AECB Score: A Guide for UAE SMEs & Auto Dealers

A strong order book doesn’t always mean a healthy cash position. Many UAE SME owners learn that at the worst moment. A distributor lands a valuable purchase order but can’t move quickly because receivables are still unpaid. An auto dealer spots fast-moving stock at the right price but has cash trapped in vehicles already sitting on the lot.

That’s where many owners start asking the wrong question. They ask, “Which provider should I approach?” before asking, “What does my aecb score say about my business today?” In practice, that three-digit number often shapes whether you move fast, face delays, or get turned away.

If you run an ambitious SME, your aecb score isn’t just a background detail. It affects how your business is viewed when you apply for modern capital solutions such as invoice discounting, dealer financing, and flexible payment terms. It also tells you what needs fixing before your next growth push.

Your Business Growth Is Stuck What Now

A common UAE business problem looks simple on the surface. Sales are coming in. Demand is real. Customers want stock now. But the cash cycle doesn’t match the opportunity.

An automotive dealer may have solid inventory and genuine buyer interest, yet money is tied up in cars that could take months to sell. A wholesaler may have issued invoices to strong customers but still has to wait before cash arrives. Growth stalls, not because the business is weak, but because timing is off.

The hidden gatekeeper

In many of these situations, business owners think the answer is more paperwork, more meetings, or a better pitch. Often, the first real filter is much simpler. It’s the aecb score attached to the business and, in some cases, closely linked financial behaviour around it.

That score helps financial providers decide one thing quickly. Can this business be trusted to meet its obligations on time?

If you already track margins, ageing, and stock turn, treat your credit profile the same way. Good operators use data to spot friction early. That’s also why it helps to get instant answers from data when you’re trying to understand what’s slowing decisions inside your business.

Strong businesses still get stuck when cash is trapped between purchase, sale, and collection.

The good news is that the aecb score is not mysterious once you understand how it works. It’s measurable, it can be monitored, and it can be improved.

What Is the AECB Score and Why Does It Matter

AECB score works like a lender’s risk snapshot of your business. It is issued by Al Etihad Credit Bureau, the UAE’s credit bureau, and gives banks, fintech platforms, and trade finance providers a shared way to judge how reliably your company handles credit.

The score is a three-digit rating. In simple terms, it helps a provider answer a practical question fast. If they extend funding today, how likely is this business to pay as agreed?

That matters more than many SME owners realise.

A traditional bank may study financial statements, collateral, and account conduct over time. A fintech provider offering invoice discounting or dealer financing also needs comfort, but often with much faster turnaround. Your AECB score helps shape that first impression. It can influence whether your file moves ahead quickly, gets priced more cautiously, or needs extra review before any offer is made.

Why it matters beyond bank loans

Many owners hear “credit score” and think only about term loans. In the UAE, the score also affects access to newer working capital tools that depend on speed and trust.

Take two common situations. A distributor wants dealer financing to move more stock without tying up all its cash. An automotive business wants funding against receivables instead of waiting for customers to pay. In both cases, the provider is not only looking at sales. They are judging payment behaviour, existing obligations, and whether the business looks controlled or strained.

Your AECB score becomes part of that judgement.

A strong score can help you access more flexible funding options that match how SMEs operate. A weaker score can limit those options, reduce approved limits, or increase the cost of capital. For a business trying to grow, that difference affects stock purchases, supplier negotiations, and how quickly you can turn opportunities into revenue.

What the score signals in practice

The score is not just an admin record. It is a signal of consistency.

If your business pays on time, manages debt sensibly, and avoids signs of financial stress, the score usually supports that story. If repayments are irregular or credit behaviour looks unstable, providers may treat the business as higher risk even if sales look healthy on paper.

That is why ambitious SME owners should treat the AECB score like any other operating metric. You would not wait until year-end to discover your margins were slipping. Use the same discipline here. Monitor it early, understand what it is saying, and fix issues before you apply for funding.

Practical rule: Review your AECB position before you need capital, not when payroll, inventory, or supplier pressure forces a rushed application.

For UAE SMEs, the AECB score affects more than approval odds. It affects your access to faster, more flexible capital structures that can support growth without relying only on a standard bank loan.

