What Is BNPL? Buy Now Pay Later for MENA SMEs

A healthy SME can still feel cash-poor. You win a large order, the buyer wants longer terms, your supplier wants payment sooner, and cash gets trapped between sale and settlement.

That is when many owners start asking what is BNPL, and whether it applies to business purchases, not just consumer checkouts.

Buy Now, Pay Later is best known in retail, where shoppers split the cost of a purchase into instalments. But for suppliers, wholesalers, distributors, and dealers in MENA, BNPL can be far more strategic. It lets a buyer order now while the seller gets paid upfront through a third-party platform. That shifts the question from “Can we afford to sell on terms?” to “Can we grow without tying up cash?”

For SMEs, that affects inventory planning, sales velocity, collections pressure, and available cash for payroll, restocking, and growth. It also rewards better process discipline. Teams that pair flexible payment tools with stronger invoicing and controls usually reduce avoidable friction. Even a simple review of avoiding common AP errors can help finance teams tighten the basics before adding a new payment option.

Introduction The Modern SME Cash Flow Challenge

A common SME problem is not demand. It is timing.

A wholesaler gets a strong purchase order from a retail buyer. An electronics distributor wants to move more stock before seasonality shifts. An automotive dealer sees a restocking opportunity. The revenue is there, but payment timing does not match supplier obligations and operating costs.

That is where BNPL for business matters. At its core, Buy Now, Pay Later lets a buyer receive goods or services now and pay over an agreed period. In a business setting, that means one party can keep selling without waiting for collections, while the other can buy without paying the full amount on day one.

Practical rule: If delayed payments are slowing sales or restocking, the issue usually is not demand. It is payment structure.

For MENA SMEs, this matters because many sit in the middle of the chain. They buy from importers or manufacturers, sell to retailers or commercial customers, and absorb pressure from both sides. Traditional trade credit can help, but it is often manual, relationship-driven, slow to approve, and hard to scale across many buyers.

BNPL changes that when set up well. It turns payment terms into a structured product with clearer approval logic, clearer collections ownership, and a cleaner handoff between seller and buyer. That is very different from extending open account terms and hoping the buyer pays on time.

The practical question is not whether BNPL is good or bad. It is whether the terms fit your sales cycle, margins, and buyer profile. For some SMEs, it is a useful growth lever. For others, it adds complexity if the repayment schedule does not match how inventory moves.

