What is Trade Credit: A Practical Guide to Boost Cash Flow

At its core, trade credit is a simple, yet powerful, B2B arrangement. It’s when a supplier provides a customer with goods or services upfront but allows them to pay later. Think of it as a short-term, interest-free payment deferral that keeps the entire supply chain moving smoothly. This is one of the oldest and most fundamental practices in global commerce, built on a foundation of trust between businesses.

Understanding Trade Credit for Your Business

You can think of trade credit as a professional IOU. It’s not a formal loan from a bank, but a flexible payment understanding directly between a seller and a buyer. This simple concept is the foundation of countless B2B relationships.

The arrangement benefits both sides. For the buyer, it means getting the inventory or materials they need right away without having to part with cash on the spot. This is a game-changer for managing daily operations and jumping on new opportunities without delay.

The Two Sides of the Agreement

For the supplier, offering trade credit is a fantastic way to win business. It can lead to bigger orders and helps build the kind of strong, loyal relationships that last for years. By being flexible, suppliers make themselves the easy choice for their clients, encouraging repeat business.

Here’s a breakdown of how it works:

- The Buyer: Gets the goods now and pays the invoice later, typically within 30, 60, or 90 days.

- The Supplier: Provides these deferred payment terms, effectively giving the buyer a chance to use or even sell the goods before the bill is due.

This simple delay in payment is a critical lubricant for the economy. It gives small and medium-sized businesses (SMEs) the breathing room they need to manage their finances, stock up on inventory, and grow in ways that would be impossible otherwise.

Ultimately, getting a handle on what is trade credit is essential for any business owner. It's a key tool for buyers to manage cash flow and a strategic advantage for suppliers to drive sales. When managed well, it's a true win-win that helps both businesses succeed.

How Trade Credit Works in Practice

So, how does trade credit actually play out in the real world? It’s not just a casual agreement; it's a structured process that becomes part of a company's financial DNA. Getting the mechanics right is what makes it work for everyone involved.

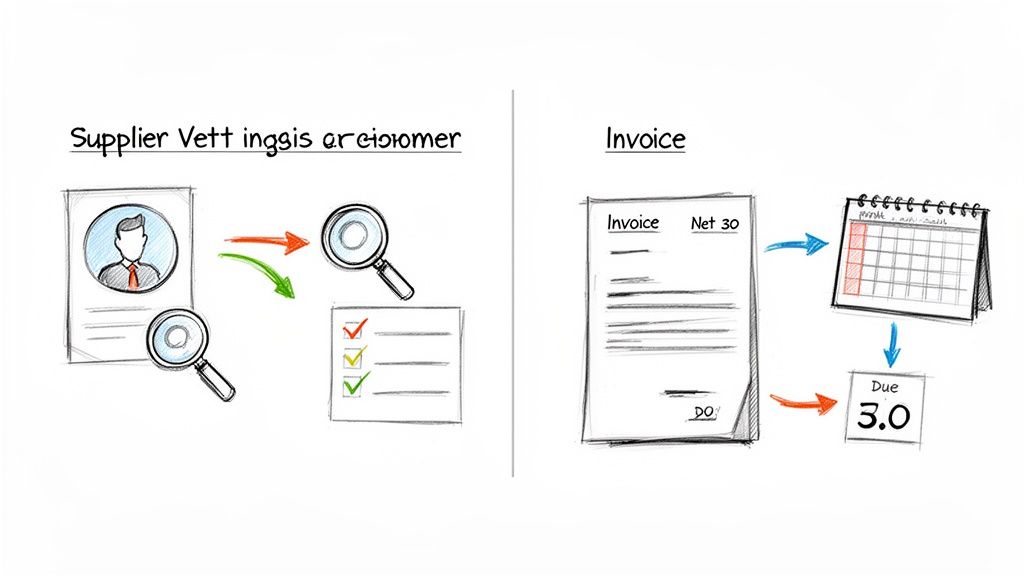

For suppliers, the process starts long before the first product ships. The first move is always to vet the customer. You need to know if they’re a safe bet, which means digging into their payment history and overall business health.

