10 Best Finance Lender Options for MENA SMEs in 2026

For small and medium-sized enterprises (SMEs) in the MENA region, consistent cash flow is the fuel for growth. Yet, managing long payment cycles and unlocking tied-up working capital can be a significant hurdle, slowing down operations and preventing expansion. This is where a modern finance lender comes in, offering specialised, tech-driven solutions designed for the agility that today's businesses need.

This comprehensive guide breaks down the different types of finance providers and the models they use, from invoice discounting and dealer floor-planning to embedded B2B Buy Now, Pay Later (BNPL) platforms. We will explore how these solutions operate, their practical benefits, and the potential risks for MENA-based SMEs. To truly understand these options, it's also helpful to consider the broader business finance landscape and how different regional ecosystems are evolving.

Our goal is to provide a clear, educational roadmap to help you navigate your options. Throughout this article, we will detail specific platforms and providers, complete with direct links and insights, to help you choose the right partner. By the end, you will have a practical checklist and the knowledge needed to select a solution that stabilises your cash flow and helps you seize new growth opportunities without getting stuck in rigid, slow-moving processes.

1. Comfi

Best for: Streamlining B2B payments and optimizing cash flow for MENA-based SMEs.

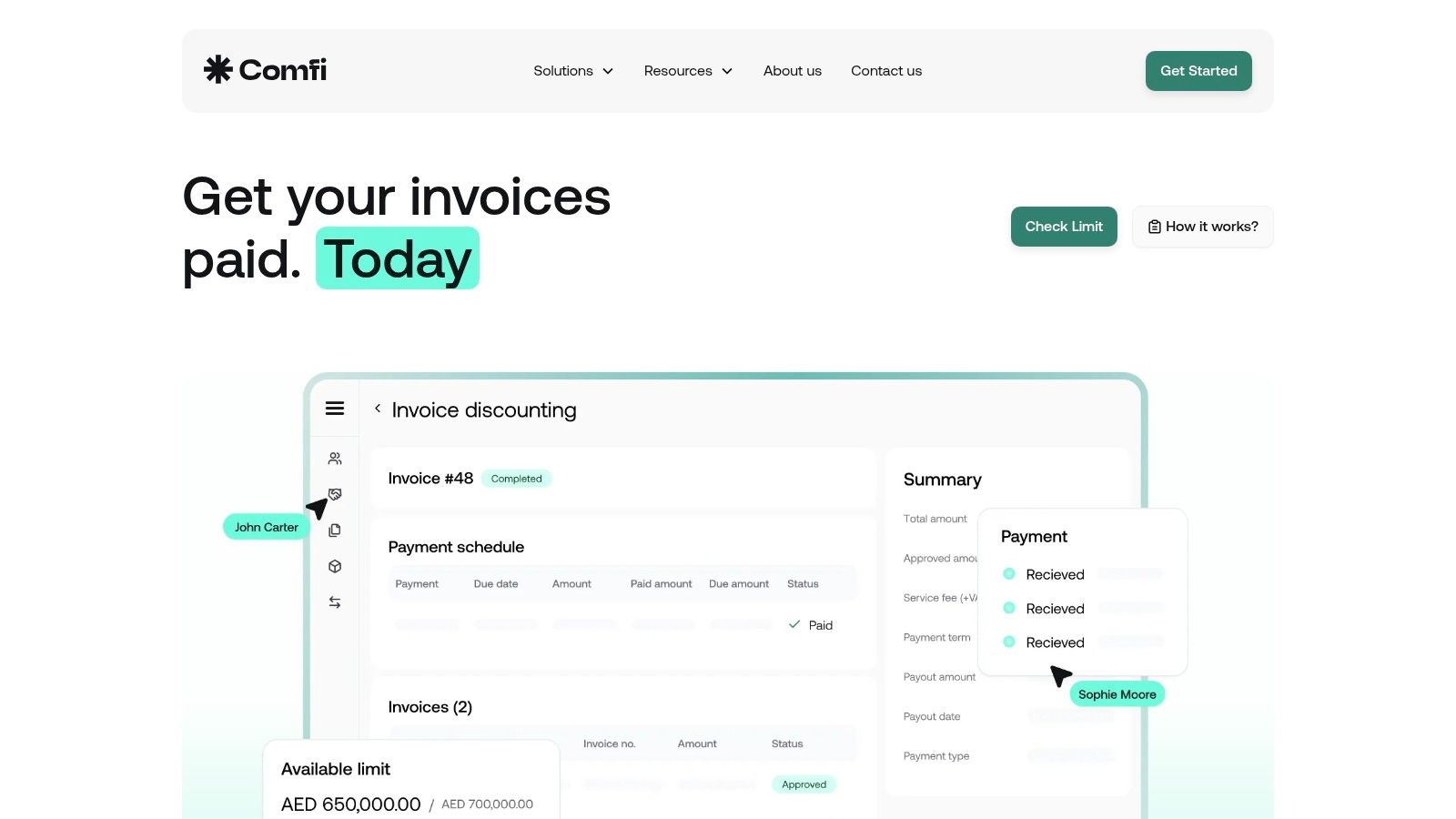

Comfi stands out as a premier fintech platform designed to give MENA SMEs greater control over their cash flow. It achieves this by transforming unpaid B2B invoices into immediate cash for suppliers, while simultaneously offering buyers the flexibility of extended payment terms. This dual-sided approach directly addresses common cash-flow bottlenecks that can slow business growth, making it an exceptional partner for suppliers, distributors, and B2B marketplaces. Through its platform, clients have been able to unlock their working capital.

What makes Comfi particularly effective is its suite of integrated solutions tailored to the B2B transaction cycle. Its Invoice Discounting service allows businesses to get paid on their invoices within 24 hours of approval, eliminating long waits. For sellers looking to boost sales, its Buy Now, Pay Later (BNPL) function lets them offer attractive 30, 60, or 90-day payment terms to their buyers, without taking on the credit risk or collection burden themselves. Comfi handles the collections process, freeing up valuable internal resources for the supplier.

