Days Payable Outstanding: A Guide for UAE & MENA SMEs

You're probably juggling this right now. A supplier invoice is due, customers haven't all paid yet, stock still needs replenishing, and payroll won't wait. If you pay too quickly, cash gets tight. If you pay too slowly, suppliers start chasing and trust slips.

That tension sits at the heart of days payable outstanding, usually shortened to DPO. For SME owners in the UAE and across MENA, it isn't just an accounting ratio. It's a practical way to see how long cash stays in the business before it goes out to suppliers, and whether that timing supports growth or blocks it.

Understanding Days Payable Outstanding

A simple way to think about days payable outstanding is this. It tells you how many days, on average, your business takes to pay supplier invoices.

If you run a trading business in Dubai, for example, your supplier may give you payment terms, but the key question is what happens in practice. Do you typically pay after a few weeks? After a month? Later? DPO captures that payment rhythm in one number.

What DPO looks like in real life

Take an electronics wholesaler. Goods arrive this week, invoices land in finance, and the stock starts moving out to retailers. The owner wants to keep enough cash on hand for the next shipment, but also wants suppliers to keep shipping without friction. If the business pays too early every time, cash leaves the business before sales catch up. If it keeps delaying beyond what suppliers expect, the next order may become harder to secure.

That's why DPO matters. It sits between cash preservation and supplier confidence.

DPO is less about being “slow to pay” and more about being deliberate about when you pay.

A healthy DPO helps an SME answer three practical questions:

- How long are we really taking to pay suppliers

- Does that timing fit our sales cycle

- Are we protecting supplier relationships while keeping enough cash available

Why SME owners often confuse it

Many owners mix up “payment terms” with “actual payment behaviour”. Those aren't always the same.

- Payment terms are what the supplier agreement says

- DPO reflects what your business does on average

That distinction matters. Your terms might say 30 days, but invoice approval delays, inventory turnover, or cash shortages can push the true average higher.

If you already track customer collections, it helps to compare DPO with receivables thinking. This guide on mastering the days sales outstanding calculation to improve cash flow is useful because payables and receivables are two sides of the same liquidity picture.

How to Calculate Days Payable Outstanding

A formula can look more complicated than the business reality behind it.

