A Guide to Mastering Your Business' Working Capital

Think of working capital as the financial pulse of your business. It's the cash and other liquid assets you have on hand to cover your day-to-day costs—from paying suppliers and covering payroll to simply keeping the lights on. In short, it’s the fuel that keeps your business running smoothly.

The Financial Fuel for Your Daily Operations

But working capital is much more than just a number on a balance sheet. It’s a real-time indicator of your company's short-term financial health and operational efficiency.

Imagine you run a retail shop. You need to buy inventory and fill your shelves long before a customer walks in and makes a purchase. The money you use for that stock is your working capital in action.

This creates a natural gap between when you spend money and when you make it back. Managing working capital well is all about balancing this cycle so you always have enough cash to operate without hitting a wall. A healthy level of working capital isn't just about stability; it's a powerful strategic advantage.

Why Healthy Working Capital Is a Competitive Edge

For small and medium-sized enterprises (SMEs), especially in a dynamic economy like the UAE, strong liquidity isn't just about survival—it's about having the power to grow.

When you manage your working capital effectively, you can:

- Seize Opportunities: Got a chance to get a great discount from a supplier by buying in bulk? Or launch a timely marketing campaign? With cash on hand, you can say yes.

- Provide a Financial Buffer: Unexpected costs, like a crucial piece of equipment breaking down or a sudden spike in material prices, won't derail your operations.

- Build Stronger Supplier Relationships: Paying your vendors on time, every time, builds trust. That trust often leads to better payment terms and more reliable partnerships down the road.

- Fuel Growth Confidently: You can take on bigger contracts or expand into new markets knowing you have the financial stability to handle the increased operational load.

A business with positive working capital has enough short-term assets to cover its short-term liabilities. This simple metric is a primary indicator of a company’s ability to remain solvent and operational.

This is even more critical in the MENA region's economic climate. The UAE's non-oil sector, for instance, saw incredible growth, outpacing other regional economies. For SME suppliers and wholesalers, this boom is a huge opportunity, but it also puts immense pressure on cash flow as they scramble to scale up and meet demand.

Ultimately, getting a firm grip on this concept is the first step toward financial mastery. To start, you can learn the specifics of the working capital formula in our detailed guide. Mastering this calculation will give you the clarity you need to make smarter, more proactive financial decisions for your business.

Understanding Your Working Capital Cycle

Having positive working capital is a great start, but the real story is in how that capital moves. This flow—the time it takes for cash to leave your business as an expense and return as revenue—is called the working capital cycle. You might also hear it called the cash conversion cycle.

Think of it as your business's financial pulse. A fast, steady pulse (a short cycle) means your money is healthy and working hard, quickly cycling from investment back into cash. A slow, sluggish pulse (a long cycle) is a warning sign. It means cash is getting stuck somewhere, which can lead to serious liquidity problems, even if your business is profitable on paper.

