What Is Working Capital: SME Guide & Strategies 2026

Sales can be rising while cash still feels tight.

That is common for SME owners in Dubai. You win more orders, buy more stock, hire people, pay suppliers, cover rent, and then wait to get paid. The money is in the business, but not in the bank when you need it. That gap is where most confusion about working capital begins.

If you have ever asked, “We are busy, so why are we still watching every dirham?”, you are already asking what working capital is.

Your Business Is Growing But Your Bank Account Is Not

A distributor lands a few large retail orders. Revenue looks strong. The warehouse is busy. But suppliers want payment before customers settle their invoices. Payroll still runs on time. Freight and VAT still need paying.

That business is not failing. It is dealing with a working capital gap.

Working capital is the money available to run day-to-day operations. Put simply, it is the gap between what you can turn into cash soon and what you need to pay soon. When that gap is healthy, the business runs smoothly. When it is tight, even a growing company can feel strained.

In the region, this is a major issue. Recent 2024 data shows that Net Working Capital days across the Middle East remain high at 101.7 days, which means the average regional business has cash tied up for over three months, according to PwC's Middle East Working Capital Study.

What this looks like in real life

Owners usually notice the symptoms before the formula:

- Stock pressure means cash is stuck in receivables when you need to reorder.

- Supplier tension shows up when sales are healthy but payments still feel late.

- Growth stress appears when every new order creates more strain instead of more room.

You can be profitable and still run short of operating cash. Profit is on paper. Working capital keeps the doors open this week.

Where readers usually get confused

Many people mix up cash flow, profit, and working capital.

- Profit shows whether the business earned more than it spent over a period.

- Cash flow tracks money moving in and out.

- Working capital shows whether you have enough short-term room to operate without stress.

That is why a company can grow sales and still feel squeezed. The business is active, but cash conversion is slow.

