SME Business Loan Options: A Guide to Merchant Cash Advance

You're probably here because your business looks healthy on paper, but cash is tight.

Orders are coming in. Customers are paying, just not fast enough. Payroll, stock, supplier terms, rent, and VAT cannot wait. That is when many owners start searching for an SME business loan and come across a fast-cash product called a merchant cash advance, or MCA.

An MCA can sound simple. Cash now, repayments linked to sales later. But simple does not always mean cheap or suitable. In the UAE and wider MENA market, that matters. A fast funding product can ease one pressure point while creating another in day-to-day cash flow.

This guide explains what an MCA is, how to calculate its real cost, where the risks sit, and when another option may fit better.

The SME Funding Challenge in MENA

A common SME story is straightforward. A distributor has a strong sales month, but two large customers pay late. At the same time, the supplier wants payment before shipping the next order. The business is not failing. It is stuck between selling and getting paid.

That gap is wider than many owners expect. In MENA, small and medium enterprises make up the backbone of the economy, but access to formal funding still lags. SMEs in the MENA region account for approximately 96% of all registered companies and roughly half of total employment, yet they receive only 7% to 8% of total bank lending. This has created a massive financing gap estimated at $210–$240 billion according to the World Bank's analysis of MSME finance constraints in MENA.

That is why many owners do not start with “What is the cheapest funding?” They start with “What can I get, and how fast?”

Why strong businesses still feel cash-poor

Revenue and cash are not the same. A business can be profitable and still feel squeezed because cash arrives late while expenses leave early.

A few examples:

- Wholesale businesses often pay suppliers before buyers settle invoices.

- Retail and trading firms may need to buy stock ahead of peak demand.

- Service companies can win contracts, then wait through approval and payment cycles.

Good funding should match the timing of your business, not just the size of your need.

That mismatch pushes many SMEs toward non-bank funding. Some options are built around invoices. Others are tied to buyer terms, inventory, or card sales. If you are trying to get finance for your business, the first step is not to grab the fastest product. It is to understand the problem you need to solve.

Where MCAs enter the conversation

A merchant cash advance often appeals when urgency is high. The business needs cash quickly, does not want a long underwriting process, or cannot access a standard bank facility.

But speed comes with trade-offs. To judge an MCA properly, you need to know what it is, how repayment works, and why the pricing often feels unclear.

