How Payment Default Dents Small Business Growth and Survival

Picture this: you’ve delivered the goods, the invoice has been sent, and you’re waiting. And waiting. But the payment never shows up. That’s a payment default. It’s not just a late payment; it’s a direct threat to your cash flow and the survival of your small business. For Small and Medium-sized Enterprises (SMEs), preventing payment default isn't just good accounting—it's a critical strategy for growth.

What Payment Default Means for Your Business

For any small or medium-sized business in the MENA region, a single payment default can set off a domino effect that cripples your operations. Think of it as a sudden clog in your company’s financial arteries—everything downstream immediately seizes up. It's an all-too-common story where a customer's failure to pay puts a sudden stop to your own ability to operate.

When a customer doesn't pay, the fallout is instant and widespread. The most obvious hit is to your cash flow, the money you need for day-to-day survival. This quickly escalates into serious operational problems, stunting growth and, in the worst cases, threatening your company's existence.

If you want to understand just how severe ongoing payment issues can become, this guide on trading whilst insolvent offers some critical insights into the worst-case scenarios.

The Immediate Business Impact

A payment default is far more than just a line item in your accounting software. It actively sabotages your ability to run the business and chase new opportunities. The ripple effects are felt everywhere:

- You Can't Pay Your Own Bills: Suddenly, you’re struggling to cover payroll, rent, or what you owe your own suppliers. This doesn't just strain your finances; it damages your reputation and the relationships you rely on.

- Inventory Grinds to a Halt: Without cash coming in, you can’t restock your shelves. You’re left with nothing new to sell to your next customer, effectively freezing your sales cycle.

- Growth Opportunities Slip Away: That chance to land a big new contract or expand into a new market? It could pass you by simply because your funds are locked up in an unpaid invoice.

Ultimately, a default kills your momentum. Instead of focusing on strategy and growth, you’re stuck chasing down old debts. With the right approach and modern tools, you can protect your revenue and build a far more resilient business.

