A Guide to Bank Loan Eligibility for SMEs in the UAE

Getting a bank loan can feel like trying to solve a complex puzzle, especially for SME owners and finance managers in the MENA region. The first and most crucial piece of that puzzle is understanding bank loan eligibility.

What Do Banks Really Look for in the MENA Region?

Think of a loan application less like filling out a form and more like a comprehensive interview. The bank wants to understand the complete story of your business's health to feel confident about its future.

At its heart, this is all about risk management for the lender. They need assurance that they’ll get their money back, plus interest. To get that confidence, they dig into every corner of your company’s financial and operational stability. It’s never about one single number; it's about the entire narrative your business tells.

The Core Areas Banks Scrutinize

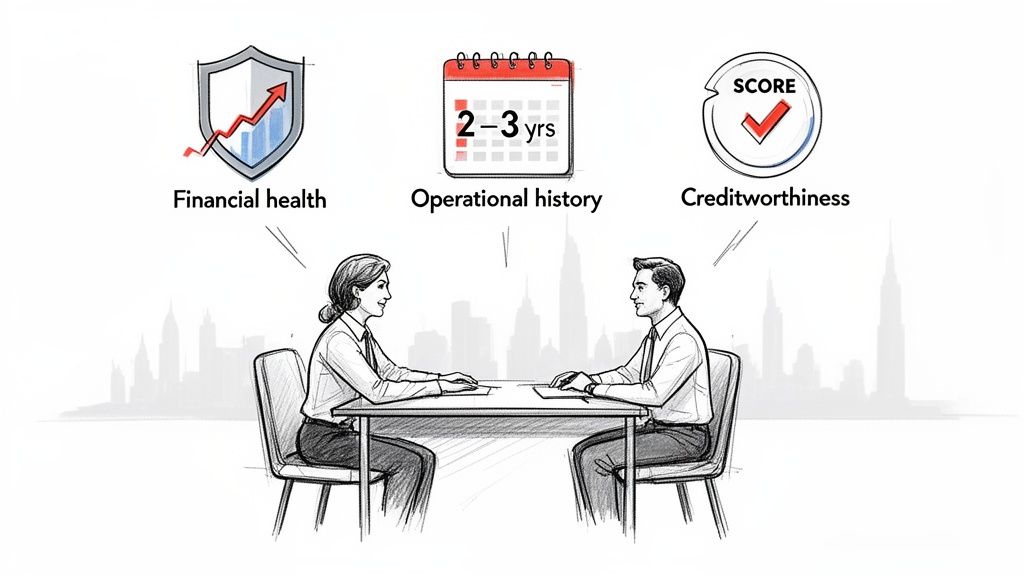

To make sense of the bank’s perspective, it helps to know the three foundational areas they will almost certainly investigate before making a decision.

- Financial Stability: This is a deep dive into your numbers—revenue, profits, and most importantly, cash flow. Banks need to see consistent, predictable income and solid proof that you can handle your daily expenses on top of a new loan repayment.

- Operational History: Lenders are naturally cautious. They prefer businesses with a proven track record, which is why an operational history of at least two to three years is often a baseline requirement. It demonstrates stability and lowers the perceived risk of backing a new, unproven venture.

- Creditworthiness: This is all about your track record. Your history of repaying past debts is one of the strongest predictors of how you'll handle future obligations.

In the UAE, your credit score from the Al Etihad Credit Bureau (AECB) is a make-or-break factor. Lenders rely heavily on these reports, which track both your company's and your personal debt and repayment history, to assess risk before moving forward.

The unique dynamics of the MENA region add another layer to this process. For instance, with a large expatriate population in the UAE, banks often place extra emphasis on residency status and the stability of the owner's personal finances alongside the business's performance.

Getting these regional nuances right is what separates a strong application from a weak one. For a broader look at the SME funding landscape, check out our complete guide on small business lending. Ultimately, success comes down to preparing your business to confidently answer the bank's one fundamental question: "Is this a safe investment?"

The Core Pillars of SME Loan Eligibility

When you approach a bank for a loan, it helps to know exactly what they're looking for. While every bank has its own rulebook, they almost always build their decision on four foundational pillars. Getting these right is non-negotiable.

Think of your loan application like building a house. If any one of your foundations is weak, the whole structure is at risk. By understanding what the bankers across the table are evaluating, you can build a much stronger case. It's crucial to understand what banks truly look for when a small business applies for a loan before you even start the paperwork.

