Guide to Florist Invoice Financing UAE

A florist in Dubai can have a full order book and still feel cash-poor.

That happens all the time. You win a wedding, a hotel contract, or a corporate gifting order. The client is happy to approve the arrangements. Your team starts sourcing stems, booking delivery slots, confirming freelancers, and preparing refrigeration space. But payment from the client may only arrive weeks later.

For a floral business, that gap is more stressful than it sounds. Flowers don't wait. Roses, hydrangeas, lilies, and imported seasonal stock all have their own shelf life. If cash is tied up in unpaid invoices, every new order can feel like a juggling act. That's why many owners start looking into florist invoice financing UAE options. Not because the business is failing, but because growth creates pressure before it creates cash.

The Florist's Cash Flow Dilemma

A familiar example looks like this.

You secure a large event order from a corporate client in Dubai. It's a strong contract and the invoice is legitimate. The problem is timing. The venue wants floral installations on schedule, the supplier wants payment sooner, and your client pays on account after internal approval. Your business sits in the middle, carrying the cost.

Where the pressure builds

A florist doesn't just buy flowers. You're often paying for:

- Imported stock: Premium stems, fillers, greenery, and specialty blooms

- Labour: Designers, setup staff, drivers, and freelance event hands

- Logistics: Vans, cold handling, last-mile delivery, and venue access timing

- Event extras: Stands, wrapping, ribbons, candles, props, and replacements for damaged stems

If payment only comes after the event, cash gets trapped in receivables.

That's why profitable florists still feel squeezed. A strong sales month can create more strain if several big invoices are still unpaid.

Healthy demand doesn't always mean healthy cash flow. In floristry, the busiest period can be the tightest period.

Why operations matter too

There's another layer here. Floral businesses often rely on quick coordination across invoicing, stock, staff schedules, and delivery planning. If those systems are messy, cash flow becomes even harder to manage. For teams trying to tighten back-office operations, Cloudvara's IT support expertise is a useful reference because better systems often reduce delays between fulfilment, invoicing, and collection.

The main issue is simple. You've already done the selling. You've earned the revenue. But the money is still stuck on someone else's payment timetable.

Unlocking Cash from Unpaid Invoices An Introduction

Invoice discounting is easier to understand if you stop thinking of it as a complex finance product and start thinking of it as early access to money you've already earned.

A florist delivers an order, issues an invoice, and waits for the client's payment date. Invoice discounting shortens that wait. Instead of sitting on the invoice for weeks, the business uses that unpaid invoice to access cash sooner.

A simple way to picture it

Consider this scenario: You've finished the job, the client owes you money, and the invoice proves it. Invoice discounting lets you pull forward part of that payment instead of waiting for the due date.

That's why many owners find it less intimidating once it's explained in plain language. You're not trying to create revenue out of nowhere. You're accelerating access to a receivable that already exists.

The four terms that matter

Here are the only terms you really need to know:

- Invoice

This is the bill you send your client after delivering flowers, décor, or event work. - Advance

This is the portion of the invoice value made available upfront. - Fee

This is the provider's charge for making the cash available early. - Balance

Once the customer pays the invoice, the remaining amount is settled after the agreed fee is accounted for.

Why UAE florists like this structure

For a creative business owner, the appeal is practical. You can buy stock for the next order without waiting for the previous one to clear. That matters when one event leads directly into another.

It also reduces the feeling that every busy week must be self-funded from your own reserves.

Practical rule: If your biggest stress comes from timing rather than lack of sales, receivables-based funding is worth understanding.

What people often confuse

Many florists hear “invoice financing” and assume it means taking on a conventional loan. That's where confusion starts.

The core idea here is different. The decision often centres on the quality of the invoice and the customer behind it, not on whether your business owns lots of hard assets. That's why this tool can fit service-heavy and order-based businesses so well.

If your customers are businesses, hotels, corporates, or event organizers, and they pay on terms, an unpaid invoice can be more useful than it looks.