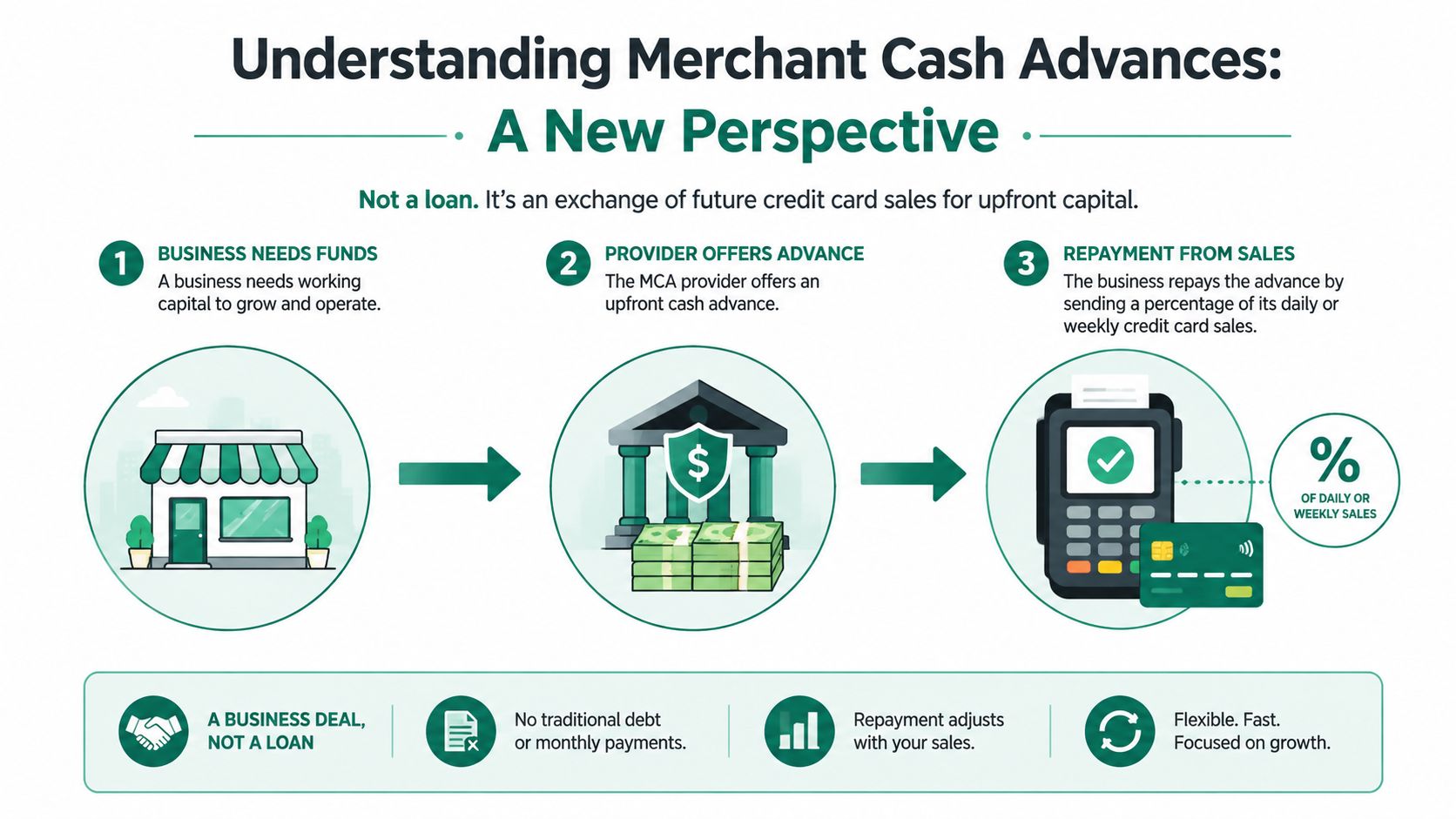

What Is a Merchant Cash Advance

A merchant cash advance is not a standard business loan. You receive money upfront, and the provider takes an agreed share of future sales until a fixed total amount has been collected.

It is like selling part of tomorrow's revenue so you can use the cash today.

The core mechanics

Most MCA offers have three moving parts:

- Upfront advance amount. The cash the business receives at the start.

- Factor rate. The multiple used to determine total payback. It is not an interest rate.

- Sales-based remittance. Repayment taken from a share of daily or weekly card sales, or through a scheduled collection method that follows that pattern.

The key difference from a typical SME business loan is that a loan usually quotes interest over time. An MCA usually quotes a factor rate, which tells you the multiple applied to the amount advanced.

