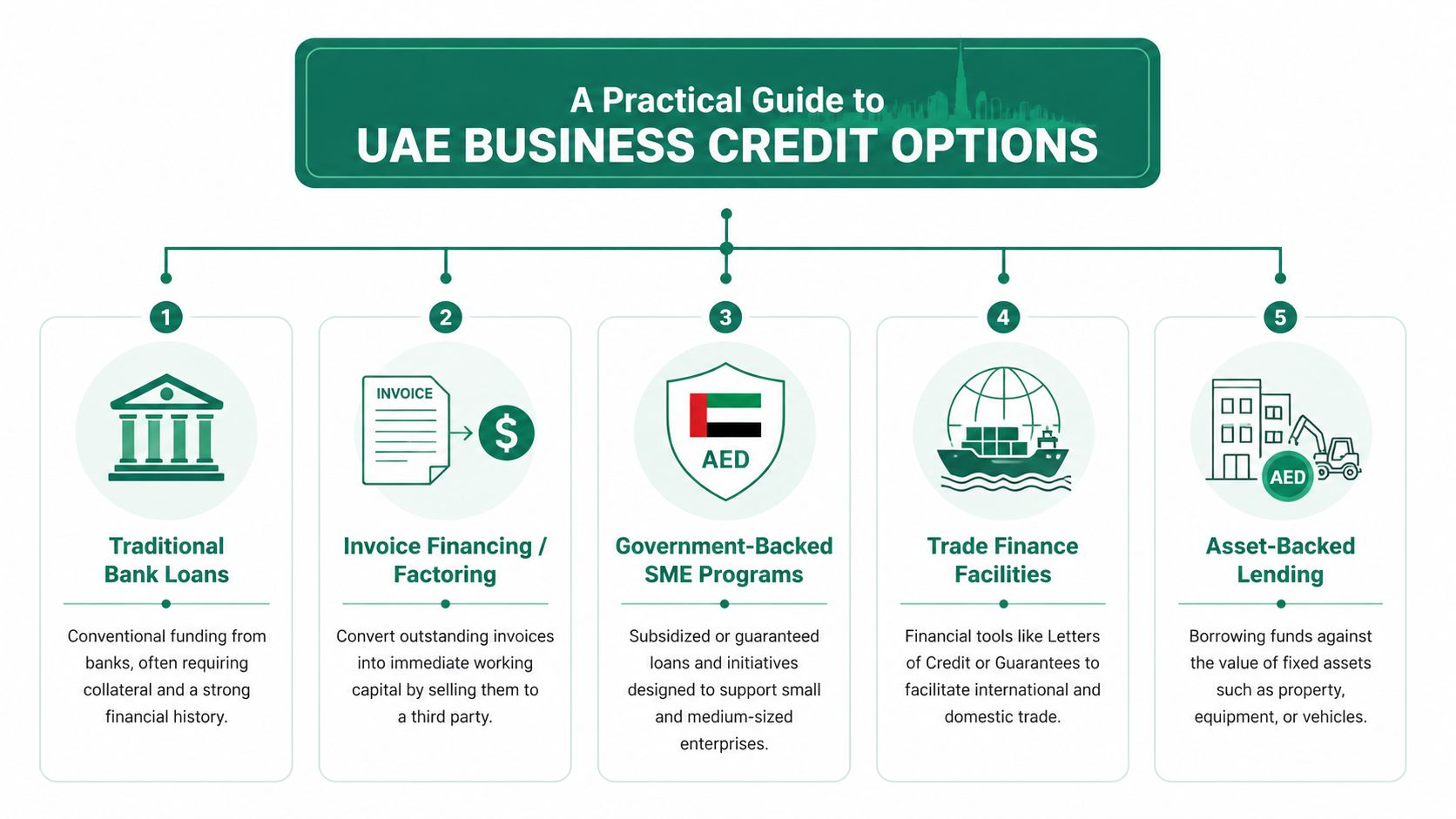

A Practical Guide to UAE Business Credit Options

Most firms don’t need every credit product. They need the right one for the job. Think of business credit the way you think about legal documents. A standard contract, an NDA, and a shareholder agreement all matter, but you wouldn’t use the same document for every situation.