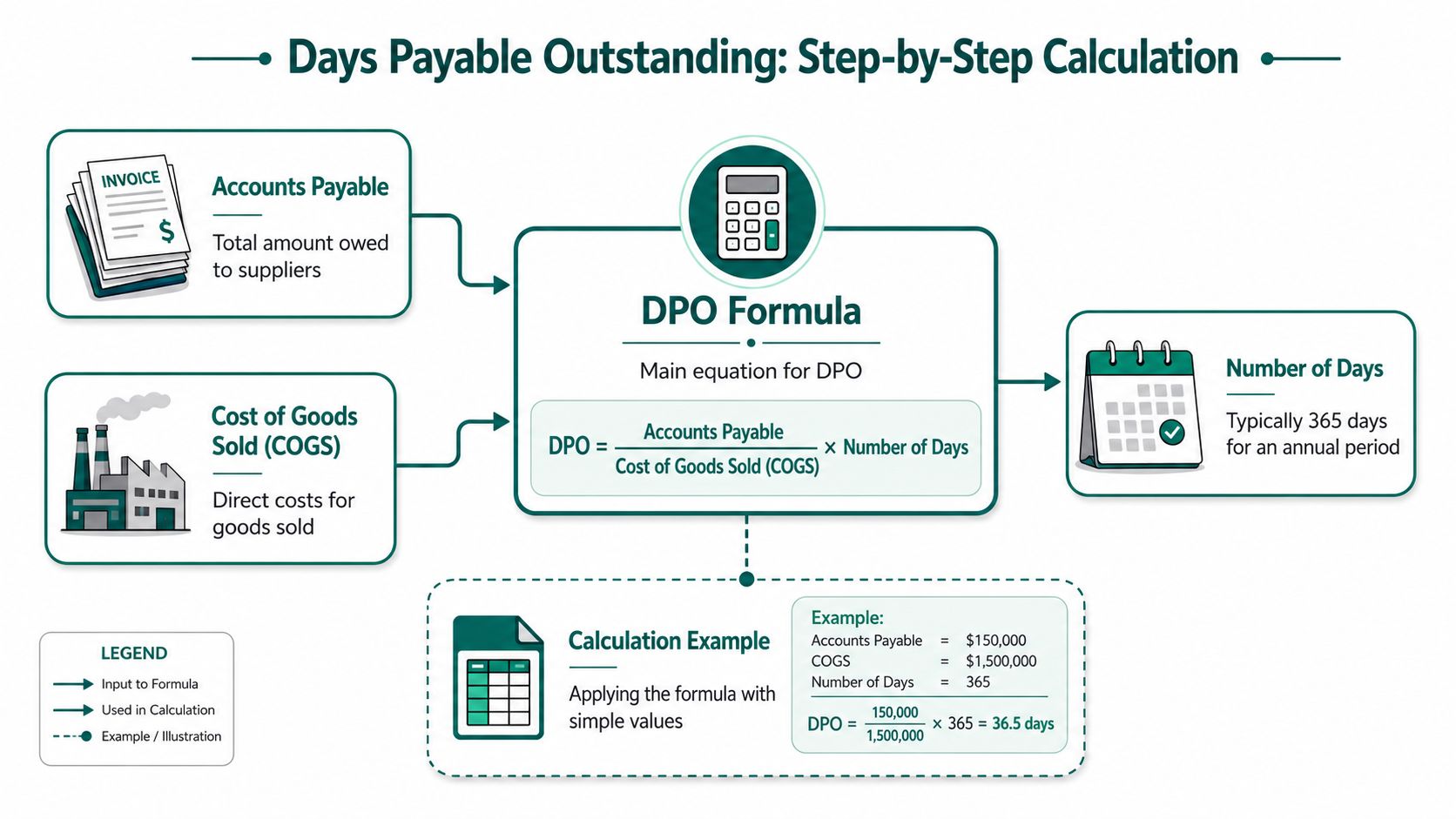

If you run an automotive parts shop in Sharjah or an electronics distribution business in Dubai, the question is simple. How many days, on average, does your company hold supplier cash before paying it out? According to Intuit's explanation of the DPO formula, days payable outstanding measures the average number of days a company takes to pay its suppliers, and it is calculated using the precise formula: DPO = (Average Accounts Payable ÷ Cost of Goods Sold) × Number of Days in the Accounting Period, where the number of days is typically 365 for annual calculations or 90 for quarterly ones.

The formula in plain language

DPO = (Average Accounts Payable ÷ Cost of Goods Sold) × Number of Days

Here's a practical way to read it.

- Average accounts payable is the average amount you owed suppliers during the period.

- Cost of goods sold (COGS) is the cost of the inventory you sold during that same period.

- Number of days is the length of the period you are measuring, usually a year or a quarter.

The formula works like a timing gauge. Accounts payable shows the unpaid supplier balance sitting on your books. COGS shows how much inventory cost moved through the business. Put the two together, and you get a rough measure of how long supplier bills stay unpaid before cash goes out.

A simple worked example

Take a Dubai electronics retailer with steady monthly purchasing.

Assume the business has:

- Opening accounts payable of 100,000

- Closing accounts payable of 140,000

- Annual COGS of 1,460,000

- Accounting period of 365 days

Now calculate it step by step:

- Find average accounts payable

Add opening and closing accounts payable, then divide by 2.

(100,000 + 140,000) ÷ 2 = 120,000 - Divide average accounts payable by COGS

120,000 ÷ 1,460,000 = about 0.082 - Multiply by the number of days

0.082 × 365 = about 30

So the retailer's DPO is about 30 days.

What that number actually tells you

A 30-day DPO does not mean every supplier is paid exactly on day 30. It means that across the full period, the business pays suppliers in about 30 days on average.

That difference matters.

