Mastering Consumer Goods Distribution in MENA for SMEs

You're probably seeing the same pattern right now. Orders are coming in from more retailers, online demand is getting harder to ignore, and your product has clear pull in the market. Yet every time the business starts to accelerate, cash gets trapped between inventory on one side and delayed collections on the other.

That's why many SME owners in the UAE misread their own distribution problem. They think they need more vans, more warehouse space, or more sales reps. Sometimes they do. But often the core issue sits in the timing gap between when they must pay and when they get paid.

Consumer goods distribution isn't just the movement of stock from supplier to shelf. It's the coordination of product flow, store coverage, demand signals, payment terms, replenishment discipline, and cash availability. If one part slips, the rest gets expensive very quickly.

The Growth Paradox in Consumer Goods Distribution

A familiar UAE scenario looks like this. A distributor wins more doors, lands a few promising accounts, and sees stronger repeat orders from neighbourhood stores and small chains. On paper, the business is growing. In practice, the owner is juggling supplier payments, chasing collections, and rationing inventory because too much cash is tied up before sell-through catches up.

That tension is becoming more important, not less. In the Middle East and Africa, the consumer goods market is projected to grow at a 5.2% CAGR from 2026 to 2034, ahead of the 4.7% global average, according to DataIntelo's consumer goods market outlook. The same projection says online retail is expected to grow at 9.1% CAGR and reach 34.0% of total sales by 2034. For an SME, that means distribution is no longer just about getting listed in physical outlets. It now means serving shelves and screens at the same time.

Growth creates strain before it creates comfort

Many owners expect growth to make the business easier. Usually, the opposite happens first.

When demand rises, you need to buy more stock earlier. You need more disciplined replenishment. You often have to offer terms to win and keep accounts. If your buyers pay later than your suppliers expect, every new sale can put extra pressure on your operating cycle.

Growth in distribution can look healthy in sales reports while quietly weakening the business underneath.

This is the paradox. The more demand you have, the more precisely you need to manage both stock and cash. A weak route-to-market model gets exposed faster in a growing market than in a flat one.

Distribution is a money system as much as a logistics system

A lot of distribution advice focuses on transport, warehousing, or merchandising. Those matter. But SME operators in MENA usually feel the pressure first in their bank account, not in a spreadsheet about network design.

If inventory arrives too early, cash sits in stock.

If it arrives too late, shelves go empty.

If retailers pay slowly, your next purchase cycle tightens.

If you spread inventory too widely, your top-performing outlets understock while weaker outlets hold dead stock.

That's why the smartest distributors treat consumer goods distribution as one connected operating system. Product movement, outlet selection, payment timing, and replenishment cadence have to work together.

Mapping Your Route to Market Channels and Models

Before fixing distribution, you need to identify what model you're running. Many SMEs operate a mixed route to market without naming it clearly. That creates confusion when sales teams push for wider coverage while finance teams try to slow stock exposure.

Direct, indirect, and hybrid routes

Think of distribution like water moving from a source to homes.

In a direct model, the manufacturer or brand sells straight to the end buyer. That may happen through your own sales team, your own website, or direct fulfilment to business customers. You keep more control, but you also carry more operational responsibility.

In an indirect model, intermediaries sit between the product owner and the consumer. These might be wholesalers, retailers, or agents. This model can extend market reach faster, especially across fragmented markets, but you give up some control over pricing, shelf execution, and customer experience.

A hybrid model mixes both. This is common in the UAE. A business might sell directly to key accounts, work through distributors for smaller territories, and also list online through marketplaces or digital channels.

If you want a simple way to think about scale versus channel control, Zinc's piece on Analyzing Amazon and Walmart is useful because it highlights how different commercial models shape assortment, reach, and operating decisions.

The three distribution strategies

Once you know the channel, the next question is coverage strategy.

- Intensive distribution means placing the product in as many relevant outlets as possible. This suits everyday consumer goods where convenience matters and brand visibility depends on being widely available.

- Selective distribution means choosing specific outlets that fit your positioning, service model, or margin expectations. This works well when the product needs better shelf execution or more controlled sell-through.

- Exclusive distribution means limiting access to one retail partner or one territory partner. This can sharpen accountability, but it also concentrates risk.

A common SME mistake is choosing intensive distribution too early. More doors sound attractive, but every extra account adds servicing cost, credit exposure, delivery complexity, and stock allocation pressure.

Practical rule: Don't ask, “How many stores can carry us?” Ask, “Which stores can move our product fast enough to justify the cost to serve?”

Why weighted distribution matters more than door count

Professionals don't judge distribution quality by store count alone. They use weighted measures such as Total Distribution Points (TDP) and % ACV, as explained in this guide to market data and weighted distribution metrics. The logic is simple. One listing in a high-volume retailer can matter more than multiple listings in low-productivity outlets.