Practical Application & Key Features

The platform is engineered for speed and simplicity. A fully digital, paperless onboarding process and instant eligibility checks mean businesses can get started quickly. For broader integration, Comfi provides low-code plugins and a developer-friendly API, allowing it to embed seamlessly into existing e-commerce platforms, ERP systems, or marketplaces. This makes it an ideal embedded payment terms provider for industries like automotive, electronics, and consumer goods.

- Fast Liquidity: Approved invoices are funded within 24 hours, dramatically shortening the cash conversion cycle.

- Risk Mitigation: Comfi assumes the collections process, removing the credit risk and operational overhead from suppliers.

- Sales Growth: Businesses using Comfi report tangible results, including up to 30% larger average order sizes and a 20% increase in new customer acquisition.

- SME-Focused: With a high approval rate (around 85%) and over 1,000 SMEs on its platform, it is proven to serve the specific needs of this segment.

Limitations: Pricing is not publicly listed; businesses must contact Comfi for a tailored quote based on their specific needs. Its services are primarily focused on the MENA region, which may not suit companies with operations outside this geography.

2. Beehive

Beehive is a leading peer-to-peer (P2P) lending platform in the UAE, connecting established SMEs directly with a crowd of investors for financing. Regulated by the DFSA, it offers a streamlined digital alternative to conventional bank loans, facilitating both conventional and Sharia-compliant funding. Businesses can apply online for term finance or invoice finance, with decisions often made within a few days, providing a much faster route to capital than traditional institutions.

This P2P model makes Beehive a unique finance lender, as funding comes from a pool of private and institutional investors rather than a single financial entity. The platform’s digital-first approach means applications are paper-light, and businesses can track their application status and repayments online. Its transparent terms and fee structure appeal to SMEs looking for clarity and control over their financing. The availability of Sharia-compliant options through a Commodity Murabaha structure also makes it an accessible choice for a wider range of businesses in the region.

- Best For: Established SMEs in the UAE and Oman seeking flexible term or invoice financing with a transparent, digital-first process.

