Credit Risk Management: A Guide for UAE SMEs

You close a sale, issue the invoice, ship the goods, and then wait.

If you're an SME owner in the UAE, that waiting period can feel longer than the agreed terms. The customer asked for 30, 60, or 90 days. Your supplier still wants payment sooner. Payroll won't pause. Inventory doesn't replenish itself. One unpaid invoice can turn a healthy sales month into a cash squeeze.

That tension is where credit risk management stops being a banking phrase and becomes a practical business skill. It's the discipline of deciding who gets terms, how much exposure you're willing to carry, how you spot trouble early, and what you do before late payments turn into real losses.

For many SMEs, the problem isn't lack of sales. It's that cash arrives later than obligations do. If you already have a stack of invoices sitting in “not yet due” and “follow up next week”, it helps to understand the wider issue behind outstanding invoices and why they strain cash flow. Once you see the pattern, you can build better controls around it.

The Hidden Risk in Every Unpaid Invoice

A wholesaler gives a new retail customer 60-day terms. On paper, the deal looks excellent. Revenue goes up, the customer seems credible, and the relationship starts well. But between delivery day and payment day, the wholesaler carries the risk.

If the customer pays late, the damage isn't only accounting-related. The business may delay a stock purchase, postpone a hiring decision, or negotiate awkwardly with its own suppliers. That's how credit risk enters daily operations. It shows up subtly, inside ordinary commercial decisions.

Why the risk feels invisible at first

Most SME owners don't think of trade terms as lending. But that's effectively what they are. When you deliver today and collect later, you're extending trust backed by your balance sheet.

The risk is hidden because the sale is already booked. The team sees growth. The problem appears later, when cash and profit stop moving together.

Practical rule: Revenue booked today doesn't mean cash available today.

What credit risk looks like in real life

For SMEs, credit risk usually appears in familiar ways:

- A customer pays slower than agreed. The invoice may still get paid, but the delay puts pressure on payroll, rent, and supplier payments.

- One large buyer takes too much space in your receivables. If that account slows down, your whole month tightens.

- You keep extending more terms to an existing customer. The relationship feels safe until the outstanding balance becomes uncomfortably large.

- Collections start too late. By the time someone notices the pattern, the issue is already harder to fix.

Credit risk management starts with a simple mindset shift. An unpaid invoice isn't just an administrative item. It's an asset with uncertainty attached to it.

What Is Credit Risk Management Really?

Credit risk management is the system a business uses to control the risk that a customer won't pay on time, or won't pay in full. For an SME, that means making thoughtful decisions about payment terms, customer exposure, monitoring, and follow-up.

A useful way to think about it is traffic control for your cash flow. Good traffic control doesn't stop all movement. It keeps vehicles moving safely, prevents pile-ups, and directs attention where congestion is building. Credit risk management works the same way. It's not there to stop sales. It's there to help you grow without creating avoidable cash blockages.

It's not about saying no to everyone

Many owners assume credit discipline means becoming overly strict. In practice, the opposite is true. Strong controls help you say yes more confidently because you know the limits, conditions, and warning signs.

That matters in the UAE. The country's annual non-oil foreign trade reached AED 3.5 trillion in 2023, which makes disciplined credit controls a core operating need for SMEs working through short working-capital cycles, where even modest payment delays can affect liquidity (Cedar Rose on UAE trade-credit risk).

If you're also trying to tighten collections and improve receivables discipline, this guide on how to improve cash flow with AR is a useful companion read.

The main types of risk SMEs actually deal with

A non-specialist doesn't need a textbook list. You need the forms of risk that show up in practice:

- Default risk means the customer may not pay at all.

- Delay risk means they probably will pay, but later than agreed.

- Concentration risk means too much of your exposure sits with one customer, one sector, or one buying pattern.

- Behavioural risk means a previously reliable customer starts changing. Smaller orders, disputes, broken promises, or stretched payment behaviour often show up before a serious problem.

The real objective

Good credit risk management helps you answer four practical questions:

- Should we offer terms to this customer?

