Top 10 SME Loan Alternatives for MENA Businesses in 2026

For small and medium-sized enterprises (SMEs) in the MENA region, securing capital is the fuel for growth. Yet, traditional bank loans often come with slow approval processes, strict collateral requirements, and rigid repayment schedules that do not always align with the dynamic nature of a growing business. This reality has paved the way for a new generation of financial tools designed for modern commercial needs.

This guide explores 10 practical SME loan alternatives that offer the flexibility, speed, and accessibility businesses require to thrive. We will break down how each option works, its specific pros and cons, and which business scenarios it suits best. Our goal is to provide a clear, educational resource that helps you make an informed decision to unlock your company's potential without the constraints of conventional lending routes. You will gain actionable insights to choose the right solution for your unique operational and growth challenges.

1. Invoice Discounting and Supply Chain Financing

As an excellent alternative to traditional SME loans, invoice discounting (also called supply chain financing) allows your business to get paid almost instantly for invoices issued to creditworthy buyers. Instead of waiting 30-90 days for your customers to pay, a third-party platform purchases your approved invoices at a small discount. They pay you upfront and then collect the full amount from your buyer on the original due date.

This method is especially useful for MENA-based SMEs dealing with large enterprises or government bodies known for longer payment cycles. For instance, an electronics distributor can unlock capital tied up in invoices to major retailers, or a food wholesaler can improve cash flow while waiting for payments from large restaurant chains. This process directly improves your cash conversion cycle. By getting paid faster, you can manage your accounts receivable turnover ratio more effectively without taking on debt.

Practical Tips:

- Digitise Invoicing: A digital process with clear, accurate invoices leads to faster approvals.

- Focus on Strong Buyers: Your eligibility often depends on your buyer's credit strength.

- Start Small: Test the process with a few high-value invoices to understand the workflow.

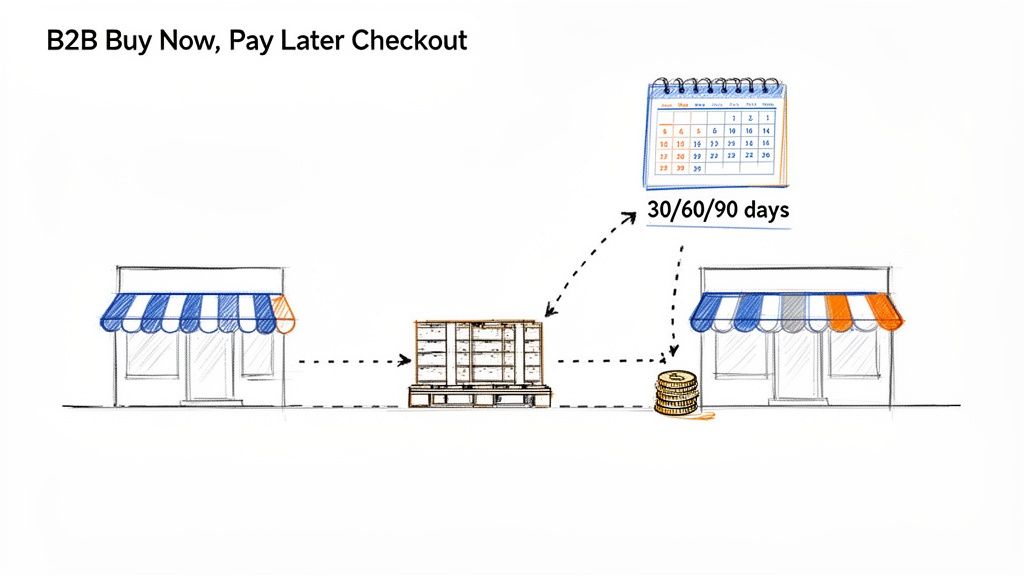

2. Buy Now, Pay Later (BNPL) for B2B

A powerful alternative to traditional SME loans, Buy Now, Pay Later (BNPL) for business-to-business transactions allows you to offer flexible payment terms to your customers at the point of sale. Instead of managing your own net-30 or net-60 terms and taking on credit risk, a BNPL platform pays you upfront. The platform then manages the payment collection from your buyer, allowing them to pay over 30, 60, or even 90 days.

This approach is transforming how MENA suppliers operate. For example, an automotive parts distributor can empower workshop chains to purchase more inventory by offering 60-day terms without impacting their own cash flow. Similarly, a specialty food supplier can help restaurants manage expenses by providing flexible payment options. This removes the burden of credit management and collections, letting you focus on growth while encouraging larger, more frequent orders from your business customers.

