Private Finance in Dubai: Capital Beyond Banks

A lot of Dubai businesses do not have a sales problem. They have a timing problem.

A wholesaler wins a purchase order but needs stock before the buyer pays. A dealer finds the right vehicles at the right margin but cannot move fast because cash is locked in existing inventory. A distributor is profitable on paper but still feels squeezed because receivables, payables, payroll, and supplier terms do not line up.

That is why private finance in Dubai has become more practical for SMEs. Not the wealth-management version. The useful side is operational: invoice-based funding, dealer inventory solutions, and B2B payment tools that match how SMEs trade.

If you run an SME in Dubai, the real question is not whether capital exists. It is whether you can access it fast enough, on terms that fit your sales cycle, without going through a bank process built for a different borrower.

Why Dubai SMEs Are Looking Beyond Banks

This becomes obvious when a business starts growing.

A food distributor gets a larger retail order. An electronics trader has a chance to buy more from a supplier. A car dealer spots inventory that should move well, but current stock is still sitting in the showroom. The opportunity is real. The margin is there. The friction is cash timing.

Traditional banks often struggle with this need. Their process can be slow, document-heavy, and geared toward fixed collateral rather than live trading activity. That does not make banks irrelevant. It just means they are often not designed for situations where speed decides the outcome.

The financing gap is operational, not theoretical

Many SME owners think the problem is unique. It is not. In the UAE, an estimated 32% of the population remains underbanked or unbanked, with SME suppliers significantly excluded from formal private finance channels, and much of the visible private finance conversation still focused on high-net-worth clients rather than day-to-day SME cash flow needs, according to Lune's analysis of financial inclusion in the UAE.

That is why so many businesses feel underserved by mainstream finance content. They are not looking for prestige lending. They need a way to bridge inventory cycles, invoice delays, and supplier payments.

Practical rule: If your business is profitable but regularly short of cash at the wrong moment, the issue is usually structure, not demand.

Why banks feel misaligned for trading businesses

For SMEs in wholesale, distribution, and automotive, cash moves in cycles. Buyers ask for terms. Suppliers want payment earlier. Inventory must be purchased before it can be sold. A fixed bank product often does not flex around that reality.

What often works better is finance tied to the transaction or asset flow.

- Invoice-led businesses need access to receivables before the customer pays.

- Inventory-heavy businesses need a way to release capital from stock on hand.

- Suppliers selling to business buyers need tools that let customers buy now without hurting the supplier’s cash flow.

Instead of asking, “Can I get a bank facility?”, ask, “Which part of my cash cycle is causing the bottleneck?”

