A Guide to Managing Payment Risk for MENA Businesses

Payment risk is the possibility that a customer’s promise to pay might not materialize as expected. The payment could be late, for less than you’re owed, or—in the worst-case scenario—it might never arrive. This threat can send shockwaves through a business, disrupting everything from supplier payments to your team's payroll.

Understanding the True Impact of Payment Risk

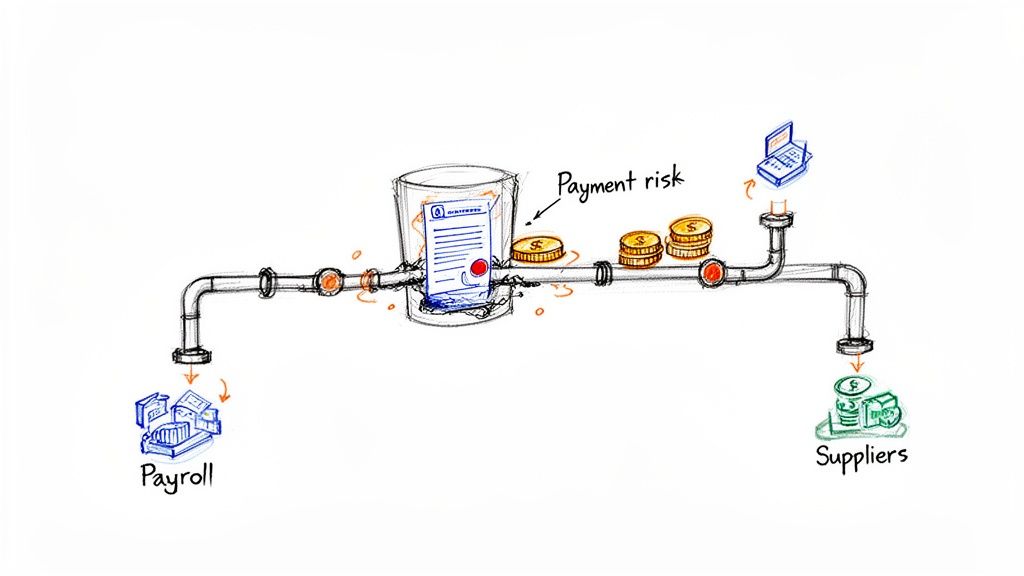

For any small or medium-sized enterprise (SME), cash flow is the lifeblood of the business. Imagine your company's finances as a series of connected pipes. When cash flows freely, operations run smoothly. However, a single late or missed payment acts like a clog, instantly building pressure that backs up the entire system.

This kind of disruption is more than a minor inconvenience. It has tangible consequences that can slow your growth or even jeopardize the entire operation. For SMEs in the MENA region, managing this risk is not just a defensive tactic—it’s a fundamental strategy for building a sustainable business.

The Domino Effect on Your Business

The moment a payment goes missing, a chain reaction begins. Suddenly, you may struggle to pay your own suppliers, which can sour key relationships and disrupt your supply chain. Next, you might find it difficult to make payroll, a situation that can damage team morale and make it hard to retain talented employees.

The core issue with payment risk is that it freezes your working capital. Money that should be fueling growth—by purchasing new inventory, investing in marketing, or hiring staff—is instead stuck in accounts receivable, waiting to be collected.

This domino effect is precisely why you can’t afford to ignore payment risk. Managing it proactively ensures your business not only survives these challenges but thrives despite them. To see how this ties directly into your financial operations, you can explore our detailed guide on optimizing payments and receivables.

From Defense to Offense

Once you start shielding your cash flow from these disruptions, you take the first step toward stable, predictable growth. With reliable systems in place to manage payment uncertainty, you can focus on the bigger picture. Here’s what solid risk management helps you achieve:

- Improved Financial Planning: Predictable cash flow allows for confident forecasting and budgeting, making it easier to plan for future investments.

- Stronger Supplier Relationships: Paying your vendors on time builds trust, which can lead to better terms, priority service, and a more resilient supply chain.

- Enhanced Growth Opportunities: With capital readily available, you can say "yes" to new opportunities, whether it’s taking on a large order or expanding into a new market, without being held back by cash flow concerns.