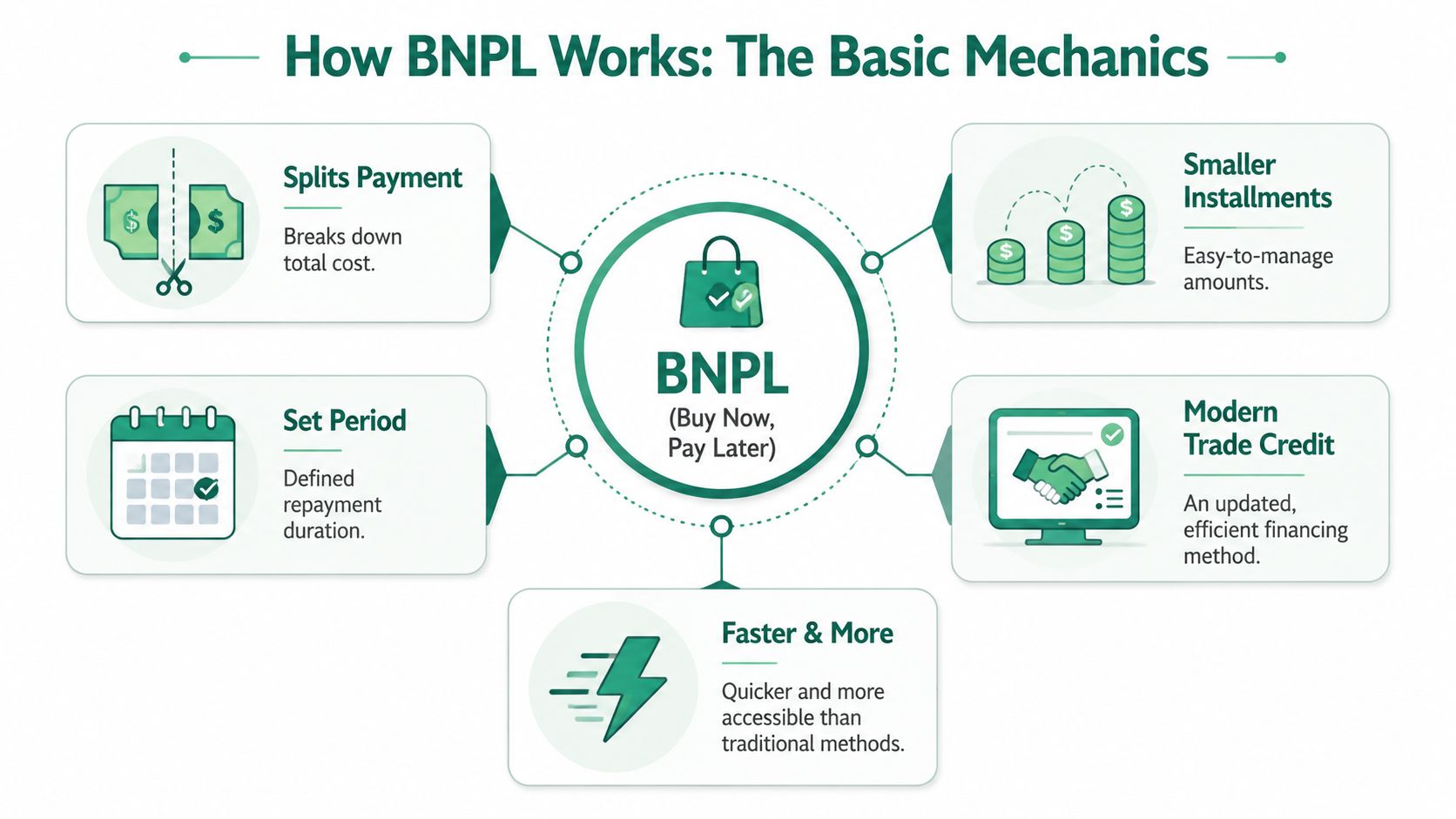

How BNPL Works The Basic Mechanics

BNPL is simple. A buyer purchases now, receives the goods or service, and repays over time in scheduled amounts instead of one immediate lump sum.

In business use, there are usually three parties involved:

- The buyer: The business that wants the goods now but prefers to pay over an agreed schedule.

- The seller: The supplier, distributor, dealer, or merchant that wants to complete the sale without waiting through a long collection cycle.

- The BNPL provider: The platform that facilitates the transaction, pays the seller based on the arrangement, and manages the buyer repayment process.

The payment flow in plain language

Think of BNPL as a faster, more structured version of trade terms.

The buyer checks out or confirms a purchase and selects deferred payment terms. The seller does not have to underwrite the buyer directly or carry the full collections burden. The BNPL platform sits in the middle and manages approval, payment flow, and repayment tracking.

That matters because it changes the seller's operating model. Instead of tying growth to how much credit the seller is willing to extend from its own balance sheet, the seller can offer payment flexibility through an external platform.

What makes the model work

The mechanics look simple, but the platform has to do several things well:

- Assess eligibility quickly so the buyer is not stuck in a slow approval loop.

- Present clear payment terms so both parties know what happens next.

- Settle with the seller smoothly so fulfilment is not delayed.

- Collect from the buyer on schedule without unnecessary friction.

Good BNPL feels simple to the customer because the complexity sits in the infrastructure, not in the checkout experience.

For SMEs, that is the practical value. Buyers get flexibility. Sellers can close orders without manually negotiating every payment exception. Finance teams also get a clearer repayment trail than they often get from ad hoc trade credit.

What does not work

BNPL stops being useful when the payment schedule ignores the operating cycle.

If a buyer needs stock that takes time to sell, very short repayment windows can create pressure instead of relief. If a seller adds BNPL without aligning invoicing, reconciliation, and fulfilment, the tool can create confusion between sales and finance. The model works best when commercial flow, payment terms, and internal controls fit together.

