Underwriting Automation: Faster Decisions for Lenders

A dealer in Dubai commits to a new vehicle order in the morning and needs a funding decision before the stock allocation disappears. A building materials distributor in Riyadh ships on open account to repeat buyers, but each new order changes exposure, tenor, and concentration risk. In both cases, the pressure is not theoretical. Revenue depends on whether credit can keep up with the trade cycle.

Manual underwriting is poorly suited to that pace. Teams still collect statements over email, re-enter invoice data into spreadsheets, call customers to resolve mismatched fields, and wait for an approver who is balancing ten other priorities. The result is familiar across MENA trade and dealer finance. Goods sit, dealer lines tighten, supplier confidence drops, and finance teams spend their time on administration instead of exposure management.

Underwriting automation improves this by turning scattered data into a repeatable decision process. It uses document extraction, policy rules, system integrations, and case routing to handle routine decisions quickly while sending exceptions to an experienced credit officer. That trade-off matters. Full automation is rarely the goal in B2B finance. The better goal is faster recurring decisions with tighter controls, especially when the same buyer, dealer, or supplier comes back every week with a new transaction.

This matters in MENA because many financing decisions are tied to live trading relationships rather than one-off consumer applications. A dealer floorplan facility, a distributor credit line, or supplier finance program needs ongoing re-assessment as inventory turns, invoices age, payment behavior shifts, and utilization climbs. Static approval at onboarding is not enough. Decisioning has to keep pace with the book that already exists.

The broader operating environment is also pushing firms in this direction. Real-time payment infrastructure, stronger digital adoption, and rising expectations from SME customers all reduce tolerance for slow credit operations. Firms that study the Future of banking automation usually reach the same conclusion. Underwriting speed improves most when it is connected to onboarding, verification, payments, and internal workflow design, not treated as a standalone software purchase.

For SME finance managers, this is an operating model choice with direct commercial impact. Faster routine approvals help dealers replenish stock on time. Cleaner exception handling helps credit teams control risk without blocking good business. Ongoing automated review helps lenders and platforms respond to changing transaction patterns before arrears, disputes, or concentration issues become expensive.

Introduction Beyond Manual Checks

A distributor in Dubai approves a dealer order in the morning, expects stock to move by the weekend, and requests financing against that turnover. By the time a credit analyst has checked PDFs, chased missing documents, and reworked the case in a spreadsheet, the commercial moment may already be gone. In B2B trade and dealer finance, underwriting delay does not just slow a loan file. It slows inventory rotation, shipment release, and cash conversion across the relationship.

Manual review struggles here because the decision is rarely one-and-done. The same dealer draws again. The same buyer requests new terms. The same supplier asks for cover on another shipment under slightly different conditions. Teams end up rechecking many of the same facts while the risk itself keeps changing.

That creates a practical operating problem for SME finance managers in MENA. Facilities are often tied to real commercial activity, not a single consumer-style application. Floorplan finance, invoice discounting, distributor programs, and supplier-led credit all depend on recurring decisions around utilisation, payment behaviour, document quality, and concentration exposure. A static approval at onboarding leaves too much unmanaged between day one and the next transaction.

Underwriting automation changes that operating model. It captures data from trade documents and business records, applies policy checks consistently, flags exceptions early, and routes only the cases that need judgment. Good systems do more than shorten approval time. They support repeated, event-driven credit decisions across the life of an account.

The benefit is control as much as speed. Credit teams can spend more time on edge cases, dealer deterioration, and buyer concentration, and less time re-keying invoices or validating the same licence twice. That matters if your team is trying to scale a book without adding the same headcount to handle each new program. It also matters if you are tightening credit risk controls for SME portfolios while still trying to protect sales flow.

Firms reviewing the Future of banking automation usually reach a similar conclusion. Automation works best when underwriting is connected to onboarding, document verification, transaction monitoring, and workflow design, rather than treated as a standalone scoring tool.

In the MENA trade context, that distinction is important. The value is not limited to faster first approvals. True value comes from making better recurring decisions on live dealer and supplier relationships, with enough consistency to scale and enough human review where policy, fraud risk, or exposure quality demands it.