For SME owners, the practical lesson is clear:

- Prioritise productive accounts: A store with stronger throughput gives you better exposure per delivery.

- Review coverage by sales velocity: Don't celebrate listings that barely rotate.

- Separate vanity reach from useful reach: Nominal presence can hide weak sell-through.

That's how larger operators think. SMEs should do the same, especially when cash is limited.

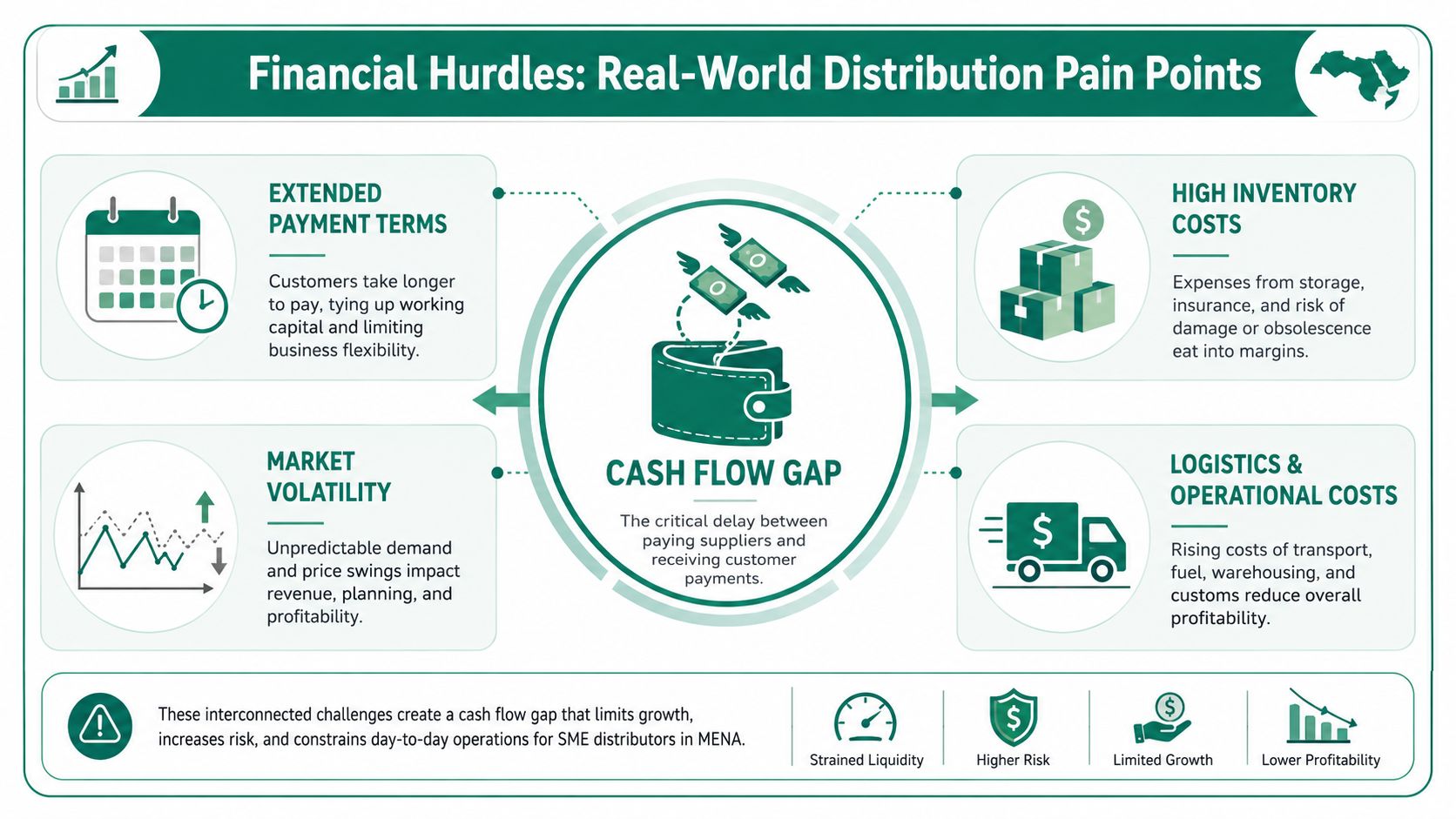

The Real-World Financial Pain Points for Distributors

Most distribution problems don't announce themselves as financial problems. They show up as stockouts, partial deliveries, delayed purchase orders, weak fill rates, and uncomfortable supplier calls. But if you trace them back far enough, the issue often starts with cash timing.

