Top 10 Invoice Discounting Providers in the UAE for 2026

.png)

In the fast-paced MENA market, delayed payments can halt growth. For small and medium-sized enterprises (SMEs), waiting 30, 60, or even 90 days for an invoice to be settled means your capital is tied up, unavailable for new inventory, expansion, or payroll. This is where invoice discounting comes in as a practical tool that allows businesses to get immediate cash for their unpaid invoices. Unlike a traditional business facility, it is not about taking on new debt. Instead, you are unlocking the value of sales you have already made.

This guide provides a straightforward breakdown of the concept and highlights 12 key providers in the UAE, from modern fintech platforms to established banks. Our goal is to help you find the right fit to stabilise your cash flow and fuel your business growth.

1. Comfi

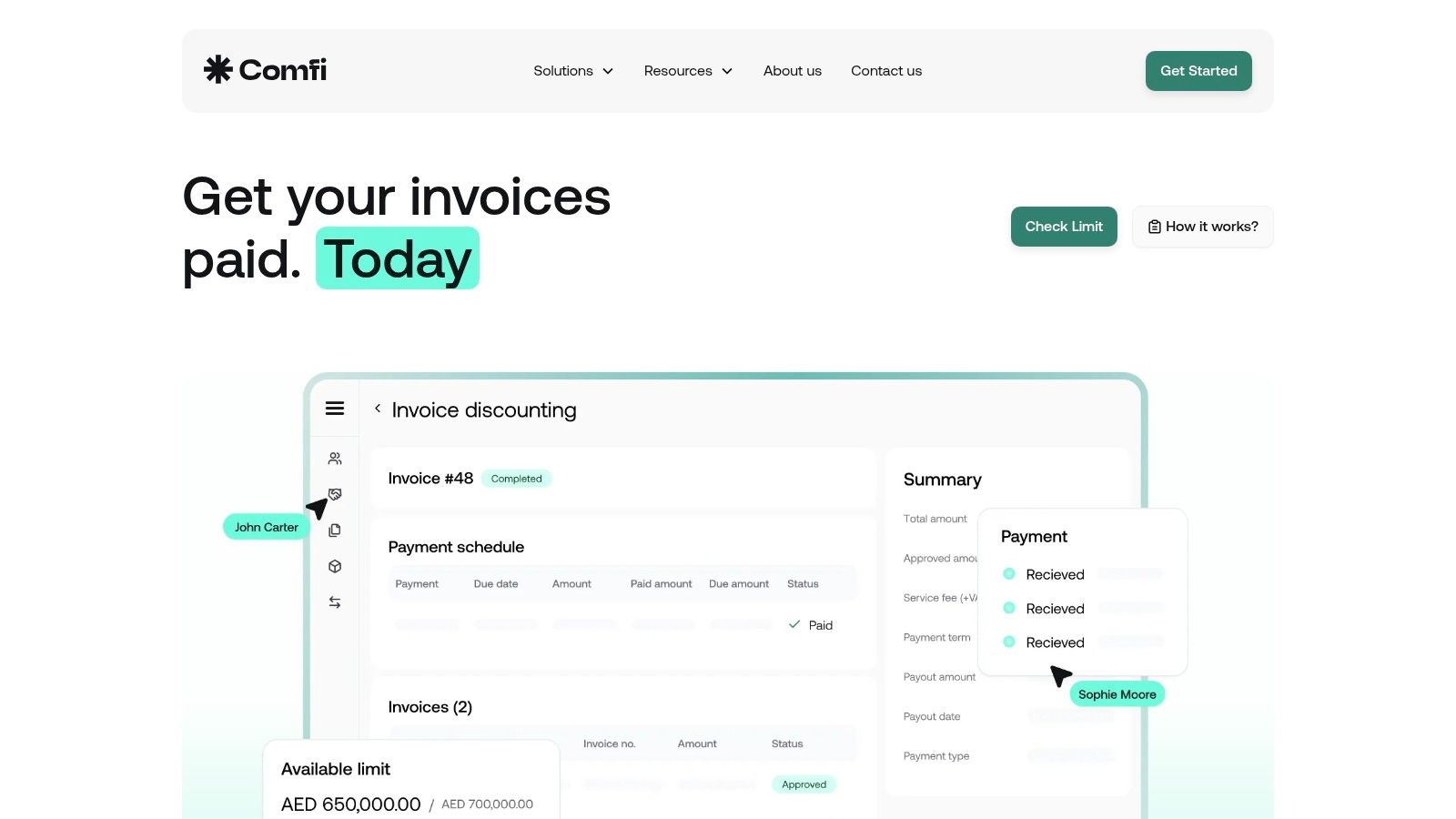

Comfi is a standout fintech platform in the UAE, engineered specifically for SMEs across the MENA region seeking to optimise their cash flow. It addresses a core challenge for growing businesses: delayed payments. Comfi advances payments for supplier invoices, effectively eliminating the typical waiting period and allowing businesses to reinvest in growth activities immediately. This approach removes payment risk and the burden of collections from the supplier.