- Availability: Services are available for businesses registered and operating in the UAE and Oman.

- Key Feature: Offers both conventional and Sharia-compliant financing, broadening its appeal to diverse business needs across the GCC.

Learn more at Beehive's website

3. Funding Souq

Funding Souq is a crowdlending platform connecting established SMEs in the UAE and KSA with a pool of retail and institutional investors. It operates as an alternative finance lender, focusing on providing Sharia-compliant business term facilities. The platform streamlines the funding process through a fully digital onboarding system, allowing businesses to apply for amounts ranging from AED 100,000 to AED 1,000,000.

This model offers a transparent and relatively quick path to capital for businesses that meet its eligibility criteria. Once a business is approved, its funding request is listed as a campaign for investors on the platform to back. Funding Souq’s UAE entity is regulated by the Dubai Financial Services Authority (DFSA), providing a layer of security and trust for both borrowers and investors. The focus on established SMEs makes it a reliable choice for companies with a proven track record looking to fund growth or manage operational expenses without approaching traditional banks.

- Best For: Established SMEs in the UAE and KSA seeking transparent, Sharia-compliant term facilities from a diverse investor base.

- Availability: Serves businesses registered and operating in the United Arab Emirates and the Kingdom of Saudi Arabia.

- Key Feature: A campaign-style crowdlending model regulated by the DFSA (for its UAE entity) that connects businesses directly with investors.

Learn more at Funding Souq's website

4. Emirates Development Bank (EDB)

Emirates Development Bank (EDB) is a government-backed financial institution established to support the UAE's economic diversification and industrial transformation agenda. As a key development finance lender, EDB provides direct and indirect financial solutions to SMEs and startups operating within priority sectors such as manufacturing, advanced technology, healthcare, and food security. Its primary goal is to bridge the funding gap for businesses that are pivotal to the nation's long-term growth.

What makes EDB unique is its Credit Guarantee Scheme, which significantly de-risks lending for commercial banks. By guaranteeing a substantial portion of the loan (often up to 85%), EDB encourages partner banks to approve financing for SMEs that might otherwise be considered too high-risk. This public-policy mandate, combined with digital application routes developed with fintech partners, makes it an essential enabler for businesses aligned with the UAE's strategic vision. This government backing improves SME access to critical working capital needed for expansion and innovation.

- Best For: SMEs and startups in priority industrial sectors needing government-backed financial support or loan guarantees to secure funding.

- Availability: Exclusively serves UAE-based businesses that meet specific eligibility and sectoral criteria.

- Key Feature: The Credit Guarantee Scheme, which partners with commercial banks to improve loan approval rates for SMEs by reducing the lender's risk.

Learn more at Emirates Development Bank's website

5. RAKBANK

RAKBANK is a prominent UAE-based bank well-known for its strong focus on Small and Medium Enterprise (SME) banking. It offers a range of business loan products designed to help SMEs secure capital for growth, expansion, or managing operational expenses. The bank provides both conventional and Islamic financing variants, with unsecured loan options available up to AED 3 million for qualifying businesses.

As a traditional finance lender, RAKBANK has streamlined parts of its process with digital tools like its "Quick Apply" workflow, which provides fast in-principle decisions. This makes it more accessible than purely branch-based banking. The institution also offers valuable resources through its SMEsouk platform, providing business support beyond just capital. However, applicants should be prepared to provide comprehensive documentation and meet credit history requirements, and be aware that pricing and penalties can vary based on risk assessment. You can explore more about trade finance options at RAKBANK to understand their offerings better.

- Best For: Established SMEs in the UAE with a solid credit history seeking traditional business loans for significant capital investment.

- Availability: Primarily serves businesses registered and operating within the UAE.

- Key Feature: Digital application process for business loans with quick in-principle approval, blending traditional banking with modern convenience.