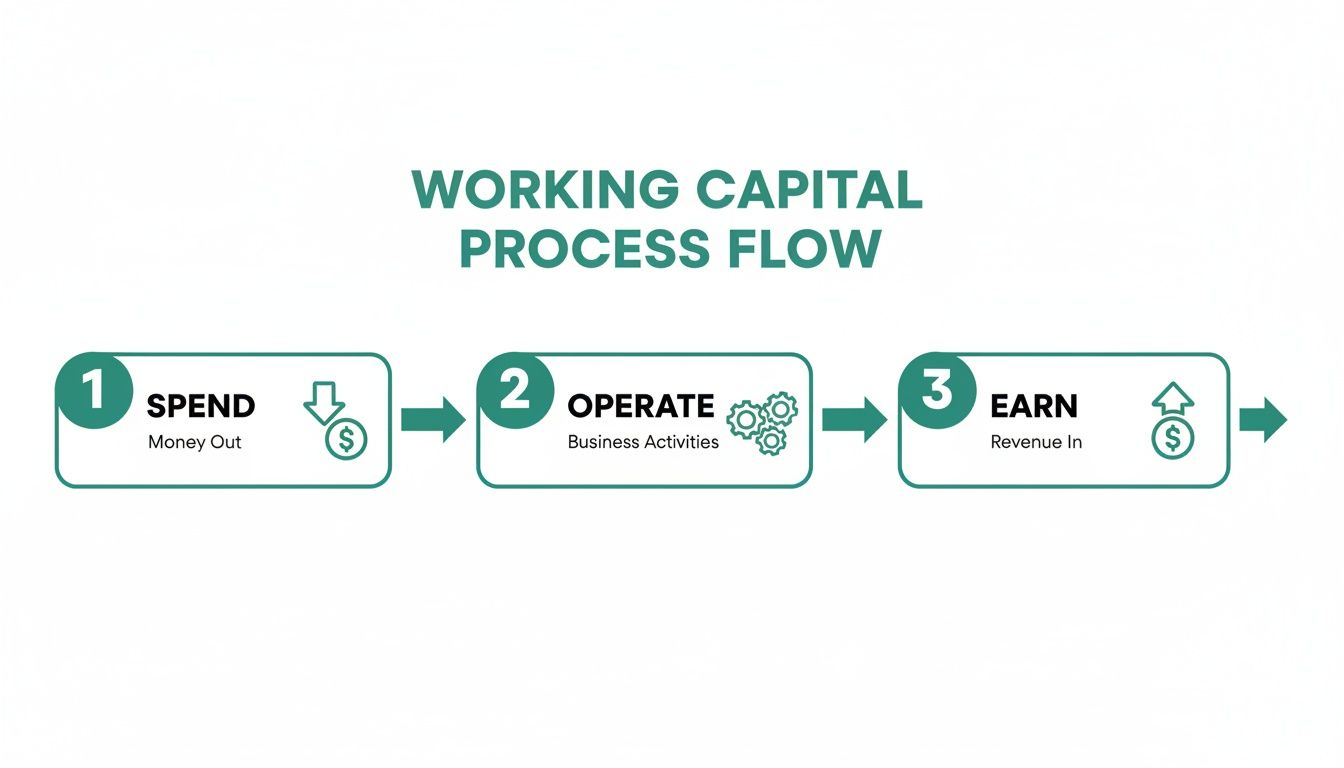

This whole process boils down to a simple, three-step loop: you spend money to run the business, you operate, and then you earn that money back.

As the visual shows, mastering working capital is all about shrinking the time between the 'Spend' and 'Earn' stages. The shorter the gap, the more cash you have on hand.

The Three Levers of Your Cash Flow

You don't need a finance degree to get a grip on this. Your working capital cycle is controlled by three main levers. Pull one, and you can speed things up; pull another, and you might slow things down. Understanding how they work is the key to managing your cash.

- Days Inventory Outstanding (DIO): This is simply how long your products sit on the shelf before they’re sold. A high DIO means your cash is physically tied up in unsold stock, which also costs you money in storage and runs the risk of becoming obsolete.

- Days Sales Outstanding (DSO): This tells you how fast your customers pay you. A high DSO is a red flag. It means you’re effectively extending credit to your clients, waiting weeks or even months to get the cash for goods you’ve already delivered.

- Days Payables Outstanding (DPO): On the flip side, this is how long you take to pay your own suppliers. A higher DPO can be good for your cash flow—you hold onto your money longer. But you have to balance this carefully to keep your suppliers happy and maintain strong relationships.

If you want to get into the nitty-gritty, our complete guide to the cash conversion cycle breaks down all the formulas. But just knowing these three levers is the first step to diagnosing the health of your cash flow.

A Real-World UAE Example

Let's make this tangible. Imagine an automotive parts distributor based in Dubai. Their success depends on having the right parts in stock when local garages need them.

They order a big shipment of brake pads from a manufacturer. The time those brake pads sit in the warehouse before being sold is their Days Inventory Outstanding (DIO). Let's say that’s 90 days—three full months where their cash is locked up in that inventory.

A local garage buys the brake pads on credit. The clock now starts on the Days Sales Outstanding (DSO), which is the time it takes the garage to pay the invoice. If the terms are 60 days, the distributor has to wait another two months for that money to come in.

Finally, the distributor has its own payment terms with the manufacturer. The time they take to pay that bill is their Days Payables Outstanding (DPO). If they have 30-day terms, their cash goes out the door after one month.

The total length of the working capital cycle here is calculated as: DIO (90 days) + DSO (60 days) - DPO (30 days) = 120 days. This means it takes a full four months for every dirham spent on inventory to make its way back into the business as usable cash.

That 120-day gap is a huge cash flow challenge. During that time, the distributor still has to pay rent, salaries, and all the other bills. Shortening this cycle is the number one goal of smart working capital management because it directly frees up cash, making the business far more resilient and ready to jump on new opportunities.

Operational Strategies to Optimize Working Capital

Knowing your working capital cycle is one thing, but shrinking it is where you find real financial freedom. Let's move from theory to action. You can pull several levers inside your own business to boost liquidity and free up cash that's currently tied up. These operational tweaks focus on fine-tuning the three core components of your cycle: receivables, inventory, and payables.