If they check out, the supplier sets a credit limit. This is simply the maximum amount of money the buyer can owe at any given time. It's a safety net for the supplier that still gives the buyer enough room to operate.

The Supplier's Role and Responsibilities

Once the goods or services are delivered, the supplier’s job is all about clear communication and diligent tracking. The invoice they send isn't just a bill; it's a contract. It has to clearly state the payment terms—like 'Net 30' or 'Net 60'—so the buyer knows exactly when the clock runs out.

On the books, this transaction is logged as accounts receivable, which is just another way of saying "money we're owed." A supplier's main tasks here are:

- Performing Credit Checks: Doing the homework on a buyer’s financial stability to avoid the headache of unpaid invoices down the line.

- Setting Clear Terms: Putting the due date and any early payment discounts right there on the invoice. You can explore the differences between offering credit terms versus prepayment discounts to see what fits your strategy.

- Managing Invoices: Keeping a close eye on who owes what and politely but firmly chasing down late payments to keep cash flowing.

A well-oiled accounts receivable process is the engine that drives a solid trade credit strategy. If you lose track of payments, you're not just creating an accounting mess—you're putting your company's financial health at risk.

The Buyer's Role and Responsibilities

From the buyer's side, it all begins with applying for credit. This usually involves sharing some basic financial info or a few trade references to prove you’re reliable. It's about building trust from day one.

After getting the green light, the buyer's primary job is simple: pay on time. That invoice from the supplier gets logged in their system as accounts payable, or "money we owe." It's critical to have a smooth accounts payable workflow, as this directly impacts the seller's cash flow.

Paying your bills on schedule isn't just good manners; it's smart business. It keeps your supplier relationships strong and ensures you can continue to rely on trade credit when you need it.

The Real Benefits and Risks for SMBs

For any small or medium-sized business, trade credit is a bit of a double-edged sword. Get it right, and it can be a massive catalyst for growth. But if you ignore the potential downsides, it can lead to serious financial headaches for everyone involved, whether you're the buyer or the supplier.

Let's look at it from the buyer's perspective first. The most obvious win is better cash flow. Instead of paying for goods or materials the moment they arrive, you get a crucial breathing room of 30, 60, or even 90 days to turn that inventory into sales before the bill is due. This kind of flexibility means you can jump on opportunities—like stocking up before a holiday rush—without having to empty your bank account.

Of course, that convenience comes with real responsibility. Missing a payment deadline isn't just about getting hit with a late fee. It chips away at your business’s reputation and creditworthiness. If you're consistently late, suppliers might tighten your terms or even switch you to cash-on-delivery, wiping out the very benefit you were enjoying.

Weighing the Pros and Cons for Suppliers

Now, flip the coin. For suppliers, offering trade credit is often just the cost of doing business—a way to stay competitive and attract customers. It can make you a far more appealing partner, encouraging buyers to place larger orders and building the kind of loyalty that lasts. Many businesses will happily pick a supplier with good terms over a slightly cheaper one that demands cash upfront.

The major risk, though, is the pressure it puts on your own cash flow. Every single invoice you issue on credit terms is cash that's tied up in your accounts receivable instead of being in your bank account where you can use it. This delay can open up a painful gap, and businesses may struggle to unlock their working capital.

Waiting for customers to pay can starve your business of the cash it needs to pay staff, buy raw materials, or invest in growth. This is the central challenge that suppliers face when offering trade credit.

Managing this risk is absolutely essential. While trade credit is a fantastic sales tool, offering it without proper checks and balances is a high-stakes bet on your customer's ability—and willingness—to pay you on time. For a deeper look into the financial options available, our guide on small business capital solutions offers valuable insights.

Here’s a quick breakdown of what you need to keep in mind:

- For Buyers (Benefits): Frees up cash, lets you buy more inventory, and builds stronger relationships with suppliers when you pay on time.

- For Buyers (Risks): You could face late fees, damage your business reputation, and strain supplier relationships if you miss payments.

