A Guide to Trade Credit for Modern MENA Businesses

At its core, trade credit is a straightforward B2B arrangement: a supplier provides goods or services upfront but allows the buyer to pay at a later date—typically within 30, 60, or 90 days. It’s a classic way for suppliers to secure larger deals and for buyers to manage their inventory without an immediate cash outlay.

Understanding Trade Credit in the MENA Market

For small and medium-sized enterprises (SMEs) competing across the MENA region, offering trade credit isn't just a perk; it's often a necessity for doing business. It’s what helps land larger orders and build the kind of trust-based relationships that last. By giving customers the breathing room to pay later, suppliers can significantly drive up their sales volume.

From the buyer's perspective, the benefit is equally clear. They gain the time needed to sell the inventory they just bought before the payment is due, which is a huge boost to their cash flow cycle. In fast-moving industries where managing stock levels is a constant challenge, that kind of flexibility is invaluable.

Accounting and Cash Flow Implications

The mechanics of trade credit leave a clear footprint on the financial statements of both parties. When a supplier makes a sale on credit, they record that amount as accounts receivable. This becomes an asset on their balance sheet—money they are owed. Conversely, the buyer records the same amount as accounts payable, a liability they need to settle.

This is where the real impact on operations comes in. While your revenue looks great on paper, your actual cash in the bank hasn't changed. That lag between invoicing and receiving payment can put a serious strain on your own ability to cover costs like payroll or rent. This is why mastering receivables is one of the most critical skills in business. To learn more, check out our guide on how to optimize your payments and receivables management and keep your cash flow healthy.

For many SMEs in the UAE, trade credit is not just a payment term—it's the foundation of their business relationships. Mastering its impact on cash flow is the difference between struggling and scaling.

Successfully navigating the competitive MENA market means getting a firm grip on these financial dynamics. It's a constant balancing act between chasing sales and keeping enough cash on hand to run the business—a challenge that truly defines success in this region.

The Hidden Risks of Extending Trade Credit

Offering trade credit can feel like a standard part of doing business, and it can absolutely be a powerful way to win deals. But it’s a double-edged sword. Every time you extend credit, you’re introducing a significant financial risk to your own company.

The most obvious danger is late payment or non-payment. Even a small delay can throw your cash flow into chaos, creating a domino effect that impacts your ability to pay your own bills. Every single sale on credit means your cash—the money you need for payroll, suppliers, or growth—is locked up in accounts receivable. It’s sitting on your balance sheet, waiting for someone else to pay up.

The Real Cost of a Single Default

Beyond the immediate cash crunch, there's the administrative headache. Chasing payments, sending reminders, and making follow-up calls all consume time and resources that could be spent growing the business. But the real danger snaps into focus when a customer defaults completely.

Let’s run the numbers on a practical scenario:

- The Business: A Dubai-based electronics distributor operating with a 10% net profit margin.

- The Sale: They provide a new retail client with AED 100,000 in trade credit.

- The Default: The client stops responding and the invoice is never paid.

To recover that lost AED 100,000, the distributor now has to generate AED 1,000,000 in new sales. The profit from ten other large, successful deals is instantly wiped out by a single bad debt. This is precisely why mitigating payment risk isn't just a "nice-to-have"—it's fundamental to survival.

This illustrates a harsh reality of B2B sales: the profit from many successful deals can be erased by the loss from just one unpaid invoice. This makes managing credit risk essential.

This dependence on trade credit is especially intense in the MENA region, where access to traditional business support can be a hurdle for many SMEs. A significant number of firms are self-funded, making them completely reliant on prompt customer payments to stay afloat.

Recognizing these dangers is the first step. The next is building a financial strategy that protects you from them.

Trade Credit vs. Invoice Discounting: A Clear Comparison

On the surface, both trade credit and invoice discounting appear to be tools for managing B2B payments. However, they serve fundamentally different purposes and operate in opposite ways. The right choice for your business depends on a key question: what are you trying to achieve with your cash flow, risk management, and customer relationships?