Financial Health and Performance Ratios

This is where your numbers have to tell a good story. Banks will pour over your financial statements to get a clear picture of your company's health. They want to see consistent profitability and smart financial management.

A few key metrics they’ll zoom in on include:

- Profitability Ratios: Are you consistently making more than you spend? Your profit and loss statements need to show a stable history of turning a profit. It’s a huge green flag for them.

- Liquidity Ratios: This is all about your ability to cover your short-term bills. A healthy current ratio (your current assets divided by your current liabilities) proves you have the cash on hand to manage immediate debts without breaking a sweat.

- Debt-to-Income (DTI) Ratio: This one is critical. It shows how much debt you're already carrying compared to your income. If your DTI is high, it signals that your cash flow is already stretched, leaving little room for another loan payment.

Here’s a quick summary of the main criteria banks in the region focus on, giving you a clear snapshot of what they're looking for and the typical benchmarks you should aim for in the UAE.

Key Eligibility Criteria at a Glance

- Financial Health: Banks look for consistent profitability, positive cash flow, and healthy liquidity. A typical benchmark is a positive net profit for the last 2 years and a Debt-to-Income ratio below 40%.

- Credit History: Lenders expect a strong Al Etihad Credit Bureau (AECB) score with no history of defaults or late payments. An AECB score of 650 or higher is often the minimum requirement.

- Business Age: A proven track record of operations and market stability is essential. The benchmark is a minimum of 2-3 years of continuous operation.

- Sector Risk: Banks assess whether you are operating in a stable or high-growth industry with predictable revenue streams. They see lower risk for sectors like healthcare and tech, with higher scrutiny for construction and hospitality.

Having these benchmarks in mind helps you see where you stand before you even submit an application, allowing you to focus on strengthening any weaker areas.

Credit History and Reputation

Your company's financial past is the best predictor of its future behavior, at least in a lender's eyes. In the UAE, your credit history is a massive deal because it shows you can be trusted to pay people back.

The single most important document here is your Al Etihad Credit Bureau (AECB) report. This report is a complete summary of your credit life—past loans, how timely your payments were, and any outstanding debt. A high AECB score is a must-have for most banks. It doesn't just get you approved; it can also get you a better interest rate.

Even a couple of late payments can drag your score down, so a perfect payment record is something you should guard fiercely. It proves you're reliable.

Business Age and Stability

Lenders don't like surprises; they prefer backing businesses that have already made it through the tough early years. Most banks in the UAE won't even look at a loan application unless the business has been running for at least two to three years.

This isn't just an arbitrary number. A few years in business gives the bank a decent amount of financial data to analyze. They can see trends in your revenue, your profits, and how you manage cash. A business that has survived and grown for several years has proven it has a place in the market and knows how to run its operations, making it a much safer bet.

Industry and Sector Risk

The final piece of the puzzle is something you can't always control: the industry you're in. Banks look at the overall health and stability of your sector. A business in a booming, predictable industry like healthcare or tech might get an easier ride than one in a volatile or seasonal market, like retail during certain times of the year.

For example, a software-as-a-service (SaaS) company with predictable, recurring monthly revenue is a very different risk from a construction firm that gets paid in big, irregular chunks based on project completion. Banks have their own internal risk ratings for different sectors. Knowing how your industry is viewed can help you prepare for the tough questions they might ask about potential risks.

Essential Documents for Your Loan Application

Pulling together all the paperwork for a loan application can feel like a real chore, but this is one of the most critical stages in the entire process. Don't think of it as just busywork. Think of your documents as the hard evidence that proves the strong financial story you're telling the bank. When you present a complete, organized, and professional set of papers, it sends a clear signal: you run a tight ship.

This isn't just about ticking boxes on a checklist. Each document gives the lender a specific insight into your business's health, stability, and future potential. Getting this right from the start makes everything smoother, which is why adopting solid document management best practices is so important for keeping your essential paperwork in order.

Your Business Financial Story

This first batch of documents is all about the numbers. They prove your company’s financial health and, most importantly, its ability to repay the loan. These are absolutely non-negotiable and will be the first thing any lender scrutinizes.

- Audited Financial Statements: You'll typically need to provide these for the last two to three years. This includes your Profit & Loss (P&L) Statement, which shows your profitability, and your Balance Sheet, which gives a snapshot of your assets and liabilities.

- Bank Statements: Get ready to hand over 6 to 12 months of your company's bank statements. Lenders pour over these to verify your revenue claims and analyze your day-to-day cash flow, looking for healthy balances and consistent activity.