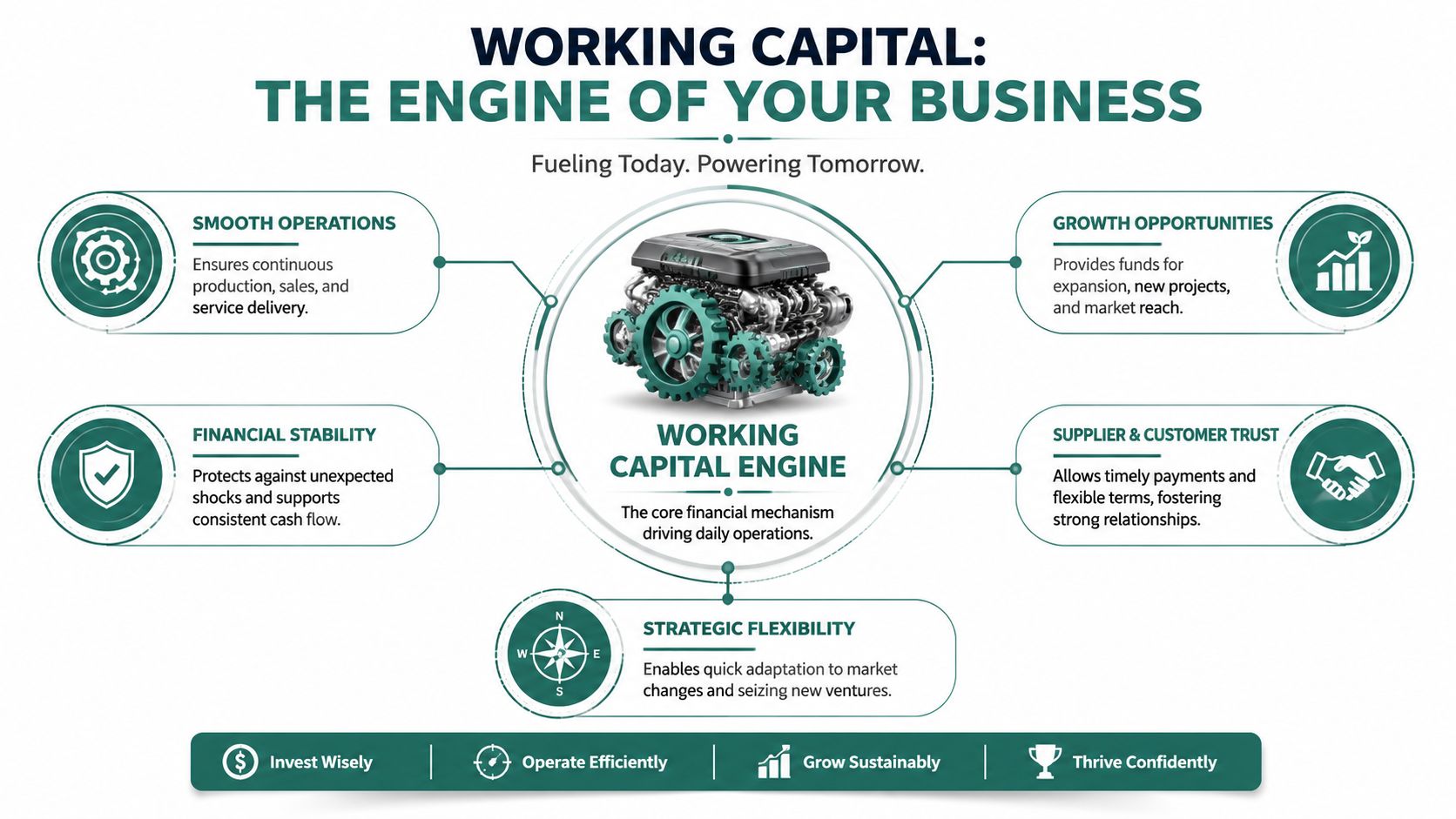

Why Working Capital Is the Engine of Your Business

Working capital is not just an accounting line. It keeps the business moving.

You can have customer demand, stock on shelves, and invoices waiting to be paid, and still struggle to cover daily costs.

It keeps daily operations moving

A healthy working capital position helps you pay staff, place supplier orders, and cover shipping, customs, repairs, and overheads without constant scrambling.

That matters because businesses usually do not break from one dramatic event. They get worn down by repeated short-term squeezes.

If you want a clean companion read on the difference between liquidity and operational movement, this guide on cash flow basics for businesses is useful.

It gives you room to grow

Growth often needs cash before it generates cash.

You may need to buy inventory ahead of demand, take a supplier deal, or hold more stock because customers order in bursts. Without enough working capital, you can see the opportunity and still miss it.

That is one reason this matters across the region. About $35.5 billion in excess working capital is currently locked up on Middle Eastern corporate balance sheets, according to CTMfile's coverage of regional working capital data. That is money businesses could use for expansion, innovation, or debt reduction.

It protects trust

Working capital also shapes relationships.

- With suppliers, it helps you pay on time and negotiate from a stronger position.

- With customers, it helps you fulfil orders consistently.

- Inside the business, it reduces the stress that builds when every payment date feels like a test.

Practical rule: if one delayed customer payment immediately disrupts payroll, purchasing, or supplier payments, your working capital structure is too tight.

Strong businesses are often the ones with enough financial flexibility to stay organised while they grow.

