What Is Factoring: Your 2026 Guide to Business Cash Flow

A strong sales month can create a cash problem.

You deliver goods, issue the invoice, and book the revenue. On paper, the business looks healthy. In practice, the cash may not arrive for months. Meanwhile, payroll is due, suppliers want paying, and the next order is already waiting.

That gap is where many SMEs get squeezed. If you're asking what is factoring, the short answer is simple. It's a way to turn unpaid invoices into cash sooner by selling those receivables to a third party at a discount, instead of waiting for the customer to settle.

For firms across the UAE and wider MENA region, that matters. Long payment cycles are common in B2B trade, and access to finance remains a meaningful constraint for many companies. The World Bank's Enterprise Surveys for MENA economies show that a significant share of firms, often in the double digits, identify access to finance as a major obstacle to operations and expansion, as noted in this regional overview of factoring and finance constraints.

Unlocking Cash Flow Trapped in Unpaid Invoices

A wholesaler in Dubai lands a large order from a well-known buyer. Good news. The buyer wants standard trade terms. Less good news. Payment won't come until the invoice matures.

That creates a familiar strain. The business has done the hard part already. It sourced stock, delivered it, and raised the invoice. But the cash is now stuck in accounts receivable rather than sitting in the bank account where it can be used.

What factoring means in plain language

Factoring is a short-term trade finance tool. A business sells its unpaid invoices to a factoring company, usually at a discount, in exchange for immediate cash. The key point is that this is tied to receivables that already exist. You are converting a future customer payment into cash you can use now.

It's like selling a post-dated cheque to someone who is willing to pay you today for slightly less than its full value.

That distinction matters because many owners still treat receivables as if they are the same as cash. They aren't. Receivables are promises. Cash is what pays salaries, duty, freight, rent, and the next supplier deposit.

Why this matters for MENA SMEs

In the UAE and across MENA, many growing businesses don't fail because they lack demand. They stall because growth absorbs cash faster than customers release it.

Practical rule: If your business is profitable but still feels short of cash, your issue is often timing, not sales.

This is especially true in import-heavy and B2B sectors where invoice values are meaningful and payment terms are standard practice. Businesses in wholesale and distribution often need a sharper grip on receivables than they realise. If you want a useful refresher on process discipline, Bookkeeping and Accounting of Florida's AR insights offer a practical checklist for tightening receivables management.

It also helps to understand the asset at the centre of the discussion. If you want the accounting side broken down clearly before evaluating funding options, this guide to accounts receivable basics is worth reading.

How the Factoring Process Works Step by Step

Most owners assume factoring is paperwork-heavy and slow. In reality, the process is usually straightforward. What matters is the quality of the invoice, the buyer behind it, and whether the underlying sale is clean and well documented.