What distinguishes Comfi is its blend of speed, accessibility, and measurable impact, tailored for the SME sector. With an impressive approval rate of approximately 85% and funds available within 24 hours of approval, the platform delivers on its promise of rapid cash access. Users report tangible business results, including up to 30% larger order sizes and around 20% new customer acquisition, demonstrating how predictable cash flow directly fuels expansion. The platform’s fully digital dashboard and developer-friendly API ensure it integrates seamlessly into existing B2B workflows.

Comfi’s model is particularly effective for businesses that rely on consistent turnover, such as electronics distributors, automotive dealers, and B2B marketplaces. By advancing payments for invoices, it helps them seize larger opportunities without capital constraints.

Key Highlights

- Rapid Fund Access: Eligibility checks are completed in minutes, with invoice payments advanced within 24 hours.

- High Approval Rate: An 85% approval rate makes its services highly accessible for a wide range of SMEs.

- Zero Payment Risk: Comfi manages the collections process, absolving suppliers of default risk and administrative overhead.

- Seamless Integration: A modern tech stack including a digital dashboard, low-code plugins, and a robust API allows for easy adoption.

Pricing and Availability

Comfi’s pricing and specific rates are customised based on the business’s profile and industry. Its primary operational focus is on the MENA region. Interested businesses are encouraged to use the "Check Limit" feature on their website to receive tailored terms. This approach ensures the structure aligns with each company's unique operational needs, a concept you can explore further by understanding the fundamentals of trade credit on comfi.ai.

Website: https://comfi.ai

2. Beehive

Beehive is one of the UAE's first and most established peer-to-peer (P2P) platforms, connecting SMEs with investors. Its marketplace model offers businesses invoice financing for receivables due within 30 to 120 days, allowing them to improve cash flow by accessing funds tied up in unpaid invoices. The process begins with a digital onboarding system designed to provide rapid decisions for qualified SMEs.

Unlike direct funders, Beehive facilitates funding from a pool of registered investors, which can lead to competitive rates. This approach to invoice discounting typically advances up to 80% of the invoice value, with funds often disbursed within 24 hours after approval and successful funding on the marketplace. This makes it a strong option for established SMEs looking for a proven, regulated platform to manage their short-term liquidity needs without waiting on lengthy bank processes.

- Best For: Established SMEs in the GCC seeking a marketplace model for invoice funding.

- Key Feature: P2P investor marketplace model with rapid decisions and disbursals.

- Limitation: The advance rate is typically capped at around 80%, and funding can depend on investor demand on the platform.

Website: https://www.beehive.ae/

3. Invoice Bazaar

Invoice Bazaar is a UAE-based specialist in receivables finance, offering a platform for businesses to manage cash flow through early invoice payments. It partners with established banks and regulated funds to deploy capital, providing a sturdy financial backing for its services. The platform is particularly notable for its unique offerings tailored to modern commerce, including traditional invoice discounting and a specialised Payment Gateway Finance programme for e-commerce sellers.

This model allows businesses to advance funds against future card or gateway receivables, a critical need for online retailers. By using Invoice Bazaar’s invoice discounting, suppliers can shorten their cash conversion cycle and access liquidity tied up in unpaid invoices or pending e-commerce payouts. Its focus on the UAE market and supply chain dynamics makes it a highly relevant choice for local businesses navigating both traditional trade and digital sales channels.

- Best For: UAE-based SMEs and e-commerce businesses needing early payment against invoices or gateway receivables.

- Key Feature: Specialized Payment Gateway Finance alongside traditional invoice discounting services.

- Limitation: Pricing is not publicly available and requires direct application. Specific product details can be fragmented across its website and third-party profiles.

Website: https://invoicebazaar.com/

4. Lendo

Lendo is a digital invoice financing marketplace licensed by the Central Bank of Saudi Arabia (SAMA) as a debt crowdfunding platform. It offers a regulated and transparent environment for SMEs to get their invoices paid early by a pool of marketplace investors. The platform is purpose-built for the Saudi market, providing a crucial liquidity solution for businesses operating within or across the GCC with a nexus to the Kingdom. SMEs can submit invoices online, which then undergo a credit review before being listed on the marketplace.

This investor-driven model for invoice discounting means funding speed is subject to investor demand and the platform’s credit assessment process. However, it provides a compliant and structured alternative to traditional bank facilities, aligning with KSA's regulatory framework. For businesses seeking a trustworthy and Shari'ah-compliant method to manage receivables, Lendo presents a unique, localised option. Its transparent workflows for both borrowers and investors have helped establish its role in regional SME trade. To understand the wider financial landscape, you can explore the benefits of trade finance in the UAE.

