Vehicle Dealer Working Capital Dubai: 2026 Growth Guide

A strong sales month can make your dealership feel weaker, not stronger. You sell through the right units, enquiries stay active, suppliers call with fresh stock, and yet your bank position looks tight because the cash from yesterday's wins is still buried inside today's operations.

That is the core of vehicle dealer working capital Dubai. The issue usually isn't lack of demand. It's timing. Cash leaves fast when you buy stock, prepare units, pay VAT, settle transport, and handle reconditioning. Cash comes back slowly, and rarely in the clean, simple pattern your supplier expects.

If your lot is full and your wallet is thin, you're not alone. You need a better operating system for capital, not just better salespeople.

The Dubai Dealer's Dilemma A Full Lot and Empty Pockets

A familiar dealership problem in Dubai goes like this. You've had a strong run on fast-moving SUVs and late-model trade-ins. A supplier offers you another batch at the right price. You know the stock will move. But your cash is trapped in units sitting on the yard, units in prep, VAT recoveries, and receivables that haven't fully converted into usable cash.

That tension has become sharper because the market itself is moving quickly. UAE passenger car sales reached 268,876 units in 2024, up 19.3% year on year, according to Comfi's review of UAE car dealer working capital pressure. The same source notes that dealers typically hold inventory for 90 to 180 days, and VAT recovery lags add more delay. In practice, a dealer can be selling steadily and still be short of deployable cash.

Why growth creates stress

When dealers grow, they usually hit three pressures at once:

- More money sits in stock: Each additional unit bought before sale increases the cash tied up on the ground.

- The wrong units stay too long: Fast movers disappear first. Slow movers remain and absorb space, attention, and capital.

- Admin lags become expensive: VAT recovery, transfer processing, and settlement timing stop being back-office annoyances and start becoming real liquidity problems.

Many dealers misread the current market situation. They assume they must reduce purchasing, decrease marketing, or cease taking selective stock positions. While that is occasionally required, it is frequently not the case. Often the primary issue is that their capital cycle has not caught up with the pace of the market.

A busy showroom doesn't guarantee a healthy cash position. In Dubai, it often hides the opposite.

What dealers often get wrong

Some owners respond by trying to “sell harder” across the whole lot. That usually creates margin damage. Others keep buying opportunistically without a stock ageing discipline. That creates a yard full of average stock instead of a pipeline of profitable stock.

Operational details matter more than many dealers admit. Clean presentation, fast prep, and disciplined merchandising all help units move sooner. Even simple showroom standards influence buyer confidence, which is why practical resources like WipesBlog.com's dealership hygiene tips are worth reviewing if your walk-ins feel softer than they should.

The better way to look at this problem is simple. You don't have a sales problem. You have a conversion-speed problem. The dealership is creating value, but your cash is arriving too late to support your next purchase cycle.

Diagnosing Your Dealership's Capital Health

Most dealers say, “I need more cash.” That's too vague to fix. You need to identify exactly where the cash slows down inside your dealership.

Start with your own operating flow. Cash goes out when you buy a vehicle. It stays out while the vehicle is transported, inspected, prepared, listed, negotiated, and sold. It may stay out longer if you're waiting on settlement, trade-in completion, or internal paperwork. Until that full loop closes, your business hasn't effectively recovered the capital.

Check the three pressure points

Look at your dealership through these lenses:

- Acquisition discipline

In UAE motor dealerships, vehicle acquisition cost is the largest expense. Dealers that get dragged into bidding wars can pay 10 to 15% above market benchmarks, while top performers using strict bid caps and targeting 45 to 60 day sales cycles report 20 to 25% higher gross margins, according to Easy Cars UAE's analysis of dealership profitability factors. - Preparation speed

A car that's bought but not retail-ready is dead capital. If trade-ins sit waiting for mechanical approval, paintwork, photography, or listing copy, your lot may look stocked while your cash remains frozen. - Collection quality

If you sell units quickly but the money lands slowly because of documentation gaps or delayed settlements, your reported sales pace won't match your actual liquidity.

Use a working worksheet, not instinct

Review the following every week:

- Ageing by stock category: Separate fresh arrivals, retail-ready units, and stale units.

- Gross margin by source: Auction, direct purchase, trade-in, fleet release, and wholesale.

- Prep delay log: Track why each unit isn't sale-ready.

- Settlement exceptions: List any deal where paperwork, customer transfer, or payment clearance is incomplete.