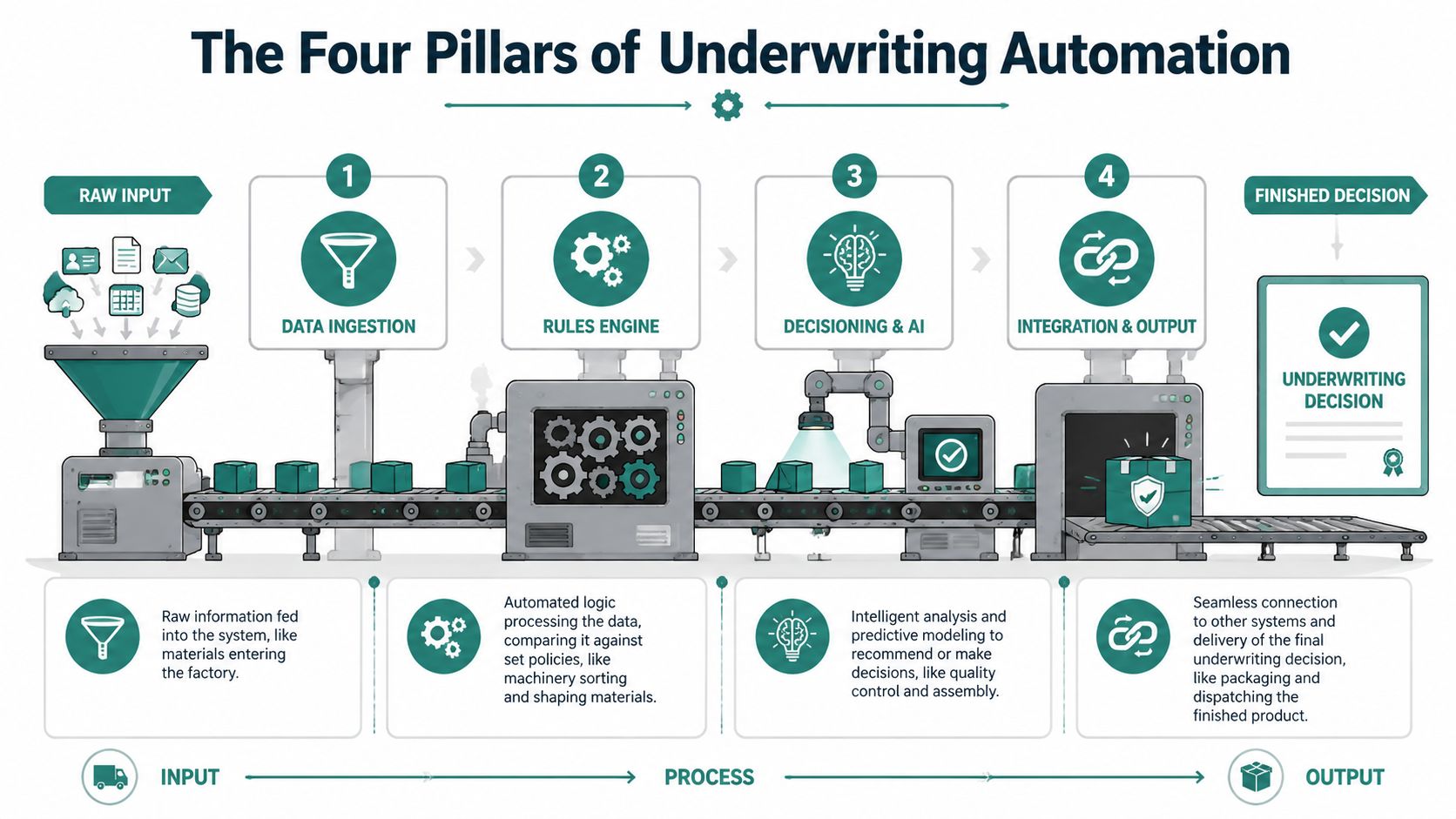

The Four Pillars of Underwriting Automation

A useful mental model is a factory line. Raw material goes in, processing happens in stages, and the output is consistent because each stage has a clear job. Underwriting automation works in much the same way.