- For Suppliers (Benefits): Drives higher sales, gives you a competitive edge, and helps build customer loyalty.

- For Suppliers (Risks): Puts a strain on your cash flow, carries the risk of customers defaulting, and adds the administrative headache of chasing payments.

At the end of the day, whether you're offering trade credit or using it, mastering this balancing act is fundamental to growing your business sustainably.

Managing the Risks of Offering Trade Credit

Offering trade credit can be a game-changer for winning and keeping customers, but let's be honest—it comes with risks. For suppliers, every time you send an invoice on credit terms, you're taking a chance. The secret isn't avoiding risk altogether; it's about managing it so smartly that it becomes a tool for growth, not a threat to your cash flow.

The first, most crucial step? Know who you’re doing business with. Before you agree to any credit terms, you absolutely have to run some checks on the buyer. This doesn't have to be a massive investigation. It could be as simple as looking at their payment history with other vendors, asking for trade references, or getting a sense of their financial health. You just want a clear picture of how reliable they are before you're on the hook.

Once you feel comfortable with a customer, the next move is to set a sensible credit limit. Think of it as a safety cap that limits how much you stand to lose with any one buyer. Just as critical is having a clear, professional process for chasing down overdue invoices. A polite-but-firm follow-up can make all the difference.

Building a Strong Risk Management Framework

To really protect your business, you need a plan. A solid framework will guide you through everything from vetting a new customer to handling a worst-case scenario, so you're never left scrambling.

A few core practices can make a world of difference:

- Establish Clear Credit Policies: Put it in writing. Your policy should spell out who gets credit, the terms you offer (like Net 30 or Net 60), and exactly what happens when a payment is late.

- Maintain Detailed Records: Keep track of every transaction, invoice, and conversation. If a dispute ever comes up, this paper trail is your best friend.

- Regularly Review Credit Limits: A customer’s financial situation isn't static. It's a good habit to periodically review their credit limits to make sure they still match their payment behavior and your comfort level.

For a wider view on handling business uncertainties, it’s also helpful to explore general Risk Management strategies which can add another layer of protection.

Insuring Against Non-Payment

Even with the best credit checks and policies in place, there’s always a chance a customer might not pay. This is where trade credit insurance steps in. It’s a safety net that protects your business from losses if a buyer goes insolvent or simply can't pay their bill.

This kind of protection is becoming more and more essential. The trade credit insurance market in the Middle East and Africa was valued at USD 1.56 billion in 2023 and is projected to keep growing. Why? A big reason is the sharp rise in business insolvencies, which shot up by 44% in 2023 alone. That statistic really underscores why businesses need to protect their accounts receivable. You can see more on this in the Middle East credit insurance market report.

By combining diligent credit checks, firm policies, and the safety net of insurance, you can confidently offer competitive payment terms. This turns trade credit from a source of financial stress into a well-managed tool for securing sales and building lasting customer loyalty.

Modern Tools That Make Trade Credit Work Better

Let’s be honest: the biggest headache for any supplier offering trade credit is the cash flow gap. Waiting 30, 60, or even 90 days for a customer to pay can put a serious strain on your own ability to pay bills, buy materials, and keep growing. It's a classic problem.

Thankfully, we're no longer stuck with just waiting and hoping. A new wave of financial tools has emerged to fix this exact issue, making the whole trade credit system much stronger for everyone involved.

Instead of staring at an unpaid invoice for weeks, suppliers can now use services like invoice discounting to get their hands on that cash almost right away. This simple shift helps businesses unlock their working capital, turning a long, stressful wait into a predictable and quick cash injection.

Closing the Payment Gap

This is where B2B payment platforms like Comfi come in. The process is straightforward: you, the supplier, deliver the goods and send an invoice with flexible terms to your buyer. But instead of you waiting for that payment, Comfi steps in and pays you directly, often within just 24 hours.

Comfi then takes on the responsibility of collecting the payment from the buyer on the original due date. It’s a pretty elegant solution that creates a win-win:

- Suppliers win because they get paid immediately. That cash is now unlocked and can be used to pay salaries, order more inventory, or fund expansion. Plus, the risk of the buyer not paying is completely off your plate.

