How to Calculate Working Capital for UAE SMEs

Calculating your working capital is surprisingly straightforward, but don't let the simplicity fool you. It's one of the most powerful health checks you can run on your business. At its core, the formula is just Current Assets - Current Liabilities.

This simple calculation gives you a clear snapshot of your company's short-term financial footing and its ability to keep the lights on.

Understanding Your Working Capital in 60 Seconds

Think of working capital as the cash and liquid assets you have available to run your business day-to-day. It’s the money left over after you account for what you owe in the near future. For any SME here in the UAE, this number is a direct indicator of your ability to cover immediate costs without breaking a sweat.

A positive figure is a great sign—it means you have more than enough resources to operate smoothly and even handle unexpected bumps in the road. On the other hand, a negative result is a red flag. It can signal a cash flow crunch on the horizon, potentially making it tough to pay suppliers or even meet payroll.

What Makes Up Working Capital

To really get a feel for it, you need to understand the two sides of the coin.

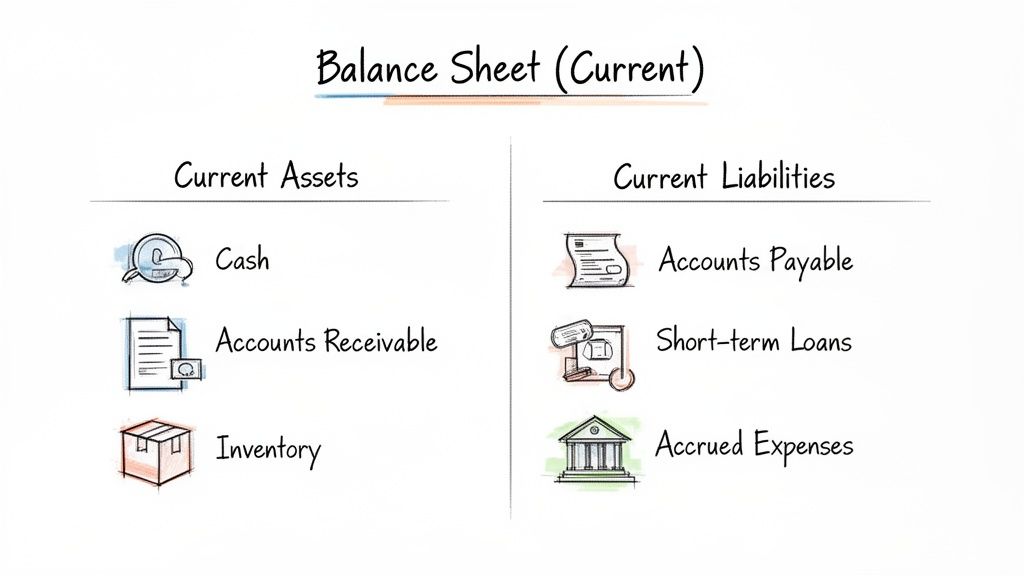

- Current Assets: This is anything your business owns that can realistically be turned into cash within a year. Think of the obvious ones like cash in the bank, but also inventory you plan to sell, and—crucially for many businesses—unpaid customer invoices (your accounts receivable).

- Current Liabilities: These are your short-term debts and obligations due within the next 12 months. This bucket includes everything from supplier bills (accounts payable) and short-term loans to rent and other running costs.

This isn't just theory; it has a real impact on businesses in the Middle East. A recent PwC Middle East Working Capital Study found that net working capital days across the region improved to 101.7 days. UAE firms are actually leading the charge here, getting smarter about how they manage both their stock and their customer payments.

By getting to grips with this simple formula, you stop just running your business and start strategically managing its financial pulse. It’s the first real step toward building a more resilient company that’s ready for growth.

Finding the Numbers on Your Balance Sheet

Before you can calculate your working capital, you need to know where to look. The two key figures you're after—Current Assets and Current Liabilities—are both found on your company's balance sheet. Think of the balance sheet not as a complex accounting document, but as a clear, single-moment snapshot of your business's financial health.

The balance sheet itself is split into two sides: what you own (assets) and what you owe (liabilities). For this specific calculation, we're zeroing in on the "current" items. These are assets you expect to turn into cash within a year, and liabilities you need to pay off in that same timeframe. This short-term focus is precisely what makes working capital such a vital metric for managing your day-to-day cash flow.