Data ingestion

The line starts with inputs. In SME and trade environments, that means bank statements, invoices, trade licences, financial statements, buyer information, stock lists, and supporting documents. Good systems don't just collect files. They normalise them.

The challenge is that B2B submissions are rarely tidy. A dealer might submit vehicle schedules from different systems. A wholesaler might upload invoices with inconsistent formats. Automation matters here because it converts those documents into usable fields instead of leaving a team to re-key everything manually.

For finance leaders, this is the stage where most implementation problems begin. If you accept poor-quality inputs without clear validation rules, every later stage becomes harder.

Rules engine

Once the data is structured, the next stage is policy logic. The rules engine is where the business defines what qualifies, what needs escalation, and what should stop immediately. This is less glamorous than AI, but in practice it's often the part that determines whether the operation stays controlled.

Examples of rules include document completeness checks, exposure limits, buyer concentration checks, invoice ageing thresholds, or inventory-specific restrictions. In trade and dealer contexts, these rules often matter more than broad consumer-style scorecards because the underlying assets and transaction cycles change constantly.

A solid rule set should be readable by the business, not just by developers. That's also why teams reviewing broader risk frameworks often benefit from grounding their approach in operational credit discipline, such as the principles discussed in this credit risk management guide.

Decisioning and AI

The system evaluates the meaning of inputs and rules. Industry guidance notes that with multimodal automation, fewer than 10% of processing tasks may still require human involvement, which shows that the main gains come from straight-through processing of simpler cases and exception handling for edge cases, as described in this underwriting automation glossary.

That doesn't mean every decision should be fully automated. It means routine cases should not consume the same energy as complex ones.

Practical rule: Use automation to narrow the human review surface, not to pretend every case is identical.

Integration and output

The final pillar is what many teams underestimate. A decision only becomes useful when it reaches the right system and triggers the next action. That may be notifying a sales team, updating an internal dashboard, creating a review queue, or passing an approved transaction into an operational workflow.

Without this last step, firms end up with a polished scoring engine and the same old manual bottlenecks at the end. The best underwriting automation setups connect decisioning directly to action.

