Mastering the Days Sales Outstanding (DSO) Calculation to Improve Cash Flow

Days Sales Outstanding, or DSO, is a straightforward yet powerful financial metric. It tells you, on average, how long it takes for your business to collect payment after a sale is made. The days sales outstanding calculation reveals the exact amount of time your cash is tied up in accounts receivable instead of being available for you to use. A higher DSO number means a longer wait for your money, which can significantly impact your business operations.

What Days Sales Outstanding Really Means for Your Business

For suppliers and wholesalers across the MENA region, DSO isn't just another number on a spreadsheet. It’s a direct measure of your company’s financial health—think of it as a vital sign for your cash flow.

When your DSO is high, it means your working capital is trapped in your accounts receivable. That's cash you can't use to buy new inventory, cover payroll, pay your own suppliers, or jump on a new growth opportunity. This situation can quickly lead to a cash crunch, even for profitable companies.

Why Tracking DSO is a Business Imperative

Keeping a close eye on your DSO gives you the clarity needed to make smarter, more proactive financial decisions. It’s not just about knowing a number; it’s about understanding the story that number tells about your business's efficiency and customer payment behaviour.

By consistently monitoring this metric, you can gain valuable, practical insights:

- Forecast Cash Availability: A stable or improving DSO makes it much easier to predict when cash will actually hit your account. This makes budgeting and planning far more reliable.

- Spot Collection Problems Early: Did your DSO suddenly jump? That’s an early warning sign that something is broken in your collections process, giving you a chance to fix it before it spirals.

- Gauge Your Credit Policies: DSO shows you the real-world impact of your payment terms. It helps you see if your trade credit policies are effective or if they need adjustment.

- Maintain Operational Stability: At its core, knowing how quickly you turn sales into cash is fundamental to keeping the lights on and the business running smoothly day-to-day.

Simply put, a low DSO means your collections are efficient and your cash flow is healthy. A high DSO, on the other hand, often signals liquidity problems on the horizon. It’s one of the most honest KPIs for your credit and collections team.

Ultimately, getting a handle on your DSO isn't just a task for the finance department. It's a strategic necessity that directly impacts your ability to operate, meet your obligations, and grow in a competitive market.

How to Perform an Accurate DSO Calculation

Before you can start improving your DSO, you first have to know how to calculate it accurately. The good news is that the standard formula is straightforward and provides a clear snapshot of your payment collection efficiency.

Here’s the most common DSO formula you'll see:

DSO = (Accounts Receivable / Total Credit Sales) x Number of Days in Period

In simple terms, this calculation tells you the average number of days it takes to turn a sale on credit into actual cash in the bank. Understanding each component of this equation is key to getting a meaningful result.

Breaking Down the Formula Components

A reliable days sales outstanding calculation is only as good as the numbers you plug into it. Using incorrect data will produce a misleading result, which could lead to poor financial decisions down the road.

Let's quickly go through each piece of the puzzle:

- Accounts Receivable: This is the total amount of money your customers owe you for goods or services they have already received but have not yet paid for. For an accurate calculation, use the accounts receivable balance from the end of the period you are measuring (e.g., the last day of the month or quarter).

- Total Credit Sales: This is a crucial point. You must only include sales made on credit. Do not use your total sales figure. Cash sales are paid immediately and do not affect collection times. Including them will artificially lower your DSO and give you a false sense of security.

- Number of Days in Period: This corresponds to the timeframe you are analysing. For a monthly DSO, you’ll use 30 or 31 days. For a quarterly calculation, it's typically 90, and for an annual snapshot, you'd use 365.

By specifically focusing on credit sales, the formula zeroes in on how well your credit and collections process is actually performing, providing a true measure of efficiency.

A More Advanced Method for Seasonal Businesses

The standard formula is great for a quick health check, but it can be misleading for businesses with significant seasonal swings in sales. For example, a massive sales spike in one month could make your DSO look temporarily worse, even if your collections team is performing well.

To get a more stable and realistic view, many finance professionals use a rolling-average or "countback" method. This involves looking at your accounts receivable against sales month by month, working backwards.