Why the factor rate confuses people

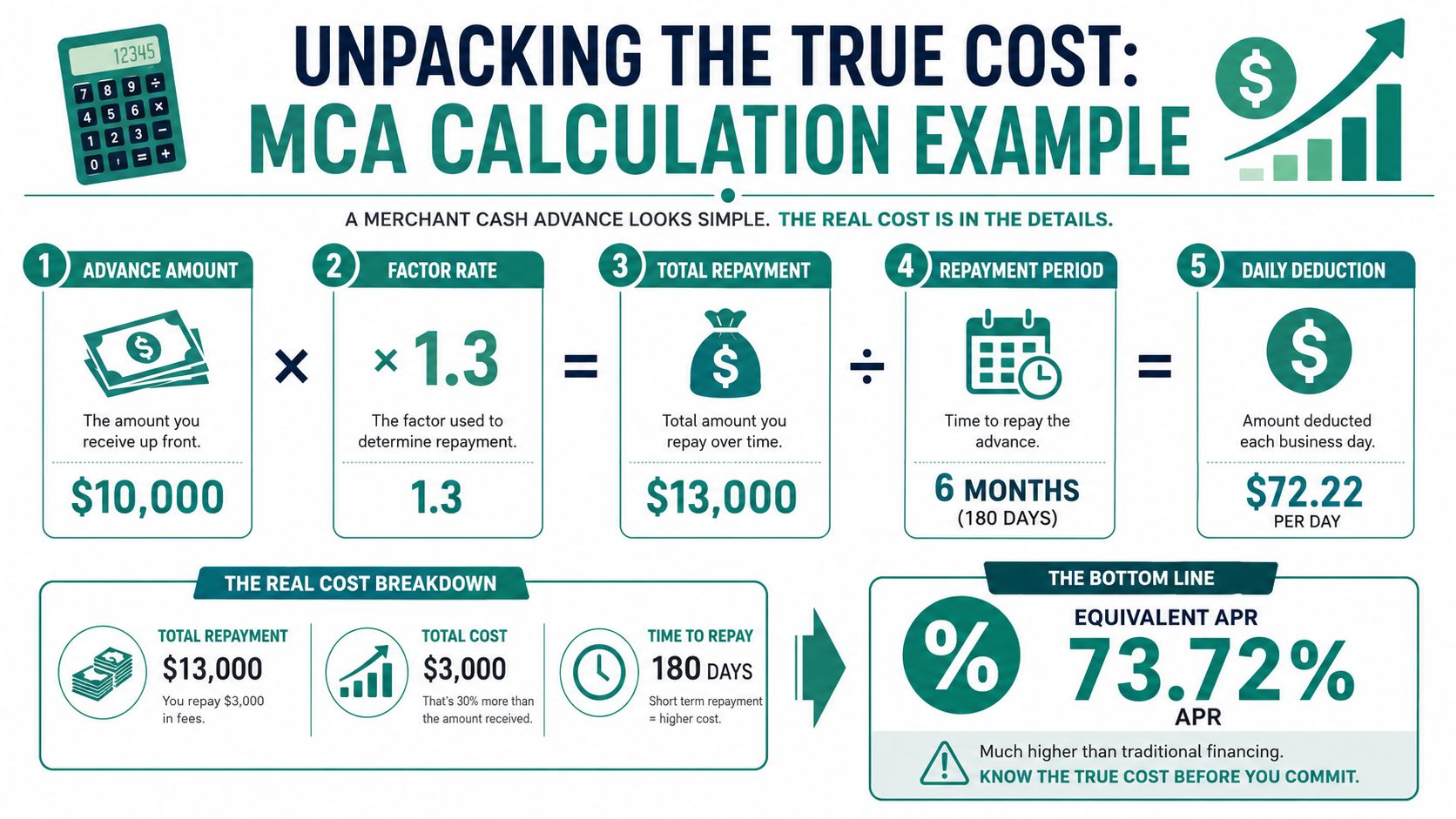

If a provider says the factor rate is 1.3, that does not mean 30% annual interest. It means you repay 1.3 times the amount advanced. If you receive 100,000 in local currency terms, you repay 130,000 in total.

That is why many owners underestimate the cost. A factor rate sounds simpler than a full annualised cost. It also hides a key point. If repayment happens over a short period, the effective annual cost can be much higher than it first appears.

If you cannot quickly identify the total payback amount, the product is not clear enough yet.

How repayment affects day-to-day trading

With an MCA, repayment often rises and falls with sales activity. On a strong sales day, the provider takes more. On a slower day, the deduction may be lower. That can help, but it also reduces the cash available for stock, wages, and supplier payments.

Owners often focus on approval speed and overlook the operating effect. The money arrives once. The deductions keep coming.

That is why it helps to think of an MCA as a revenue sale, not just fast cash. The real question is not “Can I get this?” but “Will this repayment rhythm fit my business?”