The UAE market now offers a broader mix of options, and that matters because the UAE factoring services market reached approximately AED 18 billion, reflecting strong demand for invoice-based solutions as firms remain credit constrained, according to Ken Research’s UAE factoring market analysis.

Traditional facilities

These still have a place. They’re just often overused.

- Term loans: Useful when you’re making a defined investment, such as an office fit-out or acquisition. They’re less useful for uneven receivables because repayment starts on schedule whether your clients have paid or not.

- Business overdrafts: Handy for short-term liquidity swings. The trade-off is that they can become a habit. What starts as a temporary buffer can turn into a permanent crutch.

- Credit cards: Fine for small operational spending. Poor choice for managing structural receivables gaps.

Government-linked and relationship-led options

Some firms benefit from support tied to SME policy, banking relationships, or sector-specific programmes. These routes can be worth exploring if you already bank with an institution that understands your business well.

What works here is relationship depth. What doesn’t is assuming that a general SME label automatically means the product is suited for a consultancy, design studio, or advisory firm.

Invoice-based options

For many service businesses, the fit improves sharply in such circumstances.

- Invoice discounting: This lets a firm access cash tied up in approved invoices. The logic is simple. You’re not trying to monetise a hypothetical future deal. You’re releasing value from work already delivered.

- Factoring: Similar in principle, though the operational setup can differ depending on who manages collections and how customer interaction is handled.

- Embedded payment terms for buyers: In some situations, suppliers can get paid upfront while clients receive more flexible terms. That can help sales without forcing the supplier to carry the delay.

A good way to understand invoice discounting is to compare it to property. A bank mortgage is based on owning an asset and borrowing against it. Invoice discounting is closer to accelerating cash that already belongs to you, subject to the invoice and buyer profile.

If you want a simple primer on how revolving credit facilities differ from invoice-based access to cash, this guide to a business credit line in the UAE is a useful comparison point.

What to choose and when

Use this rule of thumb:

- Choose a term-style facility when you’re funding a planned investment with a long payoff period.

- Choose an overdraft when occasional timing gaps are small and predictable.

- Choose an invoice-based structure when completed work is sitting in receivables and that delay is the main strain on operations.

The best credit product should match the shape of your cash flow, not just the amount you want.