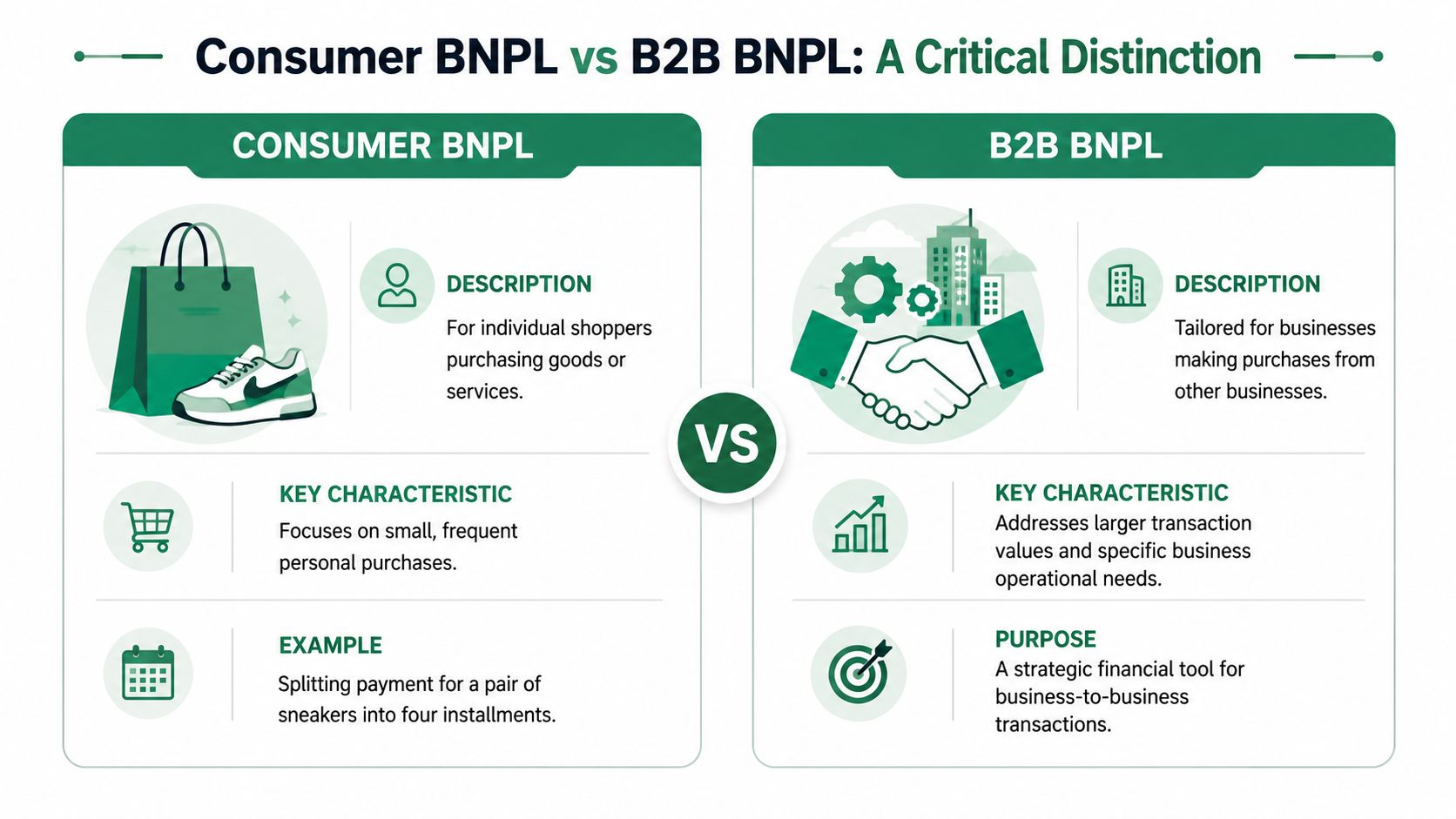

Consumer BNPL vs B2B BNPL A Critical Distinction

When people ask what BNPL is, they usually mean the consumer version. A shopper buys something online, splits payment into instalments, and completes checkout in minutes.

That is real BNPL, but it is only half the story.

For SMEs, the more important version is B2B BNPL. It supports business purchases rather than personal shopping. The use case shifts from convenience to operations. Instead of helping someone buy trainers, it helps a business buy inventory, replenish stock, source materials, or manage procurement cycles.

The difference in purpose

Consumer BNPL is usually built around personal affordability at the point of sale.