The commercial sequence

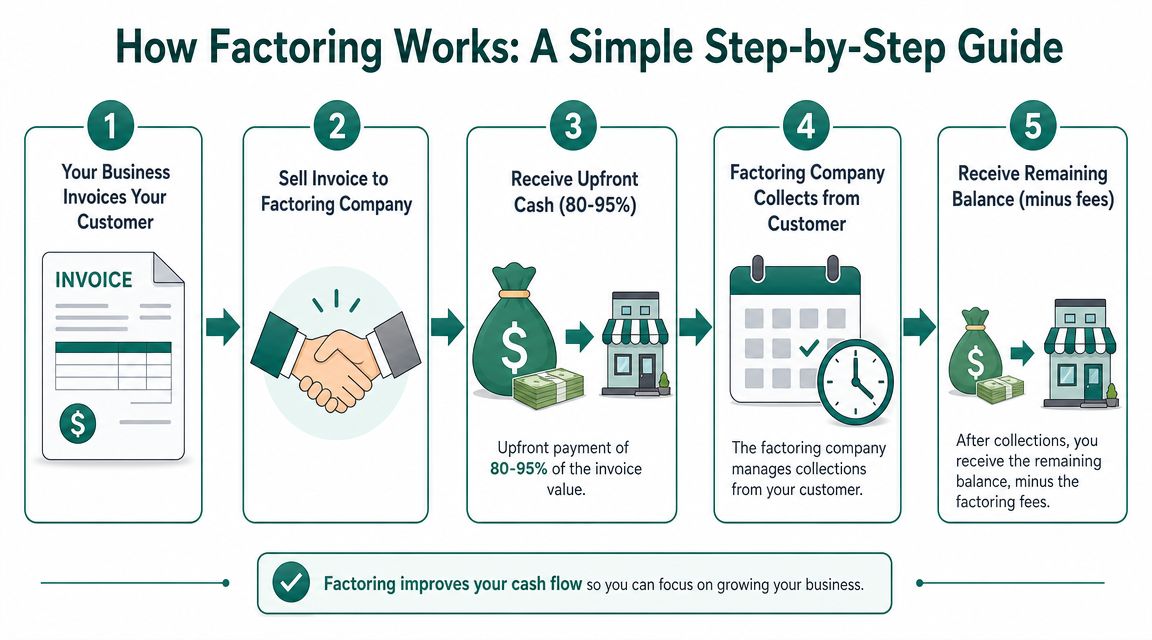

The process starts after you deliver goods or services and issue an invoice to your customer. At that point, you have a receivable on your books. Instead of waiting until the due date, you submit that invoice to a factor for review.

The factor then checks the invoice and the buyer. This is one of the biggest practical differences from a traditional facility. In many cases, the focus is less on your trading history and more on whether your customer is credible, whether the invoice is valid, and whether there are likely to be disputes.

Once approved, the factor advances part of the invoice value to your business. A company typically receives about 70% to 90% of the invoice's face value, often within 24 hours of approval, according to Qualco's explanation of the factoring process. That speed is especially useful when customer terms run to around 90 days or longer.

What happens after the advance

There are usually two cash events.

First, you receive the upfront advance. That gives you immediate liquidity to keep operating, restock, or fulfil the next order.

Second, when the customer pays the invoice, the factor settles the remaining balance to you after deducting its charges. The exact mechanics depend on the agreement, but the business logic is simple. The factor gives you speed. In return, it earns a fee and takes on administrative work, and sometimes part of the payment risk depending on the structure.

A typical workflow looks like this:

- You complete the sale and issue the invoice.

- You assign or submit the invoice to the factor.

- The factor reviews the buyer and invoice for validity and risk.

- You receive the advance once approved.

- The final settlement happens later when the customer pays.

Clean paperwork shortens the process. Missing delivery notes, unclear purchase orders, and disputed invoices slow everything down.

Where SMEs usually get caught out

The weak point is rarely the invoice itself. It's the supporting evidence. If your internal records are messy, the factor will hesitate. If your customer has a history of disputes, expect more questions. If one buyer makes up most of your receivables, concentration risk becomes a real issue.

In practice, businesses get the best results from factoring when they do three things well:

- Issue accurate invoices promptly so there's no mismatch between delivery and billing.

- Keep proof of delivery organised because factors care about evidence, not verbal assurances.

- Know the buyer profile since the buyer's payment behaviour often drives the decision.

Key Factoring Types Explained

Not all factoring arrangements solve the same problem. Some prioritise speed. Some prioritise risk transfer. Some preserve more control over the customer relationship. If you choose the wrong structure, the product can feel expensive or awkward even when the core idea is sound.

Recourse and non-recourse

The first distinction to understand is recourse versus non-recourse.

With recourse factoring, the business still carries the risk if the customer doesn't pay in the agreed circumstances. This usually makes the arrangement simpler and may affect pricing, but it also means you haven't fully passed the problem away. If the buyer fails to pay, the factor may come back to you.

With non-recourse factoring, the factor assumes the credit risk of non-payment within the scope of the agreement. This can be valuable when you're supplying larger buyers, expanding into unfamiliar customer accounts, or trying to reduce exposure to delayed settlement. It does not mean every problem disappears. If the invoice is disputed because goods were defective or delivery terms weren't met, that is a different issue from pure buyer insolvency or non-payment risk.

