B2B Buy Now Pay Later Buyer UAE: Essential Guide 2026

A familiar UAE SME problem looks like this. A good customer wants a larger order than usual. The margin is solid. The timing is right. But your cash is stuck in stock you already bought, invoices that haven't been paid yet, or supplier bills due this week. You don't lose the sale because demand is weak. You lose it because timing is working against you.

That's why more buyers are paying attention to B2B buy now pay later buyer UAE options. It isn't about adding complexity. It's about giving your business room to move when an order, a restock need, or a supplier opportunity comes up before your incoming cash arrives.

The Modern Growth Tool for UAE Businesses

A wholesaler in Dubai gets a chance to buy fast-moving stock at the right moment. An auto parts reseller in Sharjah needs to top up inventory before demand spikes. A distributor in Abu Dhabi wants to place a larger order, but most of this month's cash is still tied up in customer payment terms.

Those situations are common. Profitable businesses still get squeezed when money comes in later than it needs to go out.

That's where B2B buy now pay later comes in. Instead of paying the full supplier bill immediately, the buyer receives terms that spread payment over time while the supplier gets paid earlier through the provider. In plain language, it helps you say yes to stock, orders, or procurement needs without waiting for every customer invoice to clear first.

The UAE market is moving quickly in this direction. The UAE B2B BNPL market is projected to reach US$1,503.7 million in 2026, with annual growth of 37.7%, according to PayNXT360's UAE B2B BNPL market outlook. That matters because it shows this is no longer a niche payment feature. It's becoming part of how SMEs manage purchasing and free up cash tied up in operations.

Why owners pay attention to it

Most SME owners don't need another finance product to learn. They need a simpler purchasing tool.

B2B BNPL can help when you need to:

- Accept bigger orders: You don't have to turn down demand because your cash is tied up elsewhere.

- Restock sooner: You can move before shelves, warehouses, or showrooms run thin.

- Protect day-to-day cash: Payroll, rent, delivery costs, and marketing still need attention even when sales are growing.

Practical rule: If a purchase will help you generate revenue before your payment term ends, B2B BNPL may be useful. If it only delays a problem purchase, it probably won't.

For commercial teams trying to understand buyer demand patterns around flexible payment options, tools that boost fintech sales for revenue leaders can also help firms spot where this buying behaviour is already shaping pipeline conversations.

What B2B Buy Now Pay Later Really Means

Consumers typically encounter BNPL on consumer checkouts for fashion, electronics, or travel. B2B BNPL is different. It's built for business purchasing, not personal shopping.

A simple way to think about it is this. Traditional trade credit says, “Take the goods now and pay me later.” B2B BNPL says, “Take the goods now, pay later, and let a specialised provider handle the payment flow in between.”

It's modern trade terms, not retail instalments

The UAE already has a strong digital payment base behind this shift. The broader UAE BNPL market recorded a 24.5% CAGR from 2021 to 2024, and online channels accounted for 84.68% of revenue in 2024, according to this UAE BNPL market report covered by Fintech Futures. For business buyers, that matters because supplier portals, digital procurement, and online ordering are already normal in the market.

So when a supplier offers B2B BNPL at checkout or on an invoice, the experience feels familiar. The difference is what's happening behind the screen.

The three parties involved

There are three moving parts:

- The buyer chooses goods or services and takes payment terms instead of paying the full amount upfront.

- The supplier gets paid earlier through the provider instead of waiting through the full term.

- The provider manages approval, transaction handling, and collections according to the agreed structure.

That's why many business owners find it easier to understand once they stop comparing it to a bank facility. It behaves more like a payment layer attached to a real commercial transaction.

It's best viewed as a smarter way to buy from suppliers, not as a substitute for every other cash management tool.

If you're comparing different ways to smooth business cash timing, it can also help to explore revenue based funding separately, because it serves a different purpose and repayment logic than transaction-linked B2B BNPL.