For private transactions and trade-ins, document quality matters more than many teams realise. If your staff handles off-system purchases or direct consumer buys, a clean paper trail helps prevent payment and handover disputes. A practical reference is receipt templates for private vehicle sales, which can help standardise basic sale documentation.

Practical rule: If a unit can't be priced, photographed, and listed quickly, don't count it as usable inventory. Count it as trapped cash.

Don't ignore your credit profile

When dealers look for external capital support, they often focus only on turnover and stock value. But funders also look at repayment behaviour, banking conduct, and credit profile. If you haven't reviewed your business credit standing recently, it's worth understanding how AECB scores affect SME funding decisions.

The point of diagnosis isn't to create a finance report that looks professional. It's to answer blunt questions. Which cars tie up your money the longest? Which buying channel gives you the best spread? Where does paperwork delay a completed sale? Once you can answer those clearly, your working capital problem becomes manageable.

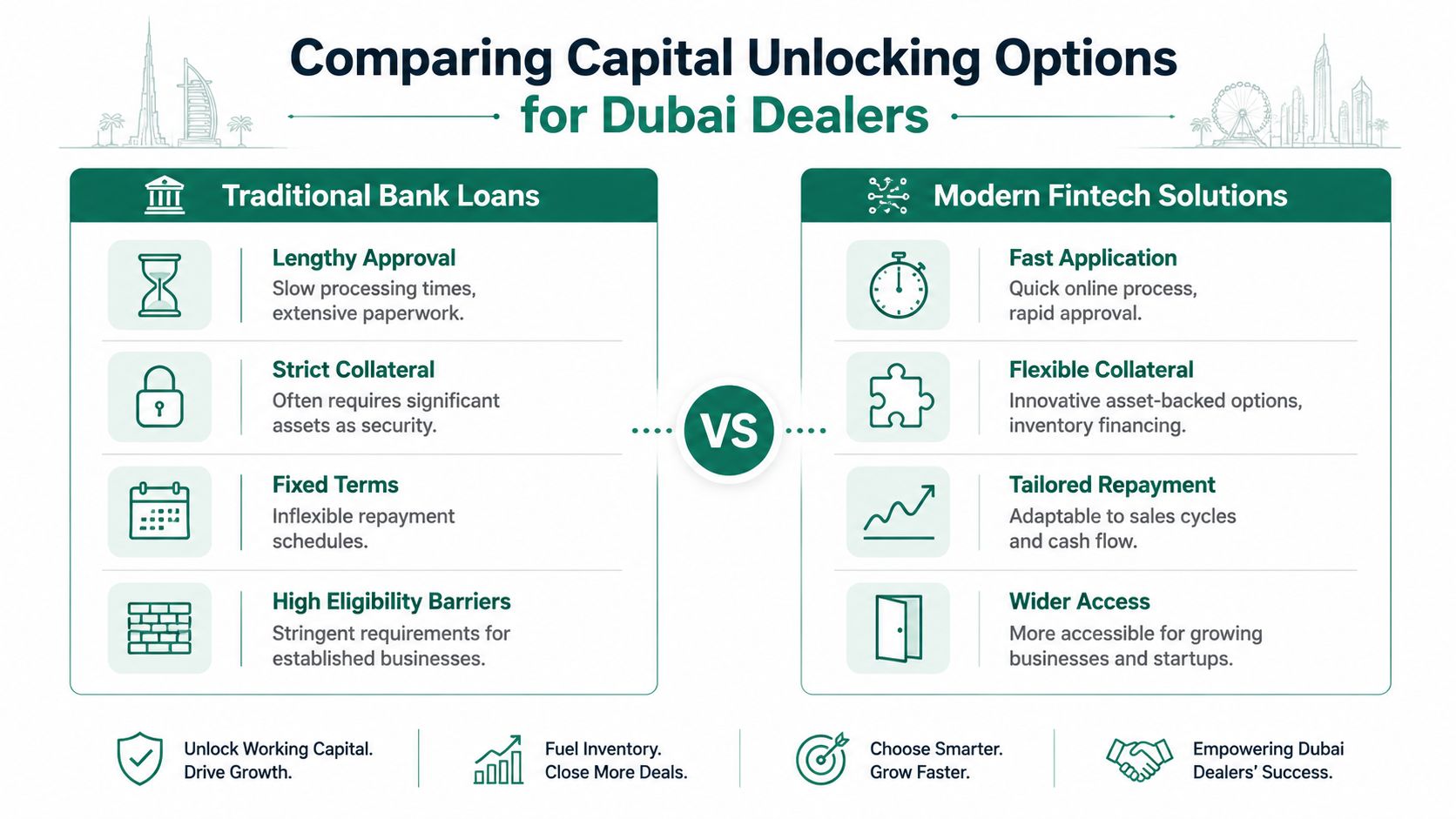

Comparing Your Capital Unlocking Options

Once you know where cash gets stuck, you can match the right solution to the right blockage. Dealers often make a mistake here. They look for one big facility to solve every issue. In practice, different capital tools suit different parts of the dealership.