Think of trade credit as a passive sales tool. You offer payment terms to make a deal more attractive and then wait to get paid. Invoice discounting, in contrast, is an active financial strategy. It allows you to take your outstanding invoices and convert them into cash immediately through a third-party platform, rather than waiting on your customer's payment schedule.

Core Operational Differences

The biggest distinction lies in who controls your cash flow timeline. When you offer traditional trade credit, your customer is in the driver's seat. They determine when you get paid, leaving your funds locked up for 30, 60, or even 90 days. This creates significant uncertainty and risk.

Invoice discounting flips that dynamic. Instead of waiting, you decide when to access the cash you've already earned. This proactive approach gives you the financial certainty needed to run your operations smoothly, which is especially critical in the high-volume trade environment of the MENA region. With total exports recently hitting USD 1,125.5 billion and imports reaching USD 966.4 billion, SMEs with ready cash can seize opportunities their competitors cannot. You can explore more of this data on regional trade volumes from the World Bank.

The fundamental choice is this: Do you want to wait for your money, or do you want to unlock it now? Trade credit means waiting and hoping, while invoice discounting means taking control of your cash flow.

Comparing Key Business Impacts

To make an informed decision, it's helpful to compare these two options side-by-side and see how they stack up on factors that truly matter to a growing business.

- Access to Cash: With trade credit, your cash is tied up until your customer pays. With invoice discounting, you can receive a large portion of your invoice value, often within 24 hours.

- Risk Responsibility: When you offer trade credit, you shoulder 100% of the risk if a customer pays late or not at all. A reliable invoice discounting solution allows you to transfer that credit risk to the service provider.

- Customer Interaction: Managing trade credit means your team is often tasked with chasing payments. When you use invoice discounting, the platform typically handles the collections process, freeing your team from that administrative burden. You can see how this works in our detailed guide on invoice discounting in the UAE.

- Business Scalability: Relying solely on trade credit can limit your growth. It strains your resources, making you hesitant to take on large new orders. Invoice discounting provides the immediate cash infusion needed to say "yes" to those growth opportunities with confidence.

Choosing the Right Tool for Different Business Scenarios

Theory is one thing, but how this plays out in the real world is another. Deciding between traditional trade credit and invoice discounting comes down to your immediate business needs and long-term strategy. The key is to match the right tool to the situation you’re actually facing.

For instance, extending standard trade credit makes perfect sense with trusted, long-term clients who have a flawless payment history. It's also a practical choice for smaller, low-value transactions where a slight delay won't put a serious dent in your cash flow. In these cases, the relationship-building aspect of trade credit often outweighs the need for immediate cash.

When to Choose Invoice Discounting

But when the stakes are higher, invoice discounting becomes the smarter, more strategic choice. It acts as a vital safety net, allowing your business to chase growth without shouldering unnecessary payment risk. Think of it as your go-to option when you need certainty and speed.

Invoice discounting really shines in specific scenarios:

- Fulfilling Large Orders: When a major order lands, especially from a new customer, you need capital now for production and supplies. Invoice discounting gives you immediate access to that order's cash value.

- Navigating Rapid Growth: During periods of expansion, cash is king. Unlocking your receivables ensures you have the funds to support hiring, marketing, and inventory investment without hitting the brakes.

- Securing Cash Flow: If your business runs on thin margins or needs predictable cash flow to manage its own payables, discounting invoices removes the anxiety of waiting for customers to pay.