The phrase "non-recourse" sounds broader than it often is. Read the dispute clauses carefully.

Factoring and invoice discounting are not the same

Many generic explainers fall short. They bundle everything under "invoice finance" and leave the owner to figure out the legal and operational details later.

The distinction is fundamental. Factoring is the sale of receivables, while invoice discounting is borrowing against receivables, as outlined in this definition of factoring and invoice discounting). That difference affects collections, control, and sometimes accounting treatment.

In practical terms:

- Factoring usually involves the financier taking a more active role around the receivable.

- Invoice discounting usually allows the business to keep more control over collections while using the invoice as the basis for liquidity.

- The better option depends on whether you care more about customer-facing control, speed, confidentiality, or risk allocation.

If you're weighing those trade-offs in a UAE context, this comparison of invoice discounting and factoring is a useful next step.

Notification and non-notification

Another useful distinction is whether the customer is told.

Notification factoring means the buyer knows the receivable has been assigned and pays the factor directly. This is common and often operationally cleaner.

Non-notification structures keep the arrangement less visible to the customer, with the supplier retaining more of the collection interface. That can matter if the commercial relationship is sensitive or if the business wants tighter control over customer communications.

A practical way to choose is to ask:

- Do you want collections support? If yes, a factoring structure may suit you better.

- Do you want to keep customer communication in-house? If yes, a discounting-style structure may fit better.

- Is buyer default your main worry? If yes, focus on how risk is allocated, not just how fast cash is released.

Understanding the Costs Risks and When to Use It

Factoring is useful when timing is the primary problem. It's less useful when margins are already thin, invoices are frequently disputed, or customers are weak credits. The product works best when the underlying trade is solid.

What you are actually paying for

The cost is usually split into two parts. There is a financing commission for advancing cash against the invoice, and there is a factoring commission for administration, reminders, and risk management. Société Générale's trade-finance glossary explains this structure clearly in its overview of factoring costs and receivables finance mechanics.

That structure has two immediate consequences:

- Time matters. The longer the invoice remains outstanding, the more the financing side of the cost matters.

- Buyer quality matters. If the buyer is viewed as riskier, the overall pricing usually becomes less favourable.

This is why owners shouldn't ask only, "What does it cost?" The better question is, "What does it cost relative to the opportunity I realize by getting the cash now?"

The risks owners underestimate

The biggest operational risk is not always non-payment. Often it's dispute risk.

If the customer says the shipment was incomplete, the specification was wrong, or the invoice doesn't match the purchase order, the receivable becomes harder to fund and harder to collect. Factoring doesn't fix poor commercial execution.

Watch for this early: A disputed invoice is a weak funding asset, even when the customer is large and well known.

Concentration is another issue. If a large share of your receivables sits with one or two buyers, your liquidity becomes heavily linked to their payment habits. In the UAE, that can become uncomfortable quickly when one major account pays late.

When factoring tends to work well

Factoring is often a strong fit in situations like these:

- Growth outpacing cash collection: You're winning orders faster than customers are paying.

- Inventory-heavy trading: You need cash to replenish stock before prior invoices mature.

- Large corporate buyers: Your customers are credible, but their payment cycles are slow.

- Cross-border supply chains: Cash timing is under pressure because landed costs arrive before customer payments do.

If your issue is recurring and tied to receivables timing, factoring can be a sensible tool. If your issue is weak demand, poor margins, or persistent billing errors, it won't solve the core problem.

Factoring Compared to Traditional Business Options

A bank loan, a line of credit, and factoring can all help with liquidity. They are not interchangeable. Each one solves a different kind of cash problem.

When a bank facility makes more sense

A bank loan is usually the better fit when you need capital for a defined long-term purpose, such as equipment, expansion, or a planned investment with a clear repayment schedule.

A line of credit is often useful when the business has uneven short-term needs and wants flexibility to draw and repay cash as required.

Those tools usually rely more heavily on your own balance sheet, financial history, and available collateral. That isn't a flaw. It's how those products are designed.

