Invoice Discounting vs Factoring: What MENA SMEs Need to Know

When it comes to unlocking cash from your unpaid invoices, the two main players on the field are invoice discounting and factoring. At first glance, they might seem similar, but the real difference comes down to one simple question: who's in control?

Understanding the Core Differences

For SMEs across the MENA region, waiting 30, 60, or even 90 days for a client to pay can bring growth to a grinding halt. Both invoice discounting and factoring are designed to solve this exact problem, but they go about it in completely different ways. Your choice really boils down to how you want to manage your client relationships and public perception.

With invoice discounting, you confidentially use your invoices as collateral to access funds. You maintain full control over your sales ledger and, most importantly, you're still the one who communicates with and collects from your customers. It's your relationship to manage.

Factoring, on the other hand, means you sell your invoices to a third-party company. That company then takes over the entire collections process, which means they'll be contacting your customers directly for payment.

Let's break down the practical distinctions in a clearer way:

- Customer Interaction: With invoice discounting, it's business as usual. You chase your own payments. With factoring, the provider steps in and deals with your customers.

- Confidentiality: Discounting is a private arrangement between you and the provider; your customers never know. Factoring is fully disclosed, so everyone is aware a third party is involved.

- Control: You keep a firm grip on your sales ledger and credit policies with discounting. Factoring means handing that control over.

- Perception: Because it’s discreet, discounting protects your company's image. Some businesses worry that using a factoring service might make them look financially unstable to their clients.

Comfi gives SMEs the best of both worlds in the form of B2B Buy Now, Pay Later (similar to invoice factoring) and invoice discounting, ensuring quick and easy access to capital when needed the most.

How Each Process Unlocks Your Cash Flow

While both invoice discounting and factoring are designed to shorten your cash conversion cycle, the way they get there couldn't be more different. The choice you make has a direct impact on your day-to-day work, who handles your admin, and even how you interact with your customers.

Getting to grips with these workflows is crucial for any business owner. Let's break down what each option actually looks like in practice.

The Modern Invoice Discounting Workflow

Modern invoice discounting is built around two key principles: speed and discretion. It puts you firmly in the driver's seat. The entire process is almost always digital, designed to slot neatly into your existing operations without causing any disruption.

Here’s a practical look at the steps involved:

- Upload and Qualify: You submit an unpaid invoice to a digital platform. Most will give you an instant decision on eligibility, based largely on your customer's credit profile.

- Receive Funds Fast: Once you’re approved, a big chunk of the invoice value—often up to 90%—lands in your account, sometimes in as little as 24 hours.

- Maintain Customer Control: This is the important part. You still manage the relationship with your customer and are responsible for collecting the payment from them on the original due date.

- Settle the Account: After your customer pays you, you simply pay back the advanced amount plus a small, pre-agreed fee to the provider.

This confidential, self-managed approach lets your business unlock cash from invoices without changing a single thing about your customer-facing processes. Your clients never even know it's happening.

The Traditional Factoring Process

Factoring is a much more hands-on service from a third party, and it fundamentally changes how you handle collections. You're not just getting access to funds; you're effectively outsourcing your accounts receivable department.

The typical factoring journey looks like this:

- Sell Your Invoice: You formally sell your invoice to a factoring company.

- Customer Verification: The factor then gets in touch with your customer directly. They'll verify the invoice and let them know that payment must now be sent to them, not you.

- Receive an Advance: The factor advances you a percentage of the invoice, which is usually a bit lower, somewhere between 70-85%.

- Outsourced Collections: From this point on, the factoring company takes over. They handle all communication with your customer and chase the payment when it's due.

- Final Settlement: Once your customer pays the factoring company, they'll send you the remaining balance, minus their fees.

The specific conditions of these payments are critical and are often detailed in your payment terms.

Ultimately, a huge part of the invoice discounting vs factoring debate comes down to these distinct operational flows. It's all about how much control you want to keep and how you want to manage your customer relationships. You can learn more about optimizing this timeline by reading our guide on the cash conversion cycle.