- How much exposure can we safely allow?

- What early signals tell us risk is rising?

- What action do we take before the situation worsens?

Credit risk management is less about predicting the future perfectly and more about avoiding surprises you could have prepared for.

That's why the best systems aren't complicated for the sake of it. They're clear, repeatable, and tied to daily decisions.

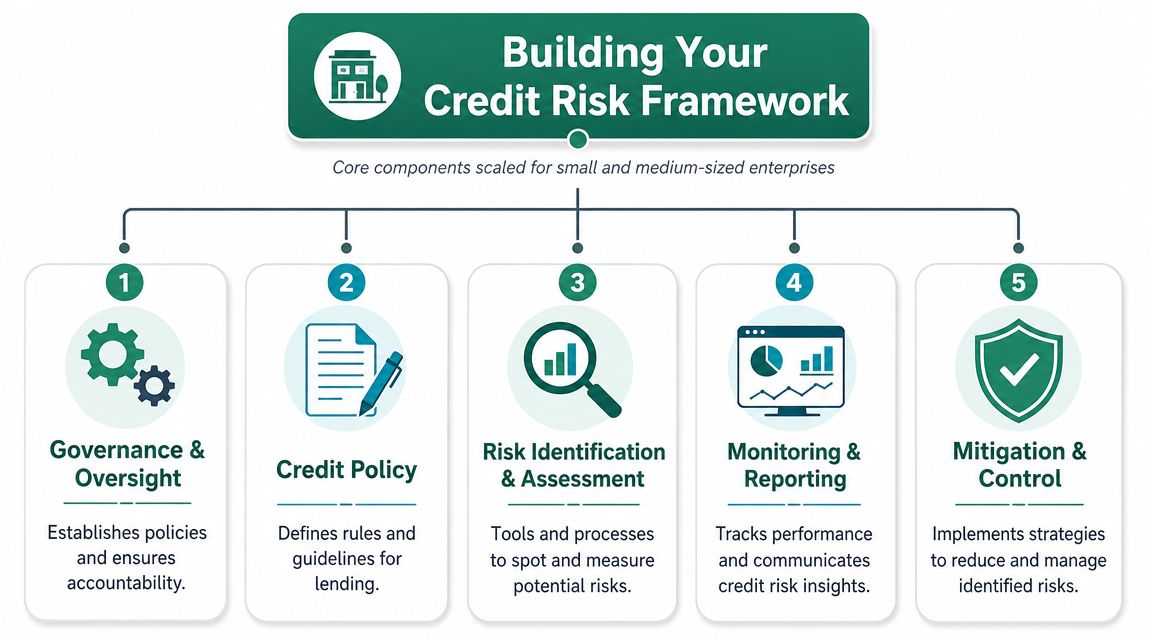

Building Your Credit Risk Framework

Most SMEs don't need a thick policy manual. They need a workable framework that turns judgment into a repeatable process. Even a one-page rulebook is better than relying on memory, urgency, or whoever shouts loudest for order release.

A sound framework also reflects a forward-looking habit. In the UAE financial system, the IFRS 9 framework requires expected credit losses to be estimated proactively rather than only after default. For SMEs, that principle matters even informally. It encourages better decisions before extending terms, not after a payment problem has already happened (overview of IFRS 9 and forward-looking credit assessment).

Here's the structure in one view:

Start with risk appetite

Risk appetite sounds corporate, but the idea is simple. How much uncertainty are you willing to accept in exchange for growth?

For an SME, that could mean deciding:

- Which customer profiles fit your business

- Which sectors you're cautious about

- How much exposure any single buyer can hold

- When senior approval is needed

If you don't define risk appetite, your sales team, finance team, and founder will each invent their own version of it.

Turn it into a credit policy

A good credit policy doesn't need jargon. It needs clarity.

