A Practical Guide to Business Credit Lines for Sustainable Growth

A business credit line is a flexible financial tool your business can access as needed, unlike a standard, one-time loan. Think of it as a dedicated reserve of capital, ready for opportunities or unexpected costs. You can use it, repay it, and then draw from it again.

Understanding a Business Credit line

Let's use an analogy. A traditional loan is like receiving a large container of water all at once. You begin making fixed repayments immediately, whether you use all the water or not. A credit line, however, is like having access to the tap itself. You can open it to draw exactly what you need, up to a pre-approved limit.

This on-demand access gives your business tremendous operational agility. Instead of going through a lengthy application process for a new loan each time a need arises, you have pre-approved capital ready. This model is ideal for managing fluctuating expenses, seizing time-sensitive inventory deals, or covering unexpected shortfalls without disrupting your cash flow.

Key Terms You Should Know

To make the most of a credit line, it's helpful to understand a few core concepts. These terms define how you can use the facility and what its costs are.

- Credit Limit: This is the maximum amount of money you are permitted to draw at any one time.

- Draw Period: This is the specific window of time during which you can access funds from your credit line. After this period ends, you typically move into a repayment-only phase.

- Interest: A key benefit is that you only pay interest on the funds you have actually used, not on the entire available credit limit.

The demand for such adaptable financial solutions is clear. In the UAE, consumer credit grew significantly from AED 14,572 million in Q1 2001 to a peak of AED 540,864 million, a trend that reflects the growing need for flexible capital among businesses as well. You can explore more about this growth in consumer credit in the UAE.

A Breakdown of Different Credit Line Types

Not all credit lines are the same. Just as you wouldn’t use a hammer for every task, different financial situations require different tools. Understanding the main types is the first step to selecting the one that best suits your business operations and future goals.

The primary distinction is between revolving and non-revolving credit. They serve different purposes, and choosing the wrong one can lead to mismanagement of your cash flow. For a supplier in Dubai, for instance, the choice depends on a simple question: do you need an ongoing, flexible buffer for your cash flow, or a one-time injection of funds for a specific project?

Revolving Credit Lines

Think of a revolving credit line as your business's financial multi-tool—it’s flexible, reusable, and perfect for day-to-day challenges. It functions much like a business credit card. You receive a set credit limit, you can draw from it whenever needed, repay it, and the full amount becomes available to use again.

This setup is invaluable for:

- Bridging Cash Flow Gaps: If payroll is due but you're waiting for a large client payment, a revolving credit line allows you to cover immediate expenses. It is essential for businesses with long payment cycles.

- Seizing Inventory Opportunities: When a supplier offers a significant bulk discount for a limited time, a revolving line lets you capitalize on the opportunity without depleting your cash reserves.

- Managing Unexpected Events: If a critical piece of equipment breaks down, you can tap into your credit line for repairs and maintain smooth operations instead of derailing your budget.

Non-Revolving Credit Lines

Conversely, a non-revolving credit line is more like a specialized tool—designed for a single, specific purpose. Once you draw the funds, the credit does not replenish as you pay it back. When the balance is paid in full, the account is typically closed.

This type is structured for one-off projects with a clear beginning and end, such as fulfilling a single, massive customer order or funding a short-term expansion project. It offers predictability but lacks flexibility.

For many businesses, a more direct approach is to unlock cash already tied up in their assets. Instead of taking on new debt, you can convert existing documents into fuel for your business. For example, you can learn how invoice discounting helps convert your unpaid invoices into immediate cash, providing a straightforward way for your business to unlock its working capital.

Weighing the Benefits and Risks for Your Business

A credit line can be an incredibly powerful tool, giving your business the agility to do more than just manage day-to-day cash flow. For suppliers and wholesalers, this flexibility is a real strategic advantage. It allows you to act on time-sensitive opportunities, like purchasing a large batch of discounted inventory, without having to empty your operational bank account.

It also serves as a financial shock absorber, helping you navigate seasonal sales cycles. With a credit line, you have a buffer to cover expenses during slower months so you can keep operations running smoothly until the next busy season.

This flexibility is crucial for funding sudden growth. If a massive, unexpected order comes your way, a credit line gives you the power to scale up production immediately. In short, it’s a reliable safety net, ensuring you don't have to turn down a golden opportunity due to a temporary cash crunch.