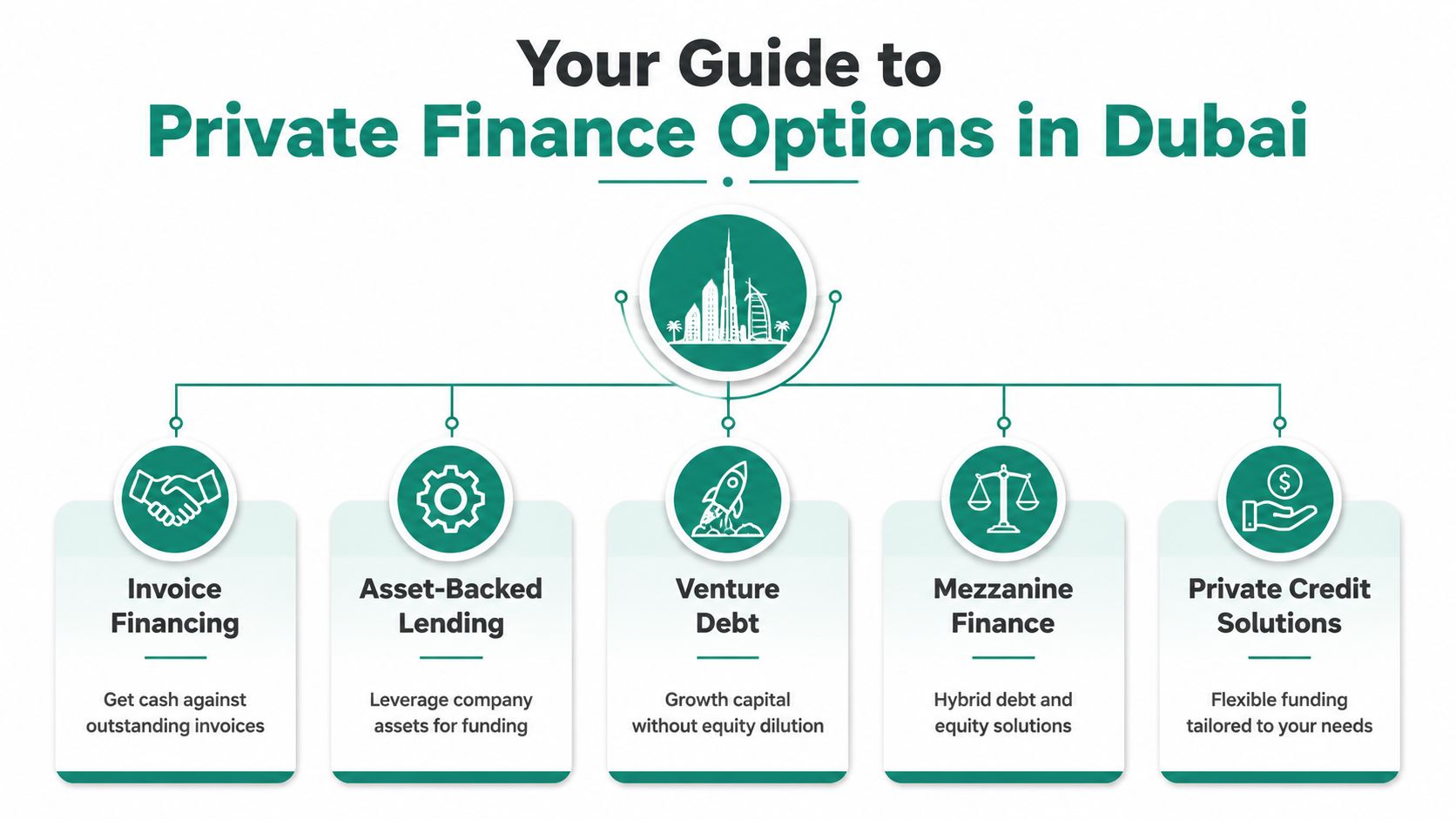

Your Guide to Private Finance Options in Dubai

When people hear private finance in Dubai, they often think of private equity, family offices, or bespoke lending. Those exist, but they are not the first tools most SMEs should look at.

The most useful options are simpler and tied to real trading activity.

The options that matter most for SMEs

- Invoice financing

If you have issued valid invoices but your buyer pays later, this lets you access cash against those receivables sooner. It suits businesses that sell on terms and do not want growth slowed by long payment cycles. If you want a plain-English breakdown of the mechanics, this comprehensive guide on invoice factoring is a useful starting point. For a more specific look at receivable-led structures, accounts receivable financing explained gives a practical overview. - B2B buy now, pay later

This works well when customers want payment flexibility but you do not want your own cash flow stretched. It is often relevant for distributors, wholesalers, and B2B sellers trying to close larger orders without taking on collection friction internally.

Who is this for? Businesses that lose sales because buyers ask for terms they cannot comfortably offer from their own balance sheet. - Dealer inventory solutions

In automotive, cash often gets locked inside vehicles waiting to sell. This is one of the clearest use cases for non-bank finance. In the UAE automotive finance sector, the market is projected to reach USD 47.32 billion by 2034, and the growth is linked to dealer liquidity solutions that release inventory capital within 24 hours. The same market projection notes that dealers using such mechanisms report 30% sales uplift and 20% new-customer growth. See the UAE auto finance market outlook.

Who is this for? Dealers whose stock position is healthy, but whose liquidity limits restocking.

Options that fit fewer SMEs

Some private finance products are real, but they are not usually the first move for a typical Dubai SME.

- Private equity can help if you are scaling aggressively and willing to give up ownership.

- Venture debt may fit funded startups with a defined growth plan.

- Mezzanine finance is usually more relevant for larger, more complex transactions.

- Asset-backed lending can help where machinery, equipment, or other business assets are central to the balance sheet.

Most SMEs do not need the most sophisticated structure. They need the one that matches how money moves through the business.

A simple way to choose the right category

Ask where the cash is stuck.