This summary captures the pressure points clearly:

Why fragmented retail is expensive to serve

The UAE and wider Gulf retail environment isn't made up of one clean channel. It includes independents, neighbourhood stores, small chains, speciality shops, marketplaces, and modern trade. Each one orders differently. Each one moves at a different speed. Each one expects service that fits its own realities.

Traditional distribution systems are often not designed to serve that fragmentation efficiently. A useful framing appears in The Food Trust's discussion of small-store distribution constraints, which notes that the main bottleneck is often execution capacity. In practical terms for UAE distributors, that means the issue is frequently working capital and logistics synchronisation, not a lack of demand.

A small retailer may need smaller drops, faster replenishment, and tighter SKU selection. That sounds manageable until you multiply it across dozens or hundreds of accounts. Then your cost to serve climbs while your inventory gets spread thin.

The hidden cost of being “available everywhere”

A lot of SME distributors chase market presence without calculating what it does to cash.

Here's what usually happens:

- Inventory gets diluted: Fast-moving stores receive less than they need because stock is spread across too many accounts.

- Collections become uneven: Your team spends more time managing small balances across many buyers.

- Supplier relationships tighten: You can't reorder aggressively because too much cash is sitting in receivables and slow stock.

- Sales quality drops: The business records revenue, but margin and replenishment quality deteriorate.

The result is a business that looks bigger than it feels.

The cash conversion squeeze

In this context, finance leaders need to get operational. If your outflows happen before your inflows, every growth phase creates strain. You buy inventory, pay transport, absorb warehousing, and service the account, then wait for the customer payment cycle to finish.

That lag is a tax on growth.

If you want a clean way to review that cycle, Comfi's article on the cash conversion cycle is worth reading because it breaks down how inventory days, receivables timing, and payables interact.

A distributor rarely fails because demand disappears overnight. More often, the business gets stuck between successful sales and slow cash recovery.

What doesn't work

Some responses make the problem worse:

- Adding more stock without tighter assortment discipline: This often increases trapped cash.

- Offering terms to every buyer the same way: Not all accounts deserve the same commercial treatment.

- Measuring sales reps only on new account wins: That encourages weak-quality distribution.

- Using one replenishment rhythm for all outlets: High-frequency stores and slow stores shouldn't be serviced the same way.

The SME operators who stay healthy usually do something less dramatic. They narrow focus, protect stock quality, and tie commercial decisions to actual cash movement.

Actionable Strategies to Optimise Your Distribution

You can improve consumer goods distribution before bringing in any external tool. Most gains come from sharper decisions, not bigger teams.

Tighten assortment before expanding coverage

Many distributors carry too many SKUs into too many doors. That creates the illusion of range while weakening replenishment quality.

A better approach is to classify your assortment by role:

- Core movers: These should almost never be out of stock in your best accounts.

- Tactical lines: Useful for specific territories, seasonal demand, or selected channels.

- Low-rotation items: These need stricter entry rules and regular review.

If a SKU doesn't earn its place, it shouldn't travel through the network just because a salesperson wants a broader catalogue. Range without rotation ties up cash and warehouse attention.

Build territories around demand, not habit

Too many route plans are based on old customer lists and driver familiarity. That's understandable, but it leaves money on the table.

Modern distributors use location intelligence and points of interest data to plan territory coverage, as described in Datappeal's guide to selecting popular places for FMCG distribution. The practical point is not that you need a complex map on day one. It's that sales coverage, stock allocation, and promotional effort should follow where demand clusters exist.

Three practical moves help:

- Cluster by outlet potential: Group stores by demand pattern, not just geography.

- Assign delivery frequency intentionally: High-turn stores need a different service rhythm from long-tail accounts.

- Review dead zones: If a territory absorbs effort without moving stock, redesign it.

Match service level to account value

Not every customer needs the same visit frequency, same delivery terms, or same product range.

A disciplined distributor separates accounts into service tiers. Key accounts get priority inventory and tighter response. Mid-tier stores get reliable but controlled servicing. Marginal accounts may move to order thresholds or reduced drop frequency.

That sounds simple, but many SMEs avoid it because they fear offending customers. In practice, unclear servicing rules cause more damage than transparent ones.

Better distribution often starts with saying no to the wrong service promise.

Strengthen the handoffs

Distribution breaks down at the handoff points. Sales promises one thing. Warehouse prepares another. Delivery arrives late. Finance blocks the next order because the account is overdue. Everyone feels busy, but the customer experiences inconsistency.

To reduce that friction:

- Run one weekly review between sales, operations, and finance.

- Flag at-risk SKUs early instead of waiting for stockouts.

- Set simple account rules for reorder approval, overdue balances, and delivery cut-off times.

