5 Types of Business Fraud Every SME Should Know

For any Small and Medium-sized Enterprise (SME) in the UAE and MENA region, growth is the primary objective. Yet, as your business expands, so do the risks. One of the most significant threats is business fraud, a danger that can cripple cash flow and jeopardise your company's survival. From falsified invoices to intricate digital scams, the methods used by criminals are constantly evolving. Understanding and addressing the possibility of fraud begins with a comprehensive fraud risk assessment.

This educational guide explores five critical types of business fraud that can directly impact an SME's operations. We will offer practical insights and preventative measures to help you safeguard your hard-earned success. Protecting your business requires more than just awareness; it demands specific, actionable knowledge. By learning to recognise the signs of fraud and implementing robust controls, you can build a more resilient and secure enterprise.

1. Supplier Identity Fraud and Impersonation

Supplier identity fraud is a sophisticated scheme where criminals impersonate legitimate businesses to exploit your payment systems. They might create fake company profiles mimicking established suppliers, use stolen UAE Trade License details, or take over existing accounts to redirect payments to themselves. This type of fraud is especially dangerous as it attacks the core trust between business partners. A common tactic involves email spoofing, such as using a domain like acme-corp.ae instead of the real acmecorp.ae to trick your accounts payable team.

This fraud erodes trust and can lead to significant financial losses. One of the most common methods used is social engineering. Understanding What Happens If You Open a Phishing Email? is a critical first step in staff training and prevention.

Practical Prevention Tips

- Verify Bank Details: Always verify any changes to supplier bank details through a secondary channel, like a phone call to a known contact.

- Due Diligence: Conduct thorough "Know Your Supplier" checks before entering into a new business relationship.

- Staff Training: Educate your finance and procurement teams to spot red flags, such as urgent payment requests or slight variations in email addresses.

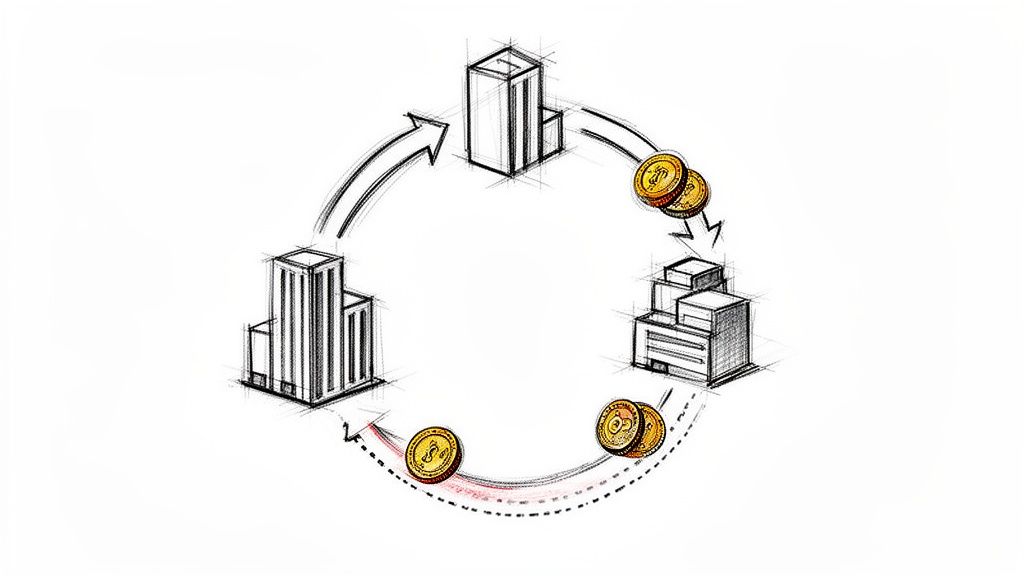

2. Collusion and Round-Tripping Fraud

Collusion is a sophisticated form of fraud where two or more parties conspire to create fake or inflated transactions. In a typical scenario, a buyer and supplier will work together to artificially inflate invoice values. The funds move from your business (or a payment facilitator) to the "supplier" and are then secretly cycled back to the "buyer" as a kickback. This creates a false impression of legitimate commercial activity while siphoning funds.

For an SME, being unknowingly involved or being the target of such a scheme can lead to severe reputational damage and financial penalties. For example, a manager at your company might collude with a parts supplier to inflate invoices by 30%, with your manager receiving a 15% kickback after your company pays.

Practical Prevention Tips

- Segregation of Duties: Ensure no single person controls the entire procurement and payment process.

- Price Benchmarking: Regularly compare invoice prices against market rates to spot significant inflation.

- Audits: Conduct periodic, unannounced audits of transactions and supplier relationships to identify unusual patterns.