- In receivables? Look at invoice financing.

- In customer conversion? Look at B2B BNPL.

- In showroom or warehouse stock? Look at inventory-led or dealer-focused solutions.

- In a long-term expansion plan? Explore broader capital structures.

Private finance in Dubai is most useful when it is tied to invoices, inventory, and payment timing.

Private Finance vs Bank Loans A Clear Comparison

A bank loan can still be the right choice. If your need is long-term, your financials are clean, your collateral is straightforward, and time is not critical, a bank facility may be sensible.

But many SME owners compare products on headline price and ignore the cost of delay.

Speed changes the economics

If a bank takes weeks to process a request and your supplier opportunity expires in days, the cheaper nominal rate does not help. Missed gross profit, lost buyer relationships, and delayed restocking are all real costs.

Private finance options, especially fintech-led ones, are typically built around speed and transaction flow. If your business needs fast movement, faster alternatives to a traditional business loan are worth reviewing before you default to a conventional application.

Waiting can be more expensive than paying for flexibility.

Collateral and eligibility are different

Banks often want hard collateral, broad financial history, and extensive documentation. That can exclude healthy businesses that trade well but do not fit a conventional profile.

Private finance tends to focus more on:

- The quality of your invoices

- The turnover of your stock

- The behaviour of your buyers

- The consistency of your trading activity

A business can be viable and still fail a bank’s internal model. Asset-led or receivable-led structures are often a better match for how SMEs operate.

Terms should match the cash cycle

A mismatch between facility structure and business cycle creates stress. If repayments start too early, or the facility does not move with sales volume, the product can create more pressure than it solves.

Bank loans are often better for stable, predictable needs such as equipment purchase, fit-out, or longer-term investment. Private finance is often better for variable, recurring pressure points such as:

- Outstanding receivables

- Inventory restocking

- Seasonal order spikes

- Buyer payment extensions

Cost needs a broader definition

Do not assess cost by one number alone. Look at the full commercial effect.

Ask:

- Does this help me fulfil more orders?

- Does it reduce the time cash is trapped?

- Does it protect supplier relationships?

- Does it let me say yes to better-margin deals?

If the answer is yes, the right comparison is not bank rate versus provider fee. It is static capital versus usable capital.

Navigating Dubai's Financial Regulations

Some SME owners hesitate because anything outside a bank can feel less formal or less secure. In Dubai, that view is often outdated.

Private finance in Dubai sits inside a financial environment that is more stable than many people assume.

Why macro stability matters to SMEs

Dubai's wider fiscal and economic position supports private capital activity. According to S&P Global Ratings' analysis of Dubai's macroeconomic prospects, the Emirates' gross general government debt is forecast to decline to approximately 34% of GDP by the end of 2024, down from 70% of GDP in 2021. That stronger fiscal position supports lender and investor confidence.

For an SME owner, the practical takeaway is simple: you are not exploring alternatives in a disorderly market. You are operating inside a maturing financial ecosystem with stronger institutional footing.

What to check before you sign

Regulation helps, but your own review still matters.

- Read the trigger events: Know exactly what starts repayment or settlement.

- Check assignment and collection terms: This matters especially in invoice-based structures.

- Review early settlement treatment: Flexibility is useful only if the contract preserves it.

- Confirm dispute handling: If a buyer disputes an invoice, know what happens next.

A well-regulated environment helps. It does not replace due diligence.