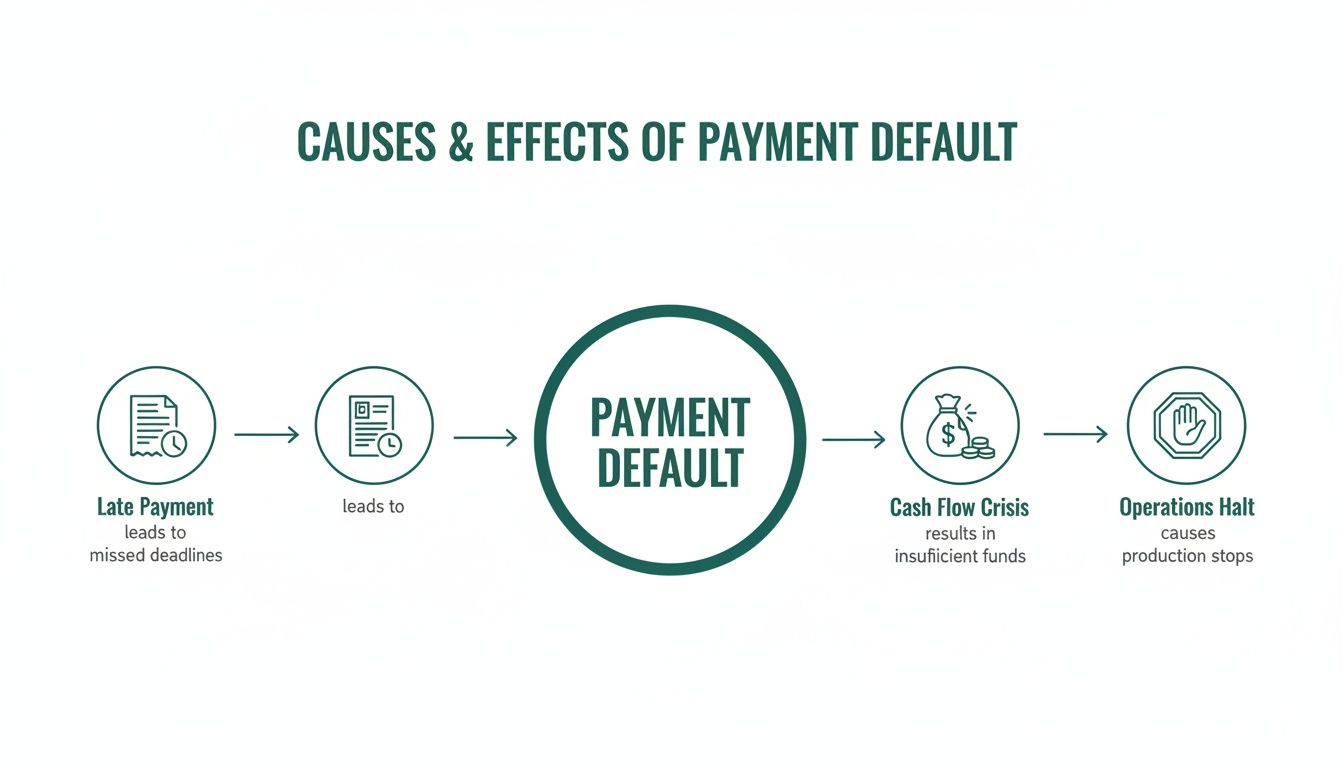

The Domino Effect of a Single Late Payment

A late payment is never just an isolated hiccup. It’s the first domino in a line, triggering a chain reaction that can destabilize your entire operation. The first thing to get hit is your working capital—the cash you need to keep the lights on.

Suddenly, you can't pay your own suppliers, cover payroll, or order new stock. This freeze in operations isn't just an inconvenience; it means lost sales and missed opportunities for growth, forcing your business onto the back foot. The longer that invoice remains unpaid, the worse the damage gets.

This flowchart shows just how quickly a single delay can snowball into a full-blown crisis that grinds your business to a halt.

As you can see, what begins as a simple missed deadline quickly spirals, choking off your cash flow and stopping your business from functioning.

The Long-Term Consequences

Beyond the immediate cash crunch, a payment default inflicts lasting scars on your company's reputation and financial standing. Here in the UAE, the stakes are especially high because of the structured systems in place for tracking financial behavior.

For SMEs, the fallout from a single unpaid invoice can be severe, potentially getting them blacklisted and making it difficult to secure future credit terms from suppliers or other business essentials they need to grow.

Official bodies like the Al Etihad Credit Bureau (AECB) keep a meticulous record of all financial defaults. Once a default is on your record, it becomes a mark on your credit history, making it incredibly tough to secure new supplier credit or other business essentials down the line. It doesn't disappear when the bill is finally paid; it lingers for years.

You can find out more about how default management works in the UAE on chambers.com.

This is precisely where getting proactive pays off. Fintech solutions from Comfi, like invoice discounting or B2B BNPL, help you sidestep these dangers. By turning your invoices into immediate cash, you cut out the waiting game and transfer the burden of collections. This lets you unlock your working capital, keeps your operations running smoothly, and shields your business from the harsh fallout of a payment default.

Why B2B Payments Fail in the MENA Region

To stop a payment default before it happens, you must understand why they occur. Across the MENA region, a late B2B payment is rarely as simple as a buyer just forgetting. The real reasons are often buried in systemic issues that can trip up even the most careful suppliers.

Often, the problem is a domino effect. Your customer is struggling with their own cash flow, and that delay trickles down until it hits you, leaving you holding an unpaid invoice. Other times, it's administrative friction—an invoice gets lost in a tangled approval process, or a dispute pops up over delivery details. These headaches are made worse by traditional B2B payment structures.

The Inherent Risk of 30, 60, and 90-Day Terms

Standard payment terms like net 30, 60, or 90 days are the bedrock of B2B trade. But they bake a massive risk of payment default right into your business model. You deliver your goods or services today but agree to wait weeks, or even months, to see the cash. That waiting period is a huge vulnerability for any SME.