Include the basics:

- Customer onboarding requirements such as trade licence, financial information, references, or internal checks

- Credit limit rules including who can approve what

- Payment terms by customer type or order profile

- Escalation triggers for overdue balances, disputes, or repeated broken promises

- Collections timing so follow-up starts on schedule, not when someone remembers

Assign ownership clearly

Confusion creates risk. So does politeness. Many SMEs avoid hard conversations because no one wants to challenge a salesperson's relationship or a founder's preferred customer.

Decide upfront:

- Sales can request terms

- Finance can assess exposure

- A named approver can override policy, but only with a recorded reason

- Collections responsibility sits with a person, not a shared inbox

Owner's shortcut: If a customer asks for more terms, your team should know exactly who decides, based on what evidence, and within what limit.

Report simply, but regularly

Reporting doesn't need a dashboard full of colours. It needs a few recurring questions:

- Which accounts are overdue?

- Which balances are getting concentrated?

- Which customers have changed behaviour?

- Which exceptions were approved outside policy?

A framework works when it reduces inconsistency. The goal isn't perfection. The goal is fewer avoidable mistakes.

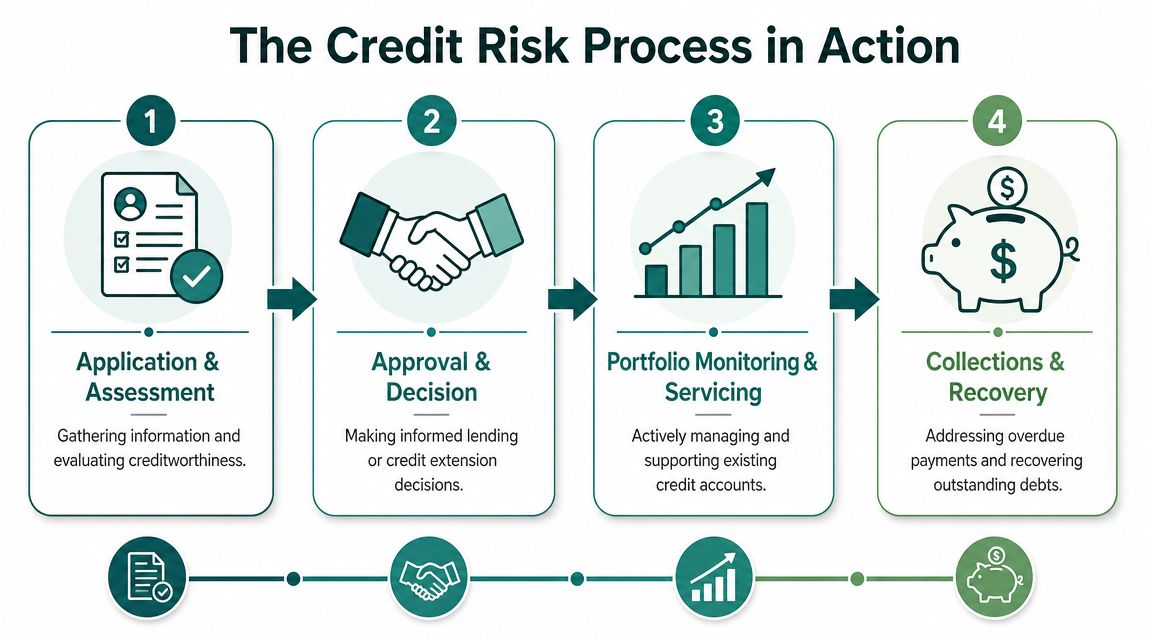

The Credit Risk Process in Action

A framework is the rulebook. The process is what your team does every week. For SMEs, the most useful version has four parts: assessment, monitoring, provisioning, and collections.

This workflow is easier to grasp visually:

Assess before you extend terms

The first mistake many businesses make is checking too little, too late. Credit assessment doesn't need to feel like a bank application, but it does need structure.

Focus on a few practical checks:

- Business identity and legitimacy such as registration details and who is authorised to place orders

- Ability to pay based on financials, trading history, or payment behaviour if they're already known to you

- Commercial logic including order size versus company profile

- Requested terms versus your normal terms because urgency often hides risk

If the customer is new, start smaller. It's easier to increase a limit later than to unwind a bad first decision.