- Buyers win because they still get the flexible payment terms they need to manage their own finances without feeling rushed.

This setup allows you to offer the competitive terms your buyers are looking for without putting your own company's financial health at risk. To see this in action, you can dig deeper into how Comfi’s B2B buy now, pay later solution enhances cash flow.

A Growing Market for Smarter Solutions

It’s no surprise that demand for these kinds of tools is exploding. The trade finance market in the Middle East and Africa is expected to hit a massive USD 10,315.1 million by 2030. A huge part of that growth is coming from receivables financing and invoice discounting, which are outpacing more traditional methods. It’s a clear sign that businesses are getting smarter about how they manage their money.

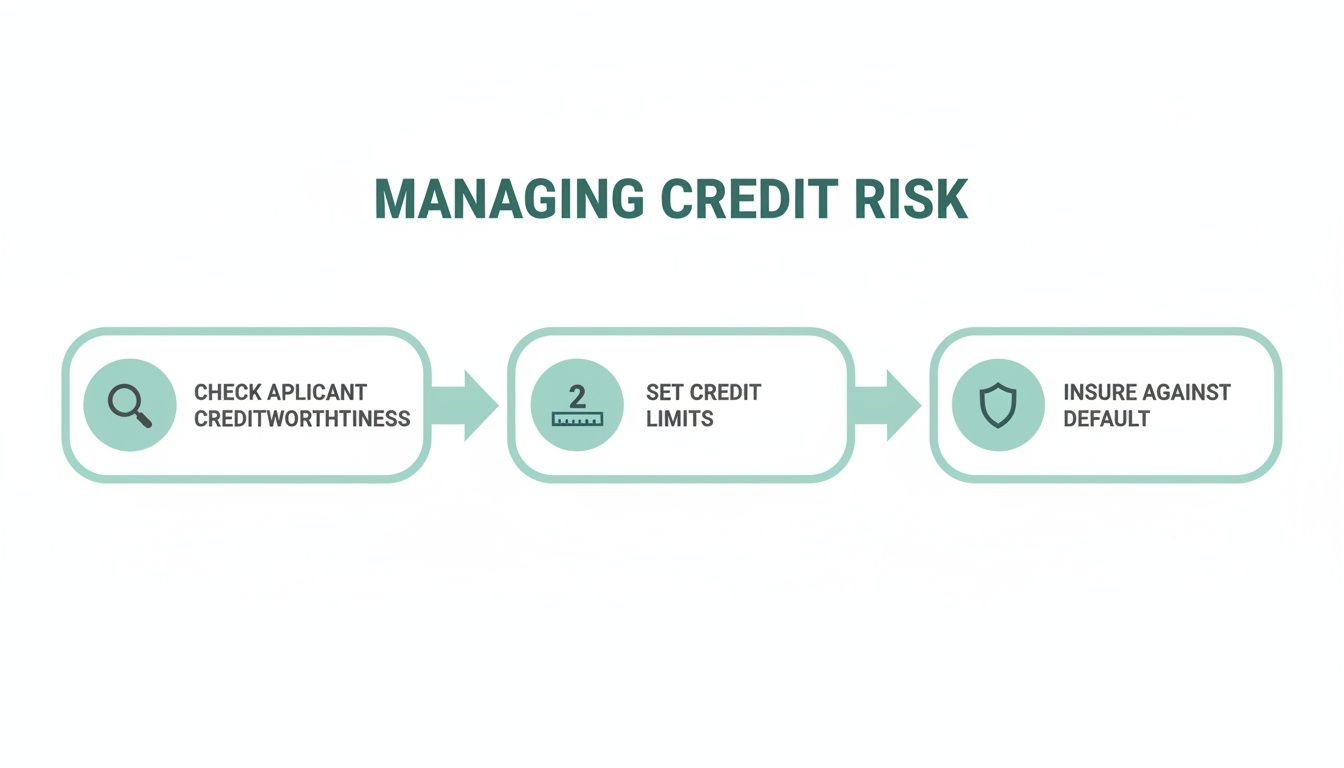

The image below breaks down the essential steps for managing the risks that come with offering credit in the first place.