Comparing Costs, Control, and Confidentiality

When you’re weighing up invoice discounting and factoring, the decision almost always boils down to three things: cost, control, and confidentiality. For any SME in the MENA region, getting these trade-offs right is key to unlocking cash without creating a whole new set of problems.

These factors aren’t just line items on a comparison chart; they directly impact your profit margins, the relationships you’ve built with your customers, and your company's reputation in the market. Let's break down what separates these two options in the real world.

Understanding the True Cost

The way you’re charged is one of the biggest differences. Invoice discounting tends to be much more straightforward.

- Invoice Discounting Costs: You’re usually looking at a single, clear percentage of the invoice value. It’s a clean, simple fee that makes it easy to forecast your costs and know exactly where you stand.

- Factoring Costs: The base fee here is often higher from the start. On top of that, you can expect extra administrative charges for the collections service, making the total cost harder to predict and potentially eating into your margins more than you first thought.

The key takeaway on cost is clarity. Invoice discounting offers a simple, pre-agreed fee, while factoring costs can accumulate with administrative and collection charges, potentially impacting your profitability more than anticipated.

However in Comfi's case, the cost of Invoice Discounting and B2B Buy Now, Pay Later is the same.

Retaining Control of Customer Relationships

How you talk to your customers is probably the most valuable asset you have. The invoice discounting vs factoring debate often lands right here: who gets to manage that conversation?

With invoice discounting, you keep complete ownership of your sales ledger. You manage all customer communication, stick to your own collection process, and maintain the direct relationships you’ve worked so hard to build. For businesses where trust and long-term partnerships are everything, that autonomy is non-negotiable. For a deeper look at how this works, platforms like Comfi offer a clear model of confidential invoice discounting that keeps you in the driver's seat.

Factoring, on the other hand, means handing over the reins. The factoring company takes over collections, which means they’ll be the ones calling your customers about payments. While this certainly takes administrative work off your plate, it also puts a third party right in the middle of your client relationships—a third party that may not share your service standards.

Maintaining Confidentiality and Trust

Finally, for many businesses, confidentiality isn't just a preference; it's a deal-breaker.

- Invoice Discounting is Private: The entire arrangement is completely confidential. Your customer has no idea a third party is involved, so their perception of your company’s financial stability never changes. It's business as usual for them.

- Factoring is Disclosed: This service is not confidential. The factor has to tell your customer that they’ve bought the debt and will be collecting the payment. This disclosure can sometimes be misinterpreted by clients, raising questions you’d rather not have to answer.

When you’re looking at providers, it’s also smart to consider how they manage their own risk, as this will influence both the cost and the quality of service. Many now rely on advanced credit risk management tools to make their own processes more efficient.

Choosing the Right Option for Your Industry in MENA

Deciding between invoice discounting and factoring isn’t just a numbers game. It's a strategic call that hinges on your industry, your business model, and the nature of your customer relationships here in the MENA region. The right choice can fuel your growth, while the wrong one can create friction with the very clients you’ve worked so hard to win.

For many businesses, the entire decision boils down to one word: confidentiality.

Sectors That Prioritize Confidentiality

Think about industries built on long-term trust and direct partnerships. Professional services firms, automotive distributors, and high-value electronics suppliers all fall into this category. In these fields, bringing a third party into your payment conversations can feel intrusive and might even signal financial instability to your clients.

- Professional Services: Consultants, marketing agencies, and legal firms live and die by their reputation. Invoice discounting lets them access cash discreetly, preserving the image of stability and direct client partnership that is so crucial.

- Automotive and Electronics Distribution: These sectors are all about established supply chains and dealer networks. Discounting injects the cash needed for inventory and operations without ever altering that delicate supplier-customer dynamic.