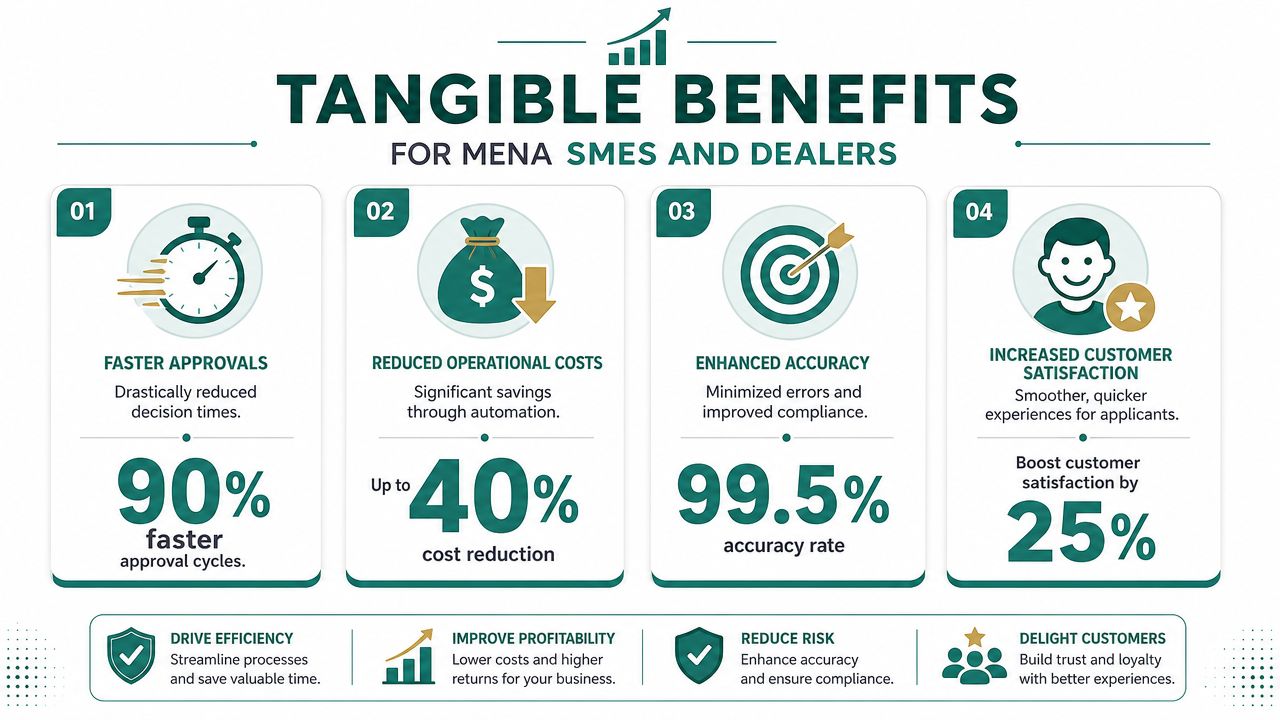

Tangible Benefits for MENA SMEs and Dealers

The business case becomes clearer when you move beyond generic speed claims and look at how these systems affect day-to-day operations for suppliers, distributors, and dealers.

Where the gains show up first

For well-structured underwriting documents, modern intelligent document processing can achieve 90% or higher straight-through processing, with extraction accuracy above 95% on key fields. For more complex files, accuracy typically stays in the 85% to 92% range. The same source notes that workflows that once took weeks can be compressed into minutes or hours for standardised cases, as explained in this insurance underwriting automation overview.

That has direct implications for MENA firms dealing with repeat transactions.

- Faster stock rotation: Dealers can move from “waiting for review” to acting on available inventory opportunities more quickly.

- Cleaner invoice handling: Suppliers spend less time reconciling submitted paperwork when core fields are captured consistently.

- Less manual rework: Finance teams stop duplicating checks across email, spreadsheets, and ERP entries.

- Better prioritisation: Underwriters and risk staff can focus on exceptions, disputes, and unusual structures instead of low-risk repetitive files.

Why B2B operations benefit differently from consumer flows

Consumer underwriting is often described as a one-time decision. B2B underwriting isn't that tidy. A supplier might assess the same buyer repeatedly across new invoices. A dealer's risk profile may change with inventory mix, sales velocity, or settlement patterns.

That's why the operational benefits are often more important than the headline automation itself.

- Consistency in repeat decisions: Similar cases are treated similarly, which helps sales, operations, and finance work from the same expectations.

- More predictable customer experience: Buyers and counterparties get quicker responses instead of uncertain follow-ups.

- Stronger internal control: Policy gets applied the same way even during busy periods or team changes.

- Capacity without proportional headcount growth: As transaction volume rises, the process scales more cleanly than a manual queue.

A practical example of where this matters is automotive distribution, where repeated stock-related decisions need to happen quickly and with discipline. The mechanics of that model are easier to understand through solutions designed for dealer financing workflows, where inventory-linked decisions are part of normal operations rather than occasional exceptions.

When underwriting becomes operationally reliable, businesses don't just make faster decisions. They plan inventory, purchasing, and collections with more confidence.

KPIs Regulation and Data Privacy in the UAE

A trade finance program can approve invoices in minutes and still create risk if nobody is watching the right signals. In UAE-based B2B underwriting, the job is not just faster approvals. It is disciplined repeat decisioning across buyers, dealers, limits, tenors, and document flows.

KPIs that actually matter

The best KPI set reflects how the credit engine behaves day after day, not just how fast it responds.

For dealer finance and supplier-led trade programs, I would track six measures closely:

- Decision turnaround time: How long standard requests take from submission to approve, refer, or decline.

- Straight-through processing rate: The share of recurring cases that complete without analyst intervention.

- Refer rate by segment: How often the system sends cases to review, broken out by buyer type, dealer tier, product line, or invoice profile.

- Policy adherence: Whether approvals, declines, limit changes, and overrides match the written credit policy.

