Finding the Right Lender: 7 Top Options for UAE SMEs

For small and medium-sized enterprises (SMEs) in the UAE and the wider MENA region, consistent cash flow is the lifeblood of growth. However, finding the right partner to help manage capital can be a complex task. The term lender often brings traditional banks to mind, but the financing landscape has evolved significantly. Today, a financial partner can be a bank, a fintech platform, a government-backed institution, or a specialised provider. Each offers a different approach to helping businesses manage their working capital and secure funds.

Understanding these differences is crucial for any finance leader looking to expand operations, purchase inventory, or simply bridge the gap between payables and receivables. This guide breaks down the various types of business financing available, explains what to look for in a financial partner, and provides a roundup of top options in the UAE, including innovative platforms like Comfi and established institutions like Emirates Development Bank (EDB). We will explore each option with clear explanations to help you make an informed decision for your business's needs.

1. Comfi: Embedded B2B Payments and Working Capital Solutions

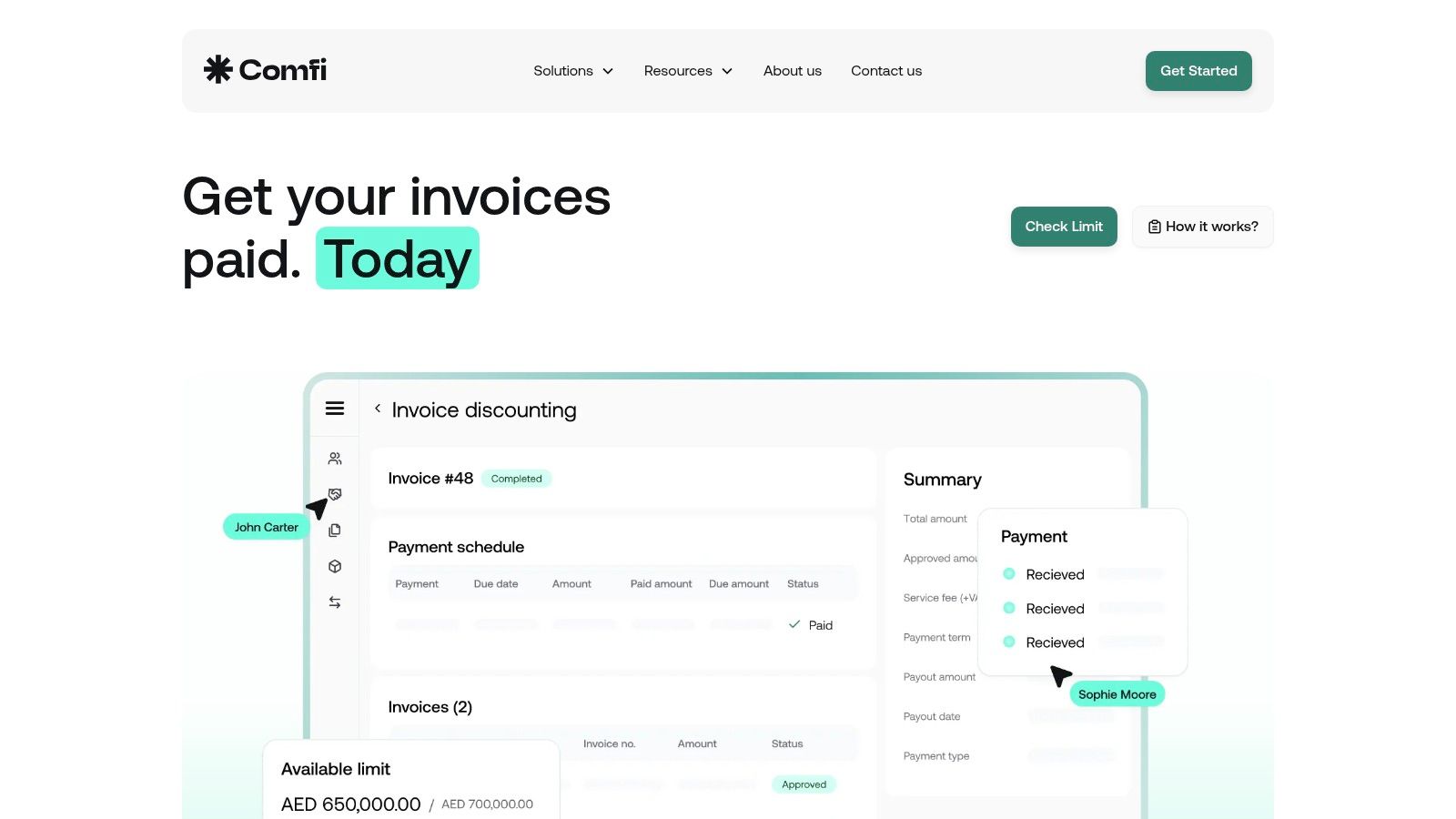

Comfi stands out as a premier fintech platform specifically designed to solve the cash-flow challenges faced by SME suppliers and wholesalers across the MENA region. Instead of acting as a traditional lender, Comfi facilitates upfront payments for suppliers by offering flexible payment terms to their buyers. This embedded payment model empowers businesses to improve their working capital, as clients were able to unlock their working capital and accelerate growth without taking on debt. The platform's core services are integrated directly into existing business workflows, making it a seamless solution for modern finance teams.

What makes Comfi a superior choice is its focus on measurable business impact and operational efficiency. The entire process is digital, from an instant eligibility check to a paperless setup, with approved invoices typically paid out within 24 hours. This speed is critical for SMEs needing predictable cash flow to seize growth opportunities. By handling collections, Comfi also removes the administrative burden and credit risk from suppliers, allowing them to focus on core activities. With a high approval rate of approximately 85% and strong social proof from over 1,000 supported SMEs, Comfi demonstrates a deep understanding of the regional B2B landscape. For an in-depth look at how different financial solutions compare, you can explore this guide on choosing a finance partner.

Key Strengths and Use Cases