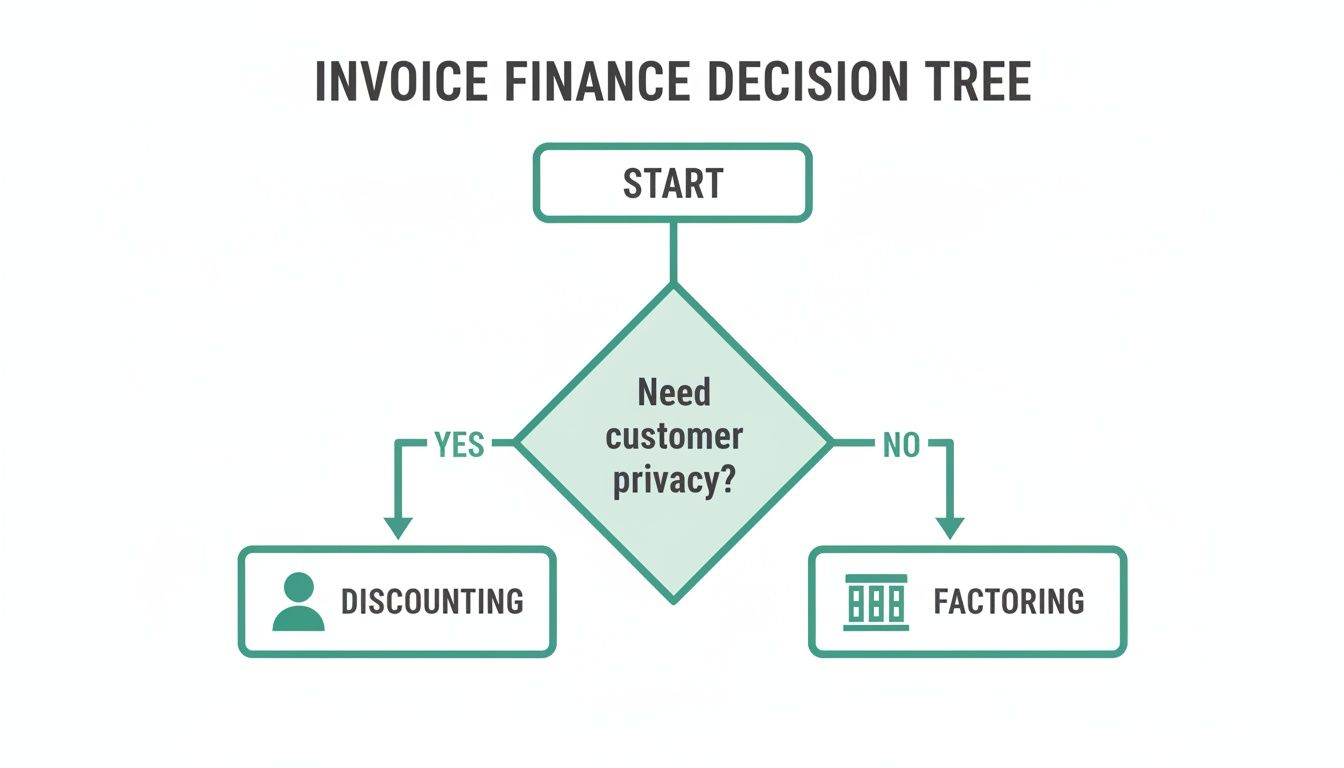

This decision tree cuts right to the chase. The first and most important question is how much you value privacy in your customer dealings.

As you can see, if keeping full control of your customer relationships is a non-negotiable for your business, then invoice discounting is the clear path forward.

When Factoring Might Be Considered

So, does factoring ever make sense? Potentially, but in very specific situations.

A company drowning in a high volume of low-value invoices, with a tiny administrative team to chase them, might see factoring as a lifeline. For them, outsourcing the entire collections process can feel like a necessary evil to reduce the internal workload, even if it comes at the cost of higher fees and losing control over customer communication.

A key advantage for modern B2B platforms is embedding invoice discounting directly into their ecosystem. This gives their sellers a seamless, integrated way to get paid instantly, offering a far more efficient and confidential alternative to clunky, old-school factoring. The integration keeps the user experience smooth while giving sellers immediate access to their cash.

