Risk Assessment Methods: A Guide for MENA SMEs

A customer offers you a large order. On paper, it looks like the kind of deal that could move your business up a level. In practice, it might stretch stock, pressure receivables, tie up cash, and expose you to a buyer or supplier you haven't fully tested.

That's where many SME owners in Dubai get stuck. They don't lack ambition. They lack a clear way to judge whether the opportunity is worth the operational and financial strain.

Risk assessment methods solve that problem. Not by telling you to avoid growth, but by helping you decide which risks you can accept, which ones you should reduce, and which ones could subtly damage cash flow if left unchecked.

A good risk process is a better decision process. It helps you ask sharper questions before you commit inventory, extend payment terms, onboard a supplier, or back a dealer stock position. If you run a lean business without a dedicated risk team, that matters even more.

Why Risk Assessment Is Your Growth Co-Pilot

A wholesaler in the UAE gets a chance to supply a regional retail chain. The upside is obvious. Bigger order volume, stronger visibility, and a route into new accounts. The downside is less visible at first glance. The buyer wants longer payment terms, the supplier needs an upfront commitment, and one delayed shipment could lock up cash for weeks.

Many owners treat risk assessment like a compliance exercise. That's a mistake. In a growing SME, risk assessment is closer to a co-pilot. It doesn't drive the business, but it helps you avoid flying blind.

When you assess risk properly, you stop asking only, “Can we do this?” You start asking better questions.

- Cash flow pressure: If this deal lands, what gets tighter first. Inventory, payroll, supplier payments, or receivables?

- Concentration exposure: Are you becoming too dependent on one customer, one supplier, or one sales channel?

- Execution strain: Can your team fulfil the order without service levels slipping elsewhere?

- Recovery options: If something goes wrong, how quickly can you contain the damage?

Practical rule: Growth decisions are rarely yes-or-no decisions. They're usually structure decisions. The question is how to take the opportunity with the right safeguards.

This is especially relevant in MENA markets where many SMEs operate with thin buffers and fast-moving trade cycles. A delayed invoice, a quality issue at customs, or slower inventory turnover can affect more than one line on the P&L. It can change the timing of everything.

Risk assessment methods help you replace instinct-only decisions with structured judgment. That doesn't make decisions slower. Usually, it makes them clearer. You see the pressure points earlier, so you can negotiate terms, change suppliers, stage inventory purchases, or tighten controls before the problem becomes expensive.