Why Your Floral Business Needs a Better Cash Flow Tool

A floral business doesn't run on average weeks. It runs on peaks, deadlines, and perishability.

One week is quiet. The next week brings a wedding, an Eid gifting run, two hotel refresh orders, and a corporate event install. If cash only arrives after those jobs are finished and approved, the business keeps stretching itself at exactly the moment it should be moving confidently.

Growth creates pressure before it creates comfort

A Dubai business guide notes that successful flower shops in the city often generate AED 1.2 million to AED 3.5 million in annual revenue, and that the standard 5% VAT rate applies to most floral products and services. It also notes that the UAE cut-flower market is projected to grow at a 13.7% CAGR from 2022 to 2028. In the same context, corporate payment terms of 30 to 90 days can tie up cash right when a florist needs it most, according to the Dubai flower business market overview.

That combination matters more than many owners realise. Revenue can look solid on paper while day-to-day cash remains tight in practice.

The real benefit is operational freedom

For florists, a better cash flow tool helps in ways that are very specific to the trade:

- You can buy fresher stock with less hesitation: when cash is available earlier, you don't have to compromise on stem quality just because a previous invoice is still outstanding.

- You can accept larger B2B orders more calmly: hotel accounts, event agencies, and corporate gifting programmes often come with bigger order values and slower payment habits.

- You can smooth seasonality: weddings, festive periods, and event seasons rarely line up neatly with when customers settle invoices.

- You can protect margins from waste: delayed cash can push owners into over-ordering cautiously or under-ordering defensively. Neither is ideal.

Better invoicing helps before funding even starts

Clean invoicing is part of the equation. If your invoice dates, delivery proofs, client details, and payment terms are scattered, collection delays get worse. Florists that want to tighten that process can learn from the ReceiptGen guide on professional invoice systems, because better invoice structure often supports faster approval and fewer disputes.

A florist doesn't just need cash. They need timing, visibility, and confidence to buy the right stock at the right moment.

The biggest shift in mindset is this. Florist invoice financing UAE solutions aren't only for rescue situations. They can also help a business say yes to more profitable work without putting every new order under strain.