Ultimately, tackling payment risk head-on transforms a major business vulnerability into a strategic advantage, clearing the path for long-term success.

The Five Key Types of Payment Risk You Need to Know

Payment risk is not a single problem but a collection of different threats, each with its own cause and solution. To protect your business, you must be able to differentiate them. Think of it like a doctor diagnosing an illness: you need to identify the specific cause to prescribe the right treatment.

The same logic applies here. Understanding the difference between a customer who genuinely cannot pay and one who is attempting to commit fraud is critical. Each scenario requires a different approach. Let’s break down the five most common types of payment risk that businesses, especially SMEs in the MENA region, encounter.

Credit Risk or Default Risk

This is the most common type of payment risk. Credit risk, also known as default risk, is the danger that a customer will be unable to pay their invoice on time due to financial difficulties. It’s usually not malicious; they could be dealing with their own cash flow crisis, a sudden drop in business, or poor financial planning.

For example, a construction supplier in Dubai might give a contractor 60-day payment terms on a large order of materials. If the contractor’s client pays them late, that delay trickles down. The contractor then can't pay the supplier, creating a cash flow gap. This is a classic case of credit risk rippling through the supply chain.

Settlement Risk

Often occurring in more complex transactions, settlement risk happens when you deliver your side of the bargain, but the other party fails to complete theirs. It's a risk of timing. Imagine you're a wholesaler shipping a container of electronics to a retailer. You send the goods, but the bank transfer that was supposed to clear upon delivery hits a technical snag or is blocked.

The goods are gone, but the money is not yet in your account. This risk is especially prevalent in cross-border deals where different banking systems, time zones, and compliance checks create multiple points where a payment can fail.

Fraud Risk

This is where the intent becomes malicious. Unlike credit risk, fraud risk involves deliberate deception. It’s when a bad actor makes a purchase with no intention of paying for it. Fraud can manifest in various ways, all posing a direct threat to your bottom line.

A study by the Association of Financial Professionals found that paper checks, still common among some businesses, remain the payment method most frequently targeted by fraud. This serves as a reminder that traditional payment methods carry modern risks.

Here are a few common examples of fraud risk:

- Identity Theft: A scammer uses stolen credit card details to make a purchase, leaving you to deal with the chargeback when the legitimate cardholder disputes the transaction.

- Phishing Scams: An employee is tricked by a fraudulent email and sends a payment to an account that looks like a legitimate supplier’s but is controlled by a fraudster.

- Friendly Fraud: A legitimate customer makes a purchase but then disputes the charge with their bank, falsely claiming they never received the product or that it was defective.

Foreign Exchange Risk

For any business in the MENA region that buys or sells internationally, foreign exchange (FX) risk is a constant concern. This risk arises from fluctuating currency values. If you invoice a customer in a foreign currency, the final amount you receive in your local currency could be less than you budgeted for if the exchange rate moves against you.

Consider a software company in Egypt billing a client in Saudi Arabia in US dollars. If the Egyptian Pound strengthens against the dollar before the invoice is paid, the revenue they receive after conversion will be lower than anticipated, squeezing their profit margin.

Liquidity Risk

Finally, there’s liquidity risk. This is the danger of not being able to meet your own financial obligations—like rent, salaries, or supplier payments—because your cash is tied up in unpaid customer invoices. Your business might be profitable on paper, but if your customers take 90 days to pay while your own suppliers demand payment in 30, you'll face a liquidity crunch.

This isn't about being unprofitable; it's about not having cash available when you need it. This type of payment risk can bring a healthy, growing company to a halt, forcing it to delay essential payments or pass up new opportunities because its working capital is stuck in accounts receivable.

How to Measure and Monitor Your Payment Risk Exposure

Knowing the different types of payment risk is a great first step, but you can’t manage what you don’t measure. To effectively protect your business, you need to shift from simply being aware of the dangers to actively tracking your exposure with a few key metrics. This is how you spot potential trouble before it becomes a full-blown cash flow crisis.

Think of these metrics as your business's early-warning system. Just as a car's dashboard indicates low fuel or engine trouble, your financial reports can signal when payment risk is increasing. By keeping a close eye on these key indicators, you can move from reactively chasing late payments to proactively defending your company’s financial health.