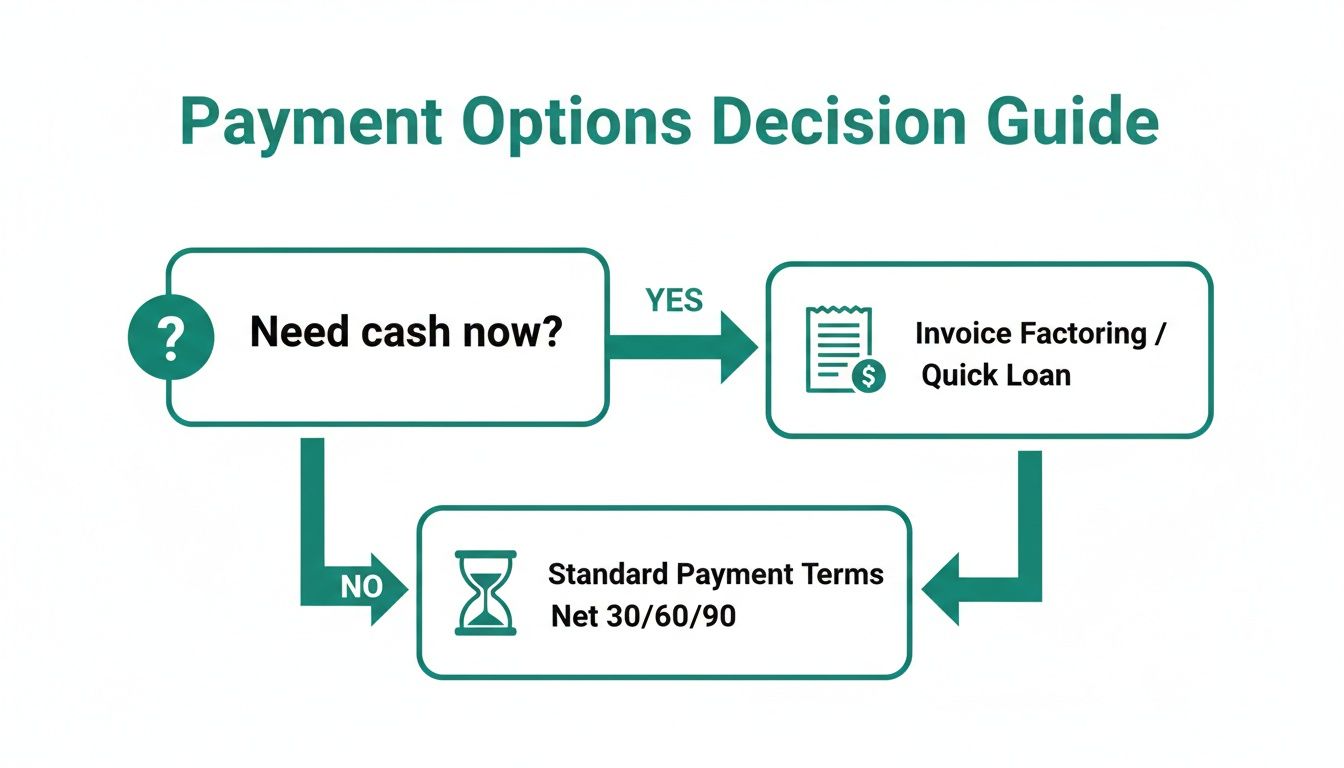

This decision tree helps simplify the core question: Do you need the cash now, or can you afford to wait?

As the flowchart shows, when immediate liquidity is the priority, invoice-based solutions offer a direct path to unlocking cash. Traditional terms, on the other hand, are better suited for situations where waiting is a viable option.

Case Study in Action: An automotive parts supplier in the UAE landed a major contract with a new car dealership. Instead of risking a cash flow gap by offering 90-day trade credit, they used invoice discounting. They received payment in just 24 hours, which allowed them to immediately fund their next production run and confidently pursue other large orders.

How Modern Solutions Mitigate Payment Risk

We’ve laid out the challenges. Now, let’s get into the solutions. Modern fintech platforms are completely changing how MENA businesses handle the risks that come with B2B sales. Offering trade credit is a must for growth, but it often leaves suppliers exposed to late payments or, worse, total defaults.

Of course, there are traditional tools like trade credit insurance. The market for this in the MENA region was a hefty USD 1,232.2 million in 2023, which shows just how seriously businesses take payment risk. You can read more about the MENA trade credit insurance market and its trajectory. But here's the catch: insurance is often a reactive measure you use after the risk is already on your books.

A Proactive Approach to Risk Management

This is where tools like Invoice Discounting come in. They offer a proactive way to secure your operations. Instead of just insuring against a potential loss, these services get the risk off your plate from day one by fundamentally changing how—and when—you get paid.