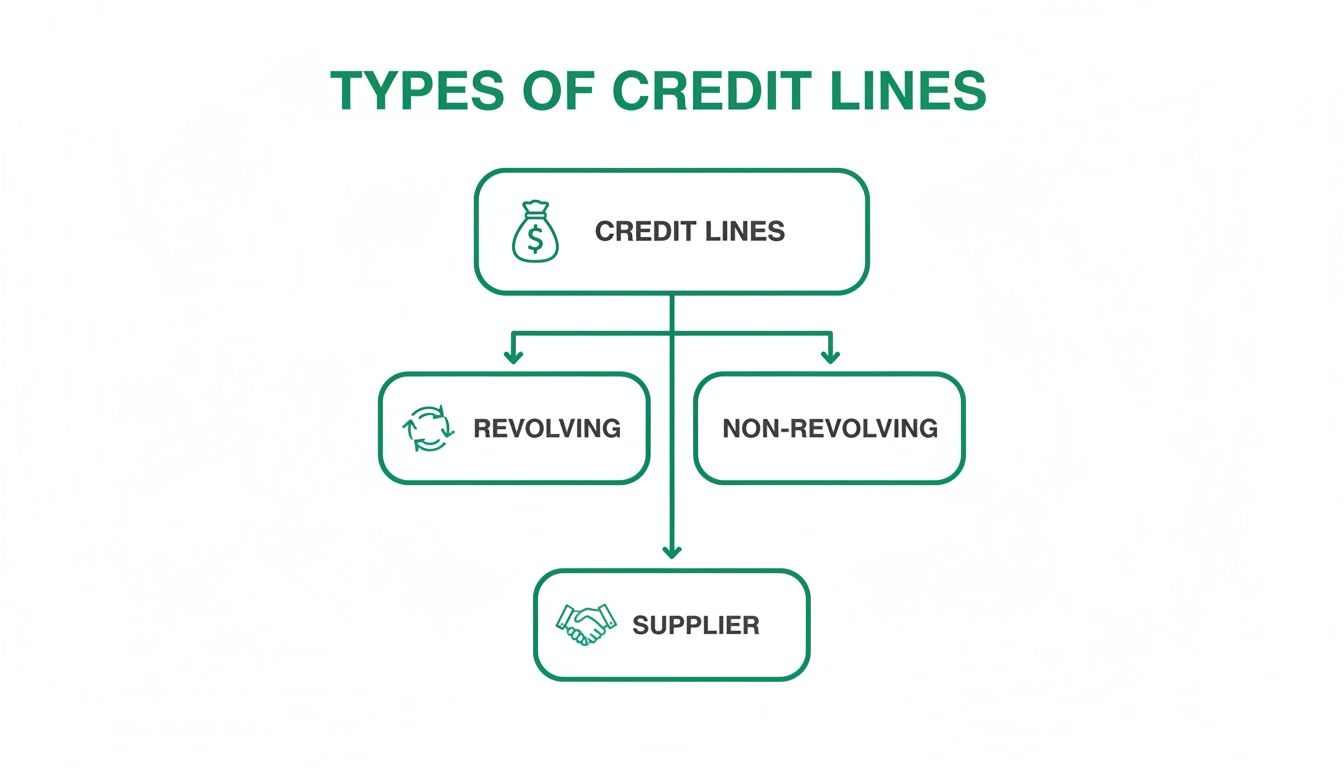

This flowchart illustrates the main types of credit lines you will likely encounter.

As shown, each type is designed for different business scenarios—from the endlessly reusable Revolving line to the single-purpose Non-Revolving option and the more specialized Supplier credit.

Understanding the Potential Downsides

This convenience comes with real risks that demand disciplined management. Easy access to funds can create a temptation to overspend on non-essentials. A more significant danger is using the credit line to cover persistent operational issues instead of addressing their root cause. This can quickly turn a helpful tool into a crippling cycle of debt.

Another major risk is variable interest rates. Unlike a fixed-rate loan, the interest on most credit lines can fluctuate with market conditions. A sudden rate hike can increase your borrowing costs overnight, putting unexpected pressure on your bottom line and making repayments more difficult to manage.