- Cash Flow Projections: This is your chance to look forward. A solid projection shows how you expect cash to move through your business in the future. It’s your way of demonstrating that you have a clear, credible plan to handle the loan repayments.

Legal and Company Formation Documents

Next, you need to prove your business is a legitimate, legally compliant entity operating by the book in the UAE. Any missing or outdated documents here are a massive red flag that can stop an application in its tracks.

Here are the key items you'll need:

- Valid Trade Licence: This is your official permission to operate. An expired license is an immediate deal-breaker.

- Memorandum of Association (MOA): This is the foundational legal document that outlines your company’s purpose, ownership structure, and rules of operation. You can learn more about why a well-structured Memorandum of Association is so crucial in our detailed guide.

- Shareholder Register: A straightforward list of all company owners and their respective shares.

- Power of Attorney: If someone is applying on behalf of the company, this document is required to prove they have the legal authority to sign the dotted line.

In the UAE, lenders are laser-focused on an SME's ability to prove repayment capacity through clear and thorough documentation. It's no surprise when you consider that private sector credit makes up 74% of all loans. With traditional banks approving around 70-80% of applications from low-risk SMEs, it’s obvious that having your paperwork in perfect order is essential.

Personal Documents of Owners and Signatories

Finally, banks need to know who is behind the business. This is a standard part of their Know Your Customer (KYC) compliance and is taken very seriously. For all partners or owners holding more than a 25% stake in the company, you'll need to provide the following:

- Passport and Visa Copies: Clear, valid copies are required for every major shareholder.

- Emirates ID Copy: A fundamental piece of identification for anyone residing in the UAE.

- Personal Bank Statements: Lenders often ask for the last six months to get a sense of an owner's personal financial stability.

- AECB Credit Report: Both the company's and the primary owners' credit reports will be pulled and reviewed carefully.

Common Reasons for Loan Rejection and How to Avoid Them

Getting a loan application rejected is frustrating, but it’s not the end of the road. Think of it less as a final "no" and more as a detailed report card from the bank. It tells you exactly which parts of your business need shoring up before you try again.

Most rejections boil down to a few common red flags that signal risk to a lender. By understanding what they are and tackling them head-on, you can turn a setback into a learning opportunity and dramatically improve your chances next time around.

Weak or Inconsistent Cash Flow

The first question every lender asks is simple: "Can this business actually afford the monthly payments?" If your bank statements are a rollercoaster of highs and lows, with frequent overdrafts and low average balances, it screams instability. Lenders need to see a steady, predictable stream of cash to feel confident.

An unhealthy cash flow is probably the number one deal-breaker. Before you even think about applying, get your financial house in order.

- Get Paid Faster: Tighten up your invoicing terms and be relentless about following up on overdue payments. You could even offer small discounts for early payments to get cash in the door quicker.

- Manage Your Own Bills: See if you can negotiate better payment terms with your suppliers. Stretching out your payables, even by a few weeks, can make a huge difference in smoothing out your cash flow.

- Keep a Buffer: Always maintain a healthy cash reserve in your account. It shows you’re a prudent manager who can handle unexpected costs without missing a loan payment.

A Poor or Limited Credit History

In the UAE, your Al Etihad Credit Bureau (AECB) score is a huge piece of the puzzle. A low score, usually the result of late payments or past defaults, is a massive warning sign. It tells the bank you’ve had trouble meeting your financial commitments before, making you a higher-risk bet.

It’s not just about a bad history, either. A short history can be just as tricky. If your business is brand new, lenders have no track record to judge you by, making it hard for them to assess your reliability. Building a good credit history is a long game, but it’s one you have to play. Always pay your suppliers and any existing debts on time, every time.

High Debt Burden and Too Much Leverage

You could have fantastic revenue, but if your business is already weighed down by a lot of debt, banks will be reluctant to pile on more. Lenders look closely at your debt-to-income (DTI) ratio. If too much of your income is already going toward paying off existing loans, there might not be enough breathing room to safely cover a new one.

A high DTI ratio tells a lender your business might be overextended and vulnerable. A small dip in your revenue could be all it takes to make repayments impossible, and that’s a risk they’re not willing to take.

Before you apply for new financing, focus on paying down your existing high-interest debts. Lowering your overall debt doesn’t just improve your DTI ratio; it also frees up cash flow, making your application look much stronger.

An Unclear Business Plan or Use of Funds

Lenders aren’t just backing your business; they’re backing your plan. If your application is vague about how you’ll use the money and what the return will be, it creates doubt. Saying the loan is just "for business growth" won't cut it.