Key Metrics for Your Financial Dashboard

You don’t need a complicated analytics suite to get started. Two fundamental tools can provide a clear view of your accounts receivable health. They are both easy to calculate and offer immediate, actionable insights into how efficiently you’re getting paid.

First is Days Sales Outstanding (DSO). This metric calculates the average number of days it takes for customers to pay you after a sale. A high DSO is a red flag, indicating that customers are taking longer to pay, which ties up your cash and increases your risk of default. A low DSO, on the other hand, signals a healthy and efficient collections process. For a deeper look, check out our guide to the Days Sales Outstanding calculation and see how it impacts your business.

The second essential tool is your Aged Receivables Report. This report is your operational map, breaking down all outstanding invoices by how long they’ve been overdue—typically in buckets like 0-30 days, 31-60 days, 61-90 days, and 90+ days. It gives you a snapshot of which invoices are becoming problematic and require immediate attention.

By regularly reviewing your Aged Receivables Report, you can instantly identify which customers are chronic late payers and how much of your capital is locked up in older, riskier invoices. An invoice that is 90 days past due is far more likely to go unpaid than one that is only 15 days late.

Spotting the Red Flags Early

Monitoring these numbers is about learning to read the signals. A sudden spike or a gradual increase in the wrong direction can be a major red flag that your risk exposure is changing. Paying attention allows you to intervene before a small issue escalates.

Here are some critical warning signs to watch for:

- A Climbing DSO: If your overall DSO starts increasing month after month, it’s a clear sign your collections are slowing down. This could be due to an internal process issue or a broader trend of customers struggling to pay on time.

- A Key Customer’s DSO Spikes: Keep a close eye on the payment habits of your largest customers. If a major client who normally pays in 30 days suddenly starts taking 60 or 70 days, it could be an early indicator of their financial trouble.

- Growing Balances in Older Buckets: When you see more money piling up in the "61-90 days" or "90+ days" columns of your report, it’s time to take action. These are your highest-risk accounts and require immediate follow-up.

To make your monitoring even more robust, consider implementing a structured fraud risk assessment. This adds another layer of security to your financial monitoring, helping you catch deliberate non-payment schemes before they impact your bottom line. Combining these key financial metrics with a formal approach to risk assessment creates a powerful defense for your cash flow.

Practical Strategies to Mitigate Payment Risk

Knowing your risks is one thing, but actively defending against them is another. It’s time to move from monitoring to action, because protecting your cash flow is non-negotiable. This involves building a proactive toolkit of strategies to reduce your exposure to late or non-payments and create a more secure financial foundation for your business.

These are not complex financial maneuvers reserved for large corporations. They are practical, common-sense steps you can start implementing right away to regain control of your payment risk. Think of each one as another layer of defense, helping you build a more resilient and predictable business.

Establish a Clear and Firm Credit Policy

The best way to manage payment risk is to prevent it from entering your business in the first place. This starts with a solid credit policy that sets clear expectations for every new customer before you offer them payment terms. A well-defined policy is your first and most important line of defense against potential defaults.

This should not be an informal understanding; your credit policy must be a formal document. It acts as a consistent guide for your team and a transparent agreement with your customers.

A strong credit policy should include the following components:

- Credit Application Process: Require every new B2B customer to complete a detailed application, including trade references from other suppliers they work with.

- Due Diligence Standards: Define the steps you will take to verify a customer's ability to pay, such as calling their references or setting an initial, modest credit limit that can be increased over time.

- Explicit Payment Terms: Clearly state your standard payment terms (e.g., Net 30, Net 60), the payment methods you accept, and any penalties for late payments.

This foundational step ensures you only extend payment terms to customers with a proven track record of reliability, reducing your risk from day one. To set this up efficiently, explore our guide on how to start accepting payments online securely.

Implement Professional Collections Workflows

Even with the best credit policy, late payments can still occur. How you handle them makes all the difference. A professional, systematic collections process ensures you recover your money without damaging valuable customer relationships. The key is to be persistent yet always polite.