Calculating the Real Cost of an MCA

An MCA becomes much easier to judge once you stop looking at the marketing label and start doing the maths.

The provider may lead with the factor rate because it sounds tidy. But your business does not pay a factor rate. It pays a total payback amount, over a specific period. Those two facts matter most.

A simple example

Use this example in plain English:

- Advance amount: AED 100,000

- Factor rate: 1.3

- Total repayment: AED 130,000

The business receives AED 100,000 and agrees to repay AED 130,000. The extra AED 30,000 is the cost of getting the cash upfront.

Now add time:

- If repayment happens quickly, the annualised cost rises sharply.

- If deductions are taken daily or weekly, pressure on operating cash becomes more obvious.

- If sales dip, the business may still feel squeezed because part of future revenue is already committed.

Why APR still matters

APR gives you a common basis for comparison. It helps you compare an MCA with an overdraft, receivables-based funding, inventory-linked funding, or another SME business loan option.

Many MCA offers do not lead with APR. That does not mean you should ignore it.

Ask the provider:

- What is the full amount I will repay?

- Over what expected period?

- What is the equivalent APR if I compare it to other forms of finance?

- What fees sit outside the factor rate?

If a provider cannot answer clearly, pause.

Practical rule: Convert every offer into one number you can compare. Total payback first, equivalent annual cost second.

Don't ignore fees around the edges

The factor rate may not tell the whole story. Processing charges, admin charges, collection fees, or penalties can sit in the fine print. That is why it helps to understand how processing fees affect funding costs before signing anything.

A rushed decision often follows the same pattern. The owner sees quick approval, notices the headline factor rate, and assumes the rest is minor. Then deductions start, fees appear, and the funding that seemed manageable starts eating into the next trading cycle.

A better way to test affordability

Before accepting an MCA, run a simple stress test:

- Take your slowest recent sales period and estimate what deductions would have looked like then.

- List fixed outgoings such as wages, rent, freight, and supplier payments.

- Check whether the business still has enough room to trade normally after deductions.

- Ask what happens if sales weaken for a month or two.

If the numbers only work when everything goes right, the product is probably too tight.