- Track exceptions manually if needed. A clean spreadsheet used consistently is better than a neglected system.

The goal isn't perfection. It's fewer surprises.

How Modern Payment Solutions Unlock Your Working Capital

Once the operational basics are in place, payment structure becomes the lever that changes what your distribution model can support.

A lot of SMEs treat payment tools as separate from operations. That's a mistake. In consumer goods distribution, payment design shapes which accounts you can serve, how much inventory you can place, and how quickly you can replenish.

This visual shows the kinds of tools now being used to reduce payment friction:

When the problem is liquidity, not demand

A useful contrarian point from Circana's discussion of underserved consumer markets is that many “underserved” doors are not weak on demand. They're understocked because distributors can't support enough inventory across many small accounts at once. That changes the conversation.

The issue isn't always, “Where should we sell?”

Often it's, “How do we support more good accounts without freezing our own cash?”

That's why modern payment solutions matter. They let the distributor manage the time gap between supply, sell-in, and collection more intelligently.

The tools that make a practical difference

Different models solve different bottlenecks.

Invoice discounting helps when you've already sold to a credible buyer but don't want to wait through the full collection cycle before using that cash again. For distributors supplying larger retailers or established business customers, this can speed up the next purchase cycle.

B2B buy now, pay later terms help when buyers want flexibility but you still need healthier cash timing in your operation. This can support order conversion and reduce the strain of extending terms informally.

Early payment programmes are useful when suppliers need cash sooner and buyers want a structured way to manage payment timing without endless manual negotiation.

Automated invoice workflows matter more than many owners realise. Delays often begin with paperwork, mismatched approvals, and slow reconciliation. Faster invoice processing reduces avoidable lag.

If you're comparing options in this space, Comfi's overview of a payment solution for SMEs is a practical reference because it explains how digital payment structures can support day-to-day trade activity rather than sitting outside it.

What to look for before adopting any solution

Don't choose a payment tool just because it sounds modern. Choose it based on operational fit.

Check these points:

- Buyer fit: Does it work with the payment behaviour of your actual customers?

- Invoice workflow: Can your team use it without creating another manual bottleneck?

- Integration simplicity: If the setup is clumsy, adoption will stall.

- Commercial effect: Does it help you place more of the right stock in the right accounts?

One market option is Comfi, which offers tools such as invoice discounting, B2B payment terms, and dealer financing that businesses use to free up working capital tied up in invoices or stock. The relevant point for distributors is not the label of the product. It's whether the tool helps move cash in line with how the business buys and sells.

If your route to market is fragmented, your payment architecture can't stay rigid.

The strongest operators in MENA now treat payment terms as part of channel strategy. That's the shift. Finance isn't sitting behind the business anymore. It's helping determine which distribution model is sustainable.

A Real-World Example of Distribution Success

Consider a hypothetical UAE electronics distributor serving independent retailers, a few small chains, and selected B2B buyers. The business has healthy demand for accessories and fast-moving devices. Sales reps keep opening accounts. Orders are coming in. But management still feels constrained every month.

The problem isn't weak sales. It's that the company keeps running into the same cycle. Large buyers take time to settle invoices, smaller buyers ask for flexibility, and the distributor can't confidently increase stock because too much cash is already committed. The warehouse is busy, yet the owner keeps delaying purchase decisions.

What changed first

The company didn't start by chasing more doors. It cleaned up execution.

It reduced SKU sprawl, prioritised faster-moving outlets, and adjusted route planning so the best accounts got tighter replenishment. Sales and finance also agreed on clearer account treatment. Some customers kept flexible terms. Others shifted to stricter ordering conditions based on payment behaviour and order quality.

What changed next

After the operating model improved, the company added modern payment support. It used a service that helped release cash tied up in approved invoices to larger buyers, while also offering structured payment flexibility to selected smaller accounts. That gave the business more room to restock core SKUs without waiting for every collection cycle to finish.

The result wasn't magic. It was better timing.

Supplier conversations improved because purchase planning became less reactive. Retailers got more reliable fulfilment on the products that moved. Sales became healthier because the business could support real demand instead of rationing stock.

An interesting example from the region is Bevarabia's case study, which shows how a UAE business used a more flexible payment structure to support growth without letting cash flow become the blocker.

The lesson is straightforward. Distribution success in MENA rarely comes from one big move. It comes from combining sharper assortment, tighter territory logic, and payment tools that match the realities of fragmented trade.

Comfi helps MENA SMEs release working capital trapped in invoices and inventory through digital payment tools built for day-to-day trade. If your consumer goods distribution business is growing faster than your cash cycle can handle, explore Comfi as one practical option for making your payment structure work more like your market does.