By implementing strategic automations for invoicing and follow-ups, businesses can significantly reduce late payments. Automated reminders can send a gentle nudge as an invoice nears its due date and more formal notices once it’s overdue. This saves your team time and helps ensure no invoice is overlooked.

A structured collections workflow isn't about being aggressive; it's about being organized. It demonstrates that you take your accounts receivable seriously while maintaining a professional tone that preserves goodwill.

When an invoice becomes seriously overdue, a phone call is often more effective than another email. That personal touch can help you understand the reason for the delay—perhaps the invoice was misplaced—and agree on a firm payment date.

Leverage Modern Payment Solutions

In the past, offering flexible payment terms to secure larger orders meant shouldering all the credit and liquidity risk yourself. Fortunately, today’s digital platforms have changed the game. Now you can provide buyers with the flexibility they need without putting your own cash flow at risk.

One of the most pressing concerns in the MENA region is fraud. For instance, the rise of cyber-fraud in Egypt and Morocco is making consumers anxious, and that concern is spreading to other North African markets. This erosion of trust is a critical payment risk for the entire region, directly increasing processing costs for SMEs as payment acquirers navigate fragmented regulations.

Solutions like invoice discounting or offering Buy Now, Pay Later (BNPL) through a third-party provider are excellent ways to sidestep these risks. These services pay you for your invoices almost immediately, while your customer gets the extended payment window they want. This approach effectively transfers the credit risk away from your business, allowing you to unlock working capital and secure your cash flow. By embracing these tools, you can turn a potential risk into a competitive advantage, helping you close more sales and grow with confidence.

How Comfi Helps You Overcome Payment Risk and Unlock Growth

Understanding the different types of payment risk is one thing, but implementing a solution is what truly protects your business. Instead of just reacting to late payments, you can build a system that prevents them from derailing your cash flow in the first place. This is where Comfi provides a clear path forward for MENA SMEs, turning payment uncertainty into a strategic advantage.

At its core, Comfi directly addresses the two biggest threats to a supplier’s stability: credit risk and liquidity risk. The moment you offer payment terms to a buyer, you are exposed to the possibility of a default, and your cash becomes locked up in accounts receivable. This ties up the working capital you need for payroll, inventory, and strategic growth.

Turn Your Invoices into Immediate Cash Flow

Comfi’s Invoice Discounting solution was built to end this waiting game. The process is simple: you complete a job or deliver your goods, send your invoice as usual, and then upload it to the Comfi platform. Instead of waiting 30, 60, or even 90 days for your customer to pay, you receive the cash for that invoice upfront—typically within 24 hours.

This single step transforms your accounts receivable from a list of future payments into cash in the bank, ready to be used. The risk of a buyer paying late, or not at all, is no longer your concern.

By getting paid upfront, you completely remove the supplier's risk of buyer default. This means you can run your business on predictable cash flow, confident that you’ll be paid for your work on time, every single time.

With this newfound liquidity, many of our clients find they can finally unlock their working capital and pursue growth opportunities that were previously out of reach.

Secure Larger Deals by Offering Flexible Terms

In a competitive market, the ability to offer attractive payment terms can be the deciding factor in winning a major contract. However, for most SMEs, offering Net 60 or Net 90 terms creates a level of payment risk and cash flow strain that is not sustainable. Comfi removes this barrier entirely.

You can confidently offer flexible payment options to close bigger deals and attract more customers. Your buyer gets the timeline they need, while you still get paid right away. This strategy gives you a significant competitive edge without forcing you to carry any of the financial weight.