Identifying Your Current Assets

Current assets are the resources your business has on hand to fund its immediate operational needs. What falls into this category really depends on your type of business. For an electronics distributor in the UAE, for example, inventory is a massive part of their current assets. On the other hand, a B2B marketing agency's biggest current asset will likely be its accounts receivable.

To get your total, just find the "Current Assets" section on your balance sheet and add up a few common line items:

- Cash and Cash Equivalents: This is your most accessible asset—the money sitting in your business bank accounts.

- Accounts Receivable: This is simply the money owed to you by customers for products or services you’ve already delivered. Think of them as your outstanding invoices.

- Inventory: This covers the value of everything you hold for sale, from raw materials and works-in-progress to finished goods ready to ship.

- Prepaid Expenses: This is anything you've paid for in advance, like your annual insurance premium or a few months of rent.

Getting these numbers right is the first half of the puzzle. It all comes down to accurate, consistent tracking, which is why having solid accounting software is a non-negotiable for SMEs in the UAE.

Pinpointing Your Current Liabilities

Next, let's flip over to the other side of the equation: your current liabilities. These are all your short-term financial commitments that are due within the next 12 months. Just like with assets, you'll find them neatly grouped under a "Current Liabilities" heading on your balance sheet.

You'll typically see items like these:

- Accounts Payable: This is the mirror image of accounts receivable—it's the money you owe to your suppliers for things you've bought on credit.

- Short-Term Debt: This includes any business loans, credit lines, or other borrowings that need to be repaid within one year.

- Accrued Expenses: These are costs you've incurred but haven't paid yet. A classic example is the salaries your team has earned this month that you'll pay out on the 1st of next month.

- Unearned Revenue: This is when a customer pays you upfront for a service or product you haven't delivered yet.

Add these up, and you have your total current liabilities.

While your balance sheet gives you the numbers for working capital, it doesn't tell the whole story. To get a truly complete picture of your financial health, you also need to understand how your profitability impacts these figures. Learning how to read your P&L statement is a great next step for deeper insight.

Once you have both your total current assets and total current liabilities, you're all set to plug them into the formula and see where you stand.

Putting the Formula into Practice with Real UAE Scenarios

Knowing the formula is one thing, but the real lightbulb moment happens when you plug in actual numbers from businesses you could meet any day. Let's move past the theory and walk through the working capital calculation for two very different SMEs you'd find right here in the UAE.

These examples really highlight how the same simple equation can paint two completely different pictures of a company's financial health.

Scenario 1: The Cash-Strapped Auto Parts Wholesaler

Picture a successful automotive parts wholesaler based in Dubai. On paper, they're doing great—sales are strong and their customer list is growing. The problem? Many of their bigger clients insist on 60- or even 90-day payment terms. This creates a huge gap between making a sale and actually getting the cash in the bank.

Let's break down their financials:

Current Assets:

- Cash in Bank: AED 50,000

- Accounts Receivable (unpaid invoices): AED 400,000

- Inventory (parts in the warehouse): AED 250,000

- Total Current Assets: AED 700,000

Current Liabilities:

- Accounts Payable (what they owe suppliers): AED 550,000

- Short-Term Loan Payment (due this year): AED 150,000

- Accrued Expenses (salaries, rent, etc.): AED 50,000

- Total Current Liabilities: AED 750,000

Now, let's run the numbers:

AED 700,000 (Current Assets) - AED 750,000 (Current Liabilities) = -AED 50,000

This wholesaler has a negative working capital of -AED 50,000. It's a classic cash flow crunch. Even though they are owed AED 400,000, they don't have enough liquid cash today to cover their immediate bills. This shortfall leads to late supplier payments, trouble ordering new stock, and a constant state of financial stress. Their growth is literally locked up in their unpaid invoices.

Scenario 2: The Agile Food & Beverage Distributor

Next, let's look at a growing food and beverage distributor in Abu Dhabi. They supply a mix of hotels and restaurants, most of whom pay quickly. On top of that, they've been smart about negotiating good payment terms with their own suppliers.