A distributor might pay one key overseas supplier in 45 days, a local service vendor in 15 days, and a freight partner in 30 days. DPO blends all of that into one average. It is a finance dashboard number, not an invoice-by-invoice payment log.

Two points that often confuse SME owners

First, use COGS, not total expenses. Rent, salaries, and marketing costs do not belong in this formula because DPO is about trade payables tied to inventory and supplier purchasing.

Second, make sure the period matches. If you use quarterly accounts payable, use quarterly COGS and a quarterly day count. Mixing annual and quarterly figures gives you a distorted result, which is a common problem in fast-moving sectors such as electronics and automotive trading.

Common calculation mistakes

A few errors show up often in SME reporting:

- Using one accounts payable balance instead of an average. This can skew the result if you made a large stock purchase near period-end.

- Including non-trade payables. VAT payable, loans, or accrued expenses can inflate the number.

- Using inconsistent periods. Opening and closing balances, COGS, and day count should all cover the same timeframe.

- Reading DPO as a target on its own. The number only becomes useful when you compare it with supplier terms, stock turnover, and cash needs.

Quick sense-check: if your DPO looks far higher or lower than the way your business actually pays suppliers, check whether your accounts payable balance includes the right liabilities and whether your COGS period matches.

For MENA SMEs, that final check is especially useful. Large seasonal buys before Ramadan, container delays, and bulk imports for automotive or electronics lines can push payables up at month-end and make a single balance misleading. That is why averaging and period matching matter so much.

Interpreting Your DPO in the UAE and MENA Context

Once you have your number, the next question is obvious. Is it good?

The honest answer is that there isn't one perfect DPO for every business. The right level depends on your sector, stock cycle, supplier relationships, and bargaining power.

A useful benchmark for SMEs

According to Signup Software's review of APQC benchmark data, the average Days Payable Outstanding across all industries globally is approximately 40 days. The same source notes that industries with longer production cycles, such as automotive and electronics, often exhibit higher DPO values, ranging from 45 to 60 days or more.

That matters in the UAE because many SMEs don't operate like simple service firms. Dealers, distributors, and electronics businesses often carry inventory longer and rely heavily on trade relationships.

What a lower DPO may signal

A lower DPO usually means you pay suppliers more quickly.

That can be positive when:

- Supplier trust matters most. Fast payment can strengthen relationships.

- Early payment benefits exist. Some suppliers reward prompt settlement.

- You want smoother supply continuity. Reliable buyers often get better treatment when stock is tight.

But a low DPO can also mean you're letting cash leave too early, especially if customers take longer to pay you than you take to pay suppliers.

What a higher DPO may signal

A higher DPO means cash stays in your business longer before you pay suppliers.

That can help when:

- Inventory takes time to sell

- Cash collections from customers are uneven

- The business needs breathing room between purchase and sale

Still, a high DPO only works if suppliers are comfortable with it. If the number rises because invoices are stuck in approvals or because the business is paying late beyond agreed terms, that's not strategy. That's friction.

How to judge your own number

Use these questions instead of asking whether your DPO is “high” or “low”:

- Does it match our supplier agreements

- Does it fit our inventory cycle

- Is it helping us stay liquid without straining vendor trust

- How does it compare with peers in our own sector

A distributor and a software firm can both be healthy businesses while carrying very different DPO levels. Context matters more than a textbook target.

For MENA SMEs, that context is often practical rather than theoretical. Businesses in automotive and electronics may need more room because goods move through longer stock cycles, while firms with lighter operations may prefer a shorter, cleaner payables pattern.

The Impact of DPO on Liquidity and the Cash Conversion Cycle

DPO becomes much more useful when you stop viewing it as a standalone metric.

Finance teams usually look at it as one part of the cash conversion cycle, or CCC. That cycle tracks how long it takes for money put into stock and operations to return as cash.

Think of the cash cycle like a relay

A simple analogy helps.

- Inventory is the first runner. Cash turns into stock.

- Receivables are the second runner. Stock is sold, but the customer may pay later.