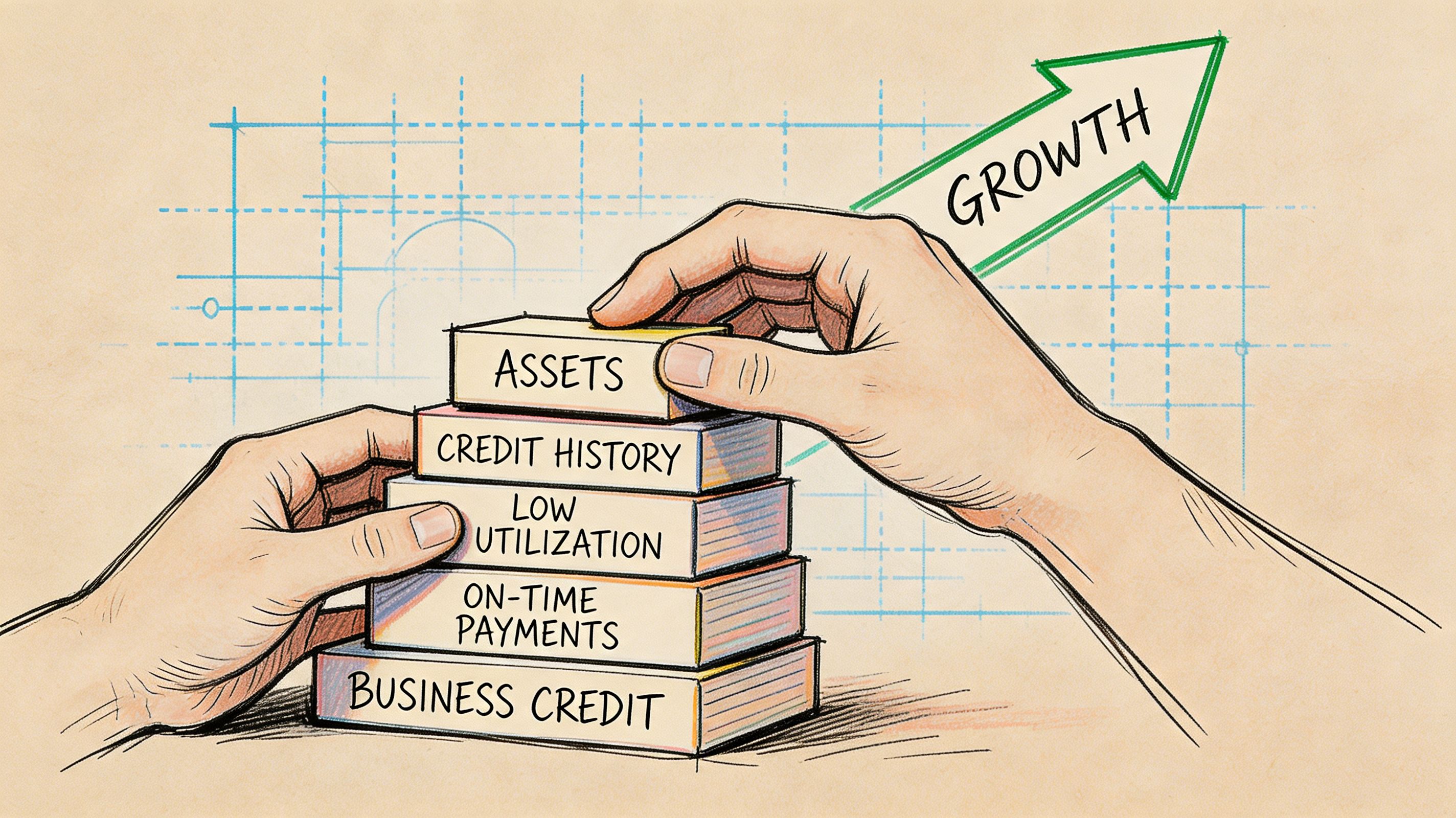

How to Build Your Firm's Credit Profile

A strong credit profile makes every option easier. It improves how lenders, fintech platforms, insurers, and counterparties read your business. Many owners wait until they need access urgently, then discover their records are incomplete, inconsistent, or difficult to assess.

That’s avoidable.

Start with clean operating records

If your books are messy, every credit conversation becomes slower. If your books are clean, many concerns disappear before they’re raised.

Keep these basics in order:

- Management accounts: Up-to-date monthly numbers matter more than a once-a-year scramble.

- Bank statements: Make sure inflows and outflows align with your reported activity. This article on preparing your business bank statement for review is useful if you want to see what reviewers typically look for.

- Audited financials when applicable: Audits help because they reduce uncertainty.

- VAT compliance: Consistent filings signal operational discipline.

Understand what credit data is actually doing

Credit reporting isn’t just a score on a screen. It helps counterparties assess payment behaviour, utilisation patterns, and trading reliability. According to D&B UAE’s overview of credit reporting services, these tools can reduce default rates in B2B transactions by up to 25% through more precise risk assessment.

That matters for your firm in two ways. First, your own behaviour shapes how others view you. Second, the quality of your customer base can influence how invoice-based solutions are assessed.

Better records don’t guarantee access. They remove easy reasons for a decline.

A practical checklist

Not every improvement requires a major project. Start with a short list:

- Pay suppliers consistently: Payment discipline builds commercial credibility over time.

- Separate personal and business finances fully: Blurred accounts create confusion and weaken trust.

- Keep licences and statutory documents current: Administrative gaps can slow decisions unnecessarily.

- Review your AECB presence: Make sure your business information is accurate and current where applicable.

- Tighten invoicing standards: Invoices should be complete, correctly addressed, and easy to verify.

Structure also matters

Your business setup can influence how others assess operational maturity. Free Zone and Mainland firms can both build strong profiles, but whichever structure you use, consistency matters more than branding. Clear ownership documents, clean filings, and reliable financial reporting carry more weight than a polished pitch deck.