Here's how their books look:

Current Assets:

- Cash in Bank: AED 300,000

- Accounts Receivable (unpaid invoices): AED 150,000

- Inventory (fast-moving goods): AED 200,000

- Total Current Assets: AED 650,000

Current Liabilities:

- Accounts Payable (bills to suppliers): AED 250,000

- Accrued Expenses (salaries, logistics): AED 100,000

- Total Current Liabilities: AED 350,000

Plugging these figures into the formula gives us a very different result:

AED 650,000 (Current Assets) - AED 350,000 (Current Liabilities) = +AED 300,000

This distributor is sitting on a positive working capital of AED 300,000. This healthy cash buffer is a game-changer. They can pay their bills with ease, handle unexpected costs, and jump on new opportunities. Whether it's placing a bulk order to get a supplier discount or investing in a new delivery van, they have the financial flexibility to do it without borrowing.

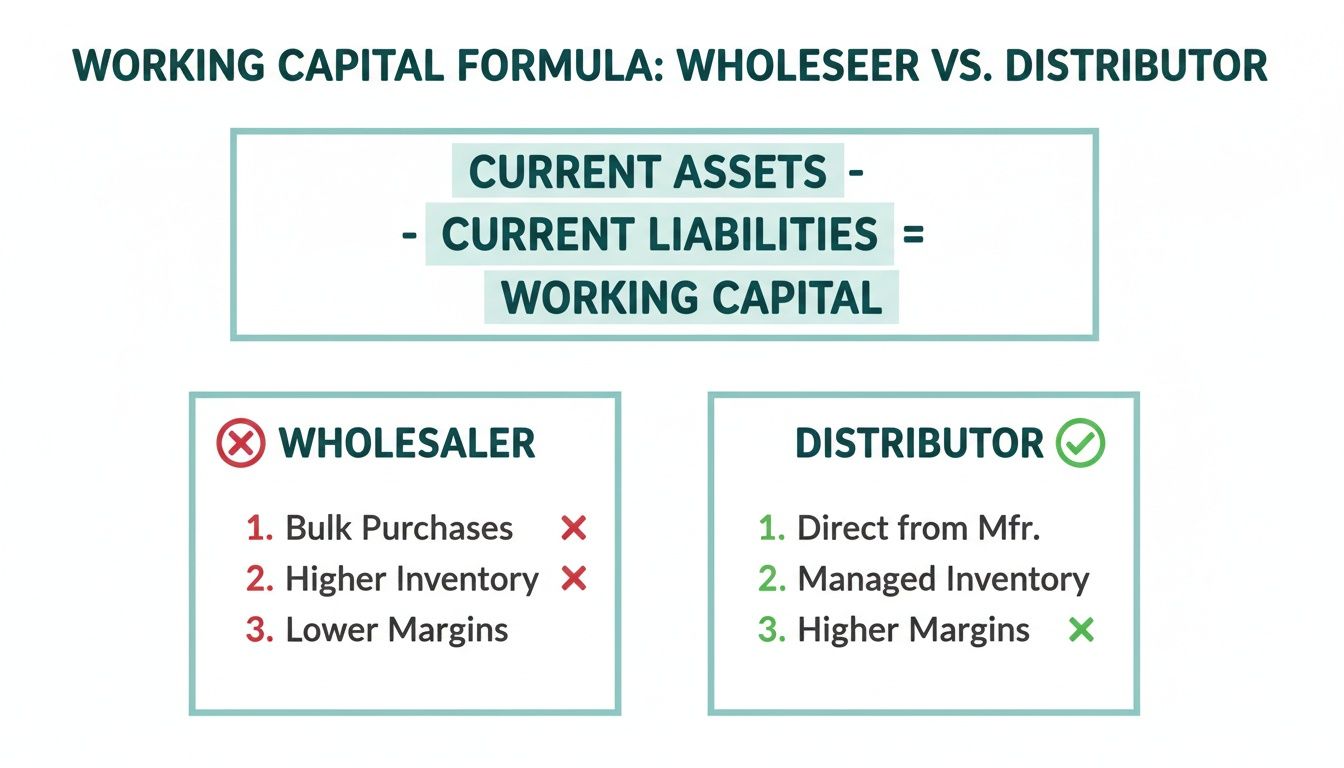

A Tale of Two Wholesalers

The comparison of these two businesses shows how different management of receivables and payables can lead to dramatically different outcomes, even when total assets and liabilities seem comparable.