This approach smooths out those peaks and valleys, giving you a more nuanced picture of your collection performance over time. It prevents one unusual month from skewing your perception. For businesses here in the MENA region with distinct peak seasons—perhaps tied to holidays or major local events—this adjusted DSO calculation offers a much truer look at your underlying financial health. It ensures your big decisions are based on a consistent trend, not a short-term blip.

Putting the DSO Calculation into Practice

Theory is one thing, but seeing the days sales outstanding calculation in action is where it all clicks. Let's crunch some numbers with a few real-world examples to show you what this looks like for a typical SME.

We'll use the formula we discussed: DSO = (Accounts Receivable / Total Credit Sales) x Number of Days.

A Standard 30-Day Cycle

Let's say your business offers standard 30-day payment terms. In March, you made AED 150,000 in credit sales. At the end of the month, your accounts receivable balance stood at AED 160,000.

Plugging those numbers into the formula, you get:

(160,000 / 150,000) x 30 = 32 days.

A DSO of 32 isn't bad at all. It means, on average, your customers are only taking an extra two days to pay. This suggests your collections process is working quite effectively.

For Businesses with 60 or 90-Day Terms

Things get more interesting when you offer longer payment terms—a common strategy in the UAE to win bigger contracts. This is where keeping a close eye on your DSO is absolutely critical for managing cash flow.

Let's see how the math plays out for these longer cycles:

- A 60-Day Example: Imagine your credit sales over a 60-day period were AED 300,000, and your receivables at the end of that time were AED 325,000. Your DSO would be (325,000 / 300,000) x 60 = 65 days. This tells you collections are slipping by about five days.

- A 90-Day Example: Over a 90-day period, you had AED 450,000 in credit sales and AED 480,000 in outstanding receivables. The calculation is (480,000 / 450,000) x 90 = 96 days. Again, a slight delay, but now you have a clear number to track against.

These examples show how your credit policy directly shapes your cash flow timeline. Your DSO isn't just a metric; it's the story of when your hard-earned revenue turns into actual cash you can use. This is a key piece of your company's overall efficiency, which ties directly into the cash conversion cycle.

Getting your DSO number is just the first step. The real value comes from what you do with it. You have to interpret the data and take action, much like how you would transform data into actionable decisions with a robust business intelligence report. This single calculation gives you a powerful baseline for tightening up your credit policies and building a stronger financial foundation.

What a Good DSO Looks Like in the UAE

So you’ve run the days sales outstanding calculation, and now you have a number. What does it actually tell you? A DSO of 45 days might be fantastic for one company but a massive red flag for another.

The honest answer is that there’s no universal "good" DSO. The right number for your business is a moving target, shaped by your industry, your clients, and most importantly, your local market. If you're running a business in the UAE or the wider MENA region, trying to match global averages will only lead to unrealistic expectations and frustration.

Understanding Regional and Industry Benchmarks

When it comes to DSO, context is king. Payment cycles and credit terms can look completely different from one sector to the next, often depending on the size of your buyers and the standard practices within your industry.

For instance, a high DSO might scream "inefficient collections" in one field, but in another, it’s just the cost of doing business with large corporate or government clients. Getting a handle on these nuances is the first real step toward setting achievable targets for your accounts receivable team. You need to know what’s normal in your world before you can decide what’s good for your business.

A "good" DSO is one that is at or below the average for your specific industry in the UAE, while still supporting your sales efforts. It reflects a balance between offering competitive credit terms and maintaining healthy cash flow.

The DSO Reality for SMEs in the UAE

Let's be frank: long payment cycles are a structural reality in the UAE's B2B world. Recent data reveals that DSO in key sectors like chemicals, agri-food, and textiles has crept past 100 days. That's a huge jump from the 2023 global average of 59 days.

This is often driven by the standardized, and sometimes slow, payment processes of large corporations and government bodies. For an SME supplier with AED 1 million in monthly credit sales, a DSO of 100 days means over AED 3.3 million is constantly tied up in unpaid invoices. This has a direct and serious impact on your liquidity and ability to grow.

This is exactly why getting a grip on your DSO is a strategic must-do for any business here. You can learn more about the credit risk exposure for MENA manufacturers to understand the broader context.