3. Delivery and Goods Non-Receipt Fraud

This type of fraud occurs when a supplier invoices you for goods that were never delivered, or when a buyer falsely claims they never received a shipment to avoid payment. For an SME supplier, the latter is more common and damaging. A fraudulent buyer receives your goods but then disputes the transaction, claiming non-receipt. This breaks the link between a financial document (the invoice) and the actual business activity (the delivered goods), creating a phantom receivable.

For SMEs, this fraud can be particularly damaging. It not only leads to lost revenue and goods but also ties up resources in disputes and investigations.

Practical Prevention Tips

- Mandatory Proof of Delivery (POD): Always require a signed delivery note, photographic evidence, or digital confirmation from the buyer before recognising the sale as complete.

- Track Shipments: Use tracked shipping services that provide real-time updates and delivery confirmation.

- Clear Terms: Ensure your sales contracts explicitly state the buyer's responsibility upon receipt of goods and the required process for documenting delivery. To secure your transactions further, explore strategies to prevent B2B payment fraud.

4. Payment Delinquency Fraud

Payment delinquency is one of the most common and damaging forms of fraud an SME can face. It occurs when a buyer accepts goods or services with no intention of ever paying, deliberately exploiting the credit terms you offer. This is not merely a late payment; it's a calculated act of evasion. The buyer might be a fraudulent shell company set up to acquire goods and then disappear, or an existing business that intentionally orders a large shipment before ceasing operations.

Implications for an SME:

- Total Revenue Loss: The income from the fraudulent transaction is completely lost.

- Cash Flow Crisis: This directly depletes your working capital, hindering your ability to pay your own suppliers, cover payroll, and fund operations.

- Threat to Survival: A significant instance of payment delinquency fraud can be enough to threaten the very survival of an SME.

How Comfi's BNPL Can Help

Comfi’s Buy Now, Pay Later (BNPL) for B2B sales helps mitigate this risk. When a transaction is processed through Comfi, you, the supplier, can receive payment upfront, often within 24 hours of invoice approval. Comfi then manages the collection from your buyer (who will be assessed by Comfi's underwriting process) according to the agreed-upon 30, 60, or 90-day terms. This solution ensures you have immediate access to your funds, effectively removing the risk of non-payment and delinquency fraud from your balance sheet. You can confidently offer flexible payment terms to attract more customers, knowing your cash flow is secure and your business is protected from this critical survival threat. To understand more about these financial exposures, you can learn more about payment risk.

5. Synthetic Identity and Account Takeover Fraud

This is a modern, high-tech form of fraud involving the creation of fake identities or the compromising of legitimate customer accounts. Criminals either build a "synthetic" identity by combining real stolen data (like a UAE national ID) with fabricated information, or they use phishing and credential theft to take over an existing buyer's account. Once inside, they can place large orders using the legitimate account's good standing, with no intention of paying.

For a B2B platform or supplier, a compromised buyer account could lead to unauthorised orders and massive losses when the real account holder disputes the fraudulent transaction.

Practical Prevention Tips

- Monitor for Red Flags: Be alert to unusual changes in ordering behaviour, such as a sudden large order from a typically small buyer, or a change in the shipping address to a new, unverified location.

- Multi-Factor Authentication (MFA): If you run an online portal for buyers, implement MFA to secure customer accounts from takeovers.

- Confirm Large Orders: For unusually large or high-risk orders, contact the buyer through a pre-verified phone number to confirm the order's legitimacy before shipping.

Building a Fraud-Resistant Future for Your SME

The landscape of business-to-business transactions is filled with opportunities, but as we have explored, it also contains significant risks of fraud. From payment delinquency to sophisticated identity scams, these threats endanger the stability and growth of any small or medium-sized enterprise. A proactive and layered defence is the only reliable approach to protect your business.

The key takeaway is that security is a continuous process, not a one-time fix. It starts with creating a culture of vigilance and implementing robust internal controls.

Remember these key areas of focus:

- Awareness: Recognise the warning signs of different fraud schemes.

- Prevention: Implement practical controls like requiring proof of delivery and conducting due diligence on new partners.

- Response: Have a clear plan to follow when a fraud incident is suspected to contain the damage quickly.

Ultimately, protecting your business from fraud is about securing your cash flow and ensuring your hard-earned revenue translates into real growth. By combining strong internal policies with modern technological safeguards, you are not just preventing loss; you are building a more resilient, trustworthy, and profitable organisation.

Ready to build a more secure payment process and reduce your exposure to buyer payment fraud? Discover how Comfi provides a secure B2B checkout experience, helping ensure you get paid on time. Visit Comfi to see how our platform can help protect your revenue and allow you to unlock your working capital.