The goal here is simple: make the journey your cash takes from leaving your business to returning as short as possible. Even small, gradual improvements in these areas can have a massive impact on your company's overall financial health, giving you more flexibility and resilience.

Accelerate Your Accounts Receivable

The money from your sales isn't really yours until it hits your bank account. Speeding up how fast you get paid is one of the quickest ways to improve your working capital. Every single day you can shave off your Days Sales Outstanding (DSO) is another day you have cash on hand to run and grow your business.

Try these proven methods to bring cash in the door faster:

- Offer Early Payment Discounts: Give your customers a compelling reason to pay you ahead of schedule. A small incentive, like 2% off for paying within 10 days on a 30-day invoice (often written as "2/10, n/30"), can be a powerful nudge that dramatically improves your cash flow.

- Automate Your Invoicing: Manual invoicing is slow and prone to errors, which only leads to payment delays. Using accounting software to automate invoice creation and send out polite, automatic reminders ensures your bills go out on time and stay on your clients' radar.

- Clarify Payment Terms Upfront: Ambiguity is the enemy of quick payments. Make sure your terms are crystal clear on every invoice and contract, leaving absolutely no room for confusion about due dates or how to pay.

Streamline Your Inventory Management

Every single item sitting on a shelf in your warehouse represents cash that isn't working for you. Of course, you need enough stock to keep customers happy, but holding excess inventory ties up a huge amount of capital and brings on extra costs for storage, insurance, and the risk of it becoming obsolete.

Optimizing inventory is a balancing act. The goal isn't to have zero stock, but to hold the absolute minimum needed to fill customer orders without a hitch. This is how you maximise the efficiency of your capital.

To cut down your Days Inventory Outstanding (DIO), you can:

- Adopt Just-in-Time (JIT) Ordering: This approach means you order goods from suppliers only when you actually need them for production or to fulfil a customer order. JIT slashes holding costs and lowers the risk of getting stuck with stock you can't sell.

- Improve Demand Forecasting: Use your historical sales data and current market trends to get better at predicting future demand. Sharper forecasting helps you avoid both overstocking and stockouts, making sure your cash is tied up in inventory that’s going to move quickly.

Strategically Manage Your Accounts Payable

While you want to collect cash from customers as fast as possible, it often makes sense to slow down payments to your own suppliers—within your agreed terms, of course. Extending your Days Payables Outstanding (DPO) means you get to hold onto your cash for longer, which can then be used to fund other parts of your business.

The key is to handle this strategically to keep your relationships with vendors strong and positive. To truly get a grip on your cash flow, understanding the complete invoice payment process is essential for managing your payables like a pro.

A great way to improve your payables is by negotiating better terms with your suppliers. If you have a solid history of paying reliably and on time, use that track record as leverage to ask for longer payment windows, like shifting from 30-day to 60-day terms.

This isn't about not paying your bills, but about intelligently aligning your cash outflows with your inflows. By putting these operational strategies into practice, businesses across the UAE can unlock trapped capital and put it back to work growing their company.

Modern Solutions That Unlock Working Capital

Fine-tuning your operations is a great start, but sometimes it isn't enough to fund rapid growth or plug an unexpected cash flow gap. When your business is ready to scale, waiting on invoices can mean missing out on game-changing opportunities. Thankfully, modern financial tools give MENA SMEs more speed and flexibility than traditional methods, helping you unlock your working capital without taking on long-term debt.

These solutions are designed to inject cash directly into your business by turning existing assets—like unpaid invoices—into money in the bank. This gives you the freedom to say yes to bigger orders, bring on new clients, and navigate unpredictable revenue cycles with a lot more confidence.

Turn Unpaid Invoices into Immediate Cash

One of the most direct ways to boost your liquidity is to tackle the delay between sending an invoice and actually getting paid. Instead of waiting 30, 60, or even 90 days for a customer to settle up, you can convert that receivable into cash almost instantly.

Invoice discounting is a straightforward process where a third party advances you a large percentage of your outstanding invoice's value. You get most of the cash right away, and the rest (minus a small fee) follows once your customer pays the invoice. This approach is a game-changer for businesses with healthy sales but slow-paying clients. You keep control over your customer relationships and collections process while getting immediate access to the funds you've already earned.

To see how this works in practice, you can explore our detailed overview of invoice discounting in the UAE.

Preserve Capital with Flexible B2B Payments

Another major drain on working capital is having to pay for inventory and supplies long before you can sell your final product. This is where modern B2B payment solutions can make a huge difference, letting you get what you need without emptying your cash reserves.