B2B BNPL is built around cash conversion timing. A business buyer is usually not trying to fund a lifestyle purchase. It is trying to align outgoing payments with future incoming revenue. That is a more operational decision.

Here is a clear breakdown:

QuestionConsumer BNPLB2B BNPLWho uses itIndividual shoppersBusinesses buying from other businessesTypical goalSplit a personal purchaseAlign payment terms with sales, inventory, or procurement cyclesContextRetail checkoutWholesale, supply chain, invoicing, stock purchasesStrategic valueConvenienceSales growth, buyer conversion, smoother purchasing

Why SMEs should care

The gap in understanding this business use case is larger than most articles admit. In the UAE, SMEs represent over 95% of businesses, and 60% face capital constraints from delayed payments. B2B BNPL platforms address that with 30/60/90-day terms, with reported outcomes including 30% sales uplift and 20% new-customer growth according to the cited source on BNPL's B2B potential in the UAE.

That matters because an SME supplier often loses deals for a simple reason. The buyer wants terms, and the seller cannot comfortably offer them. B2B BNPL can remove that deadlock.

The commercial use case is broader than most people think

This is one reason many firms are also rethinking their online sales structure. If you want context on how business purchasing journeys are evolving, these examples of powerful B2B e-commerce models are useful because they show how payment flexibility fits into digital wholesale journeys.

In practical terms, B2B BNPL can suit:

- Wholesale restocking: A retailer buys inventory now and pays over agreed terms.

- Distributor sales: A supplier closes more deals with buyers who need timing flexibility.

- Dealer purchases: A business secures stock without making the full payment upfront.

- Embedded checkout flows: A marketplace or B2B seller offers terms directly in the purchase journey.

For UAE buyers looking specifically at that model, this guide to B2B Buy Now Pay Later for buyers in the UAE gives a more direct buyer-side view.

If consumer BNPL helps an individual manage a purchase, B2B BNPL helps a business manage a cycle.

That distinction is what many SME owners miss at first. Once it is clear, the product stops looking like a retail checkout gimmick and starts looking like a sales and purchasing tool.

Benefits and Risks for SME Suppliers and Buyers

BNPL can solve a real commercial problem. It can also create a new one if teams use it carelessly.

The best way to assess it is operationally. Ask what it changes for the supplier, what it changes for the buyer, and where it could put pressure on margins, stock, or repayment discipline.

Where suppliers usually benefit

For suppliers and wholesalers, the strongest upside is usually cash timing and deal conversion.

- Faster cash receipt: The supplier does not wait through long buyer payment cycles in the same way it would under standard open account terms.

- Lower direct collections burden: The repayment process is handled through the platform arrangement rather than sitting entirely with the seller.

- Bigger order potential: Buyers who hesitate at upfront payment may place larger orders when terms are available.

- More competitive selling: Flexible terms can help a supplier win accounts that might otherwise go to a competitor willing to extend credit.

This matters most when a supplier is turning away good customers, not because demand is weak, but because payment timing is awkward.

Where buyers usually benefit

For buyers, the attraction is straightforward. They can place orders when demand is present instead of waiting until cash catches up.

That can help in several ways:

- Inventory timing: A buyer can secure stock before a selling window closes.

- Cash preservation: The business keeps more room in its operating cash position.

- Procurement continuity: Essential goods or inputs do not have to be delayed purely because of payment timing.

- Smoother purchasing cycles: Finance and procurement can work with a clearer schedule instead of repeated ad hoc extensions.

The risks are real

The biggest mistake is treating BNPL as free breathing room with no operational cost.

Watch the cycle, not the headline term. If repayment starts before the goods meaningfully convert into sales, cash strain can simply move from one part of the business to another.

For buyers, the risks usually include:

- Repayment mismatch: The payment schedule may be shorter than the inventory or receivables cycle.

- Over-ordering: Easier purchasing can tempt a team to buy more than sales velocity supports.

- Stacked obligations: Multiple deferred purchases can become hard to track if finance controls are weak.

For sellers, the risks usually include:

- Provider selection risk: A weak platform can create customer confusion, delays, or operational friction.

- Margin pressure: Merchant costs matter in lower-margin sectors.

- Poor internal rollout: If sales teams promise terms without finance alignment, disputes and reconciliation issues can increase.