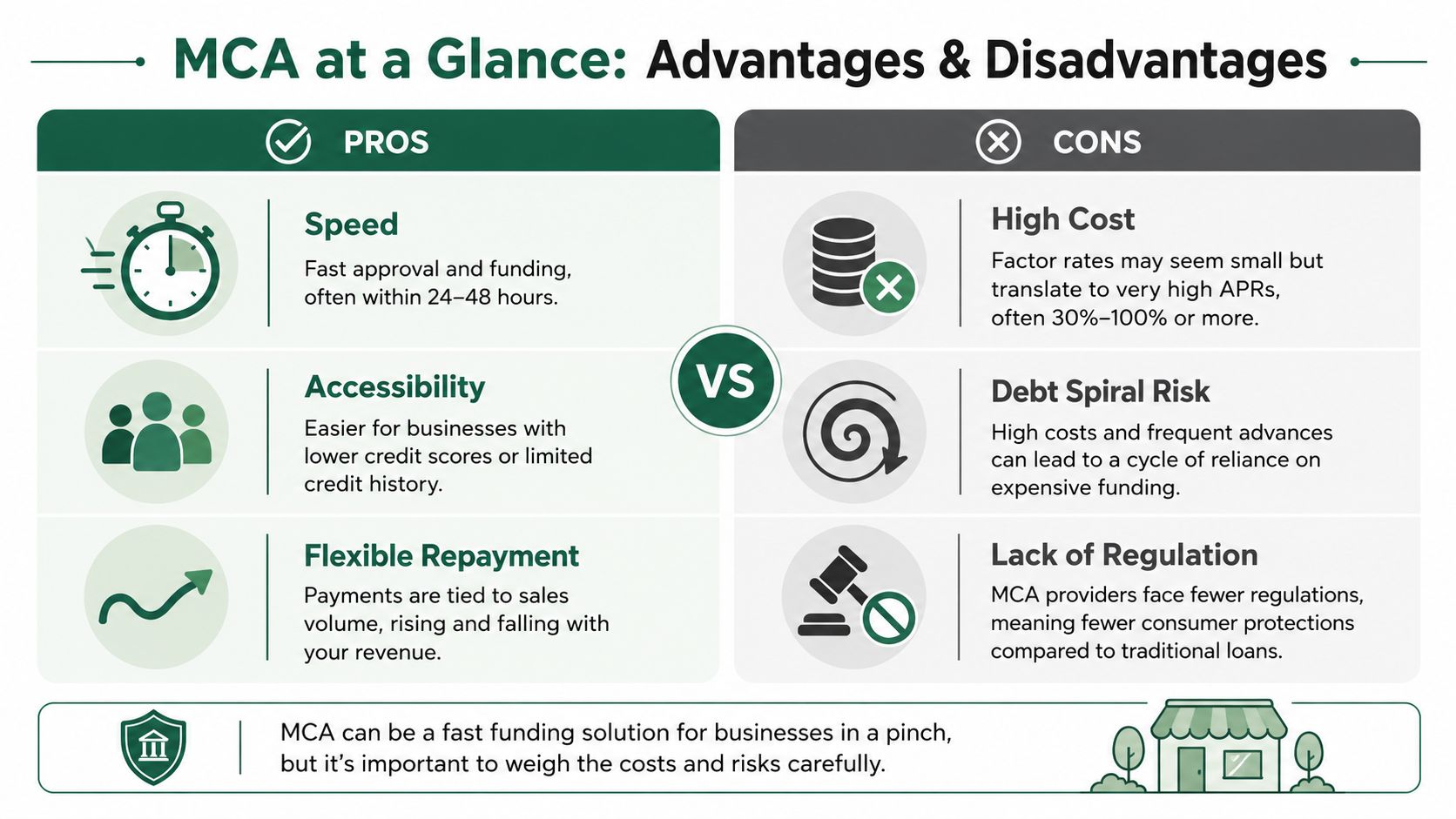

The Pros and Cons of a Merchant Cash Advance

An MCA exists because it solves a real problem. Some businesses need speed, cannot wait through a long bank process, and do not have the collateral or profile that traditional providers prefer. In that narrow use case, an MCA can be practical.

But useful is not the same as healthy.

Where MCAs can help

There are valid reasons owners consider them:

- Speed. Approval and access can be faster than a conventional facility.

- Accessibility. Businesses that struggle with bank criteria may still qualify.

- Repayment linked to sales. Some owners prefer a structure that moves with turnover rather than a fixed instalment.

For a short, urgent need, that can be appealing. If a profitable business faces a brief timing issue, an MCA may look like a bridge.

Where the risk shows up

The downside usually appears after the initial relief.

The first problem is cost. As the earlier example showed, the price can be much higher than it first seems once you translate the factor rate into a more familiar annual cost.

The second problem is cash flow drag. Daily or frequent deductions do not just reduce surplus cash. They can affect stock buying, marketing spend, supplier relationships, and your ability to absorb a slow week.

The third problem is repeat dependency. A business uses one expensive advance to cover a shortfall, then needs another because the first one already reduced operating breathing room.

Fast money can fix a timing problem. It can also turn a timing problem into a pattern.

Why SMEs get pulled toward high-cost products

The pressure behind MCA demand is easy to understand. Shell Foundation notes that SMEs in MENA often need “flexible patient capital with a longer time horizon”, while many available programmes still focus on small, short-term support, creating a missing middle in SME finance.

That gap matters because it pushes owners into products designed for urgency, not always for stability.

A balanced way to judge it

Use this lens:

- Good fit if the need is immediate, short-term, and tied to reliable sales.

- Poor fit if margins are thin, sales are volatile, or the business already feels stretched.

- Danger sign if you need the advance just to cover routine operating costs every month.