Practical Tips:

- Communicate Clearly: Ensure payment term options are visible and easy to understand at your checkout or point of sale.

- Integrate Seamlessly: Embed the BNPL option directly into your e-commerce platform or sales process for a smooth customer experience.

- Target Key Accounts: Start by offering BNPL to your most frequent or highest-value customers to build momentum.

3. Dealer and Auction Platform Payment Solutions

Specifically designed for inventory-heavy businesses, dealer and auction payment solutions are a powerful alternative to standard SME loans. It allows businesses like automotive or equipment dealers to acquire inventory from auctions and suppliers without using their own capital upfront. A third-party provider, such as Comfi, facilitates the payment for the purchase, and the dealer settles the amount once the vehicle or equipment is sold to an end customer.

This model is transformative for MENA-based automotive dealers who can now increase their stock and sales velocity. For example, a used car dealer in the UAE can instantly acquire more vehicles from auction, expanding their selection and attracting more buyers. For businesses, particularly in the automotive sector, understanding specific payment solutions is crucial. You can explore more about dedicated financing options empowering small dealerships to scale operations. This approach frees up working capital that can be reinvested into other growth areas.

Practical Tips:

- Negotiate Terms: Use your inventory turnover rate as leverage for more favourable terms.

- Integrate Systems: Link the payment solution directly with your auction platform for faster approvals.

- Monitor Costs: Keep a close watch on carrying costs to optimise how long you hold inventory.

4. Revenue-Based Financing (RBF)

As a modern alternative to SME loans, revenue-based financing (RBF) provides capital in exchange for a small percentage of your future monthly revenue. Repayments continue until a predetermined cap is reached. Unlike fixed-payment loans, RBF aligns repayments with your business’s performance, making it ideal for growth-stage SMEs with predictable income streams like subscription services or digital marketplaces. This flexibility means payments decrease during slower months, easing cash flow pressure.

This model is gaining traction among MENA-based SaaS platforms needing funds for customer acquisition or recurring B2B service businesses (e.g., maintenance contracts) looking to expand without giving up equity. It works by connecting directly to your payment systems to automate the collection process. Because the provider shares in the risk, they are invested in your success, making it a true growth partnership. This approach is a strong contender for businesses focused on scaling revenue.

Practical Tips:

- Project Revenue Accurately: Your eligibility and terms depend on well-documented, predictable revenue streams.

- Integrate Your Systems: Connect the RBF platform to your payment processor for seamless tracking and repayments.

- Invest for Growth: Use the capital for high-return activities like marketing or sales team expansion.

5. Trade Credit and Supplier Terms Optimization

Instead of seeking external funds, this classic SME loan alternative leverages your existing supplier relationships. Trade credit involves negotiating extended payment terms, such as net-60 or net-90, allowing you to use your supplier's capital to manage your own cash flow. By delaying your payables while receiving payments from customers, you can significantly improve your working capital position without taking on new obligations. This method is fundamental for effective cash flow management.

For MENA-based businesses, this strategy is highly effective. For example, a wholesale distributor can negotiate 90-day terms with manufacturers, or an e-commerce business can secure 30-day terms from its logistics providers. This gives them the breathing room to sell inventory before paying for it. By mastering this, you can better manage your business's financial health. You can learn more about how trade credit works and its benefits for SMEs.

Practical Tips:

- Build a Strong Record: Maintain a history of reliable, on-time payments to build trust.

- Formalise Requests: Approach key suppliers with a formal request for better terms, backed by your financials and order volume.

- Offer Value: Propose larger, more consistent orders in exchange for extended payment deadlines.

6. Bank Lines of Credit and Overdraft Facilities

Traditional bank lines of credit provide SMEs with access to revolving credit up to a predetermined limit, allowing you to draw and repay funds as needed. Similarly, an overdraft facility lets your business temporarily draw beyond its account balance. While these are more conventional SME loan alternatives and can be slower to arrange than fintech solutions, they often come with lower interest rates and larger amounts for established businesses with strong banking relationships.

This approach is well-suited for MENA-based SMEs that can demonstrate a stable history. For example, a well-established wholesaler in the UAE might use a seasonal credit line from a bank like Emirates NBD or FAB to manage inventory peaks. A family business with a three-year banking relationship could leverage an overdraft to cover unexpected payroll gaps. Success with these facilities depends heavily on your financial track record and relationship with the bank, offering a reliable, albeit less agile, source of capital.