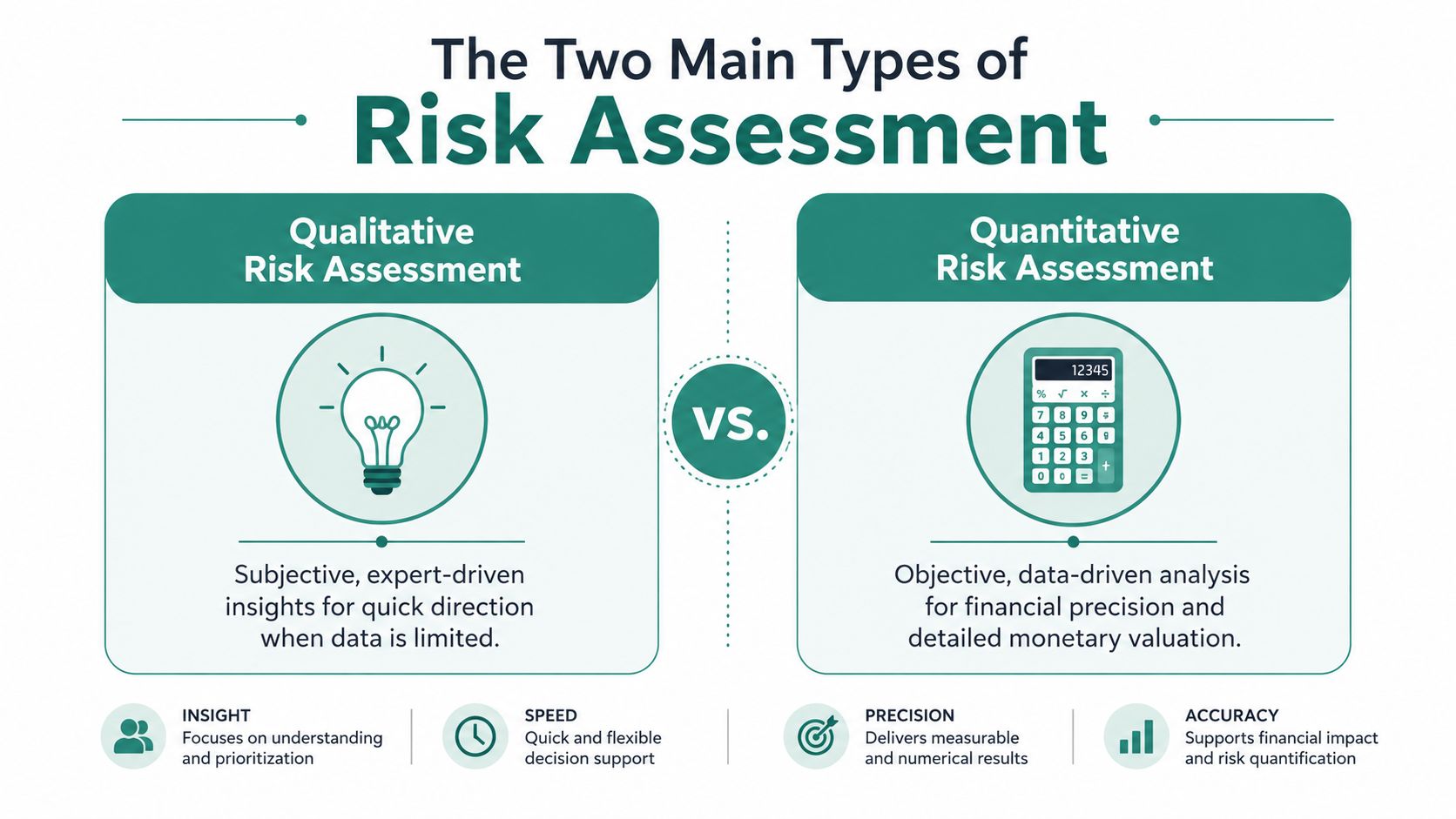

The Two Main Types of Risk Assessment

Think of risk assessment like navigating a city you don't know well.

A qualitative approach is like using local knowledge, landmarks, and a rough map. You know which areas are busy, which roads are risky at certain times, and where delays usually happen. It's fast and useful, especially when hard data is limited.

A quantitative approach is like using GPS with route timing, traffic density, and estimated arrival times. It gives you more precision. You can compare options using numbers, not just judgment.

Qualitative means structured judgment

Qualitative risk assessment methods rely on expert input, team experience, and practical scoring tools such as risk matrices. They help when you need direction quickly or when the business doesn't yet have deep historical data.

A finance manager might say a supplier disruption risk is “high likelihood, medium impact”. That isn't random opinion if the team uses consistent criteria. It's structured judgment.

Quantitative means numerical analysis

Quantitative risk assessment methods use measurable data, probability estimates, and financial models. ISACA notes that risk assessment methodology is formally structured into qualitative, semi-quantitative, and quantitative branches, with qualitative methods using rating scales and risk matrices, and quantitative workflows including tools such as Monte Carlo analysis. That formal structure lets businesses combine expert judgment with statistical data for stronger decisions, as outlined in ISACA's guidance on risk assessment and analysis methods.

For an SME, this often means turning a vague concern into a financial question. Instead of saying, “Late payment is a risk,” you ask, “What's the likely annual cost of late payment exposure, and is the control worth the spend?”

Most SMEs need both

You don't need to choose one forever. In practice, many of the best decisions use both.

- Use qualitative methods when speed matters, data is patchy, or the decision is operational.

- Use quantitative methods when the financial impact is material and you need a defensible business case.

- Use semi-quantitative methods when you want simple scoring that sits between the two.

If you're reviewing buyer exposure, supplier reliability, or collections risk, a structured framework like this becomes more useful when paired with a focused view of payment risk in B2B trade.

The point isn't mathematical perfection. The point is choosing a method that helps you make a better decision with the information you actually have.