An MCA should not be judged only by how quickly cash arrives. Judge it by what the repayment pattern does to the next ninety days of trading.

The MCA Market in the UAE and MENA

The regional picture is mixed. Access to SME finance is improving in parts of the Gulf, but the gap has not disappeared. That creates space for both useful alternatives and risky offers.

There is real momentum in formal SME lending. In the UAE, SME financing reached 9.5% of total bank loans in H1 2024, and in Saudi Arabia MSME credit grew 22.6% year on year, while authorities are targeting 20% of bank loan portfolios for SMEs by 2030, according to this review of the GCC SME lending ecosystem.

That is encouraging. But many SMEs still face a fragmented market. Some providers are clear and structured. Others rely on urgency, weak comparison habits, and contract language owners do not have time to decode.

Red flags to watch for

If you are evaluating an MCA or similar fast-cash offer in the UAE or wider MENA market, watch for these warning signs:

- Pressure to sign quickly. A trustworthy provider explains the product. They do not rush you past the details.

- No clear total repayment amount. If you cannot see the full payback in writing, stop.

- Vague language about fees. Ask what sits outside the factor rate.

- No answer on early repayment. Some owners assume paying early lowers cost. That is not always true.

- Unclear collection method. You need to know exactly how money will leave your account and how often.

- Contract terms that punish ordinary volatility. Many SMEs have uneven sales cycles. The structure has to reflect real trading patterns.

What a safer evaluation looks like

A decent provider should be able to explain the product in plain language.

Ask them to show:

- Amount received

- Total amount repaid

- Expected repayment period

- Any additional charges

- What happens if sales slow down

- Whether renewal is likely to be needed to keep operations stable

If the answers are slippery, the offer probably is too.

Evaluating Alternatives to an MCA

The best funding choice depends on what is causing the squeeze. That is where many SMEs go wrong. They search for an SME business loan when the real issue is not “I need debt”. It is “my cash is stuck in the wrong place”.

If your cash is trapped in unpaid invoices

When customers take time to pay, the issue is often receivables. In that case, invoice-based options may fit better than selling future sales through an MCA. You are addressing a timing gap linked to actual invoices rather than carving out a share of upcoming revenue.

If that is your situation, it helps to understand how accounts receivable financing works for SMEs.

If buyer payment terms are slowing your growth

Some wholesalers and distributors do not have a collections problem. They have a customer conversion problem. Buyers want more time to pay, and the supplier does not want to stretch its own cash position to offer it.

That is a different problem with a different solution. A sales-enablement structure tied to buyer terms may fit better than an MCA because it supports transactions directly rather than placing a broad claim on future sales.

Match the product to the bottleneck. Do not use one expensive tool for every cash flow problem.

If stock is tying up your cash

Inventory-heavy businesses need another lens. In automotive, this is especially visible. In the UAE auto market, vehicles can sit in stock for up to 180 days, which locks cash into inventory and slows restocking, as explained on this overview of dealer financing for UAE automotive businesses.

For a dealer, an MCA may solve today's pressure but ignore the underlying issue, which is capital trapped in inventory. An inventory-linked solution is often more logical because it aligns with how the business trades.

Use outside guides to compare structures

If you want a broader view of available products before committing, Business Lending Blueprint's lenders guide is a useful primer on the main categories of small business funding. It will not replace detailed local advice, but it can help you sort products by purpose before provider conversations.

A practical way to choose

Use this quick matching framework:

- Late-paying customers: look at invoice or receivables-based options.

- Need to offer terms to buyers: look at payment-term solutions tied to transactions.

- Cash locked in stock: look at inventory or dealer-focused structures.

- Short-term emergency with dependable sales: an MCA may be considered, but only after full cost comparison.

That is the key point. An MCA is not bad by default. It is often just too blunt. Businesses usually do better when they choose a product that follows the source of the cash flow strain.