Where buyers get confused

Two points usually cause confusion.

First, buyers assume this is only for struggling companies. It isn't. Healthy businesses often use deferred payment terms because timing matters even when margins are good.

Second, some buyers assume the supplier is taking on extra risk. In many B2B BNPL setups, the supplier doesn't hold that same delay and collection burden in the usual way. That's one reason suppliers are increasingly open to offering it.

How the Payment Flow Works for Buyers and Suppliers

The easiest way to understand B2B BNPL is to follow one order from start to finish.

A buyer places an order with a supplier. At checkout, through a portal, or against an invoice, the buyer selects the deferred payment option. The goods can move now, while payment is settled later according to the agreed term.

What the buyer experiences

From the buyer side, the journey is usually straightforward:

- Order placement: You choose the stock, materials, parts, or services you need.

- Payment choice: Instead of paying the full invoice immediately, you select a B2B BNPL option.

- Approval check: The provider reviews whether your business qualifies.

- Goods release: Once approved, the supplier can proceed with fulfilment.

- Repayment later: You settle according to the agreed schedule, often over 30, 60, or 90 days.

The key operational point is that you get the goods into your business cycle earlier. That can give you time to sell, install, distribute, or use them before the final payment date arrives.

What the supplier experiences

The supplier sees the same transaction differently.

They don't have to wait through the full buyer term in the usual open-account way. In the UAE, this model commonly works as a three-party workflow where the supplier is paid upfront, often within hours, while the buyer receives 30, 60, or 90-day terms. Buyer eligibility can require being a UAE-registered B2B business, operating for more than 6 months, with more than AED 100,000 in monthly revenue, as outlined on Comfi's BNPL product page.

That matters because it removes a lot of the friction that normally sits inside supplier-buyer payment negotiations.

Suppliers usually care about one thing first. “Will I get paid on time?” Buyers usually care about another. “Can I keep cash free for the rest of the business?” This structure is designed to answer both.

A plain-language example

Say you run a distribution business and need inventory today because your own customers are ordering this week. With B2B BNPL, you can secure that stock now rather than delay until your receivables arrive. The supplier can release goods without waiting for your full payment term to finish.

That doesn't mean every order should go through this route. It means the tool can be useful when the purchase directly supports sales velocity, continuity, or fulfilment.