Understanding Your AECB Score Breakdown

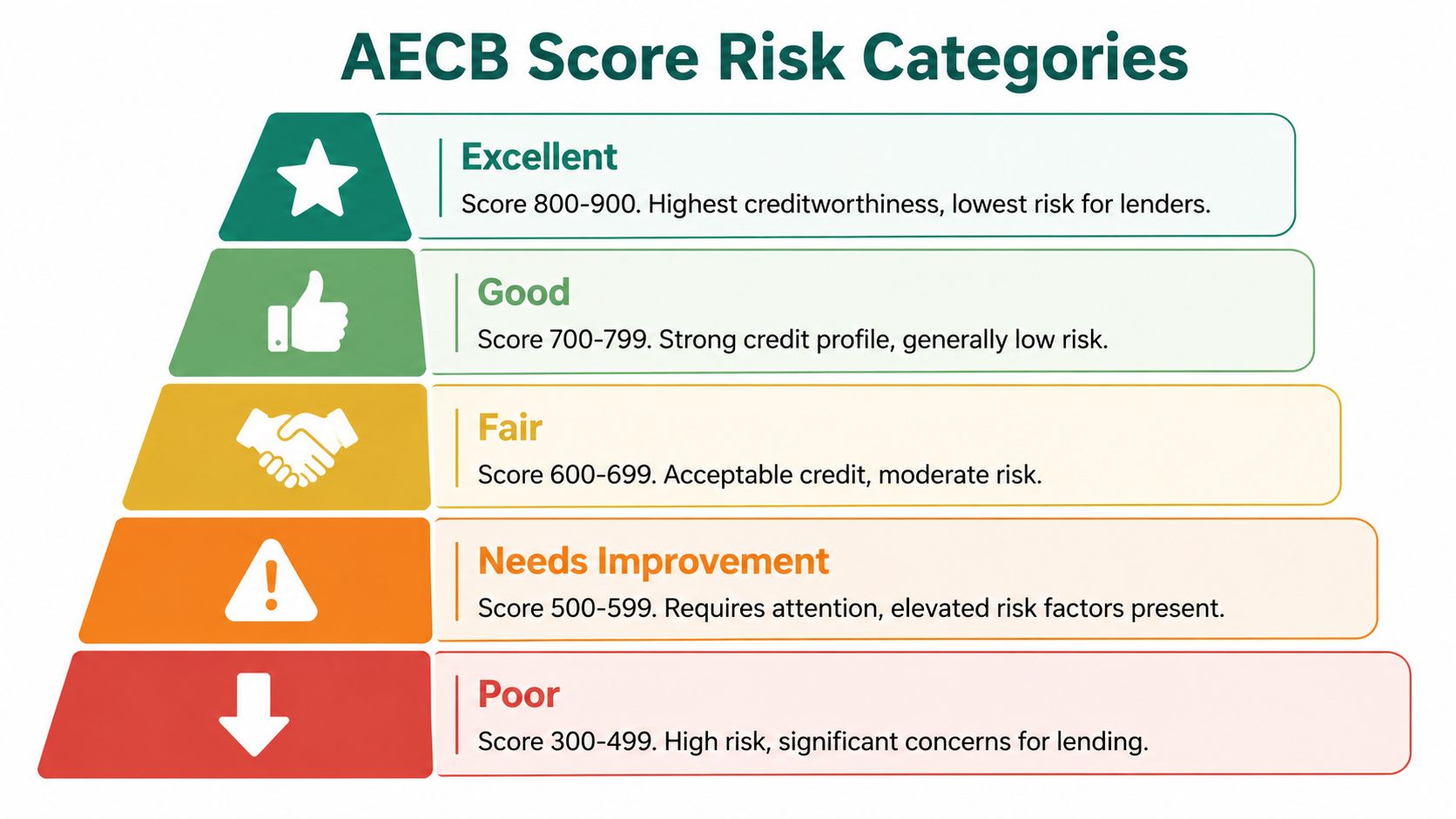

AECB score bands help a lender place your business into a risk bracket quickly. The number is the headline. The key question is what that headline tells a bank, fintech, or dealer finance provider about your likely repayment behaviour.

