Credit Period: A Practical Guide to Mastering Payment Terms for Stronger Cash Flow

In business-to-business (B2B) transactions, a credit period is the agreed-upon time a supplier gives a buyer to pay for goods or services they have already received. Instead of demanding immediate payment, the seller offers a window—often 30, 60, or 90 days—for the buyer to settle the invoice. Offering this flexibility is a common and often essential practice for winning customers and staying competitive.

Understanding the Basics of a Credit Period

At its core, a credit period is a simple agreement that facilitates commerce. Instead of demanding cash on delivery, the seller provides a specific timeframe for payment. This practice is the lifeblood of B2B transactions, particularly for suppliers and wholesalers who need to move large volumes of goods.

For a practical example, consider a local grocery store that supplies fresh produce to a nearby café. The café receives daily deliveries to make its food and drinks but pays the total bill at the end of the week. That seven-day window is their credit period. It allows the café to convert those ingredients into revenue-generating products before paying its supplier.

Why Offer a Credit Period?

Giving customers extra time to pay isn't just a courtesy; it's a powerful business strategy. For suppliers, it can be the deciding factor that wins a major contract or forges a long-term partnership with a key client.

Here’s why it’s so widespread:

- Competitive Edge: If your rivals offer flexible payment terms, you likely need to as well just to be considered.

- Larger Sales Volumes: Buyers can often commit to bigger orders when they aren't required to pay for everything upfront, boosting your sales figures.

- Customer Loyalty: Trust and flexibility are the foundation of strong, lasting business relationships. A fair credit period demonstrates that you are a supportive partner.

A credit period is essentially a short-term, interest-free arrangement that fuels commerce by allowing businesses to buy now and pay later, aligning their expenses with their revenue cycle.

This entire arrangement is a form of trade credit, a concept that acts as the backbone of B2B commerce. Understanding this foundational idea is the first step toward mastering your company’s cash flow and making smarter financial decisions.

How Credit Periods Impact Your Working Capital

Offering generous credit terms is a classic way to win new customers and build loyalty. While it's an effective sales tool, every time you give a customer 30, 60, or 90 days to pay, you directly impact your working capital—the cash you need to run your business day-to-day.

Think of it this way: every day you wait for a payment, that cash is tied up on your books as "accounts receivable." It’s money you have earned but cannot use to buy more inventory, pay your team, or cover rent. This delay creates a "cash flow gap." You’ve already paid your own suppliers and covered operational costs, but the revenue from that sale is still just an entry on an invoice.

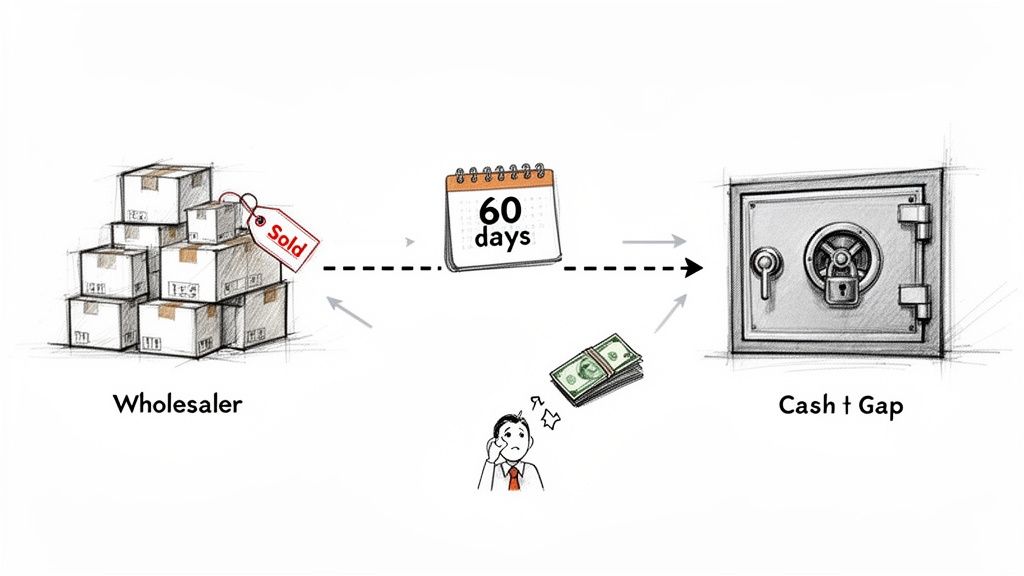

The Wholesaler's Dilemma: A Practical Example

Imagine you're an electronics wholesaler and you’ve landed a huge order with a major retailer, offering them Net 60 terms. On paper, it’s a fantastic, profitable deal. In reality, for the next two months, that cash is completely out of reach. This is a daily challenge for small and medium-sized enterprises (SMEs) everywhere.