You need to be specific and back it up with numbers.

- State the Purpose: Are you buying new machinery? Expanding your inventory? Launching a major marketing campaign? Spell it out clearly.

- Show the ROI: Provide realistic financial projections that show how this investment will boost your revenue or cut your costs. For example, if you’re buying a new machine, show how it will increase your production capacity and lead to X amount in new sales.

- Prove Your Projections: Your forecasts can’t be pulled out of thin air. They should be grounded in solid market research and your own past performance to show your plan is credible and achievable.

A strong, detailed business plan gives the lender confidence that you’re a strategic operator and that their money will be used wisely to make the business stronger—which is the best guarantee they’ll get it back.

A Step-by-Step Guide to Improving Your Loan Eligibility

Getting your business ready for a bank loan isn’t something you do overnight. It’s a long-term commitment to rock-solid financial discipline. You're not just filling out a form; you're building a convincing case that proves your business is a reliable, low-risk partner for any lender.

Think of it like training for a marathon, not a sprint. Every smart financial move you make today builds the stamina that banks are looking for.

Step 1: Get Obsessed with Your Credit Report

In the UAE, your Al Etihad Credit Bureau (AECB) credit report is the single most important document in your loan application. It’s the first thing lenders look at to gauge your creditworthiness. Any mistakes on that report can kill your application before it even gets off the ground.

Make a habit of pulling your report at least once a quarter. Scour it for errors—things like incorrect payment statuses or debts that aren’t yours—and dispute them immediately. For lenders, a clean, accurate report with a strong score isn't a "nice-to-have"; it's non-negotiable.

Step 2: Master Your Cash Flow

Strong, consistent cash flow is the heartbeat of your business. It’s also the clearest signal to a lender that you can actually handle loan repayments. They will go through your bank statements with a fine-tooth comb to see how well you manage your money day-to-day.

Here are a few practical things you can do right now to get your cash flow in shape:

- Invoice Immediately: Don't wait. Send invoices the moment a job is done and have a system for chasing down overdue payments.

- Reward Early Payers: Offer a small discount, maybe 2%, for clients who settle up within 10 days. It can work wonders.

- Manage Your Own Bills: Try to negotiate longer payment terms with your suppliers. This helps line up your cash outflows with your inflows much more effectively.