How the ranges are commonly read

These bands are commonly read in a simple way:

- 300 to 499

Poor. This usually signals serious repayment risk. Many providers will either decline the application or approve only on very restrictive terms. - 500 to 649

Fair. The business may still get funding, but limits, pricing, and conditions are often less attractive. - 650 to 699

Good. This range usually shows acceptable credit discipline and can support more standard funding conversations. - 700 to 749

Very Good. Providers often see this as a stronger sign of control and consistency. - 750 to 900

Excellent. This range usually gives a business access to the widest set of options and the strongest negotiating position.

The easiest way to read these categories is to compare them to traffic lights. Lower bands create friction. Mid-range bands keep options open. Higher bands help the application move faster because the provider sees fewer warning signs at first glance.

That matters if you are comparing a traditional facility with newer funding products. A lender reviewing business bank loan eligibility requirements may focus heavily on financial statements and collateral. A fintech offering invoice discounting or dealer financing will still care about those items, but the AECB profile often shapes how quickly they can get comfortable with your business and what limit they are willing to extend.

What low risk and high risk look like

A low-risk profile usually highlights that payments are steady. Existing obligations appear manageable. The file does not show repeated signs of stress.

A high-risk profile feels less predictable. There may be delayed payments, overextended borrowing, or cheque issues that suggest weak cash control. For a provider, uncertainty is expensive. It can reduce approval chances, shrink available limits, or push your business toward costlier forms of capital.

This is why the score breakdown matters more than many founders expect. It helps explain why two businesses with similar revenue can get very different responses from the market. One gets access to flexible working-capital tools that support inventory, supplier timing, or vehicle turnover. The other is told to accept stricter terms or wait.

If you already track customer retention, the logic is similar to Suby's guide to churn analysis. One summary number is useful, but its full value comes from understanding the drivers behind it and acting before the trend becomes a financing problem.

Key Factors That Influence Your Business Score

Most business owners know late payments are bad. Fewer realise how many other signals can shape the aecb score.

The biggest drivers

Your score is built from real financial behaviour, not guesswork. Here are the main areas business owners should watch:

- Payment discipline matters most

If your business pays obligations on time, that supports a healthier profile. If payments slip, the score can suffer. - Existing debt affects perception

A business carrying obligations it can clearly manage looks different from one that appears stretched. - Bounced cheques are a serious warning sign

In the UAE, bounced cheques are heavily penalised in the score model because they suggest instability. - Delinquent instalments hurt quickly

Missed repayments, especially repeated ones, can shift your business into a higher-risk bracket.

Alternative data now matters too

A major model expansion means the system doesn’t rely only on traditional borrowing history. According to WAM’s report on AECB score coverage expansion, AECB expanded scoring coverage to over 90% of the 13 million entities in its registry, up from 70%, by including data such as monthly salary history, cheque clearances, and utility and telecom payments.

That change matters for SMEs with limited bank borrowing history. It means a business can still build a score through disciplined everyday financial activity.

The same WAM report notes that a projected 2026 upgrade also allows faster recovery from delinquency, with movement out of the red zone possible in six months rather than 24 months in the earlier model.

What owners often miss

Some businesses focus only on bank obligations and forget the rest of their payment ecosystem. That’s a mistake. Utility bills, telecom accounts, and cheque behaviour can all contribute to how your profile is assessed.

If you’re already looking closely at customer retention and revenue leakage, the same habit applies to credit hygiene. Operational discipline compounds over time. For a useful framework on tracking avoidable loss patterns, see Suby's guide to churn analysis. The logic is different, but the management mindset is similar.

You should also understand how providers assess broader eligibility, not just the score itself. This overview of bank loan eligibility in the UAE helps clarify the wider checks many businesses face.

Businesses with thin borrowing history can still build credibility through clean, consistent payment behaviour across everyday obligations.

How to Check Your Business AECB Score

A common mistake happens right before a funding application. An SME owner applies for invoice discounting, dealer financing, or a working capital line, then finds out the business credit profile has an error, an old payment issue, or a lower score than expected. By that point, your options are narrower and the conversation starts from weakness instead of preparation.

Check your business AECB score before you need capital, not during the approval process.

AECB provides access through its official website and app. You can request your business credit information there and review the score alongside the underlying report. As noted earlier, the business report gives useful historical detail, which matters because lenders and fintech providers do not assess only one number. They also look at the pattern behind it.

What to do in practice

Start with the official AECB channel.