Accessing Working Capital with Invoice-Based Solutions

A familiar pattern plays out in UAE professional services firms. The work is finished, the client is happy, the invoice is issued, and cash still arrives 30, 60, or 90 days later. Payroll, VAT, rent, and subcontractor costs do not wait with it.

For this business model, receivables are often the primary operating asset. Traditional bank products are usually built around property, equipment, or long trading histories with hard collateral. A consulting, legal, marketing, design, or advisory firm often has none of that in meaningful volume. It has signed engagements, delivered work, and invoices due from credible clients. Invoice-based funding fits that reality better because it follows the revenue already earned.

Why this fits service businesses

A term loan solves a balance sheet problem. Invoice discounting solves a timing problem.

That distinction matters. If your firm is profitable on paper but strained between billing and collection, adding a conventional loan can be the wrong tool. It usually comes with longer approval cycles, broader documentation requests, and repayment terms that do not always match client payment behavior. Invoice-based access is closer to the source of the cash gap. You complete the work, issue the invoice, and use that receivable to bring cash forward.

For many firms, that is the cleaner match.

What improves eligibility and speed

Providers still look for discipline. They want invoices that can be checked quickly, customers that can be assessed with confidence, and a billing process that does not create avoidable doubt.

The firms that move fastest usually have a few basics in place:

- Clear invoices: Scope, dates, payment terms, purchase order references if relevant, and the correct legal entity details.

- Strong supporting records: Signed contracts, approved timesheets, proof of delivery, or email approvals where the service model requires them.

- Credible debtors: Well-established clients are easier to finance than first-time or disputed counterparties.

- Consistent billing habits: Repeat invoices against an ongoing client relationship are usually easier to assess than irregular one-off projects.

- Clean tax and company records: Administrative gaps slow reviews because they create more follow-up questions.

The commercial upside beyond cash flow

Receivables-based funding can also support growth, not just stability.

Earlier research cited in this article noted faster funding outcomes for VAT-registered firms and stronger commercial results when buyer payment friction is reduced. That matters for service businesses selling larger retainers, project phases, or cross-border advisory work. If a client wants more flexible payment timing and your firm still needs predictable collections, invoice-based structures can reduce that tension. In practice, they can help you say yes to larger opportunities without stretching your own working capital to cover the delay.

One option is invoice discounting for UAE businesses, where approved receivables are used to access cash tied up in outstanding invoices. The practical appeal is straightforward. It is often faster to arrange than a conventional secured facility, and it matches how an asset-light service firm earns money.

Used properly, this is not extra debt for its own sake. It is a way to turn completed work into usable cash on a timetable that suits the business, rather than the bank’s collateral model or the client’s payment cycle.

Creating Your Firm’s Financial Growth Plan

A smart financial plan starts by matching the tool to the decision.

If you’re opening a new office, buying equipment, or making a long-horizon investment, a traditional bank facility may still be the better fit. If your main issue is that clients pay after the work is done, invoice-based access is usually more logical. If you want to offer customers better payment flexibility without disrupting your own receipts, embedded buyer payment options deserve serious attention.

A simple decision filter

Ask yourself three questions:

- Is this for investment or timing? Investment points toward term-style borrowing. Timing points toward receivables-based solutions.

- Do I have hard collateral, or mostly contracts and invoices? Asset-light firms should avoid pretending to be asset-heavy borrowers.

- Will better payment terms help me win more business? If yes, the credit conversation is no longer only about defence. It’s also about growth.

A good growth plan also includes sales discipline and positioning. If you’re refining your offer, packaging services, or tightening go-to-market execution, these B2B growth services provide a useful example of how professional services firms can sharpen commercial strategy alongside financial operations.

Unpaid invoices shouldn’t sit in your business like locked drawers. For many UAE service firms, they’re usable assets. The firms that grow more calmly usually aren’t the ones with perfect clients. They’re the ones that choose financial tools that fit how they trade.

If your firm invoices clients for completed work and wants a more practical way to access cash tied up in receivables, Comfi is one UAE-based option to explore. It offers invoice discounting and buyer payment term solutions through a digital process, which can suit professional services businesses that want an alternative to collateral-heavy bank products.