This double-edged nature is evident when looking at business credit trends. For example, loans to the private sector in the UAE recently reached a record AED 1,448,467 million. This demonstrates how vital credit access has become for SMEs striving to stay competitive, but it also highlights the absolute necessity of smart management to protect long-term financial health. You can discover more about private sector trends in the UAE to see the full picture.

Securing a Credit Line in the MENA Region

Obtaining a credit line in the MENA region involves more than just a good business idea. Lenders, from traditional banks to modern fintech platforms, require solid proof of your business's health and stability. While specific requirements vary, a few key criteria are always on their checklist. Knowing what they are looking for is the first step to preparing a successful application.

The first hurdle is often your business's age. Most lenders prefer to see that you have been operational for at least one to two years. This track record demonstrates stability and provides a financial history they can analyze.

What Lenders Really Look For

After confirming your time in business, the next deep dive is into your financial health. They will want to review your financial statements to understand your profitability, cash flow, and overall stability. This is where having clean, organized records becomes a significant advantage.

Here are a few key metrics they will focus on:

- Minimum Annual Revenue: Many lenders have a specific revenue threshold you must meet to be considered for an application.

- Healthy Financial Statements: This means your balance sheet, income statement, and cash flow statement should all reflect a well-managed business.

- Valid Legal Documents: All your trade licenses and registration documents must be current and valid in your country of operation.

A common pitfall for businesses is applying with disorganized or incomplete paperwork. Preparing your financial statements, trade licenses, and bank records before you apply streamlines the process and presents you as a professional and reliable partner.

The traditional bank route often involves a longer, more paper-intensive process and may require physical collateral, such as property or inventory, to secure the credit line. Fintech platforms, in contrast, typically offer a faster, digital application process that relies more on your real-time business data and revenue consistency.

Regardless of the path you choose, a strong application paints a clear picture of a well-run business capable of comfortably managing its repayments. For a more detailed look at what lenders want, check out our insights on bank eligibility criteria in our detailed guide. A little preparation goes a long way.

Credit Lines vs. Loans: What’s the Difference?

It’s easy to get confused when choosing between a business credit line and a traditional loan, but the core difference is simple. A loan is a one-time transaction, while a credit line provides ongoing access to funds.

Here’s a practical way to think about it: a loan is like buying a large, sealed water bottle. You get all the water at once and start paying for the entire amount immediately, regardless of how slowly you use it.

A credit line, on the other hand, is like having a tap connected to your water supply. You turn it on when you need it, take exactly the amount you want, and only pay for what you actually use. This distinction affects everything from interest payments to your repayment schedule, making each tool suitable for different business needs.

Key Distinctions at a Glance

The most critical differences relate to how you receive the money, how you repay it, and how interest is calculated. Understanding these points will help you determine which tool aligns with your financial goals.

Here is how they compare:

- Funding Structure: With a loan, you receive a single lump sum. A credit line gives you a pool of capital to draw from as needed, up to your approved limit.

- Interest Calculation: This is a major difference. For a loan, you pay interest on the entire amount from day one. With a credit line, you only pay interest on the funds you have drawn.

- Repayment Terms: Loans typically have fixed monthly payments over a set period. A credit line is far more flexible, allowing you to repay the balance and immediately free up that credit for reuse.

The UAE’s financial market offers a wealth of options for businesses. Total domestic credit in the UAE has reached USD 472.8 billion, indicating significant available liquidity. This robust market allows companies to be selective and find the ideal tool for their needs. You can discover more about domestic credit growth in the UAE to see the full picture.

Smarter Ways To Unlock Your Working Capital

While a flexible credit line is a solid tool, it's not the only way to improve cash flow. Modern solutions are designed to help you access the money you've already earned that is currently tied up in outstanding invoices.

Instead of taking on new debt, these alternatives focus on gaining faster access to your own revenue. It's a smart way to achieve the liquidity needed for growth while maintaining a healthy balance sheet.