Learn more at RAKBANK's website

6. Emirates NBD

Emirates NBD is one of the UAE’s largest and most established banking groups, offering a comprehensive suite of business banking products. For SMEs, it acts as a traditional finance lender, providing solutions that range from working capital support and trade finance to point-of-sale (POS) receivable loans and commercial property-backed lending. The bank serves businesses of all sizes, leveraging its extensive network of branches and business banking centres across the UAE.

A key differentiator is its Dubai International Growth Initiative, launched in partnership with the Government of Dubai. This programme offers eligible Dubai-founded SMEs expanding globally access to loans of up to AED 15 million at a highly subsidised EIBOR-only rate. While this initiative provides a significant cost advantage for qualifying businesses, the bank’s standard credit criteria and documentation requirements apply across all its products, making it a more conventional finance option compared to fintech platforms.

- Best For: Established SMEs in the UAE seeking a wide range of conventional banking facilities and Dubai-based businesses planning international expansion.

- Availability: Primarily serves businesses registered and operating within the UAE.

- Key Feature: The Dubai International Growth Initiative offers exceptionally low-cost funding for qualifying Dubai-founded SMEs to support their global growth.

Learn more at Emirates NBD's website

7. First Abu Dhabi Bank (FAB)

First Abu Dhabi Bank (FAB) is one of the UAE’s largest banks, offering a comprehensive suite of SME lending solutions. Among its key products are working capital facilities, term loans, and a specialised POS Loan designed for businesses with high volumes of card transactions. This makes FAB a strong traditional finance lender for established SMEs looking to leverage their daily sales revenue for immediate liquidity, bridging cash flow gaps without disrupting operations.

The bank’s POS Loan is particularly beneficial for retail, F&B, and other customer-facing businesses that rely heavily on card payments. By advancing funds against future card receivables, FAB provides a predictable and accessible credit line tied directly to business performance. With its extensive nationwide presence, FAB offers stability and scale, although accessing detailed product information may require direct contact with the bank. The application process is relatively streamlined for businesses that meet the card turnover criteria.

- Best For: Retail and hospitality SMEs with consistent POS card turnover seeking to monetise their daily sales for working capital.

- Availability: Primarily serves businesses registered and operating within the UAE.

- Key Feature: The POS Loan option provides a direct way for merchants to secure funds based on their card machine sales volume.

Learn more at First Abu Dhabi Bank's website

8. ADIB (Abu Dhabi Islamic Bank)

ADIB is a leading Islamic bank providing Sharia-compliant SME finance solutions in the UAE. It offers a range of products designed for working capital, CAPEX, and trade finance needs, making it a reliable finance lender for businesses that require adherence to Islamic principles. Offerings like Small Business Finance and Relationship-Based Finance are structured to support day-to-day operations and long-term growth, with options available for collateral-free facilities within certain limits.

The bank's strength lies in its deep expertise in Islamic financing structures like Murabaha and Ijara, providing ethical alternatives to conventional loans. This makes ADIB an essential partner for SMEs prioritizing Sharia compliance. While the bank does have specific eligibility criteria related to business age and annual turnover, its collateral-free options for qualified SMEs are a significant advantage. The process involves standard documentation, ensuring a structured and transparent approach for businesses seeking a credible and established finance lender.

- Best For: SMEs requiring Sharia-compliant financing for working capital, trade, or asset acquisition.

- Availability: Primarily serves businesses operating within the UAE.

- Key Feature: Offers collateral-free finance options for qualified SMEs, reducing the barrier to entry for securing working capital.

Learn more at ADIB's website

9. LNDDO

LNDDO is a UAE-based digital lender, licensed by the ADGM/FSRA, that offers short-term working capital solutions specifically for SMEs. Its model focuses on providing quick, accessible funding through a fully digital onboarding process. By partnering with payment gateways, LNDDO offers pre-approved merchant finance to e-commerce businesses and POS merchants, making it a highly relevant finance lender for the modern digital economy.

The platform is designed for speed, with fast credit decisions and funding available via its partner programmes, with limits reaching up to approximately USD 100,000. LNDDO’s strength lies in its zero-collateral, short-term solutions for inventory or order funding. This approach removes significant barriers for e-commerce SMEs that need immediate capital but lack the traditional assets required by larger banks. Being regulated under ADGM provides a layer of trust and structure to its offerings.