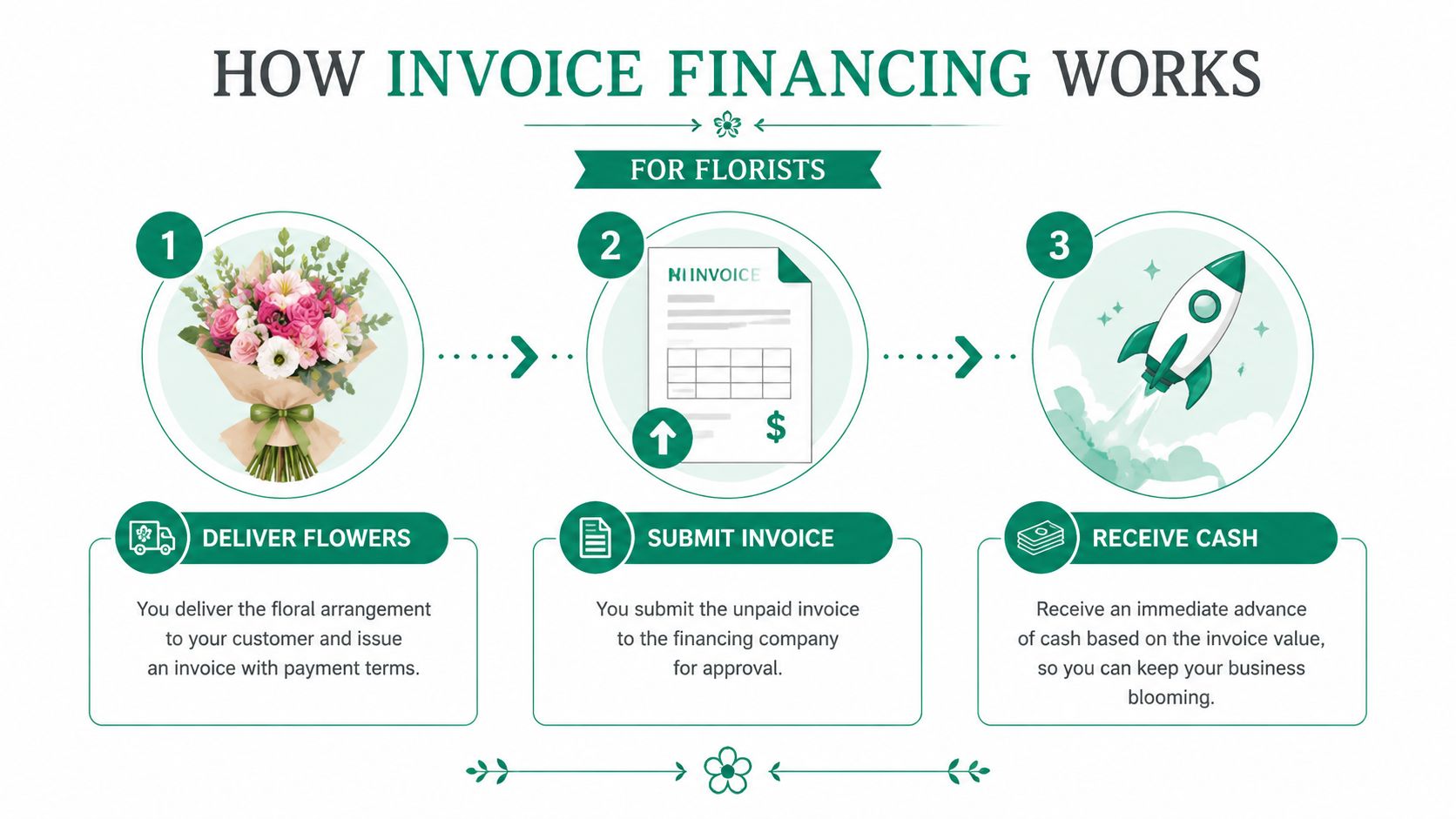

Your Step-by-Step Guide to Invoice Discounting in the UAE

Once the concept clicks, the next question is usually practical. How does this work day to day?

For UAE florists, the funding decision is commonly driven by invoice quality, and providers often advance 80% to 90% of eligible invoice value within 24 to 48 hours. Fintechs like Comfi require only a trade license, MOA, bank statement, and invoice for a B2B order and advance 100% of the invoice value.

Step 1 Check whether your invoices are a fit

This tool usually works best when your business issues invoices to other businesses, not individual walk-in customers.

Good examples include:

- Hotel supply invoices

- Corporate gifting accounts

- Wedding planner or venue invoices

- Event agency orders with documented delivery

- Recurring B2B décor or maintenance arrangements

If an invoice is clear, delivered, and owed by a business customer with acceptable payment behaviour, it's more likely to be considered usable.

Step 2 Gather the basic documents

The process is often lighter than people expect.

Most florists should prepare:

- Trade license

- Recent bank statement

- The invoice itself

- Supporting order or delivery records, if requested

If your records are organized, this stage feels straightforward. If they aren't, this is usually where delays start.

Step 3 Submit the invoice for review

At this point, the provider reviews the invoice and the customer profile behind it.

That review is why accuracy matters. A wrong legal entity name, unclear delivery proof, or disputed amount can slow things down. A clean paper trail helps the receivable look more reliable.

For businesses exploring digital options, Comfi's invoice discounting product is one example of a UAE-based workflow built around unpaid business invoices and digital submission.

Step 4 Receive the advance

If the invoice is approved, part of its value is made available before the customer pays. For a florist, that can immediately go toward new stock, drivers, event labour, or supplier settlement.

This is often the point where the product becomes real to owners. The unpaid invoice stops being a static document and starts acting like a live business asset.

Step 5 Close the loop when the customer pays

When the customer settles the invoice on the agreed date, the transaction is reconciled and the remaining balance is handled according to the arrangement.

Keep your event paperwork tight. Signed quotations, delivery notes, approval emails, and final invoices reduce confusion later.