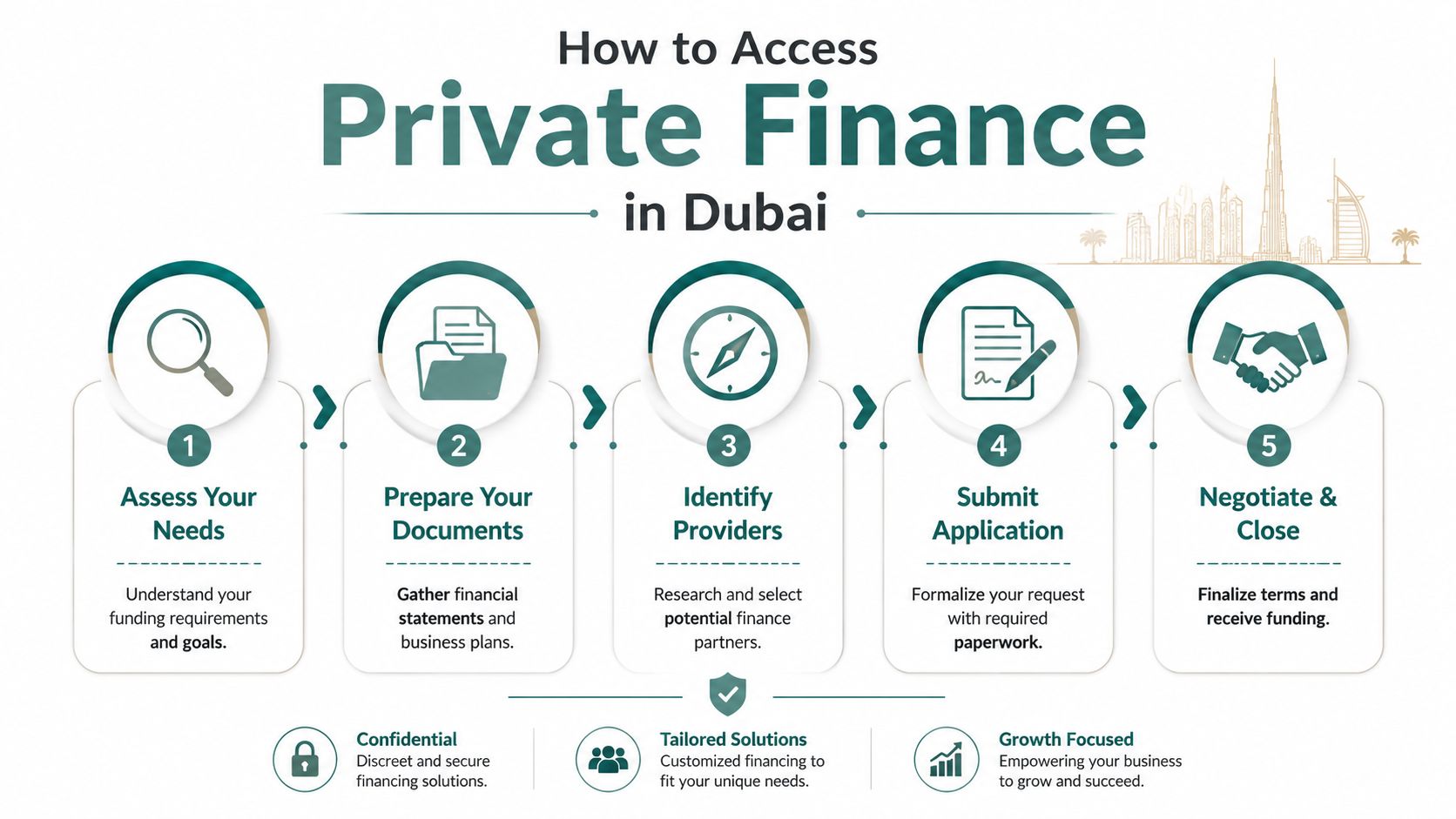

How to Access Private Finance in Dubai

Most SME owners overcomplicate this part. The route is usually shorter than a bank process, but only if you prepare for the right review.

In the UAE, SMEs account for over 95% of businesses but receive less than 20% of total bank credit, which is why asset-based alternatives have become more relevant for privately held firms, as explained in Ocorians's analysis of underserved private credit demand.

Step one means defining the bottleneck properly

Do not start by asking how much money you want. Start by identifying what the capital needs to do.

Are you bridging invoices? Restocking inventory? Offering payment terms to buyers without hurting your own cash position? Covering a one-off order spike? Each problem points to a different structure.

A vague request slows everything down. A precise use case speeds decisions.

Prepare documents that reflect live trading

Private finance providers usually care less about pitch decks and more about trading evidence.

Bring together the basics:

- Trade licence and company details

- Recent bank statements

- Invoices or receivables data

- Buyer or supplier information

- Inventory information where relevant

- Management accounts if available

The quality of your records affects both speed and credibility. If invoices are messy, customer names are inconsistent, or stock records do not reconcile, you create friction no provider can solve for you.

Choose a structure before you choose a provider

Many SMEs waste time comparing brands before deciding which category of finance fits the problem.