Practical Tips:

- Build Relationships: Cultivate a strong connection with your bank before you need the credit.

- Maintain Clean Records: Keep your financial statements and tax filings accurate and up-to-date.

- Start Small: Begin with a smaller credit request to build a positive repayment history.

- Avoid Full Utilisation: Try to keep your balance below 70% of the limit to maintain a healthy credit profile.

7. Merchant Cash Advances (MCA)

A merchant cash advance (MCA) offers businesses an upfront lump sum of cash in exchange for a percentage of their future sales. Instead of a traditional interest rate, the provider takes a fixed percentage of your daily credit and debit card transactions until the agreed-upon amount is fully repaid. This repayment model flexes with your sales volume, which can be helpful during slower periods.

This method is one of the more accessible SME loan alternatives for businesses with high daily card transactions but perhaps weaker credit histories. For instance, a popular Dubai-based restaurant can use an MCA to quickly fund a kitchen upgrade by leveraging its consistent digital payment flow. Similarly, an e-commerce store experiencing a sales surge can secure immediate capital for inventory without a lengthy approval process. The fast access to funds is the primary appeal, but often comes at a higher cost.

Practical Tips:

- Calculate True Cost: An MCA’s factor rate can be misleading; calculate the effective annual percentage rate (APR) to understand the real expense.

- Confirm Consistent Volume: This option is only sustainable if your business has predictable and steady card-based revenue.

- Read the Fine Print: Carefully review the contract for the holdback percentage and any terms related to renewals or early repayment.

8. Microfinance and Community-Based Lending

For entrepreneurs and small businesses lacking the collateral or credit history required by banks, microfinance is a powerful SME loan alternative. Microfinance institutions (MFIs) and community lenders offer small-scale funding, often under AED 50,000, tailored for sole proprietors, small traders, and early-stage ventures. This approach focuses on the viability of the business idea and the character of the entrepreneur rather than just traditional financial metrics.

This model is particularly impactful in underserved MENA markets. For instance, a woman entrepreneur launching a home-based catering business or a small-scale farmer needing funds for seeds can secure capital through an MFI. These institutions often provide essential business coaching and financial literacy training alongside the funding, helping to build a sustainable enterprise. The goal is to provide a stepping stone to larger, more traditional options in the future by helping businesses establish a formal track record.

Practical Tips:

- Research Local MFIs: Identify institutions in your region that focus on your specific industry or demographic.

- Build Relationships: This type of lending is relationship-based; actively engage with the lender and community.

- Prepare a Clear Plan: Even for a small amount, a solid business plan and repayment projection are crucial.

9. Government Grants, Subsidies, and SME Support Programs

As a powerful non-debt SME loan alternative, government grants and support programmes provide capital to foster economic growth, innovation, and job creation. Entities across MENA offer funding that doesn't need to be repaid or comes with preferential terms. Unlike loans, these are awarded based on alignment with national objectives, such as export development, technology adoption, or sustainability. They are designed to de-risk strategic initiatives for SMEs.

For example, a UAE-based technology start-up could secure a grant to commercialise its software, while a Saudi food producer might get a subsidy to expand its export operations under Vision 2030 initiatives. These programmes allow businesses to pursue growth projects that might otherwise be too costly or risky. This direct injection of capital strengthens your financial position without adding liabilities, allowing you to invest in critical areas and gain a competitive edge.

Practical Tips:

- Research Locally: Focus on programmes specific to your country, industry, and business size.

- Align Your Plan: Ensure your business plan and application strongly align with the programme's goals.

- Plan Ahead: The application and approval process can take months, so start well in advance.