- Post-decision performance: How approved exposures perform after disbursement or invoice acceptance.

- Exception concentration: Which missing documents, data mismatches, expired trade licenses, or tax and invoice issues repeatedly slow decisions.

These metrics need to be read together. A very low refer rate may mean the rules are clear and well tuned. It can also mean the system is passing weak files without enough scrutiny. Fast turnaround has the same problem if collections performance worsens a month later.

One more point matters in B2B. Review recurring decision quality, not just first-time approval quality. In trade and dealer finance, pressure sits in limit refreshes, repeat orders, invoice-level checks, and exceptions around settlement behavior.

Why the UAE context matters

The UAE is a strong market for underwriting automation because the operating environment already favors digital workflows, structured records, and faster transaction handling. That matters more in B2B than in consumer lending because decisions often depend on document consistency across invoices, deliveries, payments, and counterparty records.

For finance managers, the practical implication is straightforward. Underwriting no longer sits in a closed credit team process. It depends on how well ERP data, bank data, invoices, KYC records, and payment rails line up. In many cases, cleaner invoice data improves underwriting quality as much as a better scorecard does, which is why many teams reviewing credit automation are also tightening their e-invoicing controls and workflows.

Data privacy and governance

Data privacy becomes more sensitive once decisions are recurring and partially automated. A one-time borrower file is one thing. A live B2B program may process updated invoices, payment behavior, buyer exposure, utilization, and exception history every week or every day.

That changes the governance standard. Finance leaders need clear rules for who can view raw documents, who can edit decision logic, who can override outcomes, and how every override is recorded for audit. Access should follow role, not convenience. Retention periods should match legal and operational need. Third-party data sharing should be documented before the integration goes live, not after a dispute.

Teams that need a plain-language reference for internal discussions can use this overview with information on user data handling as a starting point. It is not a substitute for legal review, but it helps frame the operational questions that usually get missed early.

In practice, the strongest control environment is usually simple. Keep audit trails complete. Separate policy ownership from day-to-day case handling. Test override patterns monthly. If the system supports revolving trade limits or dealer stocking lines, monitor whether data permissions remain appropriate as more counterparties and transactions enter the program.