Platforms like Comfi make these transactions incredibly smooth. Suppliers can offer their business buyers flexible payment terms—like Buy Now, Pay Later (BNPL)—while still getting paid upfront themselves. It’s a win-win situation.

Key benefits include:

- For Suppliers: You close deals faster, remove credit risk, and receive immediate payment. This dramatically shortens your own cash conversion cycle.

- For Buyers: You can secure the inventory or services you need to grow without tying up your working capital, paying for the goods over time as you generate revenue from them.

By decoupling the supplier's need for immediate payment from the buyer's need for flexible terms, these platforms act as a powerful catalyst for trade and growth within the B2B ecosystem.

The impact is clear. Businesses using these tools can take on larger orders, manage seasonal demand spikes, and build stronger supplier relationships without the usual cash flow headaches. To get ahead of potential issues, some AI cash flow forecasting tools can even help you predict and prevent crunches before they happen.

The economic landscape in the UAE highlights just how crucial these solutions are becoming. The country's strong GDP growth, driven largely by the non-hydrocarbon sector, puts intense pressure on working capital as SMEs have to scale operations faster than their cash cycles can support. This makes modern payment tools not just helpful, but essential for sustainable growth.

Real Success Stories from UAE Businesses

Theory is great, but seeing how unlocking working capital actually transforms a business is where it really clicks. For many SMEs across the UAE, optimising cash flow isn't just a box-ticking exercise; it’s the move that completely changes their growth story. The following stories show how real, local businesses turned frustrating liquidity problems into a serious competitive edge.

There's a common thread running through these examples: when cash isn't trapped in long payment cycles, a business can finally invest, expand, and serve its customers better. It’s the difference between just getting by and genuinely thriving.

Fueling Growth in the Automotive Sector

Take a Dubai-based automotive parts distributor. They were stuck in a classic working capital trap: huge demand for certain parts, but never enough cash on hand to buy enough inventory in bulk. This bottleneck forced them to turn away sales and miss out on the volume discounts their international suppliers were offering.

Their problem was simple but crippling. They had to pay their suppliers upfront, then wait weeks—sometimes months—for the local garages they supplied to pay them back. That cash flow gap put a hard limit on their ability to stock the right parts at the right time.

By switching to a modern payment solution, they could pay their suppliers instantly, even for massive orders. This one change created a massive ripple effect:

- Deeper Inventory: They could finally load up on high-demand, fast-moving parts, making sure they never lost a sale because an item was out of stock.

- Better Margins: Buying in bigger quantities gave them the leverage to negotiate better prices from suppliers, which went straight to their bottom line.

- Faster Fulfilment: With plenty of stock on the shelves, they could deliver parts to garages immediately, cementing their reputation for being the most reliable supplier around.

The result? A massive 30% jump in sales in just six months. By untangling their working capital, they completely transformed their operations and started grabbing a much bigger share of the market.

Expanding Reach in B2B Electronics

Here’s another powerful example, this time from a B2B electronics supplier in Sharjah. They knew that offering flexible payment terms was the key to attracting a wider range of customers, from small independent retailers to large corporate buyers. The problem was, their own cash flow couldn't handle the risk and delay of extending 60 or 90-day credit to every client.

This put them at a major disadvantage against bigger competitors who had the deep pockets to be more flexible. They were caught in a cycle of only being able to work with clients who could pay on delivery, which severely capped their growth.

By finding a way to offer extended payment terms without shouldering the cash flow burden themselves, they could level the playing field and compete for bigger contracts.

They brought in a platform like Comfi, which let them offer buyers the flexible payment options they needed while they got their own money instantly. This strategic move unlocked several key benefits almost overnight:

- New Customer Wins: They could confidently onboard larger clients who demanded net 60 or 90-day terms as standard.

- Bigger Order Sizes: Existing customers started placing larger orders, knowing they had more breathing room to pay.

- Zero Credit Risk: The platform managed the collections and absorbed the risk of any non-payment, taking a huge weight off their shoulders.

This simple shift led to a 20% growth in their customer base in the first year alone. It’s perfect proof that smart working capital management isn't just an internal finance issue—it's a powerful tool for driving sales and market expansion.

Your Working Capital Improvement Action Plan

Theory and real-world examples are great, but turning those insights into action is what actually drives growth. This final section is your roadmap—a clear, step-by-step plan to take control of your company's financial health. Think of it as a checklist for making proactive working capital management a core part of your strategy, not just an afterthought.

Moving from constantly putting out fires to proactively optimising your cash flow requires a structured approach. Follow these steps to methodically find the weak spots, implement targeted fixes, and track your progress toward becoming a more liquid and resilient business.