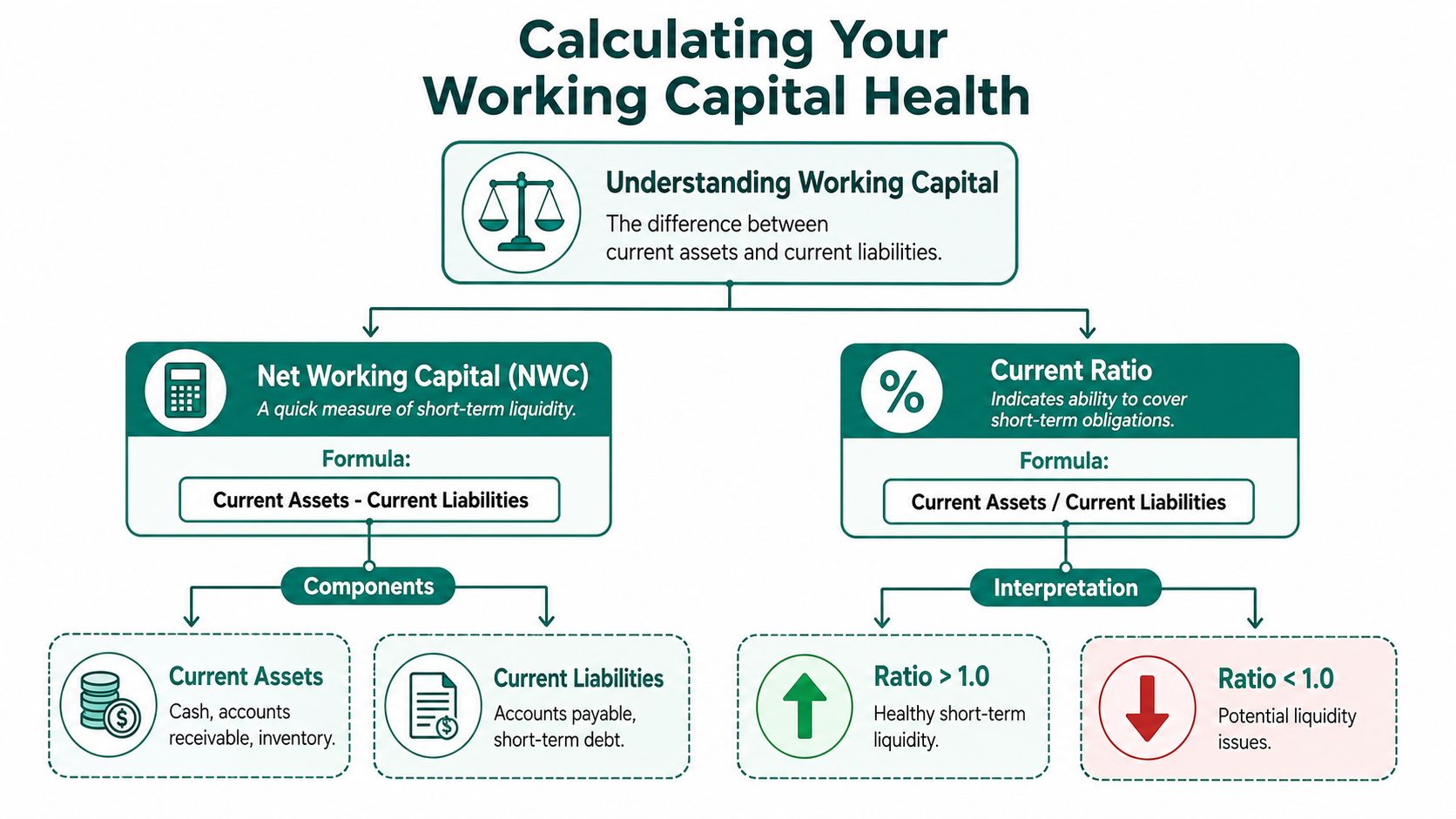

How to Calculate and Interpret Your Working Capital

You do not need a finance team to get a useful first view. Start with one simple formula, then use a second one for a more operational picture.

Start with the simple version

The basic formula is:

Net Working Capital = Current Assets - Current Liabilities

This shows whether your short-term assets exceed your short-term obligations.

Your current assets usually include:

- Cash in bank accounts

- Trade receivables from customers

- Inventory you expect to sell

Your current liabilities usually include:

- Trade payables owed to suppliers

- Short-term obligations due within the year

- Other near-term bills due soon

If the result is positive, that is a good sign. If it is negative, the business may struggle to meet near-term commitments without outside support or faster collections.

Use WCR when you want the real cash gap

A more operational measure is the Working Capital Requirement, or WCR.

The accepted formula is:

WCR = (Inventories + Trade Receivables + Tax Receivables) - (Trade Payables + Tax Payables + Social Security Payables)

This is useful because it focuses on the timing gap between cash going out and cash coming back in.

For UAE SMEs, a healthy Working Capital Ratio is between 1.2 and 2.0, and a ratio below 1.2 signals imminent liquidity risk, according to Coface's explanation of working capital requirements.

How to read the result

A number only helps if you know how to interpret it.

- Between 1.2 and 2.0 usually points to a healthy short-term position for UAE SMEs.

- Below 1.2 can mean your margin for error is too small.

- Well above the healthy range can also deserve a second look, because too much cash may be tied up in stock or receivables.

For a more detailed walkthrough of formulas and examples, this guide on how to calculate working capital is a practical reference.

A healthy ratio does not mean relax. It means keep monitoring. Working capital can tighten quickly when inventory rises or customer payments slow down.

A plain-language example

Your balance sheet may show enough cash, receivables, and stock to cover near-term bills. But if most of that value sits in slow-moving inventory, the business can still feel cash-poor.

That is why owners often say, “We have assets, but we cannot use them today.” They are describing a working capital problem.

Common Causes of a Working Capital Squeeze

Most working capital pressure comes down to timing. Cash leaves faster than it returns.

For SMEs in high-growth sectors such as distribution and automotive, the pattern is familiar. You commit cash early, but recovery takes longer than expected.

Slow collections stretch the gap

A sale is not cash until the customer pays.

Many SMEs still plan around booked revenue instead of actual collections. If clients pay on long terms, or pay late, receivables become a storage room for cash. The business may look busy while the bank balance stays tight.

This is especially hard for wholesalers and distributors, who often buy stock up front while giving buyers payment flexibility.

Inventory can quietly absorb cash

Inventory supports sales, but too much of it traps liquidity.

Growing businesses often overstock. They add extra lines, buy deeper quantities, or keep slow-moving items just in case. Over time, shelves become expensive. The stock has value, but it does not help with this week’s supplier payment.