Monitor after approval

Many SMEs treat credit as a one-time check. That's risky. A good customer can weaken quickly, and a weaker customer often gives clues before they stop paying.

In SME and corporate lending in the region, credit models are increasingly expected to use more frequent updates instead of static annual reviews. Strong practice includes setting update frequencies for data fields and checking for missing data, duplicates, and outliers so decisioning stays reliable (Finalyse on credit risk data refresh and controls).

For an SME, the simpler lesson is this:

- Review payment behaviour regularly

- Refresh customer information on a schedule

- Watch for disputes, partial payments, and sudden order spikes

- Treat changing behaviour as a signal, not a coincidence

Provision for what might go wrong

Provisioning means setting aside an allowance for likely losses. Even if your business does this informally, the discipline matters.

Why? Because receivables can look healthier than they really are. If all invoices are counted as fully collectible until proven otherwise, your internal picture becomes overly optimistic.

A sensible SME approach is to flag categories such as current, mildly overdue, and seriously overdue, then discuss what portion may be at risk. The exact accounting treatment belongs with your finance lead or adviser, but the management habit is what counts.

A receivable isn't worth its full face value if the customer is already showing strain.

Collect early and professionally

Collections aren't only about chasing old debt. They're about protecting relationships while reducing drift.

Use a structured playbook:

- Before due date send a reminder with invoice details and confirmation of receipt

- On due date follow up politely and confirm the payment timeline

- After missed payment escalate contact frequency and involve a decision-maker

- If patterns repeat review the credit limit, terms, or account status

For teams building a tighter routine, this accounts receivable playbook for SMEs offers practical ideas on organising follow-up.

The key is consistency. Customers learn quickly whether your terms are real or optional.