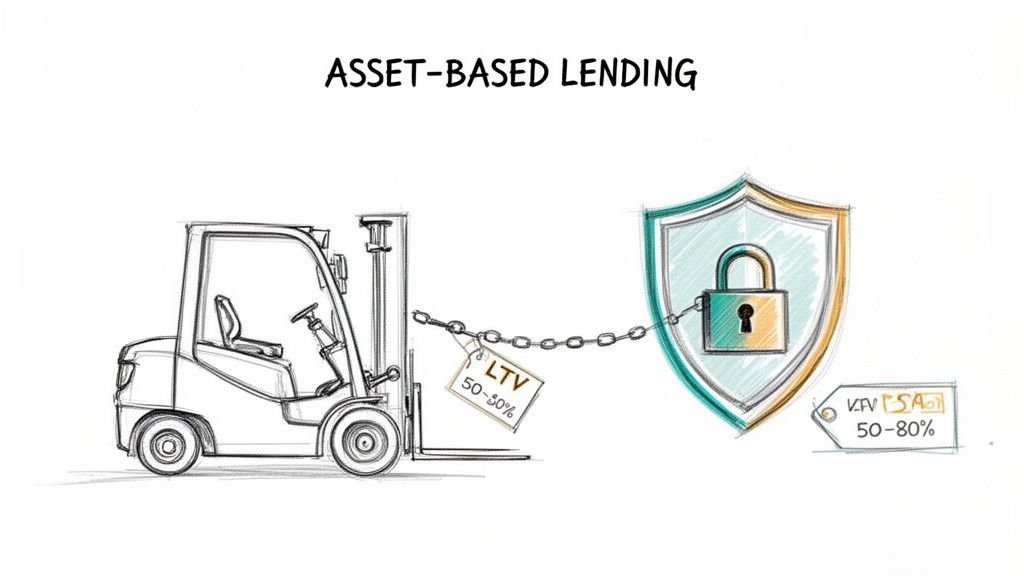

10. Asset-Based Lending and Equipment Financing

Asset-based lending uses your company's existing assets, like inventory or machinery, as collateral to secure capital. A specific form of this is equipment financing, which helps businesses purchase necessary vehicles, technology, or machinery. Instead of evaluating your business purely on cash flow or credit history, the value of the asset itself secures the arrangement, making it an accessible SME loan alternative for capital-intensive industries.

This method is ideal for sectors requiring significant physical infrastructure. For example, a construction company in the UAE can finance heavy equipment purchases, or a logistics firm can acquire a new fleet of trucks. Similarly, a manufacturing business can secure new production machinery without depleting its operational cash reserves. The asset being acquired serves as its own security, often resulting in more favourable terms compared to unsecured options.

Practical Tips:

- Get Independent Valuations: Obtain a professional, third-party valuation of your assets before applying to ensure you receive fair terms.

- Compare All Options: Evaluate the pros and cons of purchasing versus leasing or sale-leaseback arrangements for your specific needs.

- Plan for Total Cost: Factor in asset insurance, maintenance, and potential depreciation into your overall financial planning.

Top 10 SME Loan Alternatives Comparison

Here's a breakdown of the key features for each SME loan alternative:

- Invoice Discounting & Supply Chain Financing

- Core features: 70–90% advance, buyer-credit underwriting, digital upload, funding within 24h, paperless integration.

- Typical cost: Discount fee ~1–3% per invoice.

- Target audience: B2B suppliers, wholesalers, distributors with institutional buyers.

- Value proposition: Converts receivables to immediate cash, lower cost than traditional factoring, preserves customer relationships.

- Main limitations: Requires creditworthy buyers, discount reduces invoice value, needs regular invoicing.

- Core features: 30/60/90-day terms, instant eligibility, supplier paid upfront, automated collections, API/plugins.

- Typical cost: Platform fee ~2–4% per transaction.

- Target audience: E‑commerce, wholesalers, distributors, repeat B2B buyers.

- Value proposition: Increases AOV and sales (20–30%), removes collections burden, improves buyer retention.

- Main limitations: Integration required, fees reduce margins, platform eligibility limits some buyers.

- Core features: Inventory-backed payment facilitation, real-time approval at purchase/auction, flexible repayment tied to turnover.

- Typical cost: Secured rates vary by asset/LTV; fee depends on turnover.

- Target audience: Automotive/equipment dealers, auction platforms, fleet buyers.

- Value proposition: Enables inventory acquisition without pre-funding, increases bidding power and turnover.

- Main limitations: Collateral concentration risk, depends on inventory liquidity and valuation.

- Core features: Advance vs projected revenue, repayment as % of revenue (5–15%), 6–24 month typical term, integrated tracking.

- Typical cost: Repayment cap or effective cost variable (often 1.2–2.5x total).

- Target audience: B2B SaaS, subscription & recurring-revenue businesses.

- Value proposition: Payments scale with revenue, no equity dilution, flexible cash-flow-aligned repayments.

- Main limitations: Can be costly if revenue grows fast, needs predictable recurring revenue, transparency required.

- Core features: Negotiate net-30/60/90 or consignment, early-pay discounts, procurement/AP integration.

- Typical cost: Often zero direct cost (opportunity cost); forgone discounts possible.