Comfi's platform is engineered for immediate, practical benefits, making it an indispensable tool for finance leaders.

- Accelerated Cash Flow: Suppliers can get paid upfront for their invoices, while their B2B buyers enjoy flexible 30, 60, or 90-day payment terms. This unlocks working capital trapped in receivables.

- Increased Sales Volume: Case studies show that businesses using Comfi experience tangible growth, with clients reporting up to 30% larger order sizes and a 20% increase in new customers.

- Seamless Integration: The platform can be accessed via a user-friendly dashboard, low-code plugins, or a developer-friendly API. This flexibility allows it to connect directly with a company's ERP or checkout systems.

- Risk Mitigation: Comfi manages the entire collections process, which means suppliers are protected from buyer default and can forecast their revenue with greater certainty.

Website: https://comfi.ai

2. Beehive

Beehive is a UAE-based, DFSA-regulated peer-to-peer finance platform that connects businesses with investors. It specialises in digital working capital solutions and invoice discounting, making it an excellent choice for businesses looking to convert their accounts receivable into immediate cash flow. The platform is purpose-built for the regional market, offering a streamlined digital onboarding process complemented by human support.

What makes Beehive particularly attractive is its transparency. The platform clearly publishes its product details, including advance rates, timelines, and pricing bands. This clarity helps businesses make informed decisions without hidden surprises.

Key Features and Benefits

- Fast Funding: SMEs can receive funds within approximately 48 hours of approval, a crucial advantage for managing urgent working capital needs.

- High Advance Rates: Businesses can get up to 80% of their eligible invoice values, with tenors extending up to 120 days.

- Transparent Pricing: Beehive provides clear guidance on its rates, which start from 1.17% per month for working capital facilities.

- SME-Focused: The platform is designed with minimal paperwork and a quick application process, catering specifically to the fast-paced SME environment.

For services like Beehive's invoice discounting, robust and effective invoice tracking methods are essential for managing your receivables and optimising working capital.

However, keep in mind that facilities are tied to invoice performance, so early-stage firms with limited receivables may qualify for smaller amounts. As a regulated fintech platform, Beehive offers a secure and efficient route for SMEs to unlock liquidity, which you can compare with other alternative SME funding solutions.