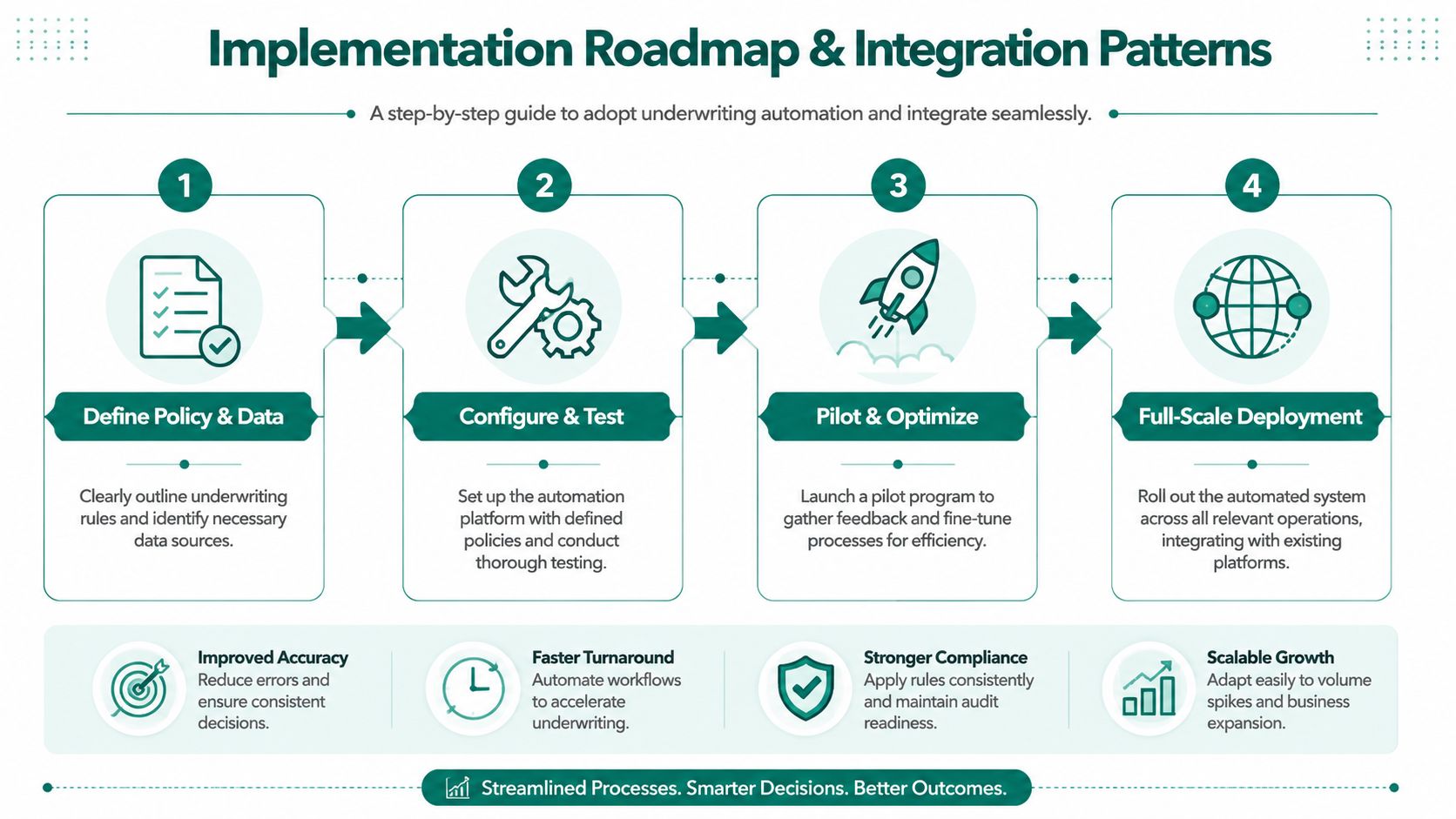

Implementation Roadmap and Integration Patterns

Most firms don't fail because the idea is wrong. They fail because they automate a messy process without first deciding what the process should do. A workable implementation roadmap starts with policy clarity, not technology selection.

Start with policy, not software

Before connecting any data source, define what the system is allowed to decide. That means spelling out approval conditions, referral triggers, hard stops, document requirements, and acceptable override paths.

If this logic only exists in a senior manager's head, automation will expose that weakness immediately. The process must be explicit.

A practical sequence looks like this:

- Define decision policy: Write down the rules for approve, refer, and decline outcomes.

- Identify required data: List which documents and data fields are necessary.

- Set confidence thresholds: Decide when automation is sufficient and when human review is mandatory.

- Map exceptions: Prepare routes for incomplete, disputed, or unusual files.

Configure around standard cases first

One of the most useful benchmarks in automation is whether standard cases can move quickly without weakening controls. Industry guidance notes that AI-powered underwriting systems can analyse factors such as debt-to-income ratio in seconds, reducing turnaround from weeks to minutes for standard cases when scorecards are paired with calibrated business rules, as outlined in this AI underwriting and risk management article.

The lesson for SME and trade contexts is straightforward. Don't begin with the hardest cases. Start by automating the predictable cases with clean documents and known patterns. Then build escalation logic for everything else.

The fastest path to value is usually narrow. Automate the repeatable lane first, then widen it carefully.

Choose an integration path that fits the business

There are usually two practical adoption patterns.

- API-led integration: Best when underwriting decisions need to sit inside an existing ERP, marketplace, procurement flow, or dealer platform. This approach offers control and enhanced workflow integration.

- Low-code plugin deployment: Better when the business wants to move quickly without a large development project. This works well for teams that need a digital workflow before they need an extensively customised one.

Both paths can work. The wrong choice is usually trying to force a fully bespoke build before the policy, data quality, and review model are stable.

Test with real historical files

A pilot should use old applications, invoices, or stock data that reflect real operating conditions. You want to see where extraction fails, which rules create false referrals, and where a human still adds value.