SME 1 (Positive WC):

- Total Current Assets: AED 650,000

- Total Current Liabilities: AED 350,000

- Working Capital: AED 300,000

- Interpretation: Healthy liquidity. Can cover all short-term debts and has AED 300,000 spare for operations and growth.

SME 2 (Negative WC):

- Total Current Assets: AED 700,000

- Total Current Liabilities: AED 750,000

- Working Capital: -AED 50,000

- Interpretation: Insolvent. Not enough liquid assets to cover short-term debts, facing a shortfall of AED 50,000.

The stark difference isn't about who sells more; it's about who manages their cash flow better. The first wholesaler is sitting on a goldmine of AED 400,000 in receivables. If they could unlock that cash, their financial story would be completely transformed, flipping their negative position into a powerfully positive one.

Getting this calculation right is a survival skill for SME suppliers in the MENA region. Staying on top of regulations like the upcoming UAE E-invoicing mandates is also vital to ensure the financial data you're using is accurate.

And, of course, how you manage your payment terms is central to all of this. Understanding what is trade credit is fundamental, as it directly shapes both your accounts receivable and payable.

Interpreting Your Working Capital Figure

So, you’ve calculated your working capital. Now what? The number itself is just the starting point; the real value comes from understanding the story it tells about your business. It's a direct signal of your company's short-term financial health and how nimble you can be.

Getting this interpretation right is what turns a simple calculation into a powerful diagnostic tool. The result can be positive, negative, or even zero, and each one paints a very different picture. Think of it as a quick financial check-up that helps you decide your next move.

From a Simple Number to a Powerful Ratio

For a more precise view, I always recommend looking at the working capital ratio. It gives you a much clearer picture of your liquidity than the raw number alone. The formula is refreshingly simple:

Working Capital Ratio = Current Assets / Current Liabilities

A ratio greater than 1.0 is the first sign of good health—it means you have more current assets than you have current liabilities. But if your ratio dips below 1.0, that’s a red flag. It signals negative working capital, meaning you don’t have enough liquid assets on hand to cover your short-term debts.

Let’s break it down further:

- A ratio between 1.5 and 2.0 is often considered the sweet spot. This suggests you can comfortably cover your bills without having too much idle cash just sitting around.

- A ratio below 1.2 could mean you're sailing a bit too close to the wind. You might find it tough to pay suppliers on time or handle an unexpected expense.

- A very high ratio (above 2.0) isn't necessarily a cause for celebration. It might mean your money isn't working hard enough for you. This often points to excess inventory tying up cash or too much money in a low-interest bank account that could be reinvested for growth.

This visual shows just how different the working capital positions can be between business models.

As you can see, the distributor's healthy position is a world away from the wholesaler's, perfectly illustrating how day-to-day cash flow management directly impacts financial stability.

Why Industry Context is Everything in the UAE

What’s considered “good” working capital isn't a universal standard. This is especially true in a diverse and dynamic market like the UAE, where the ideal ratio can vary dramatically from one industry to the next.

A construction supplier, for instance, needs a high ratio to manage huge material purchases and long project timelines. On the other hand, a digital marketing agency with almost no inventory and quick payment cycles can operate perfectly well with a much lower ratio. The only way to get a true sense of your performance is to compare your numbers to industry benchmarks.

Knowing how to calculate and interpret working capital empowers finance leaders at MENA-based SMEs to navigate market volatility—a key factor in the UAE's economic resilience. Even as regional revenue grew, only 48% of firms improved their working capital year-over-year. This highlights just how important it is to spot trapped cash, especially in sectors like automotive and F&B. You can learn more about the economic trends shaping the UAE in this report.

By regularly keeping an eye on this metric and understanding it within your industry's context, you can spot potential cash flow problems long before they become a real threat. It transforms a simple accounting figure into your strategic guide for sustainable growth.

Practical Ways to Boost Your Working Capital

Okay, so you’ve crunched the numbers and you know where your working capital stands. What now? It’s time to move from theory to action. A healthy working capital figure isn’t just a nice-to-have metric for a report; it's the lifeblood of your business, especially for SMEs here in the UAE.

Improving this number isn't about some massive, complicated business overhaul. It’s all about making smart, targeted tweaks to how you handle your assets and liabilities. The core idea is simple: get cash in the door faster while being strategic about how and when it goes out.