Why factoring feels different in practice

Factoring is tied directly to sales you have already made. The funding logic sits closer to the invoice and the buyer than to a broad assessment of the company's borrowing profile.

That changes the conversation in several ways:

- Speed: It can move faster because the review is centred on receivables and buyer quality.

- Scalability: It often grows with invoice volume rather than staying fixed at a static facility size.

- Repayment mechanics: The customer payment sits at the centre of the transaction instead of a fixed instalment schedule from your operating cash.

This is why factoring often suits wholesalers, distributors, and suppliers better than term borrowing when the cash issue is caused by payment delay rather than lack of profitability.

How to think about the trade-off

Use a simple filter.

Choose a loan when you need capital for a long-lived asset.

Choose a line of credit when cash swings are temporary and your banking profile is already strong.

Choose factoring when your cash is trapped in unpaid invoices and the receivable itself is the clearest asset available.

If the problem starts after you invoice, start by looking at receivables tools before adding general debt.

The legal and operational distinction from discounting matters here too. Factoring and invoice discounting can both convert receivables into capital, but they shift control and risk in different ways. The earlier linked guide covers that in more detail, and it's worth reviewing before you speak to any provider.

Choosing the Right Factoring Partner in the UAE

The provider matters as much as the product. Two firms can both offer invoice-based liquidity and still deliver very different experiences once documents, buyer disputes, and payment delays enter the picture.

What to check before signing

Start with operational clarity, not marketing language.

Ask how the provider reviews invoices, how collections are handled, and what happens when a buyer delays payment or raises a dispute. For UAE suppliers, that last point is critical. The value of a factoring arrangement often depends less on the supplier's own balance sheet and more on receivables quality and the factor's ability to manage buyer risk effectively, especially in a non-recourse structure, as discussed in the US Chamber's article on understanding factoring and receivables risk.

Then check the day-to-day practicals:

- Process quality: Can your team upload invoices, monitor status, and track settlements without endless email chains?

- Documentation standards: Does the provider explain what proof is needed before approval?

- Fee transparency: Are the commercial terms clearly broken out so your finance team can model the impact?

- Collections approach: Will the provider protect your customer relationship, or create friction?

- Sector fit: Do they understand the realities of wholesale, automotive, electronics, distribution, or logistics?

What works well in the UAE market

In this market, the best fit is often a provider that understands trade flow rather than one that only understands generic SME underwriting. Buyer quality, shipment evidence, and concentration risk matter a lot more than glossy sales language. It's also worth looking for digital capability.

Teams handling frequent invoices benefit from clean dashboards, faster onboarding, and fewer manual checks. For businesses with operational complexity, especially freight and multi-stop deliveries, this piece on AR automation for logistics teams is a useful companion read because it shows how document handling affects collection speed and accuracy.If you're comparing providers in the local market, this shortlist of invoice discounting companies in the UAE can help frame the options.

Beyond factoring: how B2B BNPL changes the equation

Most factoring solutions are reactive. You've already delivered, the invoice is already sitting unpaid, and you're selling it at a discount just to unlock 70–80% of the value upfront. It solves a cash flow problem, but it doesn't change the dynamic that created it. B2B Buy Now, Pay Later works differently. Instead of chasing outstanding invoices after the fact, the supplier gets paid 100% upfront (typically within 24 hours) while the buyer gets flexible payment terms. The deal closes faster because payment friction is removed before it becomes a bottleneck.

Where factoring is a cash flow patch, B2B BNPL is a growth tool. The supplier isn't discounting receivables; they're offering better terms to win more business, without taking on the risk themselves. Comfi is one example of this model in the MENA market. It pays suppliers in full upfront with zero processing fees and gives buyers the flexibility to pay over time, all through a digital workflow designed to keep things simple and paper-light. Instead of adding a middleman to the supplier-buyer relationship, it strengthens it.

A good partner should make receivables easier to use, not harder to explain. And the right question isn't just how do I get paid faster. It's how do I remove the payment friction that's slowing down my next deal.