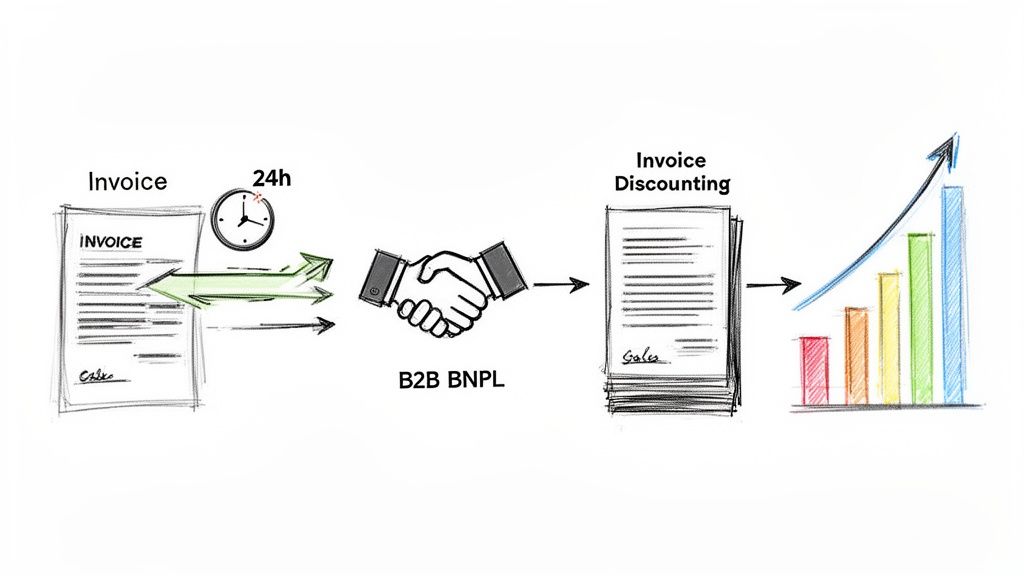

Turn Invoices Into Immediate Cash Flow

Imagine receiving payment for your work in as little as 24 hours, instead of waiting 30, 60, or even 90 days. That is the simple principle behind invoice discounting. You essentially convert your unpaid invoices into immediate cash, empowering you to fund operations, purchase more inventory, or seize new opportunities without delay. To better understand this concept, you can learn about the essentials of working capital.

This method directly transforms your accounts receivable into accessible funds. It’s not about borrowing; it’s about unlocking the value of sales you’ve already made, which can fundamentally improve how you manage your business finances.

Boost Sales With Flexible B2B Payment Terms

Another powerful tool is offering B2B Buy Now, Pay Later (BNPL) terms to your customers. By providing clients with flexible payment options, you can make it easier for them to purchase more from you, potentially increasing order sizes and boosting your sales by up to 30%.

Beyond these direct options, it is always beneficial for businesses to implement various strategies to improve cash flow to maintain strong financial health.

A Few Common Questions, Answered

If you’re considering a credit line, you likely have some questions. Here are straightforward answers to common queries from SME owners in the MENA region.

What’s the Real Difference Between Secured and Unsecured Options?

The distinction lies in collateral.

A secured credit line is backed by a business asset you own, such as inventory, equipment, or property. Because you are providing collateral, the lender views it as less risky. The benefit for you is typically a higher credit limit and a lower interest rate.

An unsecured credit line, on the other hand, does not require any collateral. This makes it a riskier proposition for the financial institution, so they will usually offer a lower limit, charge higher interest, and have stricter eligibility requirements for your business to qualify.

How Is the Interest Actually Calculated?

This is where a credit line differs from a loan. You only pay interest on the money you actually use, not the total amount available to you.

For example, if you have an AED 100,000 credit line but have only drawn AED 20,000 to cover a short-term expense, you will only be charged interest on that AED 20,000. As soon as you repay it, the interest charges stop.

Can I Use It to Pay Off Other Business Debts?

Yes, and this can be a strategic move. Many business owners use a credit line for debt consolidation.

If the interest rate on your credit line is lower than the rates on other debts (like business credit cards), you can use the funds to pay them off. This consolidates everything into a single payment and can save you a significant amount in interest. Just be sure you have a solid repayment plan, as this strategy requires discipline to be effective.

Ready to explore smarter, debt-free alternatives to a traditional credit line? With Comfi, your business can unlock the capital tied up in its invoices or offer flexible B2B payment terms to boost sales. Discover how Comfi can accelerate your cash flow.