Automotive dealers face a sharper version of the problem

In many businesses, inventory turns reasonably fast. In the UAE automotive sector, it can move much more slowly. Capital can be locked in vehicle inventory for up to 180 days before a sale occurs, creating a severe bottleneck for dealers trying to restock and grow.

That makes automotive a special case. A vehicle in the showroom may look like strength to a customer, but to the owner it can feel like frozen cash.

If your best-selling stock is easy to replace but cash is always tight, review the items that sit longest. Slow inventory often causes more stress than weak sales.

Seasonal demand and uneven purchasing

Some businesses do not sell in a straight line. They surge, pause, then surge again.

That creates awkward choices. Do you buy ahead of demand and tie up cash, or wait and risk missing sales? For businesses with imported goods, lead times add more pressure. The result is often a working capital squeeze caused by uncertainty, not poor trading.

Actionable Strategies to Improve Your Liquidity

Improving working capital usually comes down to three levers: collect cash faster, hold inventory more carefully, and manage outgoing payments with discipline.

You do not need to do everything at once. In most SMEs, one or two changes can make a visible difference.

Accelerate cash inflows

The first priority is simple: reduce the time between making a sale and receiving cash.

Tighten invoicing discipline. Send invoices as soon as delivery or completion is confirmed. Make sure documents are complete, because many payment delays start with avoidable admin issues.

Another lever is offering an early payment discount such as 2/10, n/30, meaning a 2% discount if paid within 10 days, otherwise the full amount is due in 30 days, as outlined in this guide to working capital management for UAE SMEs. It will not fit every customer, but it can improve collections in the right account mix.

You can also review practical guidance on cash flow essentials for business owners if you want a non-technical refresher on collection habits and spending discipline.

Treat receivables like an operating process

Many owners chase overdue invoices only when cash gets tight. That is too late.

Try this instead:

- Invoice fast: send the invoice as soon as goods are delivered or work is accepted.

- Confirm receipt: make sure the customer has logged the invoice.

- Track due dates: review ageing regularly, not just at month end.

- Escalate early: follow up when a payment first slips.

If receivables are a recurring pinch point, this explainer on accounts receivable financing options gives a useful overview of how businesses convert approved invoices into quicker liquidity.

Tighten inventory decisions

Inventory discipline does not mean starving the business of stock. It means separating what sells reliably from what only takes up space.

Use purchasing reviews to ask:

- Which items move consistently

- Which items sit too long

- Which lines are ordered from habit rather than demand

For distributors, this often shows that a small set of items drives most movement while other lines steadily drain cash. For automotive dealers, the focus is even sharper. Every unsold unit can delay the next purchase opportunity.

Better liquidity often comes from sharper inventory choices, not blanket cuts.

Manage cash outflows without damaging relationships

Payables need balance. Paying too early can tighten cash. Paying too late can damage supplier trust.

The goal is to align outgoing payments with incoming cash as closely as possible. That may mean renegotiating terms, batching non-urgent purchases, or being more selective about buying in bulk.

Useful habits include:

- Know your payment calendar: do not let supplier due dates surprise you.

- Match terms to sales cycles: longer sales cycles need more breathing room.

- Protect core suppliers: if you must prioritise, protect the relationships that keep stock moving.

For most SMEs, stronger working capital does not come from one dramatic move. It comes from a few steady operating decisions repeated well.

Conclusion From Cash-Strapped to Growth-Ready

If you have been asking what is working capital, the simplest answer is this: it is the money that keeps your business moving between today’s costs and tomorrow’s collections.

The more useful answer is that working capital shows how much room your business has to operate calmly, buy confidently, and grow without constant pressure. It sits behind payroll, inventory, supplier relationships, and your ability to take the next order without worrying about the next payment run.

For SMEs in the UAE and wider MENA region, this matters even more in sectors where inventory is expensive and payment cycles are long. A distributor carrying stock and waiting on receivables faces one kind of pressure. An automotive dealer with capital tied up in showroom vehicles faces another.

The good news is that working capital can be improved. You can measure it, spot the causes of strain, and strengthen it through better invoicing, tighter collections, smarter stock decisions, and better payment timing.

The shift is both financial and operational. Instead of reacting to every cash squeeze, you manage liquidity as a core business function. That is when growth becomes easier to support.

If your business is growing but cash still feels stuck, Comfi helps SMEs across MENA access working capital through tools such as Invoice Discounting, Buy Now, Pay Later, and Automotive Dealer Financing. It's a practical way to free up cash from invoices or in-stock vehicles, reduce cash-flow bottlenecks, and keep inventory, supplier payments, and growth plans moving.