A florist using this tool well usually treats it like part of their operating rhythm, not a one-off patch. The cleaner your B2B invoicing process, the easier it becomes to use invoice discounting smoothly.

A Clear Look at Pricing and Fee Structures

Cost is where most owners pause. That's sensible. A cash flow tool should make your business easier to run, not erode your margin.

The pricing for invoice discounting usually comes down to two moving parts. First, how much of the invoice value is made available upfront. Second, what fee is charged for that early access.

The two numbers to focus on

UAE invoice financing listings commonly show an upfront advance of 80% to 90% of invoice value, with fees around 1% to 3% per month and tenors of 30 to 90 days. Some providers also advertise approval in as little as 4 hours and funding within 24 hours, according to this overview of UAE invoice financing market terms.

Those numbers tell you what to evaluate:

- Advance rate: how much cash you can access now

- Fee rate: what you pay for getting that cash earlier

- Time period: how long the invoice is expected to stay outstanding

A simple example without overcomplicating it

Say your florist issues an invoice for an event order.

If the advance rate is near the market range above, you receive most of that invoice value upfront rather than waiting for the client's payment cycle. The provider's fee is then applied based on the agreed structure and time period. After the customer pays, the remaining amount is settled net of that fee.

You don't need a finance degree to assess whether that works. Ask one practical question:

Does getting the cash early help me protect margin, accept profitable work, or avoid more expensive pressure elsewhere?

How to think about the fee properly

Some florists look only at the fee and stop there. That can be too narrow.

A better lens is to compare the fee against what delayed cash is already costing you:

- Missed orders: turning down work because you can't buy stock in time

- Worse purchasing decisions: buying smaller quantities or less suitable flowers

- Operational strain: delaying payroll, transport, or supplier payments

- Higher waste risk: rushing sourcing decisions at the last minute

If the fee only smooths timing but doesn't improve decision-making, it may not be worth it. If it helps you take better jobs and handle stock more intelligently, the trade-off can look very different.

For readers who want a basic framework for evaluating service charges more carefully, Comfi's guide to processing fees is a helpful starting point.

How Invoice Discounting Compares to Other Capital Solutions

Most florists don't look at invoice discounting in isolation. They compare it with whatever else is available right now.

That usually means some combination of bank borrowing, credit cards, customer deposits, supplier credit, or waiting and hoping cash catches up. Each option can work. The question is which one fits the way a floral business operates.

Compared with traditional business loans

A loan can make sense when a business wants a larger, longer-term facility for expansion, equipment, or a broader funding need.

But a florist's cash gap is often shorter and tied to a specific order cycle. That's one reason receivables-based tools can feel more natural. The unpaid invoice is directly connected to the cash need.

Compared with business credit cards

Cards are convenient for urgent purchases. They're often used for small stock top-ups, transport costs, and emergency supplier payments.

The downside is behavioural. It's easy to start using a card for structural cash flow problems that are really about slow-paying customers. That can blur the line between short-term convenience and repeated pressure.

Compared with asking for larger deposits

Deposits are useful, especially for weddings and bespoke arrangements. They reduce uncertainty and improve commitment.

But they don't solve every B2B scenario. Some corporate clients, hotels, and event companies work on fixed procurement terms and won't adjust just because your supplier wants cash earlier. In those cases, invoice discounting can be a more realistic response than pushing harder on deposit demands.

The unit economics question

One of the most useful questions in florist invoice financing UAE decisions is whether the tool improves unit economics or only smooths cash flow. That distinction matters in a low-margin, spoilage-sensitive business. Recent UAE market commentary also points to platforms offering accounting integrations, AI checks, and same-day workflows, which makes receivables tools feel more embedded in operations than older manual setups, as discussed in this UAE article on invoice factoring as an alternative to bank loans.

If early cash only helps you survive until the next invoice, be careful. If it helps you buy better, deliver better, and win better clients, that's a different decision.

For many florists, the answer isn't “always use it” or “never use it”. It's “use it when the order quality, margin, and timing all support it”.