The timing matters even more in used cars. The UAE used car market is projected to be worth USD 22.92 billion in 2026 and grow at a 11.52% CAGR, with the USD 8,000 to 16,000 segment accounting for 49.92% of market volume, according to Mordor Intelligence's UAE used car market outlook. Faster-turning used stock creates opportunity, but only if your capital can keep pace with supply.

What each option is actually for

Traditional bank term facilities

These can work for established dealerships with strong financials and time to complete a long approval process. They suit bigger structural needs such as expansion, fit-out, or refinancing broader obligations.

What they don't do well is help you react quickly to stock opportunities. If your supplier wants a fast answer on a late-model batch, a slow approval cycle can make the facility irrelevant.

Inventory-backed dealer solutions

These solutions address a common challenge for dealerships. You already own inventory, and while that stock holds value, your cash remains tied up in unsold vehicles. Some providers allow you to access capital against eligible in-stock units, enabling you to purchase new inventory without waiting for a retail sell-through.

This works best when your stock selection is sound and your sales operation is disciplined. It works badly if you use it to carry poor inventory decisions for longer.

Invoice discounting

If your dealership also runs a service centre, body shop, fleet account, or parts operation, unpaid invoices can create a second cash trap. In that case, invoice discounting for B2B receivables may be more relevant than an inventory-linked product.

This is often overlooked by dealers who focus only on the forecourt. However, workshop and fleet receivables can consume a large share of working capital.

Buyer payment term solutions

Some dealerships and parts businesses support trade buyers, garages, or fleet clients who want extra payment time. Structured deferred-payment tools can help you complete those sales while protecting your own cash timing. Used properly, they support volume without forcing your dealership to become the bank.

A simple choice framework

Use this practical filter:

- If your problem is stock on hand: Look at inventory-linked capital solutions.

- If your problem is unpaid B2B invoices: Look at receivables tools.

- If your problem is a big long-term balance sheet need: Talk to banks.

- If your problem is customer payment timing in trade sales: Look at structured payment-term tools.

One market option in Dubai is Comfi's Automotive Dealer Financing, which is designed to access cash from eligible in-stock vehicles so dealers can restock faster. That's not the right tool for every dealership, but it fits dealers whose main issue is capital tied up in current inventory rather than a lack of demand.

What works and what doesn't

What works:

- Matching the product to the bottleneck

- Using available capital for fast-turning stock only

- Keeping drawdowns linked to real purchase plans

What doesn't work:

- Using short-cycle capital to cover weak buying discipline

- Funding stale units instead of exiting them

- Treating every liquidity issue as a stock issue when receivables may be the actual drag

Your Application Playbook A Practical Checklist

Most dealers delay action because they assume the process will be painful. It doesn't have to be, but speed depends on how organised your records are before you apply.

The strongest applications are usually not the biggest dealerships. They are the cleanest. The documents line up, the stock list is current, and the bank activity tells a clear story.

Prepare these first

Before you approach any capital provider, get the following in order:

- Trade licence and company documents: Make sure the legal entity details match your banking and operating records.

- Owner or authorised signatory ID: Keep Emirates ID and signing authority documents ready.

- Recent bank statements: Clean statements help explain your cash behaviour faster than a verbal summary ever will.

- Inventory list or invoice sample: If the solution is tied to stock or receivables, your supporting data must be current, readable, and consistent.

- Basic management reporting: Even a simple monthly trading snapshot helps if it shows stock movement, gross margin, and outstanding obligations clearly.

Present your dealership properly

Don't flood the provider with messy exports and screenshots. Package the file like a serious operator.

A good submission usually includes:

- A current stock file with registration or chassis reference, purchase date, purchase cost, expected sale value, and current status

- A short explanation of your business model, such as retail used cars, mixed new and used, fleet-focused, or service-heavy

- A note on your biggest need, whether that is restocking speed, supplier settlement timing, or receivable pressure

Lenders and capital platforms don't reject confusion. They price it, delay it, or avoid it.