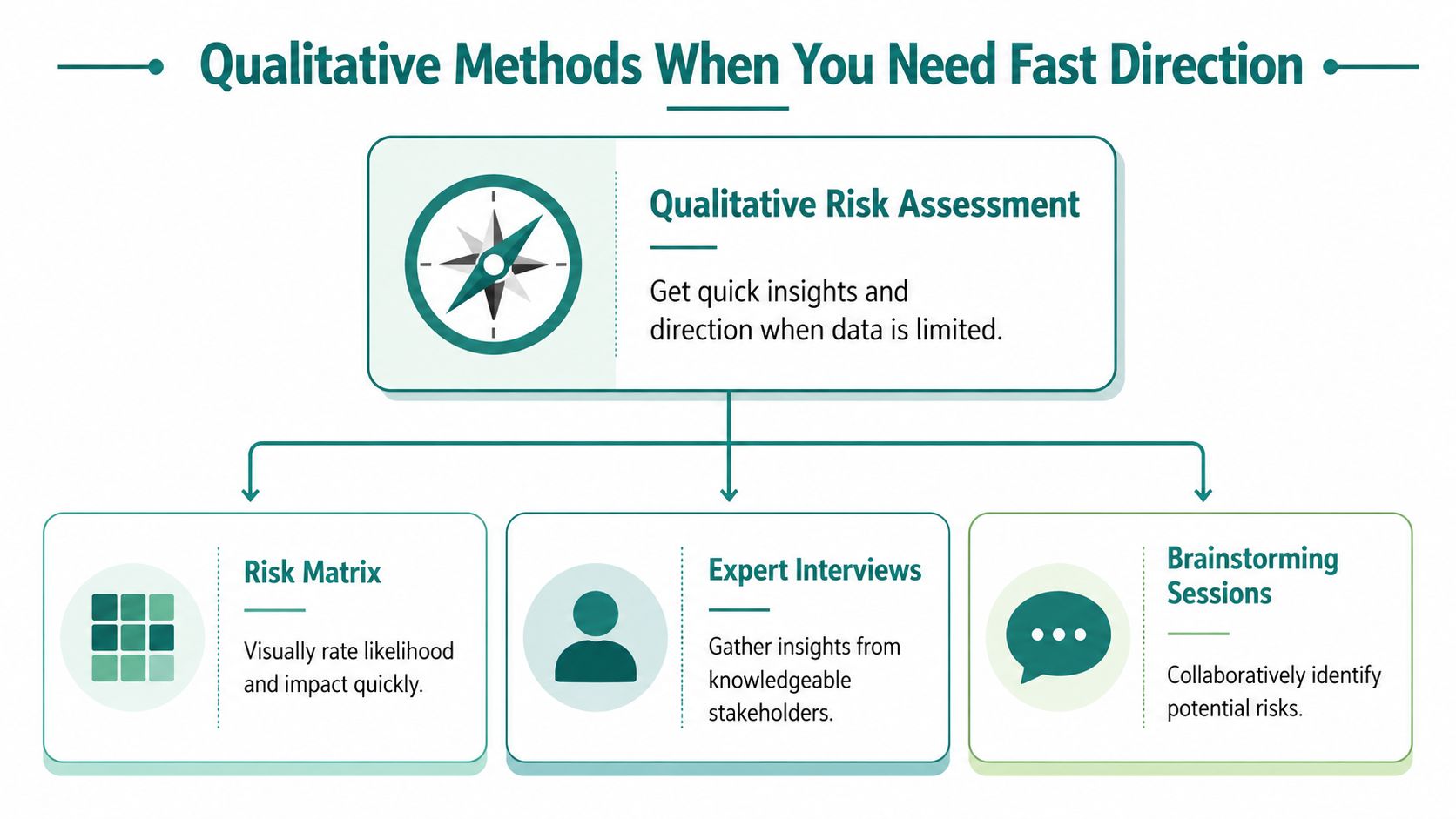

Qualitative Methods When You Need Fast Direction

When data is thin, decisions can't wait. That's where qualitative risk assessment methods earn their keep.

They give you a disciplined way to use experience, local market knowledge, and frontline judgment without pretending you have more precision than you do. For many SMEs, that's the right starting point.

The risk matrix

The most practical qualitative tool is the risk matrix. It ranks a risk on two axes:

- Probability: Low, Medium, High

- Impact: Minor, Moderate, Severe

That simple grid helps a team sort noise from priority.

Take a Dubai-based SME considering a new overseas supplier. The pricing is attractive, but the supplier is untested. The finance manager and operations lead sit down and list the main risks.

- Shipment delay: Likelihood could be medium or high if lead times are uncertain.

- Quality inconsistency: Impact could be severe if defective stock can't be sold quickly.

- Documentation errors: Impact might be moderate, but customs delays can create cash flow knock-on effects.

- Currency mismatch: Probability may depend on contract terms and payment timing.

- Single-supplier dependency: A strategic risk if there's no backup source.

Once the team plots those risks, the conversation changes. Instead of saying, “This feels risky,” they can say, “Two risks sit in the high-impact zone, so we won't proceed unless contract protections and inspection steps are in place.”

Other useful qualitative tools

A matrix is the workhorse, but it isn't the only option.

- Expert interviews: Speak to people who've seen similar transactions fail or succeed. Procurement, logistics, finance, and sales often notice different weak spots.

- Brainstorming sessions: Useful when the team is entering a new market or product line and wants a wider scan of possible failure points.