Use the AECB app or website, so you are reviewing current information rather than an old PDF saved by someone on your team.

Then look past the headline score. A score is like a dashboard warning light. It tells you something needs attention, but the report shows where the issue sits. Check whether the business name, facilities, payment history, and reported obligations are accurate.

Time your review around real business decisions. If you are preparing to increase stock, extend payment terms to larger buyers, or use a facility tied to receivables, check your profile first. For automotive businesses managing stock cycles and supplier pressure, this matters even more. A business dealing with irregular inflows should also tighten its auto dealer cash flow planning in the UAE so credit checks and funding requests happen from a position of control.

A simple review routine

- Check before any financing application

Review your score and report before approaching a bank, fintech platform, or trade finance provider. - Confirm the business details are correct

Look for reporting errors, outdated facilities, or mismatched payment records. - Save and track each report internally

Keep a dated record so your finance lead can spot changes over time, the same way they monitor receivables ageing and overdue payables. - Flag issues early

If something looks wrong, raise it through the official process before it affects a live credit decision.

This habit is small, but it changes how you access capital. A business that monitors its AECB profile regularly is easier for lenders and fintech providers to assess, and usually better positioned to get faster, more flexible funding.

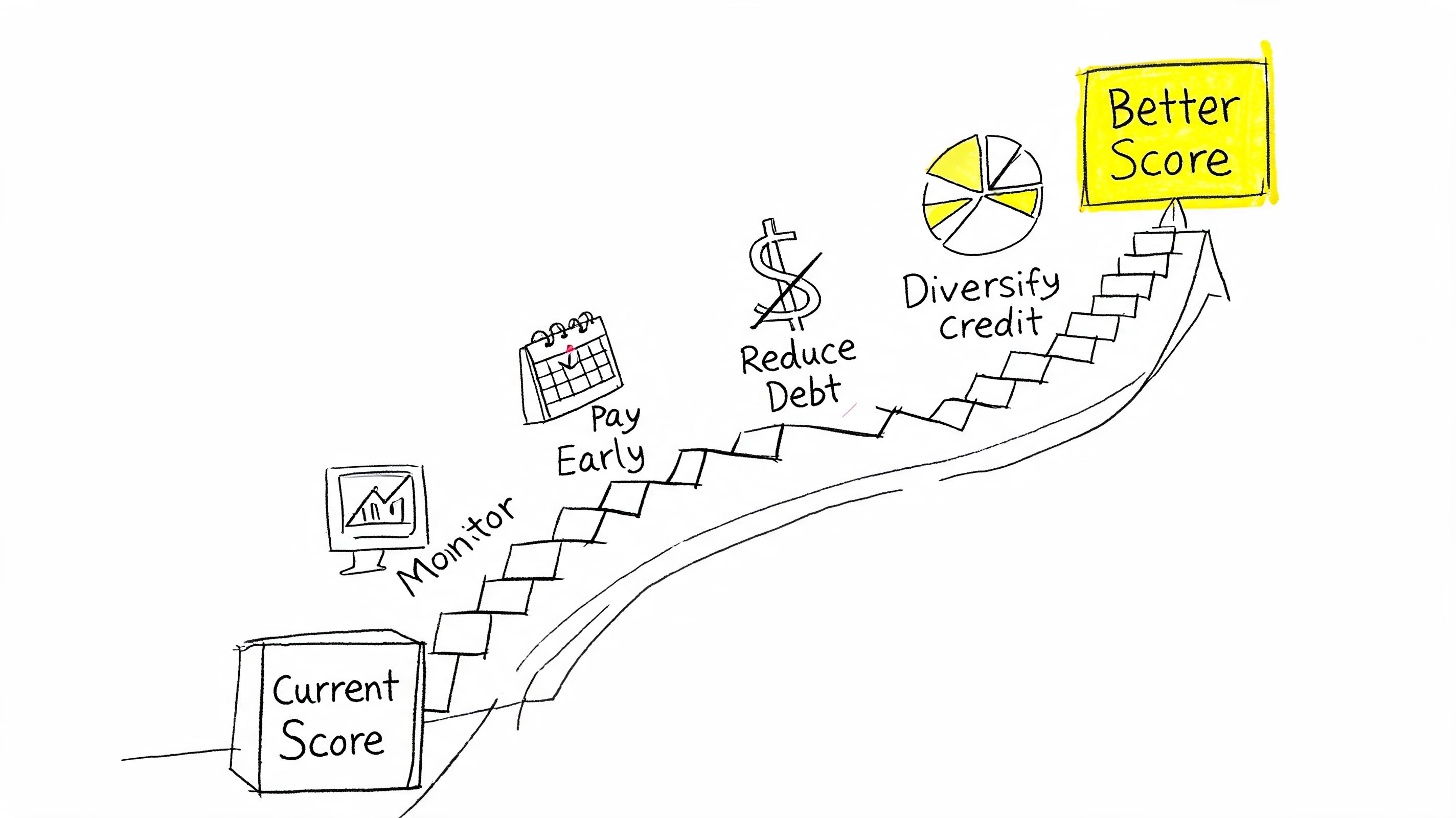

Actionable Steps to Improve Your AECB Score

A low or average aecb score is not permanent. It’s a signal that your operating habits need tightening.

The habits that make the biggest difference

Start with the basics, then stay consistent.

- Pay before due dates, not on the edge of them

If your business regularly pays late, even by a short period, your profile can weaken over time. Build payment buffers. - Prevent bounced cheques completely

This is one of the clearest danger signals in the UAE credit environment. Don’t issue cheques unless funds are already planned and available. - Reduce avoidable debt pressure

If multiple obligations are straining cash flow, restructure operations where possible and prioritise cleaner repayment behaviour. - Review your credit report for mistakes

Errors happen. If information is inaccurate, challenge it promptly through the official process.

Build a repeatable credit discipline

Improvement usually comes from routine, not one dramatic action. Put controls around the areas that tend to slip during busy periods:

- Set internal payment calendars so bills, instalments, and supplier obligations don’t depend on memory.