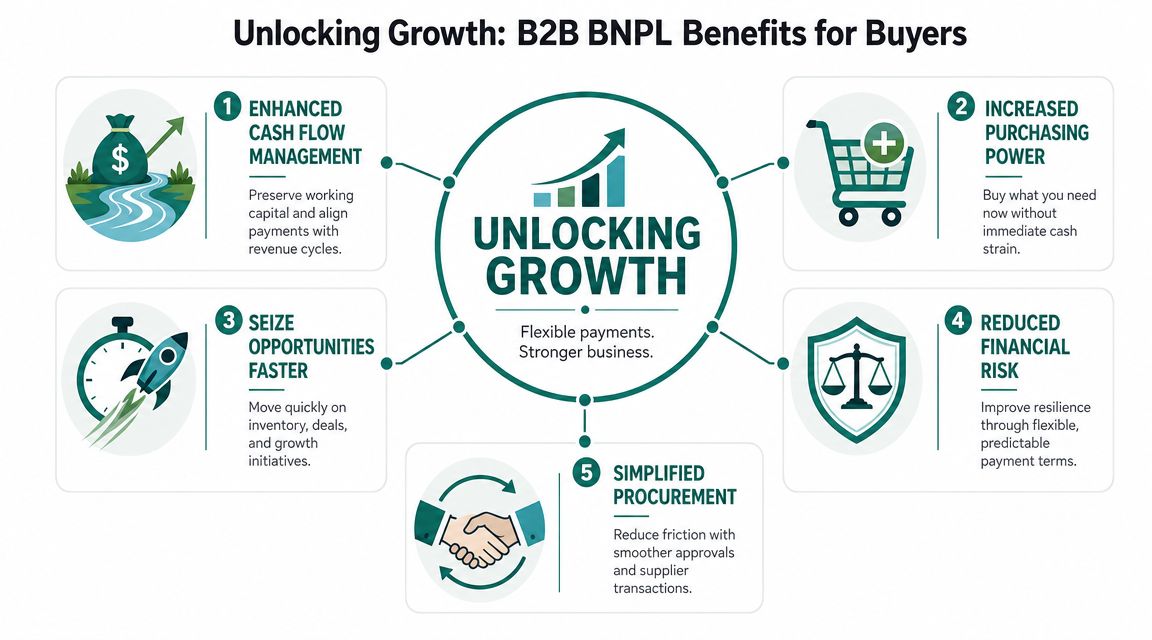

Unlocking Growth with Better Cash Flow

Cash flow is usually the primary issue, not profit on paper. A business can be busy, booked, and selling well, yet still feel stuck because payments don't line up neatly.

That's why buyers use B2B BNPL as a growth tool. The attraction isn't only delayed payment. The attraction is what delayed payment lets you do right now.

The wider environment is helping. The overall UAE BNPL market is projected to reach USD 5.02 billion in 2026, according to Mordor Intelligence's UAE BNPL market analysis. As suppliers add these payment terms into digital checkouts and invoicing systems, buyers are more likely to see BNPL offered as part of normal procurement rather than as a special exception.

Where the upside comes from

Used properly, B2B BNPL can help buyers in several practical ways:

- Preserve cash for operations: You can keep more room for salaries, transport, marketing, service delivery, or urgent supplier needs.

- Buy stock when timing matters: If a supplier has the right product available now, you may not need to wait for customer receipts before placing the order.

- Support larger purchasing decisions: Bigger baskets become easier to manage when the payment timing is spread out.

- Create more predictable planning: Fixed due dates can be easier to manage than ad hoc supplier pressure.

- Reduce strain in procurement: Buyers and suppliers spend less time arguing over terms each time an order comes up.

When it helps most

This tool tends to make the most sense when the purchase has a clear commercial purpose.

Examples include:

- Fast-moving inventory that is likely to turn before the repayment date

- Seasonal buying when demand arrives before cash collections catch up

- Expansion orders where the business needs more stock to serve new customers

- Operational continuity when not buying creates a bigger cost than using deferred terms

Buyer check: Ask one simple question before using it. “Will this purchase help my business generate cash or protect revenue before repayment is due?”

If late customer payments are already putting pressure on your business, it's also worth understanding expert AR solutions in Dubai because receivables management and smarter purchasing often need to work together.

For a practical companion to this topic, Comfi also has a guide on how to improve cash flow that helps buyers think beyond a single transaction and look at the full operating cycle.

B2B BNPL for UAE Automotive and Distribution Sectors

General BNPL explainers often stop at “flexible payments”. That's too vague for real operators. A buyer in automotive doesn't think the same way as a buyer in wholesale distribution. The stock cycle, urgency, documentation, and sales timing are different.

That's especially clear in the UAE, where sector-specific buying patterns matter.

Automotive buyers with stock sitting on the floor

Automotive is one of the clearest examples. Recent UAE-focused commentary points out that common BNPL content rarely addresses industry-specific needs, even though dealers face long inventory cycles and generic flexible-payment language doesn't really solve that operational challenge. That point is discussed in Trevex's UAE B2B BNPL overview.

A dealer may have capital tied up in vehicles, parts, or accessory stock that won't convert to cash immediately. At the same time, they may need to buy again to keep the showroom active or respond to a buyer request. In that situation, timing matters more than theory.

A practical use case looks like this:

- A dealer needs parts now: The parts can support immediate service revenue.

- Cash is locked in slower-moving inventory: Paying everything upfront creates strain.