A painful example of this is the problem of bounced cheques. Despite the push for digital payments, bad cheques are still a harsh reality for many businesses in the UAE. When a buyer's cheque bounces, it’s a clear-cut payment default that instantly freezes a supplier's working capital. You can see the scale of the issue in data from the Central Bank of the UAE’s cheque clearing system. For many SMEs, this can bring their entire operation to a grinding halt.

Once you understand these root causes—from your client’s internal struggles to the built-in risks of traditional payment terms—you can stop reactively chasing debt and start proactively protecting your cash flow.

The real fix is to get rid of the uncertainty altogether. This is where modern fintech platforms like Comfi come in, tackling the problem with two key solutions:

- Invoice Discounting: This lets you turn your approved invoices into cash almost immediately. The long, risky wait is over.

- B2B Buy Now, Pay Later (BNPL): You can offer your buyers the flexible payment terms they want, boosting your sales, while you get paid upfront. Comfi handles the collections process, completely removing your exposure to default risk.

By focusing on the real reasons B2B payments fail, you can build a far more predictable and resilient business. For a deeper dive, check out our guide on improving your B2B payment processes.

How Invoice Discounting Helps Prevent Payment Default

What if you could erase the anxious 30, 60, or even 90-day wait for a client to pay an invoice? For any business that's ever felt the squeeze of a potential payment default, this isn't just a fantasy—it's a smart, practical cash flow strategy. Invoice discounting is your shield against the risk of long payment cycles, providing a powerful way for clients to unlock working capital and keep their business moving.

The idea is simple. Instead of waiting weeks or months for your customer to settle up, you receive a cash advance against your approved, unpaid invoices. This instantly turns a future promise into real, spendable working capital.

Turn Invoices Into Instant Cash

With a service like Comfi, you can have your approved invoices converted to cash in as little as 24 hours. That long, nail-biting waiting game? It's over. Getting your money right away means you can pay your own suppliers, cover payroll, and manage your day-to-day expenses with confidence.

By using invoice discounting, you actively shield your business from the risk of non-payment. This is not just about getting paid faster; it’s about making your revenue predictable and secure.

Just as importantly, this process hands over the burden of collections. No more awkward follow-up calls or administrative headaches chasing down overdue payments. Comfi handles the follow-up directly with your buyer, freeing up your team to focus on what they do best—driving growth and serving customers.

This approach gives you a few game-changing advantages:

- Immediate Liquidity: You unlock the capital tied up in your accounts receivable, giving you the cash to pay suppliers, fund payroll, or invest in new inventory.

- Reduced Default Risk: You get your funds upfront. If a buyer ultimately fails to pay, your business is protected from the direct financial blow.

- Operational Freedom: With predictable cash flow, you can plan for the future with confidence instead of constantly reacting to cash shortages.

To see exactly how this works in the real world, you can learn more about invoice discounting in the UAE in our comprehensive guide. By securing your payments upfront, you build a much more resilient and growth-ready business.

Increase Sales and Prevent Defaults with B2B BNPL

Offering flexible payment terms is a powerful way to win more buyers, but it has always come with the risk of payment default. What if you could offer the flexibility your customers want without exposing your own cash flow? That's where B2B Buy Now, Pay Later (BNPL) comes in. This solution creates a genuine win-win, protecting your business while making you the supplier everyone wants to buy from.

The model is refreshingly simple. When you offer B2B BNPL through a partner like Comfi, you get paid the full invoice amount upfront. The risk of a buyer missing a payment or defaulting entirely is no longer your problem. It's completely taken off your books.

How B2B BNPL Creates a Win-Win

For you, the benefit is crystal clear: immediate cash in the bank and zero credit risk. For your buyers, it's a huge advantage. They get the flexibility to pay over 30, 60, or even 90 days, which helps them manage their own cash flow and place larger orders.