Why Comfi Can Be a Stronger Alternative

If the problem is unpaid invoices or buyers asking for terms, a targeted product is often stronger than a broad, high-cost cash advance.

That is where Comfi's two core products stand out:

- Invoice discounting helps you unlock cash tied up in unpaid invoices.

- Buy now, pay later for B2B helps you offer buyers 30, 60, or 90 day terms without carrying the cash flow burden yourself.

The difference is not just product structure. It is also cost clarity, approval speed, and how quickly money reaches the business.

1. Fees are clearer and easier to compare

One of the biggest problems with MCAs is pricing opacity. A factor rate can make the offer sound simple while hiding the real annualised cost, especially when repayment happens quickly.

Comfi positions both invoice discounting and B2B BNPL with a more transparent structure. According to Comfi, pricing is agreed upfront as a clear percentage of invoice value, with no hidden fees or processing charges. That makes it easier to compare the real cost with other options and judge margin impact before committing.

2. Approval is designed to be faster

When cash flow is tight, speed matters. But fast access only helps if the process is still predictable.

Comfi states that eligible UAE businesses can access a digital process with a 95% approval rate, provided they are UAE-registered, have operated for at least 6 months, and generate average monthly B2B revenue of AED 100,000 or more. That matters for SMEs that want faster decisions without moving into a product built around unclear pricing.

3. Time to money is built around trading reality

An MCA is fast because it pulls future revenue forward. Comfi's products aim to do the same more precisely, by funding the transaction or invoice that is already creating the squeeze.

Comfi says businesses can receive up to 100% of invoice value within 24 hours, often the same day. For businesses stuck in 30 to 90 day payment cycles, that can be a materially better fit than giving up a share of future sales across the business.

4. The product matches the bottleneck better

This is the strategic difference.

- If cash is trapped in receivables, invoice discounting is usually a cleaner solution than an MCA.

- If growth is being slowed by buyer payment terms, B2B BNPL can help you close sales while protecting your own cash position.

- If the issue is general short-term pressure with no clear transaction behind it, an MCA may still be considered, but only after a full cost comparison.

Comfi also argues that businesses using its products can reduce DSO and improve growth by turning slow-paying trade flows into working capital, rather than layering expensive deductions on top of daily trading activity, as outlined in its guides to invoice discounting and B2B payment terms.

The strongest finance option is usually the one tied closest to the source of the cash flow strain.