- Payables are the third runner. This is the delay before you pay your own suppliers.

If inventory moves slowly and customers pay slowly, your business needs more cash tied up for longer. DPO can offset some of that pressure by keeping cash inside the business a bit longer before supplier payments go out.

That's why DPO is often described as a liquidity lever. It doesn't create profit on its own, but it affects timing, and timing can decide whether an SME feels stable or stretched.

Why this matters in stock-heavy sectors

In the UAE automotive sector, timing is especially important. According to HighRadius on financial ratios for the automotive industry, DPO has remained disciplined between 61–71 days, reflecting a balance between cash retention and payment reliability. The same source notes that SMEs in this space may be managing inventory cycles up to 180 days.

That tells you something important. In a market where stock may sit for months, paying suppliers too early can choke liquidity. But pushing payables carelessly can disrupt supply.

DPO's effect on day-to-day decisions

When owners feel cash pressure, they often react one invoice at a time. That's understandable, but it can hide the bigger pattern.

A healthier approach is to ask:

- How long is cash tied up in stock

- How quickly do customers pay

- How long do we hold supplier payments within agreed terms

Those three timings work together. If one worsens, another may need to adjust.

For a practical explanation of how these moving parts connect, this guide to the cash conversion cycle is worth reading.

Longer isn't always better

A common misunderstanding is that a longer DPO always improves liquidity. It can help in the short run, but only when it's intentional and sustainable.

If your business extends payables because approvals are delayed, disputes are unresolved, or cash is already under strain, the DPO number may look stronger while the business becomes weaker.

That's why finance managers look beyond the ratio itself. They want to know whether the number reflects a clear commercial choice or a process problem.

A practical way to use it

Review DPO alongside your real operating cycle:

- If stock turns slowly, you may need more room before supplier payments go out.

- If customers pay promptly, you may not need to stretch payables as much.

- If supplier trust is critical, preserving reliability may be worth more than a few extra days of cash retention.

Used this way, DPO becomes less of a score and more of a planning tool.

Actionable Strategies to Manage and Optimize Payables

Most SMEs don't struggle with DPO because they've never heard the formula. They struggle because daily operations get in the way. Approvals sit with managers, invoices arrive in different formats, stock arrives before paperwork is clean, and suppliers all work on different terms.

That's why better payables management starts with process discipline, not spreadsheet tricks.

Start with supplier terms, not internal habit

Many SMEs pay according to routine rather than strategy. Someone in finance gets nervous about overdue invoices and releases payment early. Another invoice gets held too long because there's no clear owner. Over time, DPO becomes accidental.

A better approach is to reset around agreed supplier terms and business reality.

Here's what that looks like:

- Map supplier groups clearly. Separate critical suppliers from flexible ones. You may want tighter discipline with key stock providers and a different cadence for non-core vendors.

- Match terms to stock movement. If goods sell quickly, shorter terms may be workable. If inventory sits longer, the payment timetable should reflect that cycle.

- Record what was agreed. A surprising number of payment problems come from informal arrangements that no one documents properly.

Clean up the invoice journey

A DPO problem is often an invoice-processing problem in disguise.

If invoices move through email chains, WhatsApp messages, or manual sign-off, finance loses visibility. Some invoices get paid late for no strategic reason. Others get paid early because teams want them off the desk.

Focus on the mechanics:

- Standardise invoice intake so all supplier invoices enter one workflow.

- Set approval rules by amount, supplier, or department.

- Flag exceptions early when a PO, goods receipt, or quantity mismatch is holding payment back.

- Run a weekly payable review so finance and operations see the same pipeline.

Operational rule: if you can't explain why an invoice is unpaid, your DPO is being shaped by process gaps, not policy.

Decide when early payment is actually worth it

Some suppliers value fast payment enough to offer better commercial terms. Others don't. Don't assume every early payment is wise, and don't assume every delay helps.

Ask three things before paying early:

- Does this improve margin or access to stock

- Is this supplier strategically important

- Can the business spare the cash without creating pressure elsewhere

This turns payment timing into a deliberate choice.