When you work with a platform like Comfi, the headache of running customer eligibility checks and chasing collections is no longer yours. That means your team isn't tied up making awkward phone calls or trying to figure out who is creditworthy.

Modern fintech solutions turn a traditionally high-risk process into a secure business advantage. They allow you to offer flexible payment terms without carrying the financial burden or administrative overhead yourself.

By offloading the credit risk, suppliers can confidently offer deferred payment terms to a much wider customer base. It’s a shift from playing defense to playing offense, empowering you to chase growth opportunities without hesitation.

Turning Risk Mitigation into a Growth Engine

The benefits go way beyond just playing it safe. Businesses that adopt these modern financial tools often see a real impact on their key growth metrics. They can offer competitive payment terms that win over new buyers who might have gone elsewhere.

Clients using these platforms find they can achieve tangible results that hit both their top and bottom lines:

- Significant sales uplifts: By making it easier for customers to say "yes," suppliers close bigger deals, more often.

- New customer acquisition: Offering flexible, risk-free payment terms becomes a powerful selling point that sets you apart from the competition.

- Unlocked working capital: Getting immediate access to cash from your sales means you can reinvest in inventory, marketing, or expansion without missing a beat.

Ultimately, these solutions do more than just manage risk. They turn a potential liability into a strategic asset that fuels sustainable growth and solidifies your position in the market.

Common Questions About Trade Credit

As businesses across the MENA region navigate B2B sales, a few key questions about cash flow consistently arise. Understanding the available tools, especially trade credit, is fundamental to building a sustainable business. Here are clear, practical answers to the questions we hear most often.

What's the Real Difference Between Trade Credit and Invoice Discounting?

The simplest way to think about it is this: who carries the risk, and who waits for the cash?

When you offer trade credit, you are the one taking the risk. You let your customer pay later, which means you carry 100% of the risk if they pay late or not at all. All the while, your money is tied up in that unpaid invoice, completely locked away until it finally gets settled.

Invoice discounting flips that script. It’s an active financial strategy where you sell your unpaid invoices to a third-party platform. This unlocks the value of your sales almost instantly, pumping cash back into your business without the agonizing wait. The risk is transferred, and you get paid. It's a straightforward way to maintain control over your cash flow.

Is Invoice Discounting a Good Move for Small Businesses in the UAE?

Absolutely. It’s an incredibly practical tool for SMEs, not just in the UAE but across the entire MENA region. Most small businesses don't have large cash reserves to fall back on, so invoice discounting provides a vital service by giving them immediate access to the money they've already earned.

This injection of liquidity is crucial for covering day-to-day costs, funding new projects, and seizing growth opportunities before they disappear.

For example, it gives SMEs the power to:

- Confidently say "yes" to bigger orders from new customers.

- Sidestep the cash flow gaps created by long customer payment terms.

- Invest in more inventory or expand their operations without delay.

Because modern solutions are designed specifically for SMEs, they are often a very accessible and powerful option.

How Exactly Does Offering Trade Credit Hurt My Cash Flow?

Offering trade credit directly creates a gap between the day you make a sale and the day you actually get paid. Every single time you extend credit, you’re reducing your available cash until that invoice is paid—even if your business is wildly profitable on paper.

This is how you end up in a classic cash flow crunch: a company that looks great on the profit and loss statement but doesn't have the actual cash to operate. It makes paying your own suppliers, covering payroll, and handling other essential costs a real struggle. This is precisely why managing your receivables or using a service like invoice discounting is so critical.

This delay doesn't just slow things down; it directly impacts your ability to run your business smoothly and fund your growth.

Ready to take control of your cash flow? With Comfi, you can get your invoices paid in 24 hours, eliminate credit risk, and clients are able to unlock their working capital to grow. Learn more and get started today.

Related Reading

- What Is Trade Finance and How Does It Work for SMEs

- What Is Trade Finance and How Does It Work for SMEs

- Trade Finance Fund

- Boost Resilience: Supply Chain Disruption Financing UAE

Looking to improve your cash flow? Explore Comfi's Invoice Discounting solutions. Get started today.