During this 60-day waiting period, you're left juggling serious challenges:

- Paying Your Own Suppliers: The factories you source from probably demand payment in 30 days or less.

- Meeting Payroll: Your team needs to be paid on schedule, regardless of when your customers settle their invoices.

- Seizing Growth Opportunities: A hot new product might hit the market, but without cash on hand, you can’t make the investment to stock it.

This is how a business can be profitable on paper but still find itself under constant financial stress. This system of credit is a major engine of the economy. In the UAE, for instance, domestic credit provided by the financial sector was 79.49% of GDP in 2022, highlighting how deeply these payment arrangements are integrated into business operations.

The longer the credit period, the wider the cash flow gap. This gap is the critical time between spending money to create a product or service and actually getting paid for it.

Closing this gap is one of the most important aspects of managing your company’s financial health. To better understand how these moving parts fit together, you can learn more about the cash conversion cycle in our detailed guide. When you manage your credit periods effectively, you're not just collecting payments—you're unlocking the working capital that fuels your growth.

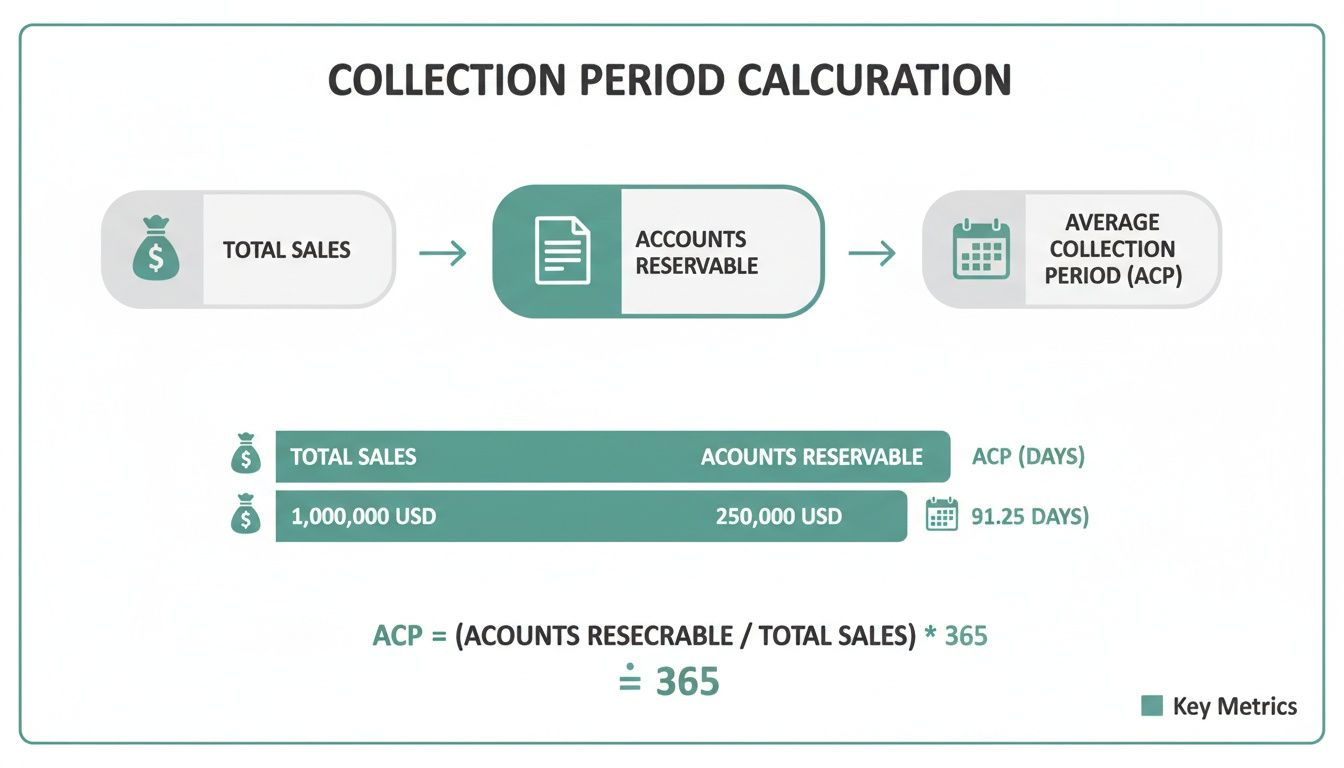

How to Calculate Your Average Collection Period

Your official credit period is Net 30. That’s what’s written on the invoice. But the real question every business owner needs to ask is: how long does it actually take to get paid?