Remove friction before it appears

A few practical habits make a big difference:

- Update stock statuses daily: If sold units still appear as available, your file loses credibility.

- Reconcile bank inflows to sales records: Unexplained movements create unnecessary questions.

- Separate personal and business spending: It sounds obvious, but mixed usage slows reviews and weakens trust.

- Explain anomalies early: If you had a difficult quarter, a temporary dip, or a one-off payment issue, address it directly.

This part matters because application speed is operational, not magical. Dealers who maintain disciplined records usually move faster because they make it easy for a provider to understand the business.

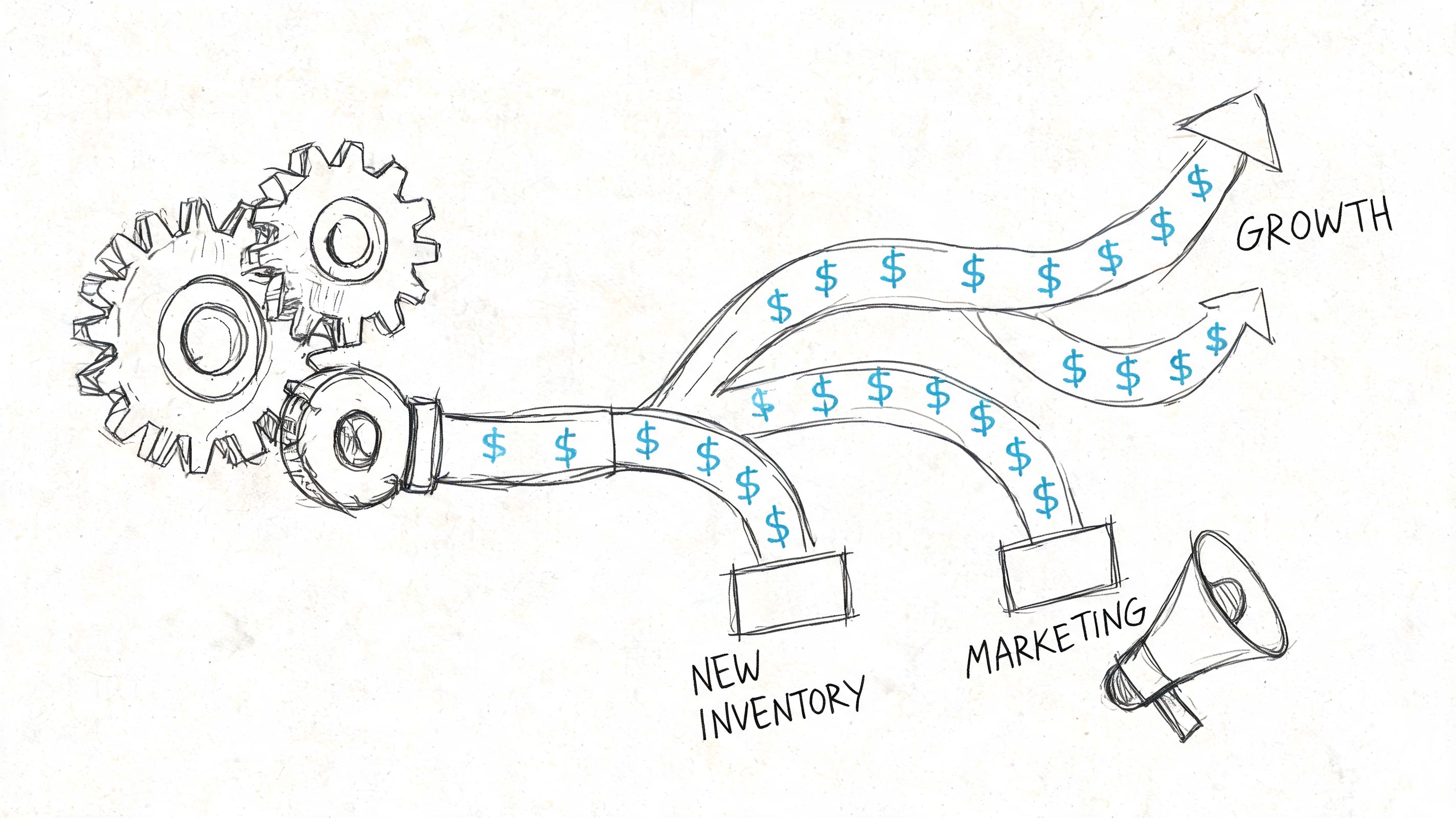

Putting Capital to Work How to Integrate and Grow

Accessing capital is only useful if you deploy it better the second time. Too many dealers solve the immediate cash squeeze, then pour the money back into the same undisciplined buying pattern that caused the squeeze in the first place.