Website: https://www.beehive.ae

3. Emirates Development Bank (EDB)

The Emirates Development Bank (EDB) is a pivotal federal institution established to drive the UAE's economic diversification and industrial growth. As a government-backed institution, it offers specialised financing solutions for small and medium-sized enterprises (SMEs) that are crucial to the national economy, with a focus on priority sectors such as manufacturing, advanced technology, and healthcare. Its primary goal is to bridge funding gaps for businesses that may struggle to secure financing from traditional commercial banks.

What makes EDB a unique lender is its Credit Guarantee Scheme (CGS), which significantly de-risks loans for its partner banks. By guaranteeing a large portion of the loan, EDB makes it easier for SMEs with limited collateral or operating history to get approved for financing, effectively expanding access to capital across the UAE.

Key Features and Benefits

- Credit Guarantee Scheme: EDB guarantees up to 85% for startup loans and up to 70% for existing SME loans, increasing approval likelihood.

- Priority Sector Focus: The bank offers favourable terms and dedicated programmes for businesses operating in sectors vital to the UAE's strategic development.

- Partner Bank Network: Its co-lending and guarantee model is delivered through a wide network of commercial banks, giving SMEs multiple access points for EDB-backed facilities.

- Digital Banking: The EDB 360 app provides a fully digital platform for businesses to open an account and manage their banking needs efficiently.

The government backing helps SMEs meet stringent requirements, which you can learn more about by reviewing common bank loan eligibility criteria.

However, it's important to note that access to these guaranteed facilities is typically managed through the partner banks, meaning processes and final pricing can vary. Eligibility is also targeted, so businesses outside the designated priority sectors might not qualify for all programmes.

Website: https://www.edb.ae

4. RAKBANK – Business Loans

RAKBANK is a well-established lender in the UAE, providing traditional banking solutions for small and medium-sized enterprises. The bank is a strong choice for businesses seeking conventional term loans, offering both standard and Sharia-compliant options. With a focus on relationship banking, RAKBANK combines digital servicing with dedicated support, making it suitable for SMEs that value guidance from a recognised financial institution.

Its direct approach to business loans caters to a wide range of capital needs, from expansion to operational funding. The bank's established presence provides a sense of security and reliability for businesses looking for a long-term banking partner.

Key Features and Benefits

- Flexible Loan Amounts: Offers unsecured business loans up to AED 3 million, providing significant capital for growth or operational expenses.

- Varied Financing Options: Businesses can choose between conventional and Islamic financing structures to align with their principles.

- Dedicated Support: Provides access to dedicated business banking support alongside a functional digital servicing app for account management.

- Established Reputation: As a prominent local bank, it has a deep understanding of the UAE market and the specific challenges SMEs face.

A key consideration is that pricing information like rates and fees is not publicly available and is determined after a full application and credit assessment. Depending on the business's credit profile and the loan amount, this lender may also require collateral or guarantees, which is a standard practice for traditional bank loans.

Website: https://www.rakbank.ae/en/business/business-finance/business-finance/business-loan

5. Commercial Bank of Dubai (CBD) – Business Banking

Commercial Bank of Dubai (CBD) is a well-established, full-service UAE bank offering a comprehensive suite of SME lending solutions. As a traditional lender, it provides everything from term loans and trade finance to working capital and asset-backed products. Its strength lies in its deep understanding of the local market and its ability to support businesses with diverse financing requirements through a combination of digital services and dedicated relationship managers.

A significant advantage of working with CBD is its strategic partnership with the Emirates Development Bank (EDB). This collaboration enables co-lending and guarantee programmes, which can improve an SME's eligibility for larger facilities, potentially up to AED 10 million, and secure more favourable terms.

Key Features and Benefits

- Diversified Lending Suite: Offers a broad range of products, including trade finance, working capital loans, term loans, and asset-backed financing to suit various business needs.

- EDB Partnership: The co-lending and guarantee arrangements with EDB enhance SME access to substantial funding, often with improved pricing and eligibility criteria.

- Blended Support Model: Combines the convenience of digital business account onboarding with the personalised guidance of an experienced relationship manager.

- Established Reputation: As a reputable UAE bank, CBD provides a trusted and reliable financing partnership for growing businesses.