Build a payment calendar around cash reality

A practical payable strategy needs a schedule. Without one, payment decisions become reactive.

Useful habits include:

- Batching payment runs on planned dates

- Reviewing large invoices separately from routine payments

- Aligning supplier payments with expected collections

- Escalating disputes quickly so legitimate invoices don't sit unresolved

These aren't flashy changes, but they reduce noise. Once finance can predict outgoing payments with more confidence, DPO becomes easier to manage.

Use tools that reduce the buyer-supplier tension

SMEs often face a trade-off. The buyer wants more time to pay. The supplier wants certainty and speed. Traditional payables processes don't resolve that tension well.

Modern payables tools can help structure it more cleanly. In the UAE, many finance teams are exploring options that let buyers extend payment timing through a Buy Now, Pay Later structure while helping suppliers receive payment promptly. For owners thinking about how to approach those conversations, this article on how to get extended payment terms from suppliers in the UAE gives a practical starting point.

Some businesses also use invoice discounting on the supplier side to improve cash flow across the supply chain, especially where one side of the transaction needs speed and the other needs flexibility. The important point isn't the label. It's that the business should look for structures that preserve supplier confidence while giving the buyer room to operate.

A practical checklist for SME finance leaders

If you want to improve DPO without damaging relationships, focus on these actions first:

- Review your top suppliers and note actual payment behaviour against agreed terms.

- Segment invoices by priority so essential stock suppliers don't get lost in the same queue as low-impact vendors.

- Fix approval bottlenecks that create accidental delays.

- Set internal payment rules instead of relying on habit.

- Track trends monthly so you can spot drift before suppliers do.

Most of the gains come from consistency. Businesses rarely improve payables because of one dramatic policy change. They improve because finance, procurement, and operations start acting on the same timetable.

Common DPO Pitfalls and Key Metrics to Monitor

A lot of advice makes it sound like a higher DPO is always smarter because cash stays in the business longer. That's too simplistic.

According to Aspire's guide to days payable outstanding, a DPO value of 30 to 45 days is generally considered standard across many businesses and industries in the UAE and MENA region, though it varies by sector. The same source notes that low DPO of 15 to 30 days often signals early payment habits that build supplier trust and may secure early payment discounts, while higher DPO suggests cash is being retained longer.

Pitfalls that catch SME owners

Some warning signs are easy to miss:

- Late payment disguised as strategy. If DPO rises because invoices are overdue beyond agreed terms, suppliers will notice before your dashboard does.

- Missed early payment opportunities. Some suppliers reward reliability. If you stretch every payment, you may lose commercial advantages.

- Overreliance on one metric. DPO can look healthy even while approvals are messy or supplier disputes are increasing.

Metrics worth watching alongside DPO

Treat DPO as one part of a finance dashboard, not the whole dashboard.

Keep an eye on:

- Accounts payable turnover. This helps you see how often payables are settled over a period.

- Current ratio. It gives a broader view of short-term liquidity.

- Invoice ageing by supplier. This shows whether delays are concentrated with specific vendors.

- On-time payment performance. This reveals whether your DPO reflects disciplined timing or missed commitments.

Keep one eye on process trends

Payables management is also changing quickly in the region. If you want a broader operations view, this piece on the future of AP services in the UAE offers useful context on where accounts payable practices are heading.

Healthy DPO management means paying neither as fast as fear suggests nor as late as cash pressure allows. It means paying on purpose.

The best finance leaders don't chase the highest possible DPO. They aim for a number that fits the business model, protects supplier trust, and keeps operations moving.

If you want a simpler way to manage payables, free up cash tied up in stock and invoices, and give buyers more flexible payment timing without creating friction for suppliers, explore Comfi. It supports SMEs across MENA with tools including Invoice Discounting, Buy Now, Pay Later (30/60/90 days), and Automotive Dealer Financing, all built for fast-moving sectors such as automotive, electronics, retail, and distribution.