So, where should you be aiming?

- Research your industry: Find reliable data on the average DSO for your specific sector in the UAE. This gives you a realistic benchmark.

- Check against your terms: Your DSO should ideally hover close to the payment terms you offer. If you give clients 60 days to pay but your DSO is consistently 90, there’s a clear gap in your collections process that needs fixing.

- Watch the trend: More important than any single number is how it changes over time. A DSO that is steadily decreasing is a sign that your efforts to improve cash flow are working.

Ultimately, a good DSO is about hitting that sweet spot between operational efficiency and financial stability, all within the unique business environment of the MENA region.

Proven Strategies to Lower Your DSO

A high Days Sales Outstanding (DSO) isn't just a number on a spreadsheet; it's a direct reflection of how quickly your hard-earned revenue turns into actual cash. The good news is, you have more control over it than you might think. Bringing that number down is one of the fastest ways to improve your cash flow and put money back into your business where it belongs.

It all boils down to a mix of smarter internal habits and embracing modern financial tools. You don't need to reinvent the wheel—often, small, consistent changes have the most significant impact on your payment cycle.

Strengthening Your Internal Processes

Your invoicing and collections workflow is the bedrock of a healthy DSO. Every single delay, error, or moment of confusion can easily add days—or even weeks—to how long it takes you to get paid. Think of streamlining this process as your first and most powerful line of defense.

It starts before you even make a sale. Get your credit policies crystal clear upfront. Your payment terms should be explicitly stated in every contract and proposal so there are absolutely no surprises down the line.

From there, it’s all about speed and precision.

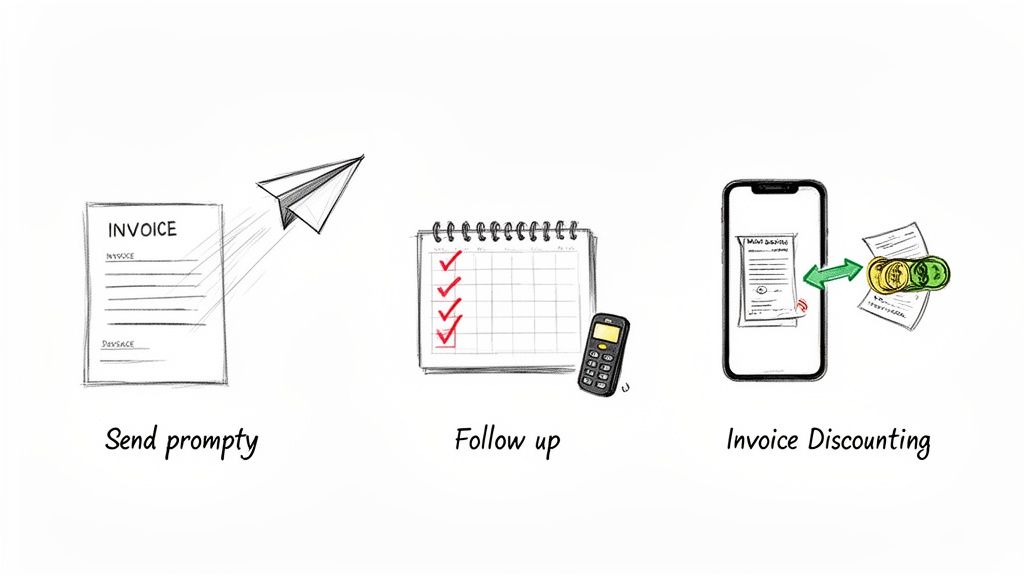

- Invoice Immediately: Don't wait. Send invoices the moment goods are delivered or services are completed. Any delay on your end automatically pushes back your payment date.

- Ensure Accuracy: Double-check every invoice for the correct PO numbers, line items, and contact details. A simple typo can send an invoice into a lengthy dispute and approval loop.

- Establish a Follow-up Cadence: Don't just sit back and wait for the due date to pass. A friendly reminder a few days before an invoice is due can keep you top of mind. For a more hands-off approach, you might explore an automated invoice system to handle this for you.