A clear example from automotive

This issue becomes sharper in high-ticket sectors. In the UAE auto market, dealers often have capital tied up in inventory for up to 180 days, and 45% of SME auto dealers experienced cash-flow bottlenecks due to mismatched BNPL repayment schedules, according to the cited analysis of BNPL risks in automotive.

That does not mean BNPL is wrong for automotive. It means the repayment design has to reflect the actual turnover profile of vehicles, not a generic retail repayment rhythm.

The BNPL Landscape in the MENA Region

BNPL is no longer a fringe payment option in the region. It has become part of the wider fintech and retail infrastructure, especially in the Gulf.

The growth signals are strong. The Middle East BNPL market is projected to reach US$5.79 billion in 2025, with 28.8% CAGR from 2021 to 2024, according to Grant Thornton's review of BNPL in the UAE and regional market context. That matters for SMEs because it shows payment flexibility is becoming a normal part of how buyers expect to transact, not a niche feature.

Why the UAE stands out

The UAE has become a practical test bed for BNPL. That is partly because the market is digitally active, and partly because regulatory guardrails are becoming clearer.

Under CBUAE rules cited in the same Grant Thornton source, BNPL credit is capped at AED 20,000 or three months of verified net income, whichever is lower, and total fees are capped at 30% of the original amount. Those controls matter because they push providers toward more disciplined product design.

For SMEs, that has two effects. First, it supports trust in the category. Second, it means any provider operating seriously in the market has to think about compliance, underwriting controls, and product governance, not just sales growth.

Growth does not mean every use case is equal

The market is expanding, but SMEs still need to distinguish between consumer-led checkout adoption and business-focused use cases. If you are evaluating deferred terms for procurement or trade purchases, this explanation of deferred payment for business purchases in the UAE is a useful lens because it focuses on payment timing in a business setting rather than retail instalments.

Regional BNPL growth is a good signal. It is not, by itself, a reason to adopt a product without checking fit, fees, and repayment structure.

The more mature the market becomes, the more that distinction matters. The winners will not be the businesses that add BNPL because it sounds modern. They will be the ones that match it carefully to buyer behaviour, sales cycles, and internal controls.

Practical Steps for BNPL Implementation

Adopting BNPL does not have to mean a long systems project. For most SMEs, implementation falls into two broad paths. One is lighter and faster. The other is more embedded.

Option one is dashboard-led rollout

A web dashboard suits businesses that want to start quickly with limited technical lift.

A supplier uploads invoices or transaction details, monitors approvals, tracks payment status, and manages activity from one place. This works well for firms that still sell through account managers, direct invoicing, WhatsApp orders, or offline procurement processes.

The strength of this route is speed. The trade-off is that the payment option may feel less embedded in the customer journey than a native checkout experience.

Option two is API integration

An API route fits businesses with established digital workflows, e-commerce layers, or internal systems that need BNPL built directly into the buying journey.

That can let a marketplace, procurement flow, or B2B checkout offer deferred terms inside the purchase path itself. Done well, it reduces handoffs and keeps the buyer inside one consistent experience.

The infrastructure behind that matters. A successful BNPL stack requires an API-first, modular architecture with sub-second authorisation flows, real-time risk signalling, and dynamic routing between funding sources, as explained in Marqeta's overview of BNPL infrastructure requirements.

What to check before you launch

Use a practical checklist, not a hype checklist.

- Approval flow: Can buyers get decisions quickly enough to keep sales moving?

- Operational ownership: Does sales know what to offer, and does finance know how reconciliation works?

- Repayment fit: Do the offered terms match actual stock turn or receivables timing?

- Customer experience: Are terms clearly presented, with no confusion at checkout or invoicing?

- Control framework: Are identity, authorisation, and payment processes handled securely?

On that last point, teams revisiting payment workflows often benefit from reading Orbit AI's secure payment form insights, especially when they are thinking about authorisation clarity and payment handling in digital journeys.

If your business sells on terms, buys inventory on tight cash cycles, or needs a cleaner way to offer 30/60/90-day payment options, Comfi is one UAE-based option to explore. It supports B2B payment-term workflows for SMEs in MENA through a digital dashboard and API-led setup, helping suppliers get paid upfront while buyers pay over time.