The strongest operators treat fresh liquidity as a routing decision. Every dirham gets assigned to the highest-velocity use.

Put new cash into movement, not comfort

A useful lesson comes from outside the forecourt. Dubai commercial vehicle fleets have achieved 73% higher utilisation rates through dynamic pricing and micro-rentals, and the same source notes that access to instant funding can enable restocking with an 85% approval rate, cut sales cycles from 180 to 60 days, and drive up to 30% sales uplift, according to this case-based review of Dubai commercial fleet operations. The exact tactics differ for dealerships, but the operating lesson is the same. Capital should accelerate turnover.

Four ways to use unlocked capital well

- Buy proven stock, not tempting stock: Put money into the models, trims, and price bands you already know how to move.

- Negotiate with suppliers from strength: Faster settlement often improves your position in allocation discussions, especially when desirable units are scarce.

- Shorten the prep queue: If detailing, mechanical work, tyres, or cosmetic fixes are delaying listings, use capital to remove that bottleneck first.

- Support demand generation selectively: Better stock only helps if the right buyers see it. Use part of the liquidity to keep high-intent marketing active around fast-moving categories.

Build capital into operations

Many dealers separate themselves from competitors in this manner. They do not treat capital support as an occasional rescue. Instead, they integrate it into their buying calendar, reconditioning flow, and pricing decisions.

For a practical regional example of this approach in action, review how Instacar and Comfi are supporting UAE car dealers. The useful takeaway isn't the provider name. It's the operating model. Capital works best when it is tied directly to stock rotation and replenishment.

If fresh capital only helps you breathe, you used it defensively. If it helps you buy, prep, and retail faster, you used it properly.

Measuring Success KPIs That Matter for Your Dealership

Revenue is the last thing to improve, not the first thing to watch. If you want to know whether your vehicle dealer working capital Dubai strategy is working, track the operational metrics that move before the sales headline does.

A better-capitalised dealership should feel different week by week. Your ageing profile should tighten. Your stock mix should improve. Your strongest salespeople should stop apologising for not having the right units available.

The KPI set that actually matters

Focus on these indicators.

- Inventory days by category: Break this down by brand, model type, price band, and source. A blended average hides poor decisions.

- Retail-ready time: Measure how long a unit spends between acquisition and live listing.

- Gross margin per unit: Watch whether improved buying discipline is protecting your spread.

- Stock ageing concentration: Identify how much capital sits in your oldest units.

- Repeat restocking speed: Measure how quickly money from sold stock becomes available for the next purchase.

- Lead-to-sale match rate: If buyers ask for cars you don't have, your capital plan and inventory plan are out of sync.

Use cohort reviews, not just monthly totals

Monthly reporting is too blunt on its own. Group vehicles by purchase month or source, then compare how each cohort performs. That shows whether the problem sits with auction buying, direct sourcing, trade-ins, or specific sales managers.

A practical review rhythm looks like this:

- Weekly stock meeting

Remove excuses. Which units are blocked and why? - Fortnightly buying review

Compare purchase decisions against current market response. - Monthly capital review Check whether released liquidity went into fast-moving categories or drifted into low-conviction stock.

What a good outcome looks like

A well-run dealership doesn't just carry more inventory. It carries better inventory. The lot becomes more intentional. Slow units are identified earlier. Prep delays become visible. Purchasing shifts away from ego buys and towards repeatable margin.

Here's the practical pattern I see when dealers improve this area:

- They stop judging performance by lot size alone.

- They separate “owned stock” from “productive stock”.

- They become harder buyers and faster retailers.

- They use capital to remove friction, not to postpone decisions.

That is the actual return on working capital improvement. You do not just ease pressure. You improve the quality of the whole business.

If your dealership has solid demand but too much cash tied up in stock, Comfi's dealer financing is worth evaluating as one of the options available in the UAE. It helps dealers access capital from eligible in-stock vehicles and can fit alongside a disciplined plan for stock rotation, supplier payments, and faster reinvestment.

Related Reading

- How Can MENA SMEs Master Working Capital?

- Inventory Financing vs Invoice Discounting for UAE SMEs

- Mastering Auto Dealer Cash Flow in the UAE: A Practical Guide

Looking to improve your cash flow? Explore Comfi's Dealer Financing solutions. Get started today.