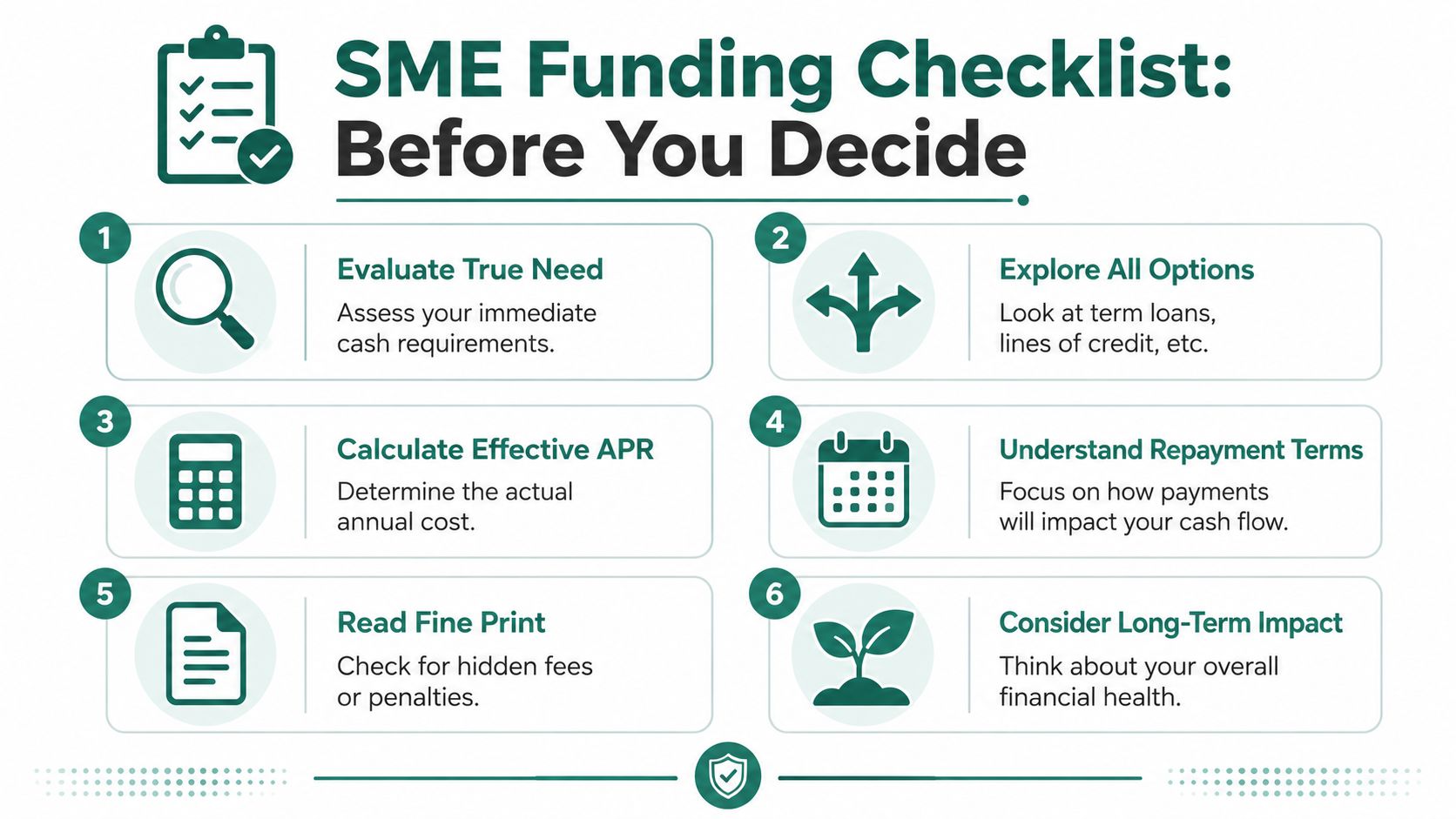

Your SME Checklist Before Choosing

A funding decision gets safer when every provider answers the same questions. That turns a stressful sales conversation into a comparison exercise.

Questions worth asking every provider

- What problem is this product designed to solve? If the answer is vague, the fit may be poor.

- How much cash will I receive, and how much will I repay in total? You need both numbers in writing.

- What is the equivalent annual cost? Even if the product uses a factor rate, ask for an annual comparison.

- How often is repayment collected? Daily, weekly, and monthly structures feel very different in practice.

- What happens if my sales slow down? Do not accept a generic answer.

- Are there extra fees, penalties, or charges outside the headline price? Fine print matters most when cash is tight.

- Does early repayment reduce my cost? Never assume it does.

- Will this help the business trade better next quarter, or just relieve this week's pressure? That is the true test.

One final reality check

In sectors where capital moves quickly, choosing the wrong structure has a visible cost. That is one reason product fit matters so much. The broader automotive finance market was valued at USD 295.13 billion in 2024 and is projected to reach USD 514.72 billion by 2032, according to this automotive finance market outlook. Large markets attract more products, more providers, and more complexity. Not every option is built for your business model.

The best funding product is the one that solves the cash bottleneck without creating a new one.

If you are comparing an MCA with another SME business loan option, slow down just enough to do the maths, test the repayment pattern, and match the structure to the underlying issue. That small pause can save a lot of pain later.

If your business needs a more specific method to access cash from invoices, buyer payment terms, or inventory, take a look at Comfi. It's built for SMEs in MENA that want a funding structure aligned to real trading activity, with a digital process designed to reduce cash flow bottlenecks rather than add new ones.