How Local Laws Made Invoice Finance a Go-To for UAE Businesses

When you're weighing up invoice discounting and factoring, you can't ignore the local landscape. Here in the UAE and across the MENA region, new regulations have completely changed the game, making modern invoice discounting a secure and straightforward way for SMEs to get a handle on their cash flow. This isn't just a market trend; it's a shift driven by some very deliberate legal reforms.

The real turning point was Federal Decree-Law No. 20 of 2016. This piece of legislation was huge. It modernized the entire financial sector by creating a proper legal structure for using movable assets—like your accounts receivable—as security. This paved the way for compliant digital platforms to offer SMEs a way to access liquidity, something that was often out of reach due to old-school banking hurdles.

What This Means for SME Access to Capital

This legal groundwork has been the fuel for the rapid adoption of invoice discounting. When Federal Decree-Law No. 20 of 2016 was fully activated in December 2021, it transformed how businesses could assign their receivables. Before this, SMEs were stuck in slow approval queues. After the law came into full force, approval rates for invoice discounting shot up by an estimated 25-30%. You can dig into more of the numbers in the Middle East factoring and discounting services market report.

This regulatory backing has made a real difference on the ground by:

- Cutting Through the Red Tape: The law established the national Movables Security Register, which made the process of registering receivables much simpler and more transparent.

- Building Confidence: A clear, predictable legal framework gives both businesses and providers the security they need to operate with trust.

- Sparking Innovation: Legal clarity gave fintechs the green light to build smart, digital-first solutions designed specifically for the challenges MENA-based SMEs face.

Thanks to this supportive legal environment, invoice discounting is no longer just a niche alternative. It's now a mainstream, dependable tool for any UAE business serious about unlocking its cash flow and powering sustainable growth.

Got Questions? Here’s What MENA Business Owners Usually Ask

When you get down to the nitty-gritty of invoice discounting versus factoring, a few practical questions always come up. Getting straight answers is the final step before you choose the right way to unlock your cash flow and really start growing.

Here are the most common queries we hear from business owners across the region.

How Do I Know if My Business Qualifies?

Good news: qualifying for modern invoice discounting is less about your business history and more about the quality of your customers. These digital platforms are primarily looking at the creditworthiness of the clients you're invoicing.

So, if you’re a registered business in the MENA region and you regularly invoice reputable, reliable clients, your chances of getting approved are high. Unlike old-school bank processes, this isn't about mountains of paperwork or years of financial statements. It’s a much more accessible path for a wide range of SMEs to access liquidity.

Will My Customers Find Out I’m Using This?

Not at all. One of the biggest advantages of invoice discounting is that it’s completely confidential. The entire arrangement is a private matter between you and the provider. Your customers are never notified.

You stay in the driver's seat, managing your client relationships and chasing payments just like you always have. This is a world away from factoring, where the provider has to contact your customers directly to collect the money.

With invoice discounting, your customer interactions don't change one bit. It’s all about protecting the valuable relationships you’ve worked so hard to build.

How Fast Do I Actually Get the Money?

Speed is the name of the game here. After a quick, usually paperless setup, you can expect to receive the cash advance against your approved invoices within 24 hours.

This isn't about waiting weeks for a decision. It’s designed for immediate needs, letting you pay suppliers, cover payroll, or jump on a new opportunity without that painful 30, 60, or even 90-day wait for your customers to pay up.

What if My Customer Pays Late?

You handle it. In a standard invoice discounting agreement, you’re still responsible for collecting the payment from your customer. If an invoice goes past its due date, you’d simply follow your usual credit control process to chase it down.

The provider's agreement will spell out exactly how late payments are handled, which might involve a short extension or some additional fees. It’s really important to read and understand the recourse terms, as they clarify everyone's responsibilities if an invoice goes unpaid for a long time.

Ready to unlock your business's potential without disrupting your customer relationships? Comfi offers a fast, confidential, and digital-first platform designed for MENA SMEs. Get started with Comfi today.