Get Smarter with Your Inventory

Think of excess inventory as cash sitting on a warehouse shelf, gathering dust. You obviously need enough stock to keep customers happy, but holding too much just ties up funds and racks up carrying costs. A few smart inventory practices can free up that cash in no time.

- Try a Just-in-Time (JIT) approach: Instead of stockpiling, try to order goods closer to when you actually need them. This move alone slashes storage costs and lowers the risk of getting stuck with outdated products.

- Dig into your sales data: Take a hard look at what’s flying off the shelves and what’s not. Funnel your capital into the fast movers. For the slow sellers? Consider a sale or bundle deal to turn that stagnant stock back into liquid cash.

Speed Up Your Accounts Receivable

For many B2B companies, the biggest working capital killer is the long wait between sending an invoice and seeing the money hit your account. If you can shorten that collection window, you'll see an immediate, positive impact on your cash flow. It's a critical piece of the puzzle, which we cover more deeply in our guide to the cash conversion cycle.

One of the most powerful moves you can make is to unlock the cash tied up in your unpaid invoices. Why wait 30, 60, or even 90 days for a customer to pay when you can get that money now?

This tactic gives your current assets a direct shot in the arm by turning receivables into cash, all without adding to your liabilities. The result is a much stronger working capital position, giving you the freedom to pay suppliers on time, take on bigger orders, or even offer better terms to land your next major client.

Be Strategic with Your Accounts Payable

While you're working to get paid faster, the other side of the coin is paying your own suppliers more strategically. This absolutely does not mean paying late—that’s a quick way to ruin your reputation and business relationships.

It’s about using the full payment terms your vendors give you. If a supplier offers 60-day terms, use all 60 days. This simple act keeps cash in your business longer, where it can cover payroll or other immediate needs. It’s all about managing your liabilities intelligently to give your working capital a lift. Combine these three strategies, and you'll be in firm control of your company's financial health.

Got Questions About Working Capital? We’ve Got Answers.

As you start digging into your own numbers, a few questions are bound to pop up. That’s perfectly normal. Getting to grips with the finer points of working capital is what separates businesses that just survive from those that truly thrive.

Here are some of the most common questions we hear from business owners across the MENA region, answered in plain English.

What’s a Good Working Capital Ratio for a Small Business in the UAE?

A good rule of thumb is to aim for a working capital ratio between 1.5 and 2.0. This sweet spot usually means you've got enough cash and other current assets to comfortably cover your short-term bills, without leaving too much money idle.

But—and this is a big but—it’s not a one-size-fits-all number. A retail business holding a lot of stock will naturally need a higher ratio than, say, a digital marketing agency with very little inventory. The smartest move? See how you stack up against others in your industry and, more importantly, track how your own ratio changes over time.

Is It Possible to Have Too Much Working Capital?

Absolutely. While having plenty of working capital feels safe, it can actually signal that your money isn't working hard enough for you. It's a classic sign of inefficiency.

Think of it this way: excess working capital could mean you have cash gathering dust in a bank account instead of being invested back into the business. It might also point to money being tied up in slow-moving inventory or suggest you're not making the most of the payment terms your suppliers are offering. The goal isn't just to have a high number; it's to have the right number.

How Can Invoice Discounting Help My Working Capital?

Invoice discounting gives your working capital a direct and immediate boost. It's a straightforward process: you essentially turn your unpaid invoices (accounts receivable) into cash right away.

Instead of waiting 30, 60, or even 90 days for a customer to pay, you get the cash now. This instantly improves your current assets without adding a single dirham to your liabilities. The result is a much healthier working capital position, freeing up the cash you need to pay your staff and suppliers, or jump on a new opportunity. It’s one of the fastest ways to shorten your cash conversion cycle.

Ready to stop waiting on unpaid invoices and take control of your cash flow? Through Comfi's platform, our clients have been able to unlock the working capital tied up in their receivables in as little as 24 hours. Learn more about how we help businesses like yours grow without financial constraints.

Related Reading

- How Can MENA SMEs Master Working Capital?

- Staffing Agency Payroll Financing UAE: Boost Cash Flow 2026

- SME Cash Flow Management: A Guide for MENA Businesses

- Improve Working Capital for UAE IT Services Business

Looking to improve your cash flow? Explore Comfi's Invoice Discounting solutions. Get started today.