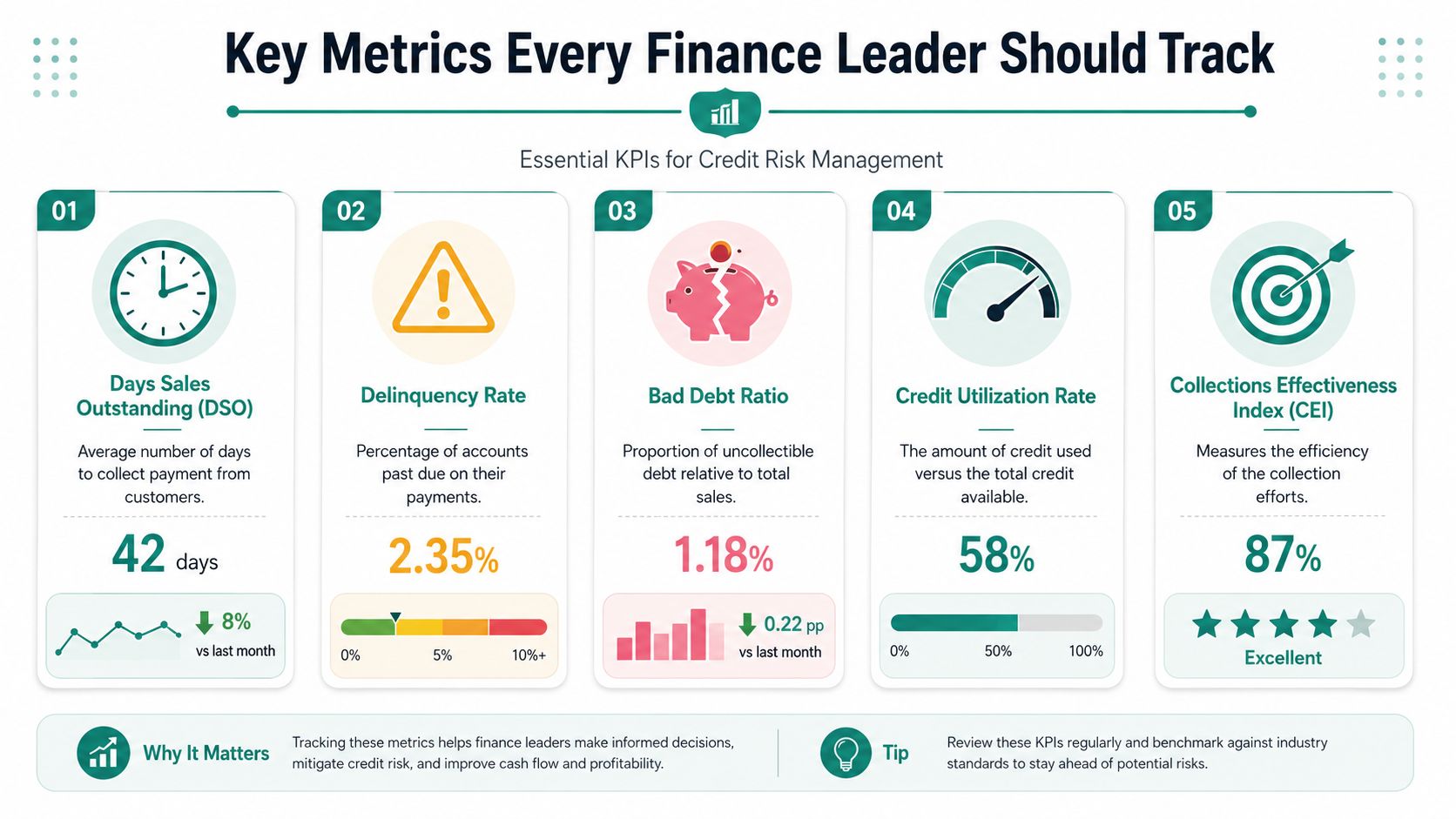

Key Metrics Every Finance Leader Should Track

You can't manage credit risk with intuition alone. You need a short list of measures that tell you whether receivables are healthy, stretched, or gradually deteriorating.

For businesses in the region, portfolio concentration control and monitoring receivables aging are core levers. Best practice includes setting exposure limits by customer and industry, then tracking delinquency and aging to catch deterioration early (Ramp on concentration and receivables monitoring).

This visual captures the core dashboard items:

Receivables aging tells you where pressure is building

Aging is one of the simplest and most useful reports in finance. It groups receivables by how long they've been outstanding.

What to watch:

- Current balances that are not yet due

- Recently overdue invoices that may still be routine

- Older buckets where recovery gets harder and attention should increase

A worsening aging profile often appears before write-offs do. That's why many experienced finance leaders look at aging before they look at profit.

Concentration shows whether one account can hurt you

If one customer represents a large share of receivables, your exposure is concentrated even if they've always paid on time. Dependability and concentration are not the same thing.

Track concentration by:

- Customer

- Industry

- Geography

- Product line if risk patterns differ materially

This helps answer a blunt but useful question. If this one segment stalls, how much stress lands on your cash flow?

Delinquency, DSO, and loss thinking

Three more measures deserve regular attention:

- Delinquency rate tracks how many accounts are past due. Even without a complex formula, a rising pattern is a warning sign.

- Days Sales Outstanding or DSO shows how long it takes to collect, on average. If sales rise but DSO drifts upward, growth may be consuming cash faster than it appears.

- Loss thinking through PD and LGD helps frame risk. Probability of default (PD) asks how likely non-payment is. Loss given default (LGD) asks how much you'd likely lose if default happens.

You don't need a bank-grade model to use these ideas. You can ask simpler versions:

- Which customers look increasingly likely to miss payment?

- If they do, how much could we realistically recover?

- Are we pricing and limiting exposure with that in mind?

Management habit: Track trends, not just snapshots. A customer who moves from current to mildly overdue repeatedly may be riskier than one isolated late payer.

Smarter Decisions with Modern Tools and Data

Traditional credit assessment relies heavily on what a customer has already done in formal credit systems. That still matters. But for many SMEs, especially thinner-file businesses, it doesn't tell the full story.