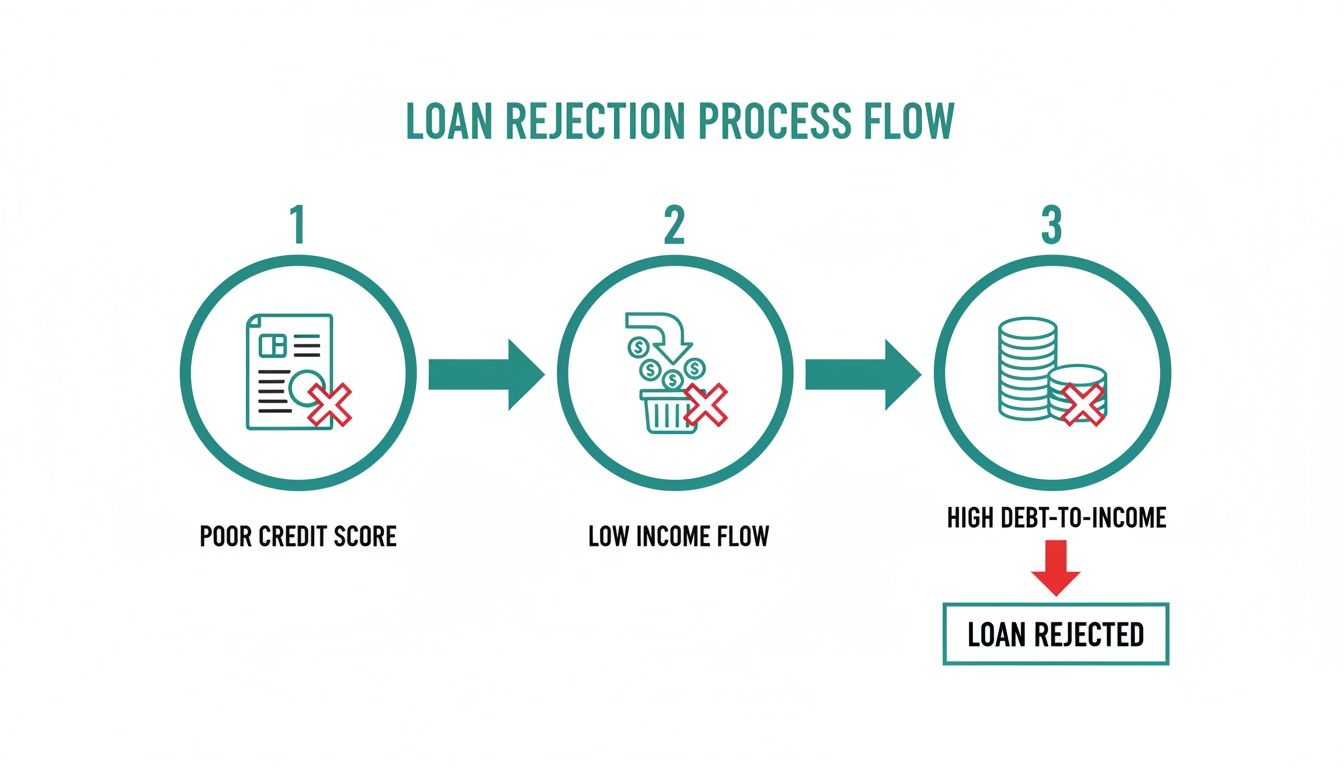

This flowchart breaks down the common reasons a loan gets rejected. Poor credit, weak cash flow, and too much existing debt are the big three.

Getting these three areas right is fundamental. They form the core of how any lender will assess your risk.

Step 3: Lighten Your Existing Debt Load

A lender will always look at the debt you're already carrying to figure out if you can realistically take on more. If your debt-to-income ratio is high, it sends a clear signal: your cash is already spoken for, leaving very little wiggle room.

Before you even think about applying for new financing, make it a priority to pay down existing high-interest debts. That means tackling credit card balances or any other expensive short-term loans first. Cutting your overall debt shows you’re a savvy financial manager and frees up cash flow—making your application look a whole lot stronger.

UAE SMEs are navigating an environment where bank loan eligibility is increasingly shaped by AECB credit reports and proven operational stability. For many businesses in sectors like F&B and retail, key benchmarks include operating for at least two years and having an AECB score above 600. Focusing on these metrics is crucial in a market that saw loan growth hit 17.10% in November, showing strong lender appetite for well-qualified firms. Discover more insights about the UAE personal loan market.

Step 4: Write a Business Plan That Sells

Your loan application needs a story—a clear and convincing one. Lenders need to know exactly how you'll use their money and, more importantly, how that investment will generate the returns needed to pay them back. A vague request for "growth capital" is a huge red flag.

Your business plan has to be detailed and backed by data:

- Be Specific About the Funds: Clearly spell out what you’re buying. Is it new machinery? More inventory? A targeted marketing campaign?

- Show Them the ROI: Back it up with realistic financial projections. How will this investment boost revenue or cut costs? For example, "This new machine will increase our production capacity by 40%, leading to an estimated AED 200,000 in additional annual revenue."

A well-researched plan tells the bank you’re a strategic thinker and gives them the confidence that their money is in good hands.

What to Do When the Bank Says No (Or Takes Too Long)

Let's be honest, even with a flawless application, a traditional bank loan isn't always the right move for an SME. The painfully slow approval process and rigid checklists can be a huge roadblock, especially when a great opportunity lands on your desk and you need to act fast. Thankfully, you're not out of options. Modern financial solutions offer a completely different path—one built for speed and flexibility.

These alternatives aren't just a plan B; they're smart, strategic tools designed for how businesses actually operate today. They shift the focus away from a bank's obsession with years of profitability and physical collateral. Instead, they look at the real-time strength of your business, like the value locked up in your outstanding invoices.

Unlock Cash from Invoices with Invoice Discounting

One of the most powerful ways to get your cash flow moving is invoice discounting. Think about it: all that cash just sitting in your unpaid B2B invoices is your money. Instead of waiting 30, 60, or even 90 days for clients to pay up, you can get a huge chunk of that cash right now.

It’s surprisingly simple:

- You send an invoice to your customer, just like you always do.

- You show that invoice to a provider like Comfi.

- They advance you a large percentage of the invoice's total value, often within just 24 hours.

- When your customer pays the invoice on the due date, you get the rest of the money, minus a small, transparent fee.

This isn’t about taking on long-term debt. It’s about unlocking the working capital you’ve already earned. It's a solution that scales directly with your sales—the more you sell, the more cash you can access.