This is where your Average Collection Period (ACP) comes in. Also known as Debtor Days, this metric provides an honest, data-driven look at the health of your accounts receivable and its true impact on your cash flow.

Calculating your ACP isn’t just an accounting exercise; it’s about uncovering the gap between your stated payment terms and your financial reality. If you offer a 30-day credit period but your ACP is 65 days, that’s a major red flag indicating that your collections process needs a serious review.

The Simple Formula for ACP

To calculate your average collection period, you need two key figures from a specific timeframe, such as a quarter or a full year: your total credit sales and your average accounts receivable.

The formula is:

(Average Accounts Receivable / Total Credit Sales) x Number of Days in Period = Average Collection Period

Here's a quick breakdown of each component:

- Average Accounts Receivable: The average amount of money customers owed you during the period. Calculate it by adding your starting and ending accounts receivable balances for the period and dividing by two.

- Total Credit Sales: The total value of all sales made on credit during that same timeframe. Be sure to exclude any cash sales.

- Number of Days in Period: The number of days in the period you're measuring (e.g., 90 for a quarter, 365 for a year).

Putting It Into Practice

Let’s run through a quick example. Imagine you’re a B2B food supplier looking at your numbers from the last quarter (90 days).

- Your starting accounts receivable was AED 40,000.

- Your ending balance was AED 60,000.

- Your total credit sales for the quarter came to AED 300,000.

First, find your average accounts receivable:

(AED 40,000 + AED 60,000) / 2 = AED 50,000

Now, plug everything into the ACP formula:

(AED 50,000 / AED 300,000) x 90 days = 15 days

This calculation shows it takes your business, on average, just 15 days to collect payments. If you're offering Net 30 terms, this is fantastic news for your working capital. You’re getting paid well ahead of schedule.

If your ACP is running higher than your standard credit period, it’s a clear signal to act. To get your collection metrics back on track, it's worth exploring practical strategies on how to collect unpaid invoices effectively.

Understanding Common Payment Terms: Net 30, 60, and 90

In the B2B world, you’ll see terms like Net 30, Net 60, and Net 90 on nearly every invoice. This isn’t just accounting jargon—it’s the language of trade credit. A firm grasp of what these terms mean is the first step to managing your cash flow and customer expectations effectively.

Each term represents a distinct strategic choice. Net 30, where payment is due within 30 days, is often the standard for smaller, repeat orders with trusted clients. It strikes a good balance, allowing you to stay competitive without putting your working capital under excessive strain.

The Strategic Trade-Offs of Longer Terms

Net 60 and Net 90 are a different matter. These longer credit periods are often expected by larger corporate clients, especially for high-value contracts. Offering 60 or 90 days to pay could be the very thing that helps you land a major deal and scale your business.

But that flexibility comes at a cost. The longer you wait to be paid, the more pressure you put on your own finances. Buyers often prefer these terms because it helps them manage their inventory and sales cycles. In reality, they're shifting the cash flow burden directly onto you, the supplier.

Offering a longer credit period is a strategic trade-off. It can secure larger clients and boost sales, but it dramatically increases the time your working capital is tied up in accounts receivable.

This isn't just a local trend; it's a global business reality. The infographic below shows you how to calculate your collection period, which is the perfect way to see the real-world impact these terms have on your business.

This calculation helps you determine the actual time it takes to convert a sale into cash—one of the most vital metrics for any supplier. To set these terms effectively, you must understand the different aspects of invoice payment terms Australia, from standard practices to legal requirements. Knowing how to meet customer demands without taking on unsustainable risk is key to long-term success.

How to Manage Credit Risk and Protect Your Cash Flow

Offering generous credit terms is an excellent way to win business, but it shouldn't jeopardize your own cash flow. The solution isn't to stop offering credit; it's to manage the associated risk proactively. You need to shift from reacting to payment issues to implementing a solid strategy that protects your company from the outset.

This starts with a robust credit policy. Before agreeing to any payment terms, you need a clear, consistent method for evaluating customer risk. This isn't about creating barriers for your customers; it's about making smart, informed decisions that keep your business financially healthy. Your credit policy is your first line of defense against late payments and bad debt.