- Scenario discussion: Ask what happens if the customer pays late, the shipment slips, or a key approval doesn't come through.

A good qualitative review doesn't need perfect data. It needs clear criteria, the right people in the room, and a record of why a decision was made.

Where readers often get confused

Some owners think qualitative means vague. It doesn't. A weak qualitative process is vague. A strong one is documented and repeatable.

Use short scoring definitions so everyone means the same thing. “High impact” should mean something specific to your business, such as stock being stranded, customer penalties, or a serious collections issue. If each manager defines risk differently, the matrix becomes theatre.

Qualitative methods are best when you need fast direction. They help you screen decisions, prioritise attention, and spot where a deeper numerical review is worth doing.

Quantitative Methods For Financial Precision

At some point, judgment isn't enough. A large inventory commitment, a major customer exposure, or a control investment needs a number attached to it. That's where quantitative risk assessment methods become useful.

They translate uncertainty into the language finance teams use every day. Cash impact, expected loss, recovery cost, and return on a control.

Start with Annual Loss Expectancy

One of the most practical tools is Annual Loss Expectancy, often shortened to ALE.

The basic idea is simple:

ALE = Single Loss Expectancy × Annualised Rate of Occurrence

In plain English, you estimate two things:

- Single Loss Expectancy: What one incident is likely to cost you

- Annualised Rate of Occurrence: How often that incident is likely to happen in a year

Wolters Kluwer describes ALE as a practical benchmark for estimating annualised financial exposure. It also notes that stronger models should include Return on Security Investment (ROSI) so teams can compare the cost of a control against the loss it could prevent, as explained in this overview of common GRC risk methodologies.

A dealer financing example

Take an automotive dealer holding stock that may age longer than planned. The core risk isn't just that a vehicle sells late. Instead, the key problem is the financial effect of extended holding time, margin pressure, storage cost, and delayed cash conversion.

A quantitative review might ask:

- What's the loss if one vehicle remains unsold beyond the planned sales window?

- How often does that happen across the portfolio?

- What carrying costs rise when ageing inventory builds up?

- Would a control, such as tighter stock selection or earlier discounting, reduce the expected annual loss enough to justify the operational effort?

That gives the finance team a clearer basis for action. Instead of debating opinions, they compare expected exposure against the cost of changing the process.

Don't fake precision

Many SMEs slip by using decimal-heavy spreadsheets that look rigorous but rest on weak assumptions.

If your probability inputs are uncertain, say so. If loss ranges are wide, model a sensible range rather than forcing a single neat answer. Teams that want to improve this part of the process often benefit from understanding how probability assumptions are shaped. A practical primer on understanding the distribution fitting workflow can help if you're moving from rough estimates toward more defensible modelling.

Quantitative analysis is useful when it sharpens a decision. It becomes a distraction when the model looks more certain than the business reality.

For SME owners, the value of quantitative risk assessment methods is straightforward. They help answer whether a risk is financially acceptable, whether a control is worth paying for, and which exposure deserves attention first.

Choosing the Right Method for Your SME

The best risk assessment method isn't the most advanced one. It's the one that fits the decision in front of you.

A small software subscription decision doesn't need a dense model. A large stock purchase tied to uncertain customer demand probably does. Problems start when businesses use the same blunt scoring method for every decision, regardless of the cash impact.

Four filters that make the choice easier

Use these questions before you choose your method.

- Decision size: If the downside could materially disrupt cash flow, move beyond a quick qualitative score.

- Data quality: If you have usable payment history, defaults, stock ageing records, or supplier performance data, quantitative analysis becomes more worthwhile.

- Time pressure: If the decision must be made quickly, a qualitative screen may be the practical first pass.

- Cost of analysis: Don't build a complex model for a low-stakes decision.

A hybrid method often works best. Start with a qualitative screen to identify the main issues. Then apply quantitative analysis only to the highest-impact exposures.

Why generic scores often fail

This is especially important for MENA businesses with several warehouses, branch locations, delivery routes, supplier origins, or asset types. A generic score can hide localised exposure.

PreventionWeb highlights a commonly missed point in risk assessment methods. Many estimates rely on simplified proxy data, which can materially misstate exposure. It argues for moving toward asset-level, location-specific analysis where the decision requires that level of detail, and notes that the most effective method is the one that matches the needed granularity, not necessarily the most complex one, as discussed in this piece on gaps in climate risk assessment methods.

That principle extends well beyond climate risk. If you have one branch with strong receivables quality and another with recurring payment delays, a single company-wide score may be too blunt to guide action.