It's important to note that specific pricing and rates are not publicly listed and are provided upon application and credit assessment. While CBD offers a robust digital platform, some site content may have geo-restrictions if accessed from outside the UAE, making it an ideal local lender for businesses operating within the region.

Website: https://www.cbd.ae/business

6. Tradeling

Tradeling is a prominent UAE-based B2B marketplace that uniquely integrates procurement with embedded buyer payment terms, positioning itself as a hybrid platform rather than a direct financial provider. It is an ideal solution for wholesalers, distributors, and suppliers who require inventory payment flexibility or wish to offer flexible payment terms to their buyers. The platform allows buyers to access 30, 60, or 90-day payment terms, while ensuring suppliers receive their payments promptly, bridging a critical cash flow gap in B2B transactions.

What makes Tradeling stand out is its one-stop-shop approach. It combines a vast digital marketplace with built-in payment solutions, simplifying the entire procurement-to-payment cycle. This model is particularly beneficial for businesses needing trade payment options to manage inventory levels effectively.

Key Features and Benefits

- Embedded Net Terms: Buyers can secure 30, 60, or 90-day payment terms and instalment options directly on the platform, while suppliers get paid quickly.

- Integrated Logistics: The platform offers end-to-end logistics and fulfilment services for the UAE and KSA, reducing operational complexity for both parties.

- One-Stop Procurement: It acts as a comprehensive B2B marketplace with built-in payment solutions, which is very helpful when payment flexibility is needed for inventory.

- Broad Buyer Base: Suppliers gain access to a large network of verified business buyers across the UAE, creating significant growth opportunities.

However, it's important to note that the payment flexibility is tied to purchases made on the Tradeling platform and isn't a general-purpose working capital facility. Eligibility and limits are also subject to approval and due diligence, with terms not fully published upfront.

Website: https://www.tradeling.com

7. FlapKap

FlapKap is a prominent revenue-based financing (RBF) provider headquartered in the UAE, catering to e-commerce, retail, trading, and F&B SMEs across the MENA region. This fintech company offers collateral-free advances that are repaid as a percentage of future revenues, making it an ideal partner for online merchants and fast-growing retailers needing to fund inventory and marketing without giving up equity.

What makes FlapKap unique is its alignment with a business's growth trajectory. The repayment model flexes with sales, easing the pressure during slower periods. Positioned as an equity-free and Sharia-compliant solution, it offers a modern alternative to traditional debt for digital-first businesses.

Key Features and Benefits

- Fast Funding Decisions: Merchants can receive funding offers in approximately 48 hours after connecting their sales channels (like Shopify or WooCommerce) and submitting the required documents.

- Tailored for E-commerce: The model is specifically designed for businesses with trackable online or card revenue, directly integrating with their sales data to determine funding capacity.

- Growth-Oriented Capital: The advances are intended to fuel growth activities such as inventory purchasing and marketing spend, helping businesses scale more rapidly.

- No Collateral or Equity: Unlike traditional lenders, FlapKap does not require hard assets as collateral or demand a share of ownership in the business.

This model is particularly effective for fast-growing merchants who may lack the hard collateral required by conventional banks. However, businesses should note that the effective cost can be higher than a standard bank loan, and its suitability is greatest for companies with consistent online or card-based revenue streams.

Website: https://www.flapkap.com

Top 7 Options Comparison

Here is a summary of the key features of each platform:

Comfi

- Implementation complexity: Low — digital dashboard, low‑code plugins, API

- Resource requirements: Minimal internal changes; invoice data or API integration

- Expected outcomes: Very fast payout (≈24h), offloaded collections, measurable revenue uplift (case studies)

- Ideal use cases: MENA SMEs, suppliers/wholesalers needing invoice discounting or BNPL

- Key advantages: Fast payouts, ~85% approval, handles collections, seamless integrations

Beehive

- Implementation complexity: Low — digital onboarding with human support

- Resource requirements: Invoices/receivables, standard documentation; DFSA compliance

- Expected outcomes: Funds typically within ~48h, advance rates up to ~80% of eligible receivables

- Ideal use cases: GCC SMEs with receivables needing transparent invoice finance

- Key advantages: Published rate guidance, clear product terms, DFSA‑regulated

Emirates Development Bank (EDB)