- Assign ownership to one finance team member who checks the report and monitors problem accounts.

- Forecast cheque commitments alongside incoming collections so surprises don’t create avoidable damage.

- Separate growth decisions from optimism. If inventory or expansion plans will tighten cash too much, slow the move before your score reflects the strain.

Clean credit behaviour is usually the result of clean finance operations.

If you improve the process, the score often follows.

How a Strong AECB Score Unlocks Modern Financing

A supplier is ready to release stock today. A customer has approved a large order. Your sales pipeline looks healthy, but the cash is still trapped in invoices or inventory. In that moment, your AECB score starts to matter in a very practical way.

A strong score helps lenders and fintech providers assess your business faster. That can shorten the distance between an opportunity and the funding needed to act on it. For an SME, that often means less waiting, fewer manual checks, and better access to short-term working capital tools.

This matters more with modern financing than with traditional term loans. Products like invoice discounting, Buy Now, Pay Later for B2B purchases, and dealer financing are built around speed, transaction quality, and repayment confidence. Your AECB profile acts like a business health signal. A cleaner signal makes approvals easier and pricing more competitive.

What that means in real business terms

If you are a wholesaler, a stronger score can help you turn approved invoices into cash while the order book is still active. If you run an automotive business, it can improve access to dealer finance that frees up money tied up in vehicles, so you can rotate stock faster instead of watching margin sit on the forecourt.

That speed changes decisions.

You can buy in volume when suppliers offer better terms. You can accept larger customer orders without stretching payroll or rent. You can keep inventory moving without relying on expensive stopgap borrowing.

For UAE auto dealers, this connection is especially clear. This case study on how Instacar and Comfi help car dealers in the UAE access faster funding shows how quicker capital access supports better stock movement and day-to-day commercial flexibility.

If your business is growing faster than your cash cycle, Comfi can help you explore flexible options such as Invoice Discounting, Buy Now, Pay Later, and Automotive Dealer Financing. If you already know your aecb score, you will be in a much better position to assess what fits and move quickly.

Related Reading

- Vehicle Dealer Working Capital Dubai: 2026 Growth Guide

- Inventory Financing vs Invoice Discounting for UAE SMEs

- Vehicle Dealer Working Capital Dubai: 2026 Growth Guide

- Inventory Financing for UAE SMEs: A Practical Guide to Unlocking Growth

Looking to improve your cash flow? Explore Comfi's Dealer Financing solutions. Get started today.