Step 1: Diagnose Your Current Cycle

You can't improve what you don't measure. The very first thing to do is calculate your current working capital cycle (you'll also see it called the cash conversion cycle). Get the formulas out for Days Inventory Outstanding (DIO), Days Sales Outstanding (DSO), and Days Payables Outstanding (DPO) and nail down a precise number of days.

This single number is your baseline. It tells you exactly how long your cash is tied up in the business and gives you a starting point to measure every improvement against.

Step 2: Pinpoint the Bottleneck

With your cycle calculated, it's time to play detective. Look at the three parts. Where’s the biggest drag?

- Is your DSO too high? This is a huge red flag that slow customer collections are draining your cash.

- Is your DIO elevated? That means too much of your capital is sitting on shelves as slow-moving inventory.

- Is your DPO unusually low? You might be paying suppliers faster than you need to, needlessly hurting your own cash reserves.

Usually, one of these areas will be a much bigger problem than the others. Focusing your initial efforts there will give you the biggest and fastest win.

Step 3: Implement Operational Improvements

Now for the action. Pick one or two specific strategies from this guide that directly address your bottleneck. If slow collections are killing your cash flow, start by offering a small early payment discount. If dusty inventory is the problem, focus on better demand forecasting to avoid overstocking in the first place.

The key is to start small and be consistent. Trying to fix everything at once is a recipe for getting overwhelmed. Master one change, measure its impact, and then build on that success.

Step 4: Evaluate Modern Solutions

Once you’ve tightened things up internally, it's time to look outside. Could modern tools help you grow even faster? See how platforms that let you offer flexible payment terms—while you get paid right away—could help you land bigger deals or break into new markets. This is all about using external solutions to get past the limits of your own internal working capital.

Step 5: Set Goals and Track Progress

Finally, you need to make it official. Set clear, measurable goals. For example, aim to reduce your working capital cycle by a specific number of days within the next quarter.

Then, check your metrics every month. See what's working, celebrate the wins, and adjust your plan as needed. This continuous loop of analysis, action, and review will embed sharp working capital management into the very DNA of your business.

Frequently Asked Questions

When you're running a business, getting your head around working capital can bring up a lot of questions. We've put together some straight answers to the most common queries we hear from business owners, helping clear up the key concepts we've covered in this guide.

How Often Should I Review My Working Capital?

You should be calculating and reviewing your working capital at least monthly. Think of it as a regular financial health check-up. A monthly look is frequent enough to catch any negative trends or potential cash shortfalls before they snowball into serious problems. This rhythm gives you a clear, consistent picture of your liquidity.

If your business is in a high-growth phase or the economy feels a bit shaky, stepping that up to a weekly review is a smart move. It gives you the agility to make quick, informed decisions when things are moving fast. Using good accounting software can automate these calculations, giving you a real-time dashboard of your financial health without all the manual crunching.

Is It Possible to Have Too Much Working Capital?

Yes, absolutely. While having negative working capital is a clear red flag that you're in financial trouble, having way too much can signal some major inefficiencies. It often means you have a pile of cash just sitting idle in a bank account instead of being put to work growing the business.

An overabundance of working capital might also be a sign that your money is unnecessarily tied up in slow-moving or, even worse, obsolete inventory that isn't selling.

The goal isn't to maximise working capital; it's to find that sweet spot—the optimal level that fuels your daily operations efficiently without wasting precious resources. This is exactly why optimising your working capital cycle is so critical.

What Is the Difference Between Working Capital and Cash Flow?

This is a really important distinction to get right. Working capital is a snapshot. It’s your company’s financial health at a single moment in time, calculated by taking your Current Assets and subtracting your Current Liabilities. It shows you the resources you have on hand to cover your short-term bills.

Cash flow, on the other hand, measures the actual movement of money in and out of your business over a period of time—say, a month or a quarter. A business can look profitable on paper but still go under because of poor cash flow. This happens all the time when, for example, customers take too long to pay their invoices. Getting a solid grip on your working capital is one of the most direct and effective ways to strengthen your overall cash flow.

Ready to stop waiting on invoices and unlock your business's growth potential? With Comfi, you can get paid instantly while offering your customers flexible payment terms. Discover how our seamless platform can improve your cash flow and help you scale faster. Get started now.

Related Reading

- How Can MENA SMEs Master Working Capital?

- Staffing Agency Payroll Financing UAE: Boost Cash Flow 2026

- SME Cash Flow Management: A Guide for MENA Businesses

- Improve Working Capital for UAE IT Services Business

Looking to improve your cash flow? Explore Comfi's Invoice Discounting solutions.