- Best For: KSA-based SMEs or those with a strong Saudi operational presence seeking a regulated, marketplace-based funding solution.

- Key Feature: A SAMA-licensed debt crowdfunding marketplace connecting SMEs directly with investors.

- Limitation: Primarily KSA-focused, and funding speed is dependent on investor appetite and platform credit checks.

Website: https://www.lendo.sa/en

5. HSBC UAE — Receivables Finance

For established businesses seeking a traditional, bank-backed receivables finance solution, HSBC UAE offers a robust framework. As a global bank, it provides a structured approach suitable for companies with significant trade volumes. Its service allows qualified clients to receive an advance of up to 90% of their invoice value, often with next-day availability, providing a powerful way to manage liquidity across different currencies. The process is supported by digital application tools designed to streamline submissions for existing clients.

This invoice discounting facility is ideal for larger SMEs and corporations that need multi-currency capabilities and the security of a global financial institution. A key advantage is the availability of non-recourse structures, where the bank assumes the risk of non-payment, offering businesses greater protection against bad debt. While the corporate KYC process can be more detailed than fintech alternatives, the benefit lies in a stable, long-term relationship-based facility designed for complex trade finance needs.

- Best For: Larger, established businesses needing structured, multi-currency receivables finance from a global bank.

- Key Feature: Non-recourse options for risk protection and advances of up to 90% of invoice value.

- Limitation: Onboarding can be more involved, often requiring a relationship-banking setup and extensive documentation.

Website: https://www.business.hsbc.ae/en-gb/products/receivables-finance

6. Emirates NBD - smartSCF

Emirates NBD, a leading UAE bank, offers a robust digital Supply Chain Finance platform called smartSCF. This buyer-led solution is designed for established supply chains where a large buyer initiates a programme to offer its suppliers early payment on approved invoices. The platform provides a streamlined, web-based dashboard where suppliers can view outstanding invoices and elect to receive funds early, often at preferential rates linked to the buyer’s strong credit profile. It supports a fully contactless supplier onboarding process, simplifying participation.

This model is ideal for suppliers who work with large corporations already banking with Emirates NBD. By participating in a buyer-led invoice discounting programme, SMEs can gain predictable cash flow and strengthen their relationship with key customers. The platform’s integration capabilities with Enterprise Resource Planning (ERP) systems also reduce manual work for both buyers and suppliers, making the entire process efficient and transparent from invoice approval to settlement.

- Best For: Suppliers dealing with large corporate buyers who have an established smartSCF programme.

- Key Feature: Buyer-led programmes offering preferential rates and contactless digital onboarding for suppliers.

- Limitation: Access is generally dependent on a buyer initiating a programme or a business having a specific bank facility.

7. Mashreq

As one of the UAE's leading financial institutions, Mashreq offers established trade and structured finance solutions for corporate clients. Its services include conventional invoice discounting and factoring, providing businesses with a reliable, bank-backed method to monetise their receivables and manage cash flow. The bank’s deep regional expertise makes it a strong partner for companies engaged in significant local and international trade, offering structured, buyer-approved programmes tailored to complex supply chains.

What sets Mashreq apart is its dual offering through Mashreq Al Islami, which provides Sharia-compliant alternatives to traditional invoice discounting. This appeals to businesses seeking financing structures that align with Islamic principles. While the setup and documentation process can be more involved than with fintech platforms, the stability and comprehensive trade finance leadership of a major bank is a significant advantage for larger, well-established enterprises looking for robust, long-term financial partnerships.

- Best For: Established UAE-based businesses needing bank-backed receivables solutions with conventional or Islamic options.

- Key Feature: Offers both conventional and Sharia-compliant trade finance structures.

- Limitation: Facility setup can be document-heavy, and pricing is customised based on credit profile, not publicly listed.

8. ADCB — Trade Finance (Invoice Financing)

Abu Dhabi Commercial Bank (ADCB) offers established UAE businesses a traditional banking route to manage cash flow. Through its trade finance services, ADCB provides invoice financing for both sales and purchases, alongside receivable purchase and export bill discounting. This allows companies to convert their credit sales into immediate cash, which is crucial for managing operational expenses and funding growth. The bank’s approach combines digital tools with personalised trade advisory services to structure suitable solutions for its clients.

This makes ADCB a strong option for larger enterprises engaged in international trade that require comprehensive support beyond simple invoice discounting. Their end-to-end services are designed to address complex transaction needs, from local sales to cross-border exports. The bank’s established reputation provides a sense of security, although the application process may involve more traditional steps like direct advisor interaction and providing collateral, differing from purely digital fintech platforms.

- Best For: Larger UAE-based enterprises and exporters needing comprehensive trade services from a major bank.

- Key Feature: A wide range of instruments including receivable purchase and export bill discounting.