Building Your Credit Management Framework

A strong credit policy is built on several core practices working together. Each component plays a specific role in minimizing risk while allowing you to offer the competitive payment terms your customers expect.

Get started by implementing these fundamentals:

- Run Customer Credit Checks: Before agreeing to terms, do your due diligence. This could involve requesting trade references, reviewing payment history with other suppliers, or using a credit reporting agency to get a clear picture of a new customer's financial reliability.

- Set Clear and Consistent Terms: Ensure every invoice clearly states the credit period (e.g., Net 30), the exact due date, and any penalties for late payments. Consistency eliminates confusion and sets clear expectations from the start.

- Create a Structured Collections Process: Don't wait for an invoice to become 60 days overdue. Map out a clear follow-up process, perhaps starting with a friendly reminder before the due date and escalating to more direct communication after it passes.

By putting these foundational pieces in place, you stop hoping for on-time payments and start actively managing your credit risk. This simple shift is absolutely critical for maintaining healthy working capital.

Modern Solutions for Immediate Cash Flow

Even with the best credit policy, waiting 30, 60, or 90 days for payment creates a cash flow gap. Modern platforms can help close that gap, enabling you to offer attractive extended terms without feeling the financial strain. One powerful option is invoice discounting.

With a platform like Comfi, you can submit an approved invoice and receive the cash in your bank account in as little as 24 hours. This eliminates the waiting period, giving you immediate access to your working capital. This approach is becoming a go-to for businesses looking to sidestep the risks of long payment cycles.

By combining smart, traditional risk management with modern tools, you can confidently offer competitive credit periods, knowing your cash flow is secure. To learn more, check out our complete guide on how to manage B2B payment risk.

Got Questions About Managing Credit?

Even with a good handle on credit periods, practical questions often arise when applying these concepts to your daily business operations. Here are straightforward answers to the most common queries we hear from SME owners and finance managers.

How Do I Decide Which Credit Period to Offer Customers?

Choosing the right credit period is a balancing act. You must consider industry standards, your customer's reliability, and—most importantly—your own cash flow needs. A good first step is to research what your direct competitors are offering. You need to be in the same ballpark to stay competitive, but that doesn't mean you should be reckless.

For new clients, it’s wise to start with shorter terms, like Net 15 or Net 30, after conducting a basic credit check. As you build trust or when dealing with larger, more established companies, you might need to offer longer terms like Net 60 to win or retain their business. The golden rule is to always assess your own working capital first to ensure you can comfortably manage the delay in payment.

What's the Difference Between a Credit Period and a Credit Limit?

They are two distinct tools that work together to manage your risk. Think of it this way:

- A credit period is the when—the timeframe for payment (e.g., your customer has 30 days to pay you).

- A credit limit is the how much—the maximum amount of debt you'll allow that customer to accumulate at any one time (e.g., a total outstanding balance of AED 50,000).

For example, you might offer a key client a Net 30 credit period with an AED 20,000 credit limit. This means they must pay each invoice within 30 days, and their total unpaid balance can never exceed AED 20,000. Setting both is fundamental to any solid risk management plan.

The credit period controls the timeline, while the credit limit controls the exposure. Both are vital parts of a strong credit policy that shields your business from potential losses.

Should I Offer Discounts for Early Payments?

Absolutely—offering an early payment discount can be a fantastic way to accelerate your cash flow. The most common structure is something like "2/10, n/30." This means you offer a 2% discount if the invoice is paid within 10 days; otherwise, the full amount is due in 30 days.

This gives your customers a clear financial incentive to pay you sooner, putting cash back into your business where it can be used. The only consideration is the cost. Does the benefit of receiving cash early outweigh the profit you're giving away in the discount? For businesses with tight margins, the cost of that discount might be too high, making other solutions a better fit for unlocking working capital.

By mastering your credit management, you can build stronger customer relationships and accelerate your growth. Comfi helps suppliers achieve this by providing immediate access to cash from your invoices, allowing you to offer competitive payment terms without the long wait. Learn how Comfi can help you unlock your working capital today.

Related Reading

- How Comfi’s B2B Buy Now Pay Later Solution Enhances Cash Flow for Businesses in the UAE

- How Can MENA SMEs Master Working Capital?

- Deferred Payment for Business Purchases UAE: A Guide 2026

Looking to improve your cash flow? Explore Comfi's Buy Now Pay Later and Invoice Discounting solutions. Get started today.