Modern credit risk management increasingly uses a broader mix of signals. That includes utility records, telecom data, rental behaviour, and cash-flow information. For UAE SMEs, that matters because many solid businesses trade actively but don't fit neatly into old-style credit files.

Traditional data versus alternative data

Traditional data is familiar:

- Credit bureau history

- Financial statements

- Trade references

- Past payment record with your business

Alternative data adds another layer:

- Utility payment patterns

- Telecom payment behaviour

- Rental data

- Cash-flow activity

The World Bank notes that using utility, telecom, and cash-flow data can improve the predictive power of risk models by 5% to 20% compared with traditional-only models, while improving access for underserved businesses (World Bank report on alternative data and SME credit assessment).

Why this matters for SMEs

An SME can be operationally healthy and still look “thin” on conventional credit records. That creates a gap between real business activity and formal credit visibility.

Alternative data helps close that gap because it answers a practical question: does this business show a pattern of keeping commitments across day-to-day obligations?

That doesn't mean every new data source is automatically useful. The quality of the process still matters. Data needs to be governed, refreshed, checked, and interpreted carefully. Faster inputs are only helpful if they improve judgment rather than create noise.

The role of fintech tools

Fintech tools make this approach more accessible because they can pull multiple signals into one process, rather than forcing teams to review everything manually. That supports quicker, more current decisions for SMEs that need terms, invoice-based workflows, or embedded payment options.

If you want a broader view of how digital platforms are reshaping financial operations for businesses, this overview of fintech and how it changes SME finance is worth reading.

The practical takeaway is simple. Better data helps you make fairer decisions. It can help you avoid rejecting a good customer just because the old file is incomplete, and it can also help you spot risk that a basic bureau check would miss.

How New Payment Models Change the Risk Equation

Once you understand credit risk management, a bigger strategic question appears. Should your business carry all that risk itself?

Many SMEs still treat trade credit as unavoidable self-funding. They offer terms, wait to be paid, chase collections, and absorb the uncertainty. New payment models change that setup by moving parts of the risk, timing, and admin burden away from the supplier.

What changes with invoice discounting and B2B BNPL

These models differ in structure, but they all affect the same core issue. They change who waits, who assesses buyer risk, and who manages repayment mechanics.

In practical terms:

- Invoice discounting can let a B2B supplier access cash tied up in approved invoices within hours, instead of waiting through the full payment cycle.

- B2B Buy Now, Pay Later lets B2B suppliers unlock credit invoices within hours, and allows their buyers to access flexible terms while the supplier avoids carrying the full collection burden alone.

That shift matters in fast-moving sectors where cash is constantly being recycled into inventory, fulfilment, and new sales.

Risk transfer isn't the same as risk disappearance

A useful misunderstanding to clear up is this. New payment models don't make credit risk vanish. They reallocate it and manage it differently.

That usually means a specialised partner takes on more of the underwriting, exposure control, servicing, or collections function. For the SME, the value is often operational as much as financial. The business can focus more on selling, stocking, and serving customers, rather than manually carrying every receivable risk on its own books.

For a non-specialist SME owner, the lesson is straightforward. Different products behave differently over time. You shouldn't judge all payment models by one blended average.

When to reconsider your current setup

It may be time to rethink your approach if any of these sound familiar:

- Sales are rising, but cash still feels tight

- A few buyers dominate your receivables

- Your team spends too much time chasing collections

- Inventory sits on the balance sheet longer than is comfortable

- You want to offer better terms without increasing stress on liquidity

For wholesale and distribution businesses exploring this shift, this guide to wholesale distributor BNPL in the UAE gives a more concrete view of how these structures work in practice.

The broader point is that payment design is now part of risk design. The way you structure terms can be just as important as the way you analyse the customer.

If your business is extending terms, waiting on invoices, or carrying too much cash-flow pressure between sale and payment, Comfi helps SMEs free up cash tied up in receivables within 24 hours, and offer flexible payment options through Invoice Discounting and Buy Now, Pay Later. That can reduce collection strain, support more predictable cash flow, and give your team more room to grow without taking on the full burden of credit administration alone.