- Best For: E-commerce and POS merchants in the UAE needing fast, zero-collateral working capital for inventory and operational needs.

- Availability: Primarily serves businesses based in the UAE.

- Key Feature: Ecosystem integrations with payment gateways to provide embedded, pre-approved merchant financing directly within their existing platforms.

Learn more at LNDDO's website

10. Liwwa

Liwwa is a technology-driven SME finance lender operating primarily in Jordan and Egypt, offering a modern approach to business loans for MENA-based businesses. The platform leverages an investor marketplace model to fund its loans, enabling fast and data-driven lending decisions. A key differentiator is its offering of Sharia-compliant financing structures, catering to a specific and significant market need within the region.

The platform is designed to overcome traditional banking hurdles by providing quick access to capital, often with minimal collateral requirements. Liwwa targets a decision-making timeframe of around two days, which is a significant advantage for SMEs needing to act on growth opportunities swiftly. With thousands of businesses already financed, this finance lender has a proven track record of supporting SME development in its core markets. Its focus on impact and substantial lending history make it a credible option for businesses in the Levant and North Africa.

- Best For: SMEs in Jordan and Egypt seeking fast, collateral-light business loans, including Sharia-compliant options.

- Availability: Primarily serves businesses registered in Jordan and Egypt; entities in other MENA countries should confirm eligibility.

- Key Feature: An investor marketplace model that powers its data-centric underwriting process for rapid funding decisions.

Learn more at Liwwa's website

Making Your Final Decision: Partnering for Sustainable Growth

Navigating the diverse landscape of financial solutions can seem complex, but understanding your options is the first step toward securing your business's future. Throughout this guide, we have explored a range of partners, from traditional banks like Emirates NBD and RAKBANK to innovative fintech platforms such as Beehive and Comfi. Each offers a unique approach to addressing the cash flow challenges that SMEs in the MENA region frequently encounter.

The key takeaway is that the ideal partner depends entirely on your specific business needs. A traditional finance lender might offer established processes and a wide array of services, but a fintech specialist often provides superior speed, flexibility, and technology integration tailored for the fast-paced SME environment. Your decision should be a strategic one, based on a clear understanding of your operational bottlenecks and growth ambitions.

Key Considerations Before You Choose

Before making a final commitment, revisit the core evaluation criteria we discussed. Your goal is to find a partner, not just a provider.

- Problem-Solution Fit: Does the solution directly address your primary pain point? If delayed B2B payments are stifling your growth, an embedded payments specialist like Comfi is a more targeted solution than a conventional business loan. If you need capital for a large, one-off expansion, a bank or P2P platform might be more suitable.

- Operational Integration: How easily can the solution fit into your existing workflow? Modern platforms that integrate directly into your invoicing, e-commerce, or ERP systems can save significant time and reduce manual errors, allowing you to focus on your core business.

- True Cost and Transparency: Look beyond the headline rates. Understand all associated fees, the repayment structure, and any potential penalties. The most effective financial tools are those with clear, transparent pricing that aligns with your revenue cycle.

Actionable Next Steps for Your Business

Choosing a finance lender or payments partner is a pivotal decision that will shape your company's growth trajectory. Don't rush the process. Start by shortlisting two or three options from this guide that seem most aligned with your business model. Prepare your financial documents and create a list of specific questions about their process, integration capabilities, and support model.

By taking a methodical and informed approach, you are not just securing funds; you are building a partnership that supports sustainable growth. The right choice will empower you to manage your working capital effectively, seize new opportunities with confidence, and build a more resilient and scalable enterprise.

Ready to see how a modern payments solution can unlock your business potential without the complexities of traditional lending? Discover how Comfi provides instant payment options for your B2B invoices and checkouts, helping you improve cash flow and boost sales. Explore our tailored solutions for SMEs at Comfi.

Related Reading

Looking to improve your cash flow? Explore Comfi's Invoice Discounting solutions. Get started today.