- Target audience: All B2B businesses, distributors, retailers, e‑commerce.

- Value proposition: Zero-cost working capital when negotiated well; strengthens supplier relations.

- Main limitations: Requires strong payment history, active supplier management, may strain suppliers.

- Core features: Revolving limit, interest on drawn amounts, collateral/guarantees, multi‑year commitments.

- Typical cost: Interest typically ~6–12% p.a.; fees and collateral may apply.

- Target audience: Established SMEs (3+ years), businesses needing larger capital.

- Value proposition: Lower rates and larger amounts, flexible draw/repay, builds banking relationship.

- Main limitations: Slow approval (weeks), collateral/personal guarantees often required, stricter underwriting.

- Core features: Lump-sum advance repaid as % of daily card sales, quick approval/funding, automatic holdbacks.

- Typical cost: Effective APR very high (40–300%); daily/weekly holdback 5–10%.

- Target audience: High card-volume retailers, restaurants, e‑commerce with daily payments.

- Value proposition: Fastest funding, no credit score requirement, repayment scales with sales.

- Main limitations: Very expensive, can strain cash flow, limited transparency, risky long-term.

- Core features: Small loans (AED ~5k–100k), flexible collateral/group guarantees, business coaching.

- Typical cost: Interest ~15–25% typical.

- Target audience: Micro-entrepreneurs, sole traders, underserved SMEs, women-led businesses.

- Value proposition: Accessible without formal credit, mentoring and capacity building, builds credit history.

- Main limitations: Small amounts vs growth needs, higher rates than banks, limited digital integration.

- Core features: Non-dilutive grants or below-market loans, program-specific support, mentorship & networks.

- Typical cost: Often grant or below-market rates; tranche-based disbursement.

- Target audience: Tech/innovation SMEs, exporters, green projects, priority sectors.

- Value proposition: Free or cheap capital, mentorship, reduced lender risk via guarantees, market access.

- Main limitations: Lengthy bureaucratic processes, strict eligibility and reporting, competitive selection.

- Core features: Financing against equipment/inventory/receivables, LTV ~50–80%, fixed terms, lease/sale-leaseback options.

- Typical cost: Interest typically ~8–15% depending on asset/LTV.

- Target audience: Capital-intensive firms: automotive, manufacturing, logistics, construction.

- Value proposition: Larger secured amounts, lower rates than unsecured, predictable payments, tax benefits.

- Main limitations: Risk of asset seizure, personal guarantees possible, valuation and maintenance required.

Choosing the Right Path to Fuel Your Business Growth

The landscape of business funding has evolved far beyond traditional bank loans. For SMEs in the MENA region, the journey to securing capital is now filled with diverse and flexible SME loan alternatives, each tailored to specific operational needs and growth stages. From unlocking cash tied up in unpaid invoices with factoring to leveraging B2B Buy Now, Pay Later to boost sales, the power has shifted towards solutions that align with your actual business cycle.

The central takeaway is that there is no one-size-fits-all answer. Your ideal funding mix depends entirely on your industry, cash flow patterns, and strategic goals. A wholesaler might find immense value in dealer financing to manage inventory, while a service-based business could rely on invoice discounting to bridge payment gaps. The key is to move from a reactive search for funds to a proactive financial strategy. This involves not only selecting the right tools but also optimising your core operations. For instance, a deeper focus on understanding logistics management can streamline your supply chain, which in turn reduces your working capital needs and strengthens your financial position.

Ultimately, mastering these modern funding options is about more than just accessing cash; it's about building resilience and agility into your business model. By thoughtfully evaluating the pros and cons of each alternative, you can create a robust financial foundation that doesn't just solve immediate shortfalls but actively fuels your long-term ambitions. This strategic approach empowers you to seize opportunities, manage risks, and confidently steer your business towards sustainable growth.

Ready to unlock your business's potential without the hurdles of traditional financing? Comfi offers streamlined payment solutions designed to help your business unlock working capital and accelerate growth. Explore how our B2B BNPL and supplier payment tools can empower your business today at Comfi.

Related Reading

- Your 2026 Guide to the 11 Best SME Business Loan Options in the UAE

- Finance Lender: How to Choose the Right Partner for SMEs

- 7 Faster Alternatives to a Traditional Business Loan

- Your Bank Statement: A Key to Unlocking Business Funding

Looking to improve your cash flow? Explore Comfi's Invoice Discounting solutions. Get started today.