This simple flow—vetting your customers, setting sensible limits, and having a backup plan for defaults—is the bedrock of any solid credit strategy. The great thing is, modern platforms help automate and simplify every part of it.

Answering Your Questions About Trade Credit

When you’re running a business, the world of B2B payments can feel overly complicated. You don't need jargon; you need straightforward answers that you can actually use. Let's tackle some of the most common questions about trade credit to help you feel more confident about using it.

We'll break down the important differences, common terms, and what it all really means for your bottom line.

How Is Trade Credit Different from a Bank Loan?

This is probably the most important distinction to grasp. While both trade credit and bank loans let you buy something now and pay later, they are fundamentally different.

A bank loan is a formal deal with a bank or other financial institution. You get a lump sum of cash, which you then have to pay back over a set period, almost always with interest tacked on. It’s a cash-based transaction.

Trade credit, on the other hand, is a simple agreement between you and your supplier. It’s not about getting cash; it's about getting goods or services with a promise to pay the invoice later. And if you pay on time, it's typically interest-free. The approval process is also usually much quicker and less formal than a bank's rigorous application.

Here’s a simple way to think about it: A bank loan gives you cash to use anywhere. Trade credit gives you a specific product with a delayed due date on the bill.

What Are Common Trade Credit Terms?

The "terms" are just the rules of the agreement, and they should be spelled out clearly on every invoice. Getting familiar with them is essential for managing your cash flow, whether you're the buyer or the seller.

You'll see these terms pop up all the time:

- Net 30, Net 60, or Net 90: This is the most common setup. It simply means the full invoice amount is due within 30, 60, or 90 days of the invoice date. Simple and to the point.

- 2/10 Net 30: This one offers a nice little bonus for paying early. A buyer can take a 2% discount off the total if they pay within 10 days. If not, no big deal—the full amount is just due in 30 days.

- End of Month (EOM): This term means payment is due by the last day of the month the invoice was issued. It’s a handy way to simplify accounting and align payments with monthly cycles.

How Does Offering Trade Credit Affect a Supplier's Cash Flow?

This is the classic double-edged sword for suppliers. Offering trade credit is a fantastic way to attract and keep customers, but it can put a serious squeeze on your cash flow.

Every time you send out a product and an invoice with payment terms, that money goes into your accounts receivable. It’s money you’ve technically earned, but it isn’t in your bank account yet.

This lag time between shipping a product and getting paid creates a cash flow gap. Your cash is essentially frozen, tied up in those unpaid invoices. That can make it tough to pay your own bills, meet payroll, or order more inventory to keep growing.

This is the single biggest headache for many growing businesses. It’s also why modern payment solutions are becoming so popular—they can pay you for your invoices right away, closing that cash flow gap so you have the money you need, when you need it.

Can New or Small Businesses Get Trade Credit?

Absolutely! It just might take a little more groundwork. For suppliers, giving credit to a well-known business with a perfect payment history is a no-brainer. A brand-new business, however, is more of an unknown.

To build that initial trust, a supplier might ask a new business for things like trade references (names of other suppliers you pay on time) or a look at your recent financial statements.

Here’s a great tip for any new business: start by building a relationship. Place a few smaller orders and pay for them upfront and on time. After you’ve shown you’re reliable, that supplier will be much more willing to offer you credit terms on bigger orders down the line.

Ready to offer flexible payment terms without the cash flow strain? See how Comfi can help you get paid on your invoices in as little as 24 hours while your customers still enjoy the payment flexibility they need. Visit Comfi.ai to learn more.

Related Reading

- What Is Trade Finance and How Does It Work for SMEs

- How Can MENA SMEs Master Working Capital?

- A Guide to Trade Credit for Modern MENA Businesses

Looking to improve your cash flow? Explore Comfi's Invoice Discounting and Invoice Discounting solutions. Get started today.