A portfolio can look healthy in aggregate while one location, customer cluster, or stock category creates most of the downside.

A simple decision rule

Choose qualitative when you need speed and direction. Choose quantitative when the decision affects money in a meaningful way. Choose hybrid when the business has enough data to measure some risks, but not all of them.

If your team is building a broader framework around operational and financial exposure, a useful next step is developing a sharper internal language for business risk and how it shows up in day-to-day decisions.

A Practical 5-Step Risk Management Process

The most useful risk assessment methods are the ones your team will consistently repeat. A simple process beats an impressive document nobody updates.

Consider an electronics wholesaler deciding whether to offer invoice discounting terms to a new large customer. The customer could lead to bigger volume, but the receivable could also become a major concentration risk if payment slows.

Step 1 Identify

List actual risks, not just the obvious one.

For this wholesaler, the first risk is customer non-payment or delayed payment. But there are others. Disputed invoices, over-reliance on one buyer, margin compression from delayed cash collection, and internal process errors that slow reconciliation.

Historical-data-based modelling changed modern risk assessment by shifting the discipline from pure judgment toward probabilistic forecasting. One example is the Early Warning Project's statistical model, which trains on historical episodes from 1960 to 2015 and uses current-country data to generate a two-year-ahead estimated risk. That methodology shows how historical evidence became the foundation of predictive risk assessment, as explained in the Early Warning Project's statistical model methodology.

For an SME, the lesson is practical. Use your own history where possible. Past payment delays, past disputes, past customer behaviour. Your records are not just archives. They're inputs.

Step 2 Analyse

Now decide how to assess each risk.

A quick screen might use a qualitative matrix. If this customer is strategically important and the receivable could be large, the finance team may also run a quantitative view of expected loss, payment timing, and concentration impact.

Look at the nature of the exposure, not just its headline amount.

- Counterparty risk: How reliable is the buyer based on available payment behaviour and references?

- Operational risk: Could billing or documentation mistakes delay collection?

- Liquidity risk: What happens to cash flow if payment slips materially?

- Concentration risk: How exposed are you if this one account becomes dominant?

Step 3 Evaluate

This is the decision point. Is the risk acceptable as-is, acceptable with controls, or unacceptable?

A useful discipline is to define your acceptance criteria before the deal gets emotional. If one delayed invoice would force you to postpone supplier payments, the tolerance may already be too tight.

Teams that want another practical reference can compare their own workflow with this guide to the risk management process in the UK. The terminology may vary by market, but the core logic is familiar and useful.

If you can't explain why a risk is acceptable in one short paragraph, you probably haven't evaluated it clearly enough.

Step 4 Treat

Treatment means choosing a response.

You may reduce the risk by limiting exposure, tightening invoice controls, shortening terms, requiring staged delivery, diversifying the customer mix, or transferring part of the risk through a third-party structure. The key is matching the treatment to the specific risk source.

Not every risk should be eliminated. Some should be priced, capped, or monitored more closely.

Step 5 Monitor and review

Risk assessment isn't a one-off exercise. Conditions change. Payment patterns change. Customer quality changes. Internal controls improve, then drift.

For the electronics wholesaler, monitoring could include payment timeliness, invoice dispute frequency, collections trends, and customer concentration over time. If the risk profile worsens, the original decision needs to be revisited.

If your team is building this into a repeatable receivables workflow, it helps to align the process with a practical view of credit risk management for growing businesses.

Turn Risk into Your Competitive Advantage

Most SME owners don't need more theory. They need a way to make sharper calls when cash, timing, and growth pull in different directions.

That's why risk assessment methods matter. Qualitative methods help when you need fast direction. Quantitative methods help when you need financial precision. A hybrid approach usually gives the best balance for real businesses operating in fast-moving markets.

The primary advantage isn't that risk disappears. It doesn't. The advantage is that you start seeing risk early enough to shape it. You negotiate better terms. You avoid weak exposures. You commit capital with more confidence. You protect liquidity while still pursuing growth.

That changes the role of risk in your business. It stops being a brake and becomes a filter for better opportunities.

The SME owner facing that large order at the start of this article doesn't need to say no just because the deal looks complicated. With the right method, they can test the pressure points, understand the downside, and move forward with a clear plan.

That's how resilient businesses grow in competitive MENA markets. Not by avoiding uncertainty, but by pricing it, managing it, and turning it into an edge.

If your business is trying to grow without tightening the cash-flow bottleneck, Comfi can help you explore practical ways to access working capital through invoice discounting, buy now pay later options, and automotive dealer financing structures built for SMEs across MENA.