Specialized Tools like Dealer Financing

For certain industries, the solutions get even more specific. Take dealer financing, for example. It's built from the ground up to solve the unique inventory and cash flow challenges of businesses in the automotive sector. It provides access to capital needed to fill a showroom floor, ensuring dealers never miss a sale because they couldn't get the right vehicles in stock.

The real game-changer with these modern solutions is their totally different view on bank loan eligibility. Instead of digging through years of old financial statements, they look at the quality of your customer invoices or your role in the supply chain. This fresh perspective opens doors for countless strong businesses that just don’t fit the old-school banking mold.

Comfi is built to deliver these kinds of solutions with a focus on speed and simplicity. With a straightforward digital process and approval rates hitting as high as 85%, SMEs can get a decision in a matter of hours, not weeks. This allows you to manage your cash flow strategically and jump on growth opportunities when other avenues are either closed or just too slow.

If you're interested in exploring this further, our deep dive on alternatives to traditional SME loans is a great next step.

Your Top Questions About Bank Loan Eligibility, Answered

Getting a handle on bank loan eligibility can feel like trying to hit a moving target. To cut through the noise, we've gathered the most common questions we hear from SME owners and finance managers across the UAE and put together some straight, practical answers.

How Long Does the Bank Loan Approval Process Take?

Let's be realistic: getting a bank loan approved in the UAE is rarely a fast-track process. From the moment you submit your complete application to the day the funds actually land in your account, you should brace for a timeline of anywhere from four to eight weeks.

Several things can stretch out this timeline:

- Application Completeness: A single missing document or an unchecked box is the number one cause of delays. Banks simply won't move forward until every piece of the puzzle is in place.

- Loan Complexity: A simple working capital loan will almost always get processed faster than a large, complex request for project financing, which demands a much deeper level of due diligence from the lender.

- Bank Workload: Just like any other business, banks have their busy seasons. The approval speed can sometimes come down to their internal capacity and how many applications are in their queue.

Can a New Business Get a Bank Loan?

Securing a traditional bank loan for a business that's less than a year old is, to put it bluntly, next to impossible. The vast majority of banks in the UAE have a hard rule: your business must be operational for at least two to three years before they’ll even consider your application.

The logic behind this is all about risk. Lenders need to see a proven track record of consistent revenue, profitability, and stable cash flow to feel confident you can repay the loan. A new business just doesn't have that history. Without years of financial statements and a credit history to analyze, the perceived risk is simply too high for most conventional lenders.

While a bank loan might be off the table for startups, this is exactly where alternative solutions come into their own. They often look at different metrics—like the strength of your customer invoices—which can give young, healthy businesses the capital they need to fuel their growth.

Does a Previous Loan Rejection Affect Future Eligibility?

A past rejection isn't a permanent black mark, but it does leave a footprint. When you apply for a loan, the bank pulls your credit file, and that inquiry gets logged on your AECB report. A cluster of inquiries in a short time can slightly ding your credit score, as it might signal to lenders that you're in financial distress.

What matters more, however, is why you were rejected. If it was for something fixable—like incomplete paperwork or a temporary dip in cash flow—and you’ve since corrected the issue, your odds are much better the next time. The best approach is to treat that rejection as valuable feedback. Understand the weaknesses in your application and fix them before you approach another lender.

What Is the Minimum Turnover for an SME Loan?

There’s no single, universal number for minimum annual turnover, as it really varies from one bank to the next and depends on the specific loan product. That being said, a common unofficial benchmark for many SME loans in the UAE is an annual turnover of at least AED 1 million. For smaller loan amounts or specialized programs, some banks might look at businesses with turnovers starting from AED 500,000.

But remember, turnover is only part of the story. Banks are far more interested in your profitability and actual cash flow. A business with an AED 3 million turnover but razor-thin profit margins could easily be seen as riskier than a business with an AED 1.5 million turnover and a healthy, consistent profit.

When the hurdles of traditional bank loan eligibility are slowing you down, you need a partner built for speed and flexibility. Comfi provides modern financial tools like Invoice Discounting that help you unlock the cash tied up in your unpaid invoices, often within 24 hours. Stop waiting on slow approvals and start putting your working capital to use today. Learn more at https://comfi.ai.

Related Reading

- Your 2026 Guide to the 11 Best SME Business Loan Options in the UAE

- Finance Lender: How to Choose the Right Partner for SMEs

- 7 Faster Alternatives to a Traditional Business Loan

- Your Bank Statement: A Key to Unlocking Business Funding

Looking to improve your cash flow? Explore Comfi's Invoice Discounting solutions. Get started today.