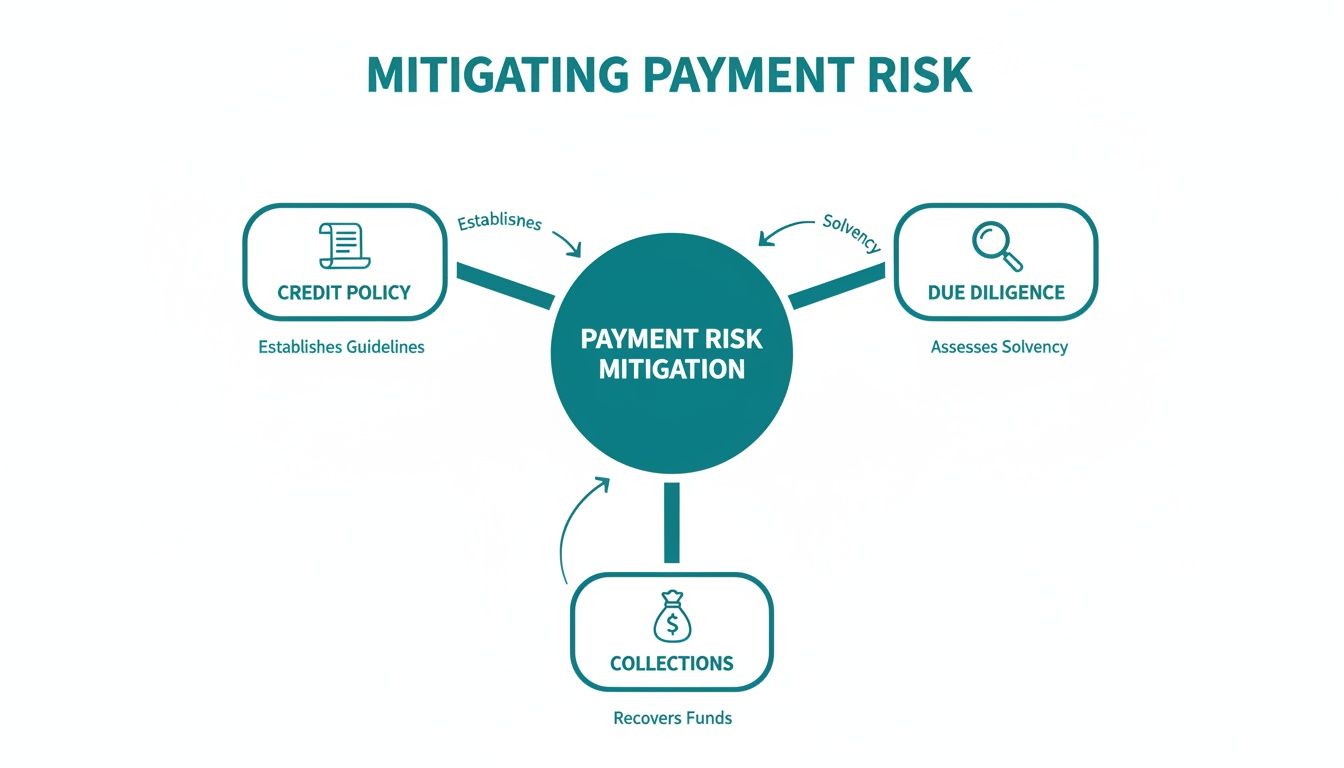

The flowchart below illustrates the core pillars of a solid risk mitigation strategy, which Comfi helps automate and secure for you.

This visual breaks down how a combination of strong credit policies, proper due diligence, and smart collections creates a powerful defense against payment risk—all elements that are managed when you partner with a platform like Comfi.

A Secure and Digital Process Built for MENA Businesses

Security is another critical piece of the puzzle. The average cost of a data breach in the Middle East reached $8.75 million in 2024, an 8.4% increase in just one year. In the UAE, where digital payment adoption is at 88%, the sheer volume of transactions makes businesses a prime target for cybercriminals. You can read more about the key payment trends shaping the region to understand how quickly the landscape is changing.

Comfi’s entire process is digital, fast, and secure, designed to integrate seamlessly into your existing workflow without causing disruption. Here’s a quick look at how it works:

- Simple Onboarding: Set up your account through a completely paperless, online process.

- Instant Eligibility Checks: Integrate with our platform via low-code plugins or a developer-friendly API to get instant decisions.

- Fast Funding: Once you're approved, simply upload your invoices and get funded within 24 hours.

This efficiency helps MENA SMEs grow with confidence, knowing their payments are secure and their cash flow is stable.

Got Questions About Payment Risk? We've Got Answers.

Here are clear, straightforward answers to the questions we hear most often from business owners in the MENA region. Navigating payment risk can feel complex, but with the right information, you can make confident decisions that protect your cash flow and support your business's growth.