- Implementation complexity: Medium — via partner banks and program processes

- Resource requirements: Business plan, partner‑bank application, program eligibility

- Expected outcomes: Improved loan access, guarantees up to 85% (startup), longer tenors (up to 10 years)

- Ideal use cases: UAE SMEs in priority sectors needing guaranteed loans or lower collateral

- Key advantages: Government‑backed guarantees, co‑lending network, reduced collateral barriers

RAKBANK – Business Loans

- Implementation complexity: Medium — bank application and credit review

- Resource requirements: Financial statements, possible collateral or guarantees

- Expected outcomes: Term/unsecured loans up to AED 3M, flexible tenors, relationship banking

- Ideal use cases: SMEs seeking conventional or Sharia‑compliant term financing

- Key advantages: Established SME lender, Islamic & conventional options, digital servicing

Commercial Bank of Dubai (CBD) – Business Banking

- Implementation complexity: Medium — bank processes; EDB partnership options

- Resource requirements: Documentation, credit assessment, possible partner guarantees

- Expected outcomes: Broad SME lending (trade, working capital, asset finance), financing up to ~AED 10M with EDB support

- Ideal use cases: SMEs needing trade finance, asset‑backed loans, or larger facilities

- Key advantages: Diversified product suite, EDB co‑lending improves eligibility/pricing

Tradeling

- Implementation complexity: Low–Medium — marketplace onboarding, platform dependency

- Resource requirements: Active marketplace sales, transaction data, platform eligibility

- Expected outcomes: Buyers can access 30–90 day net‑terms; suppliers get prompt payment on platform sales

- Ideal use cases: Wholesalers, distributors and suppliers using B2B marketplace for procurement payment flexibility

- Key advantages: Integrated procurement + payments, built-in logistics, one‑stop-shop

FlapKap

- Implementation complexity: Low — connect sales channels (Shopify, gateways)

- Resource requirements: Online/card revenue channels, sales data; minimal collateral

- Expected outcomes: Quick advances (decision ≈48h), revenue‑tied repayments, growth capital for inventory/marketing

- Ideal use cases: E‑commerce merchants and retailers with card/online revenue

- Key advantages: Revenue‑based, collateral‑free, fast decisions, equity‑free option

How to Choose the Right Financial Partner for Your Business

Selecting the right financial partner is a strategic decision that goes far beyond simply securing capital. It’s about identifying a solution that aligns with your specific business model, supports your growth trajectory, and integrates smoothly with your daily operations. The MENA region offers a diverse landscape of options, from the established security of traditional banks like EDB and RAKBANK to the agile, tech-driven solutions provided by fintech innovators like Comfi and Beehive.

The key takeaway is that no single type of lender or financial partner is universally best. A large, asset-heavy enterprise might benefit from a conventional bank loan for a major capital expenditure. In contrast, a fast-growing e-commerce supplier will likely prioritise speed and flexibility, making digital platforms offering embedded payment terms or invoice discounting a more suitable choice. The decision hinges on a careful evaluation of your immediate needs and long-term goals.

Your Actionable Next Steps

To make an informed choice, start by assessing your requirements for speed, flexibility, collateral, and overall cost.

- For immediate working capital needs: Explore invoice-based payment platforms or B2B BNPL providers that can unlock cash tied up in receivables within days, not weeks.

- For large, planned investments: Engage with traditional banks or government-backed institutions that offer structured loans with competitive rates for significant projects like factory expansions or major asset purchases. When evaluating various financial partners, a comprehensive guide to equipment financing options can provide valuable insights into specific asset-based lending available for businesses.

- For enhancing sales and customer experience: Consider how embedded payment solutions can be integrated directly into your sales process, offering your buyers flexible terms without straining your own cash flow.

Ultimately, the ideal financial partner acts as a true enabler of growth. By understanding the distinct advantages of each type of lender and financial solution, you can forge a partnership that not only funds your business but actively accelerates its success in the competitive regional market.

Ready to offer flexible payment terms and get paid instantly without the complexity of traditional financing? Discover how Comfi can embed seamless B2B payment solutions directly into your checkout, helping you boost sales and improve cash flow. Learn more at Comfi.