- Limitation: The application process may be less streamlined than fintech alternatives, often requiring branch visits and collateral.

Website: https://www.adcb.com/en/business/products-solutions/trade-finance-services/grow-your-business

9. National Bank of Fujairah (NBF) — Receivables Financing

The National Bank of Fujairah (NBF) offers a traditional banking approach to receivables financing, tailored for established UAE suppliers and contractors. Its suite of services provides structured solutions that go beyond simple discounting, accommodating both local and overseas invoices. This makes NBF a strong choice for businesses with complex trade cycles that require more than just a digital platform, benefiting from the stability and comprehensive support of a well-regarded financial institution.

NBF’s model is particularly useful for project-driven sectors, offering Post-Dated Cheque (PPC) and bill discounting alongside standard invoice discounting. A key differentiator is the option to include trade credit insurance, which helps mitigate buyer non-payment risk and strengthens the overall financing arrangement. While most structures are with recourse, this flexibility allows businesses to build a solution that aligns with their specific risk appetite and operational needs, providing a robust way to manage cash flow.

- Best For: Established UAE-based suppliers and contractors needing structured, bank-led receivables solutions.

- Key Feature: Optional trade credit insurance to mitigate buyer risk and support for overseas receivables.

- Limitation: Recourse structures are common, and transparent pricing is not available without a direct enquiry.

Website: https://eidavg.nbf.ae/en/business/transaction-banking/receivables-financing

10. Standard Chartered UAE - Receivables Financing / SCF

Standard Chartered offers sophisticated receivables financing and buyer-led supply chain finance programmes for established businesses in the UAE. This global bank provides structured solutions that go beyond simple invoice payments, making it suitable for mid-to-large corporates with complex needs. Their services are designed for companies seeking integrated facilities, including options that incorporate export credit insurance or are linked to sustainability performance criteria, reflecting a more strategic approach to working capital management.

The bank leverages its extensive transaction banking expertise to create tailored programmes. Unlike fintech platforms, Standard Chartered’s invoice discounting solutions are often part of a broader corporate banking relationship, involving a formal onboarding process. This model works particularly well for large-scale suppliers and buyers who need robust, structured facilities, as demonstrated by their known sustainable receivables deals in the region. This service is less about quick, one-off invoice sales and more about establishing a long-term, comprehensive receivables management programme.

- Best For: Mid-to-large corporates needing complex, structured receivables programmes.

- Key Feature: Ability to integrate sustainability-linked structures and export credit insurance.

- Limitation: Geared towards larger corporations, meaning SMEs may face higher entry thresholds and a more formal setup process.

Website: https://www.sc.com/ae/

Making the Right Choice for Your Business's Cash Flow

Navigating the landscape of invoice discounting solutions in the MENA region reveals a clear divide between agile fintech innovators and established banking institutions. The key takeaway is that there is no one-size-fits-all answer; the right choice depends entirely on your business's unique operational needs, scale, and strategic goals. The tools and providers we’ve explored offer a spectrum of options, from rapid, tech-driven platforms to more traditional, structured trade facilities.

Your decision-making process should be a strategic evaluation. Start by clearly defining your primary objective: is it immediate cash flow to cover operational costs, or is it a long-term strategy to unlock working capital for ambitious growth projects? For SMEs prioritizing speed and a seamless digital experience, modern platforms like Comfi offer a distinct advantage with their quick onboarding and fast access to funds. In contrast, larger enterprises with existing banking relationships might find value in the comprehensive trade suites offered by institutions like HSBC or Emirates NBD.

Before committing, it's crucial to weigh the most important factors:

- Speed vs. Structure: Do you need funds within 24-48 hours, or can you accommodate a longer, more formal application process?

- Integration: How important is it for the solution to integrate with your existing accounting or ERP software?

- Confidentiality: Is maintaining a confidential relationship with your customers a priority?

- Cost and Transparency: Understand the full fee structure, including any setup, service, or early repayment charges.

Ultimately, choosing the right invoice discounting partner is about more than just securing funds. It's about finding a partner that aligns with your business model and empowers you to build a more resilient financial foundation. By taking a measured approach, you can confidently select a solution that transforms your unpaid invoices from a liability into a powerful asset for growth.

Ready to take control of your cash flow with a fast, flexible, and fully digital solution? Explore how Comfi helps businesses in the MENA region get invoices paid in as little as 24 hours. Visit Comfi to learn more and see if it's the right fit for your business.

Related Reading

- A Practical Guide to Invoice Discounting in the UAE

- 8 Best Accounts Receivable Software for SMEs in 2026

- Inventory Financing vs Invoice Discounting for UAE SMEs

- What Is Accounts Receivable: Your 2026 Guide for UAE SMEs

Looking to improve your cash flow? Explore Comfi's Invoice Discounting solutions. Get started today.