These are not textbook definitions but practical answers to the real-world challenges you face every day, from evaluating new customers to managing cross-border payments.

What Is the Single Biggest Payment Risk for a Small Business?

For most SMEs, the biggest risk is credit risk. This is the classic scenario where a customer fails to pay their invoice. Whether they are unable or unwilling, the result is the same: a gap in your cash flow. For a small business, that gap can be devastating.

Unlike large corporations with deep cash reserves, an SME’s financial cushion is often much thinner. You might rely on a handful of key clients, so a single large unpaid invoice is more than an annoyance; it can bring your entire operation to a halt.

Suddenly, you're struggling to pay your own suppliers, cover payroll, or invest in new inventory. This is why having a robust credit policy and using modern tools to secure your payments is essential for survival and growth.

How Can I Check the Creditworthiness of a New B2B Customer?

Checking a new B2B customer’s ability to pay is one of the smartest, most proactive steps you can take. You don’t need a team of analysts; a few methodical steps can tell you almost everything you need to know about their financial reliability.

Start with a formal credit application form. This simple document should ask for their basic business information and, most importantly, trade references from their other suppliers. Those references are invaluable.

Give their other suppliers a call. It’s the best way to get unbiased, real-world insight into their payment habits. Do they pay on time? Are they consistently late? Do they become difficult when it's time to collect?

For larger deals or if you’re offering significant payment terms, it might be worth obtaining a formal report from a credit agency in the MENA region. A smart approach for new clients looks like this:

- Start with a modest limit. Keep your initial exposure small and manageable.

- Monitor the first few payments closely. Timely payments are the best signal you can get.

- Increase their limit gradually. As they build a track record of paying on time, you can reward that trust with more flexibility.

This phased approach allows you to build a relationship based on proven performance, protecting your business while you grow together.

Does Offering Flexible Payment Terms Increase My Risk?

Traditionally, the answer was yes. Offering Net 30, 60, or 90 terms meant you were effectively acting as your customer’s bank. This increased your exposure to credit risk and tied up your working capital in unpaid invoices, putting a significant strain on your liquidity.

However, modern fintech platforms have changed the landscape. You no longer have to choose between making a sale and protecting your cash flow. By partnering with a service like Comfi, you can offer buyers the attractive, flexible terms they want while you get paid for the invoice upfront.

In this model, the credit risk is shifted off your shoulders. This turns what used to be a major financial gamble into a powerful sales tool. You can confidently offer the payment flexibility that wins deals, securing a major competitive edge without taking on the associated risk.

How Do I Manage Foreign Exchange Risk Across MENA Countries?

If you conduct business across borders in the MENA region, you must manage foreign exchange (FX) risk. This is the danger that currency fluctuations will reduce the value of your payment between the time you issue the invoice and the day the money arrives in your account. A profitable deal can quickly become a losing one if the market moves against you.

Fortunately, there are practical ways to protect yourself. The simplest strategy is to invoice customers in your own local currency. This passes the FX risk to the buyer, as it becomes their responsibility to handle the currency conversion.

If that isn't an option, you can use a few financial tools to lock in your revenue:

- Forward Contracts: These allow you to agree on a specific exchange rate for a future date, providing certainty on the amount you’ll receive.

- Currency Options: This gives you the right—but not the obligation—to exchange currency at a set rate, protecting you from losses while allowing you to benefit from favorable moves.

- Multi-Currency Accounts: You can also open bank accounts in the currencies you use most frequently, reducing conversion fees and administrative hassle.

Consulting with a financial advisor who specializes in international trade can help you determine the most cost-effective strategy for your business.

Ready to eliminate payment risk and unlock your business’s full potential? Comfi provides fast, secure solutions that turn your invoices into immediate cash, allowing you to offer flexible terms to buyers without carrying the risk. Grow your sales, improve your cash flow, and focus on what you do best.

Related Reading

- B2B Payments

- Solve Creative Agency Late Payment UAE Issues

- How Payment Default Dents Small Business Growth and Survival

- A Guide to B2B Payment Solutions for MENA Businesses

Looking to improve your cash flow? Explore Comfi's Buy Now Pay Later solutions. Get started today.