Bridging the Cash Flow Gap

Even with a perfect internal system, the long payment terms common in the MENA region can put a serious strain on your operations. This is where modern solutions can be a game-changer, allowing you to get paid on your schedule, not your customer's.

Platforms that offer invoice discounting, like Comfi, provide a powerful way for businesses to turn outstanding accounts receivable into immediate, usable cash. Instead of waiting 60, 90, or even 120 days for a customer to pay, you can access the value of your invoices within hours.

This strategy effectively decouples your cash flow from your clients' payment cycles. By selling your unpaid invoices at a small discount, businesses have been able to unlock the capital tied up in them, giving them the liquidity to pay suppliers, manage payroll, or seize new growth opportunities. It’s a strategic move that directly relieves the pressure caused by a high DSO. Beyond just this one metric, a broader understanding of mastering cash flow management is crucial for long-term stability.

Recent regional data shows this kind of optimization is making a real difference. Despite economic headwinds in 2024, businesses in the Middle East improved working capital by an average of six days, bringing the regional net working capital days down to 101.7. The UAE, in particular, has shown that enhanced collection efficiency is entirely possible. For an SME, trimming even a few days off your DSO can unlock significant capital and give you a powerful competitive edge. You can see more insights from PwC's Middle East working capital study to benchmark your own performance.

Got Questions About DSO? We've Got Answers

When you start digging into the days sales outstanding calculation, a few common questions always seem to pop up. Getting clear on these points is crucial for using the metric correctly and making smart moves for your business's financial health.

Let's walk through some of the most frequent queries we get from SMEs just like yours.

How Often Should I Be Calculating DSO?

For most small and medium-sized businesses, running the numbers monthly is the sweet spot. This gives you a regular, up-to-date look at how well you're collecting payments and helps you catch any worrying trends before they spiral. Plus, a monthly calculation fits right in with your other financial reporting, so it's easy to make it part of the routine.

Now, if your sales tend to swing wildly or you're in the middle of a major growth spurt, you might even want to calculate it weekly. When things are changing fast, a more frequent check-in gives you much tighter control over your cash flow.

Can My DSO Actually Be Too Low?

It might sound strange, but yes. While a low DSO is almost always a good thing, an extremely low number can sometimes be a sign that your credit policies are too tight. Are you potentially scaring off perfectly good customers who just need a little more flexibility?

Think about it: if you're demanding payment in 15 days while all your competitors offer standard 30-day terms, you could be losing out on sales. The goal isn't just to hit the lowest DSO possible. It's about finding that perfect balance—getting paid promptly without putting a brake on your sales growth.

A DSO that looks "too good to be true" might signal overly strict credit terms. The real win is finding the equilibrium between efficient collections and offering competitive payment options that keep customers coming back.

Nailing that balance is what sustainable growth is all about.

How Do Seasonal Swings Impact My DSO Calculation?

Seasonality can really throw a wrench in your DSO numbers if you're not paying attention. A huge month of credit sales followed by a naturally slower collection period can make your DSO shoot up, triggering a false alarm. It doesn't mean your collections process is failing; it's just the normal rhythm of your business cycle.

To get a clearer, more stable picture, try these approaches:

- Use a rolling average: Instead of just looking at one month, calculate your DSO over a longer timeframe, like a rolling 90-day or 12-month period. This helps smooth out the peaks and troughs.

- Compare year-over-year: Look at your DSO for June and stack it up against your DSO from last June. This simple comparison helps you analyze your performance in the right seasonal context.

By making these small adjustments, you can be sure you're reacting to real trends, not just temporary blips on the radar.

Ready to take control of your cash flow and shrink that DSO? Comfi helps businesses unlock working capital by turning unpaid invoices into cash in the bank. Find out how you can get paid faster and pour fuel on your growth.

Related Reading

- How Can MENA SMEs Master Working Capital?

- Staffing Agency Payroll Financing UAE: Boost Cash Flow 2026

- SME Cash Flow Management: A Guide for MENA Businesses

- Improve Working Capital for UAE IT Services Business

Looking to improve your cash flow? Explore Comfi's Invoice Discounting solutions. Get started today.