This isn't a niche idea; it’s a major market shift. Across all kinds of industries, Buy Now Pay Later (BNPL) continues to surge in popularity as businesses hunt for more adaptable ways to trade.

By integrating B2B BNPL, you’re not just tweaking your payment terms. You’re deploying a strategic tool that actively drives sales while building a fortress around your revenue.

This proactive approach is what separates businesses that get ahead from those that are always playing catch-up.

With a solution like Comfi's B2B BNPL, you can:

- Boost your sales by making your products easier to buy.

- Attract new, larger customers who need flexible payment terms.

- Eliminate default risk completely by getting paid upfront, every time.

By adopting this model, you can grow your business with confidence, turning the headache of potential payment defaults into guaranteed, predictable revenue. Find out how B2B Buy Now, Pay Later from Comfi can build a more resilient financial foundation for your business.

Build a Resilient and Default-Proof Business

For too long, businesses have treated payment defaults as a frustrating, but unavoidable, cost of doing business. But that’s a dangerous and outdated mindset. A default isn’t just bad luck; it’s a solvable problem, and the solution starts with a fundamental shift in how you think about getting paid.

The key is to move from a reactive position—chasing down late payments after the damage is done—to a proactive one. You need to stop simply hoping for payment and start architecting a system that guarantees it.

The goal is to shift your mindset from reactively chasing payments to proactively securing your revenue from day one. Partnering with a modern fintech provider like Comfi allows you to do just that.

This is where smart tools like invoice discounting and B2B Buy Now, Pay Later (BNPL) completely change the game. By weaving these into your sales process, you take back control and sidestep the worst parts of traditional payment terms. Suddenly, you can:

- Get Paid Instantly: Turn your outstanding invoices into cash in the bank, wiping out the risky 30, 60, or 90-day waiting period.

- Transfer Default Risk: Hand over the stress and uncertainty of collections. If a buyer doesn’t pay, it’s no longer your problem or your loss.

- Focus on Growth: Free up your team’s precious time and mental energy to pour back into what really matters—innovation, customer service, and expansion.

When you implement these kinds of solutions, you're not just improving your cash flow. You're building a foundation of predictable, reliable revenue that allows you to plan, invest, and manage your business with real confidence.

Frequently Asked Questions

It's natural to have questions about how modern fintech solutions work, especially when it comes to protecting your cash flow. Here are answers to some of the most common things business owners ask when looking to prevent payment defaults.

How Fast Can I Get Funds Through Invoice Discounting?

Speed is the whole point. Once your business is set up on the Comfi platform and your invoices are approved, the cash is typically in your bank account within 24 hours. This isn't a long, drawn-out process. It’s about turning your outstanding receivables into working capital you can use right away, solving immediate cash flow gaps almost instantly.

Do I Have to Chase Buyers for Payments with B2B BNPL?

Absolutely not—and that’s one of the biggest reliefs for our clients. When you use Comfi's Buy Now, Pay Later option, you get paid the full invoice amount upfront. From that moment on, the collections process is completely off your plate. Comfi manages the follow-up directly with your buyer based on the 30, 60, or 90-day terms they’ve selected, so you can focus on your business, not chasing payments.

What Happens If My Buyer Fails to Pay Comfi?

This is where the real peace of mind comes in. When you use a service like Comfi, the risk of a customer defaulting on their payment is transferred away from your business. You keep the money you received upfront, no matter what happens on the buyer’s end. This protection is a core part of the service, designed specifically to shield your revenue from bad debt and the unpredictability of credit risk.

Ready to build a default-proof business? Explore how Comfi can secure your revenue and help you grow with confidence at https://comfi.ai.

Related Reading

- B2B Payments

- Solve Creative Agency Late Payment UAE Issues

- How Payment Default Dents Small Business Growth and Survival

- A Guide to B2B Payment Solutions for MENA Businesses

Ready to improve your business cash flow? Get started with Comfi today.