Putting It into Practice A UAE Florist Case Study and Checklist

A hypothetical example makes this easier to visualize.

A Dubai florist wins a Ramadan corporate décor contract. The client is reputable and the order is attractive, but payment will come later under business terms. The team needs imported blooms, extra installers, refrigerated transport planning, and backup stems for replacements.

How the decision plays out

Instead of draining reserves, the florist uses invoice discounting against the approved B2B invoice. That gives the business earlier access to cash tied to the job.

Now the owner can make sharper operating decisions:

- commit to better-quality stems rather than cheaper substitutes

- schedule additional event staff without worrying about immediate collection

- keep enough liquidity aside for the next week's regular hotel orders

- avoid turning one large contract into a month of cash stress

The benefit isn't just “more money”. It's better sequencing. The business can fulfill a larger order without knocking the rest of the operation off balance.

The internal discipline that makes it work

This kind of setup works best when the florist tracks each job carefully.

That means separating:

- Customer deposits: these should be treated differently from receivables

- Event-level costs: flowers, labour, delivery, wastage, and venue-specific extras

- Invoice status: issued, approved, disputed, paid, or overdue

If a florist mixes deposits, unpaid invoices, and general cash in one loose system, it becomes harder to judge what can be used.

You can also review Comfi customer case studies to see how receivables-based workflows are used across other business types, even though each sector applies them differently.

A simple preparation checklist

Before applying, get these items ready:

- Your trade license and MOA: make sure the business details are current and readable

- Business bank statement: keep recent records organized and easy to share (past 6 months)

- Emirates ID: front and rear side

- Eligible B2B invoices: use invoices tied to completed, documented work

- Customer details: legal entity name and payment terms should match your records

A florist that prepares these items in advance usually finds the process much less intimidating.

Frequently Asked Questions about Florist Invoice Financing

What's the difference between invoice discounting and factoring

This is the question most owners ask first, and it matters.

Under factoring, the provider often manages collections and has more visibility into your sales ledger. Under invoice discounting, the arrangement is typically more confidential, so the florist keeps control of customer relationships and collections. The trade-off is that invoice discounting usually requires stronger internal accounting discipline, as explained in Trade Finance Global's overview of invoice finance structures in the UAE.

Will my customers know I'm using it

With invoice discounting, they typically may not have the same level of visibility that they would under factoring. That's one reason some florists prefer it, especially when they want to keep the customer experience unchanged.

If preserving a direct relationship with hotels, corporates, and event agencies matters to you, this distinction is important.

What if my client pays late

Late payment doesn't automatically mean disaster, but it does matter.

If your client often pays beyond agreed terms, it can affect whether that receivable is suitable in the first place. That's why florist owners should review not only invoice value, but also the customer's payment behaviour and any history of disputes.

Is this only for businesses in trouble

No. It can be used defensively, but that's not the only use case.

For a florist, it can also be a planning tool. Some businesses use it selectively for large B2B orders, seasonal spikes, or moments when they want to keep reserves free for stock and staffing rather than letting cash sit in unpaid invoices.

When does it make more sense than deposits or supplier credit

Usually when the client won't alter payment terms, the order is documented, and the margin still works after fees.

If a deposit is easy to secure, that may be the simpler route. If a supplier gives generous credit, that can also help. But when neither option fits, invoice discounting can fill the timing gap without forcing awkward client negotiations.

If your floral business is growing but cash keeps getting stuck between delivery and payment, Comfi is one option to explore for invoice discounting in the UAE. It gives B2B businesses a way to access cash from approved invoices through a digital process, which can help florists manage seasonality, perishable stock, and larger order cycles with more control.

Related Reading

- A Practical Guide to Invoice Discounting in the UAE

- 8 Best Accounts Receivable Software for SMEs in 2026

- Inventory Financing vs Invoice Discounting for UAE SMEs

- What Is Accounts Receivable: Your 2026 Guide for UAE SMEs

Ready to improve your business cash flow? Get started with Comfi today.