Good calibration isn't about proving the system is perfect. It's about learning where to trust automation and where not to.

Real-World Use Cases with Comfi

The clearest examples of underwriting automation in MENA sit in recurring B2B decisions, not one-off consumer applications. That's especially true in inventory-linked and invoice-linked transactions, where the underlying exposure changes over time.

Automotive dealer inventory decisions

An automotive dealer in the UAE often faces a simple but costly problem. Vehicles are already in stock, but cash is still tied up in them. Until that stock turns into cash, restocking decisions become conservative, even when there is clear buyer demand.

Dynamic underwriting matters more than static approval. The relevant question isn't only whether the dealer is creditworthy in general. It's also what the current stock looks like, how quickly units are moving, and whether the inventory position supports another transaction.

That approach fits the wider UAE context. With outstanding private sector bank credit at about AED 1.24 trillion in 2024, the primary opportunity increasingly sits in dynamic trade and inventory decisions that are re-evaluated as stock moves, rather than in consumer-style one-time approvals, as discussed in this analysis of underwriting for trade and inventory finance.

In practice, automation helps by structuring inventory data, applying policy rules to eligible stock, and narrowing the cases that need manual review. The result is a cleaner path to releasing cash tied up in vehicles without treating every request as if it were entirely new.

Invoice-based supplier workflows

Now consider a B2B electronics supplier selling to business buyers on extended payment terms. The issue isn't usually whether sales exist. The issue is whether the supplier has to wait through the full payment cycle before using that cash again.

In this case, underwriting automation evaluates the invoice, checks whether the supporting data is complete, assesses buyer-related risk signals, and determines whether the transaction fits policy. Because invoices age and counterparties behave differently over time, these checks are recurring by nature.

That recurring nature is what makes B2B underwriting different. The model works best when the system can reassess rather than assume yesterday's decision still holds today.

Why these use cases matter

Both examples show the same principle. In MENA trade environments, the strongest value often comes from re-underwriting at the transaction level.

- Stock changes: Inventory value and composition don't stay fixed.

- Invoices mature: Ageing affects risk and operational urgency.

- Buyer behaviour evolves: Payment patterns can shift across cycles.

- Exposure concentration moves: New orders can change the risk picture quickly.

Underwriting automation becomes most useful when it is embedded into those recurring commercial moments, not when it is treated as a one-time gate at onboarding.

Avoiding Pitfalls and The Future of Decisioning

The most common mistake is feeding weak data into a fast system. Automation can process poor inputs efficiently, but it can't make them reliable. Clean document capture, validation checks, and clear exception handling matter more than flashy models.

Another problem is black-box anxiety. If a finance manager can't explain why a file was referred or declined, trust drops quickly. Keep the logic visible. Show the failed rules, missing fields, and confidence flags. Explainability doesn't just help compliance. It helps adoption inside the business.

Over-automation is the third trap. Not every trade file should go straight through. Disputed invoices, unusual dealer stock, incomplete submissions, and concentration risk cases still need human judgement. The strongest operating model is hybrid. Machines handle repeatability. People handle ambiguity.

Teams also shouldn't ignore technical governance. When underwriting logic touches sensitive business and customer data, review practices around integration security, permissions, and code quality matter. For organisations tightening control over AI-enabled workflows, this perspective on an AI code security audit is a useful reminder that speed and control have to move together.

Good underwriting automation doesn't eliminate judgement. It reserves judgement for the files where it earns its keep.

The future of decisioning in MENA is likely to be more embedded, more continuous, and more transactional. A supplier won't think of underwriting as a separate department activity. It will sit inside the invoice flow. A dealer won't wait for a disconnected review cycle. Decisioning will happen alongside inventory movement. That shift is already visible. The next advantage won't come from digitising manual steps alone. It will come from building decision systems that can react as the trade itself changes.

Businesses across MENA don't need more paperwork between demand and action. They need faster, better-structured decisions that fit how trade works. If you're exploring practical ways to access working capital, support dealer inventory cycles, or streamline invoice-based transactions, Comfi is worth a closer look.