- Deferred payment helps bridge the gap: The buyer keeps moving while stock and service activity continue.

Distributors who need speed, not more admin

Distribution has a different pain point. Orders often come in waves. One week is quiet. The next week several customers place large requests and expect fast fulfilment.

If the distributor waits for incoming payments before restocking, service levels drop. If they stretch suppliers manually, relationships weaken. B2B BNPL can sit in the middle and keep the purchasing engine moving.

This is especially useful for businesses such as electronics, FMCG, industrial supply, or specialist wholesale where basket size can change quickly and buyers need digital speed.

A few signs the model may fit your sector:

- Your inventory turns, but not evenly

- Your customers ask for larger quantities than your current cash cycle comfortably supports

- You buy through digital portals or repeat supplier relationships

- Your growth is being limited by purchase timing, not lack of demand

For distributors exploring how this works in their own channel, this guide on wholesale distributor BNPL in the UAE is a useful follow-on read.

Industry fit matters. A payment tool that helps a fast-moving distributor can be less useful for a buyer purchasing slow-turn, low-priority stock.

Choosing a Provider and Getting Started

Once a buyer sees the value, the next question is simple. Which provider fits the business?

This decision should be practical, not brand-driven. You're looking for a partner that fits your buying habits, supplier relationships, and internal processes.

What to check before signing up

Use a short checklist when comparing providers:

- Local fit: The provider should understand UAE business documentation, onboarding expectations, and supplier behaviour.

- Clear pricing: If fees, charges, or repayment terms feel hard to understand, pause and ask for written clarity.

- Term flexibility: Make sure the available structure suits your operating cycle and not just the provider's template.

- Easy use: Some businesses need a dashboard. Others need direct integration into a platform or checkout flow.

- Support quality: If an order gets delayed or a supplier needs confirmation, responsive support matters.

- Room to scale: A tool that works for today's order size should still work if your purchasing grows.

One option in the UAE market is Comfi, which offers B2B buy now pay later with 30, 60, or 90-day terms for eligible UAE businesses and a digital setup flow through its platform.

What getting started usually looks like

The onboarding path is often lighter than buyers expect. In many cases, you submit business details, complete document checks, and wait for an eligibility review. After approval, you can use the option with participating suppliers or through the provider's workflow.

Before applying, it helps to review your business credit profile and records. If you're unsure what lenders and providers may look at in the UAE context, this guide to understanding your AECB score can help you prepare.

A good provider should make the process feel organised. If the explanation is confusing before you sign, the day-to-day experience usually won't get easier after you sign.

Common Questions from B2B Buyers in the UAE

Will this hurt my business credit profile

It depends on how the provider handles reporting and how your business manages repayment. The sensible approach is to ask directly what data is reviewed, what may be reported, and what happens in a late-payment scenario. Don't assume. Get it in writing.

Are there hidden fees

There shouldn't be. A serious provider should explain charges, schedules, and any penalties before you use the service. If the pricing explanation feels vague, treat that as a warning sign.

Is my company data safe

Ask how documents are stored, who can access them, and what security controls are used inside the platform. You don't need technical jargon. You need clear answers about process, access, and protection.

Can I use it with every supplier

Not always. Some providers work through existing supplier networks or platform integrations. Others support a broader transaction workflow. Ask whether your current suppliers are already supported and what setup is needed if they aren't.

Is it only for companies under pressure

No. Many buyers use it because they want better timing, not because the business is failing. Healthy companies still need flexibility when demand moves faster than collections.

How do I know if it's right for me

Start with one purchase category. Use it where timing clearly affects sales, stock availability, or fulfilment. If it improves your buying rhythm without creating repayment stress, it may deserve a larger role in your process.

If you're exploring a practical B2B buy now pay later option in the UAE, Comfi is one provider to review. It supports eligible business buyers with 30, 60, or 90-day terms while paying suppliers upfront through a digital workflow.