Use this simple lens:

- Receivables issue

You have sold already, but payment is delayed. Invoice-led structures are the natural fit. - Conversion issue

Buyers want terms you cannot comfortably extend yourself. B2B payment tools are often more suitable. - Inventory issue

Capital is tied up in stock and slowing your next purchase cycle. Inventory-led solutions make more sense.

The best application starts with a clear operational problem, not a generic request for funds.

Review workflow fit, not just approval likelihood

A product can look good and still create friction inside your business.

Check these points:

- Dashboard usability: Can your team upload and track transactions without constant back-and-forth?

- Documentation burden: Is the process digital and repeatable, or does every transaction restart from zero?

- Collections and settlement flow: Who handles follow-up, and how visible is the status?

- Integration potential: If you run on an ERP, marketplace, or sales platform, can the process fit into your workflow?

The right finance tool should reduce admin, not add another layer of it.

Expect a faster cycle, but do not confuse fast with careless

Good providers move quickly because they focus on relevant data. That does not mean the process is casual. You still need to answer questions clearly, verify documents, and show that the underlying trade is genuine.

What helps most is responsiveness. If a provider asks for invoice backup, buyer details, or stock information, send it in complete form the first time. Many delays happen when the business submits partial information.

Choosing the Right Private Finance Partner

The provider matters as much as the product. Two firms can offer something that sounds similar, but the working experience can be very different.

A good partner understands your industry, gives clear visibility into the process, and does not force your finance team to manage everything manually.

Start with sector fit

A provider that understands automotive inventory will ask better questions than one that treats a dealership like a generic SME. The same applies to electronics distribution, FMCG, or B2B wholesale.

In automotive, for example, timing and stock movement are central. Vehicle inventory in the UAE can remain unsold for up to 180 days, tying up working capital and restricting restocking, according to this review of inventory and cash management pressures for auto dealers. A provider that does not understand that cycle is less likely to structure the relationship well.

Use a due diligence checklist

Do not evaluate a finance partner on speed alone.

- Transparency first: You should understand the fee logic, operational steps, and what happens if a buyer delays or disputes.

- Operational maturity: Look for digital dashboards, clear status tracking, and repeatable transaction handling.

- Workflow compatibility: API access or low-code integration can matter if you process volume and do not want your team rekeying data.

- Industry relevance: Ask what kinds of businesses and transaction patterns they handle well.

- Eligibility clarity: Serious providers define who they serve instead of promising everything to everyone.

One practical benchmark is whether the provider is explicit about qualification criteria. For example, Comfi states that its UAE auto dealer offering is for dealerships that have operated for at least 6 months, have a physical showroom, and generate average monthly revenue of AED 400,000. That kind of specificity helps businesses self-screen early through Comfi's dealer financing eligibility page.

Technology is not a nice-to-have

For SMEs, the hidden cost in finance is often admin. If your team has to chase updates by email, send duplicate files, and manually reconcile every transaction, the product will feel expensive even if the commercial terms are acceptable.

That is why a usable platform, strong document flow, and clear process ownership matter. If you want a practical lens on how to evaluate whether a provider is acting more like a finance operator than a traditional lender, this explanation of what a finance partner versus lender looks like is a useful read.

Choose the partner your operations team can live with, not just the one your finance team can approve.

Taking Control of Your Business Growth

For many SMEs, private finance in Dubai stops being abstract once you tie it to one recurring problem: cash arrives later than the business needs it.

That is why the most useful solutions are not the most glamorous. They are the ones that release cash from invoices, stock, or customer payment terms without forcing the business into a slow, rigid borrowing process. Used well, these tools do not replace discipline. They support it by matching capital to the pace of trade.

The businesses that benefit most usually take a practical approach. They identify the exact bottleneck, choose the right structure, and work with a provider that understands the workflow behind the transaction.

If you are running a wholesaling business, managing receivables, or trying to keep inventory moving faster, the goal is not simply to “get funding”. It is to build a cash cycle that lets you act on opportunities while they still matter.

If your business needs a faster way to access cash from invoices, extend flexible payment terms, or free up capital tied in dealer inventory, Comfi is worth a closer look. Its digital tools are built for SMEs that want less paperwork, quicker decisions, and a finance workflow that fits real trading activity in the UAE.