Mastering FMCG distributor payment terms UAE

You have the order. The retailer is happy. Your sales team is celebrating.

Then finance opens the ageing report and the mood changes.

That is the daily reality behind FMCG distributor payment terms UAE. On paper, the business looks healthy because goods are moving. In the bank account, it can feel tight because cash is not moving at the same speed. A supplier can win shelf space in a major chain, deliver on time, and still spend weeks or months waiting to collect.

For new suppliers, this mismatch is usually the first shock. FMCG is fast on the shelf and slow in receivables. If you do not manage that gap properly, growth starts to punish you. The more you sell, the more cash gets trapped between delivered stock and delayed payment.

The UAE FMCG Supplier's Dilemma Sales Are Up But Cash Is Down

A common pattern looks like this. A supplier lands a supermarket listing, pushes inventory out, hires more delivery support, and increases purchases from manufacturers to keep fill rates stable. Revenue rises. Cash drops.

The reason is simple. Retailers often pay on long cycles, and many do not pay exactly when the contract says they should. The pressure is not limited to one or two difficult accounts. In the UAE, 56% of B2B invoices become overdue, and large supermarkets can impose terms such as Net 120 days, which creates a serious cash-flow gap for FMCG suppliers (supermarket supplier payment terms in the UAE).

Why growth can hurt

In FMCG, every extra order creates immediate obligations:

- You need stock now: Your manufacturer or importer expects you to confirm and pay on their timeline.

- You need logistics now: Warehousing, transport, merchandising, and route costs do not wait for the retailer to settle.

- You need buffer stock: If one SKU moves faster than forecast, you still need to replenish.

A new supplier often assumes bigger orders mean more comfort. In practice, bigger orders often mean bigger exposure.

Tip: Treat every large retail order as two transactions, a sale to the retailer and a separate funding event you must survive until collection.

The invisible squeeze

The squeeze gets worse when your own suppliers are overseas. Import partners often want deposits, quicker settlement, or tighter discipline before releasing the next shipment. So while your receivable sits with a retailer, your payable sits on your desk demanding attention.

That is why so many UAE FMCG businesses say the same thing in different words. Sales are strong, but cash feels weak. The issue is not demand. The issue is timing.

Understanding Standard FMCG Payment Terms in the UAE

A new supplier often sees Net 30 on a customer form and assumes cash will arrive a month after delivery. In UAE FMCG, that assumption causes trouble. The term on the contract is only the starting point. The actual collection cycle depends on invoice acceptance, delivery confirmation, claim handling, and the buyer’s actual payment run.

Across local trade, suppliers often work with Net 15, Net 30, Net 60, and Net 90. Some smaller accounts still ask for COD, and some new or higher-risk relationships start with partial upfront payment. If you need a practical benchmark for how large retailers set these terms, this guide to supermarket supplier payment terms in the UAE gives useful context.

In practice, Net 15 to Net 30 is common on paper, but actual payment often slips by an additional 15 to 20 days, extending the effective collection cycle to 30 to 50 days (payment terms culture in the UAE).

What each term really means

Net terms

Net 15 / Net 30 / Net 60 / Net 90 means the buyer is expected to settle the full invoice value within that number of days from the invoice date.

The label matters less than the process behind it. I have seen disciplined buyers pay a Net 60 account more reliably than a messy Net 30 account. The difference usually comes down to whether the buyer posts the GRN on time, clears matching issues quickly, and releases payments on a fixed cycle without constant follow-up.

Check four things before treating any term as usable cash timing:

- invoice acceptance speed

- goods received note processing

- clean matching between PO, delivery note, and invoice

- actual payment discipline against agreed dates

That constitutes the true credit profile.

COD and partial upfront payment

Cash on Delivery shows up more in smaller outlets, independent trade, and early-stage account relationships than in large organised retail. It protects liquidity, but it also limits access to buyers that expect supplier credit as part of the commercial model.

A staged payment structure often works better when the stock is imported, made to order, or allocated specifically for one customer. Common setups include:

- Deposit on order confirmation

- Balance on delivery

- Balance after a short credit period

That structure shares the funding burden instead of leaving it entirely with the supplier.

Terms are only half the agreement

Payment terms should be reviewed together with deduction rules, claim timelines, listing charges, promotional support, and document requirements. A short nominal term can still be weak if the buyer routinely parks invoices over minor discrepancies or deducts first and reconciles later.

The practical question is simple. How fast does an approved invoice become cleared cash in your account?

Key takeaway: A good payment term is one your customer can process cleanly and pay consistently, without disputes, undocumented deductions, or missed payment runs.

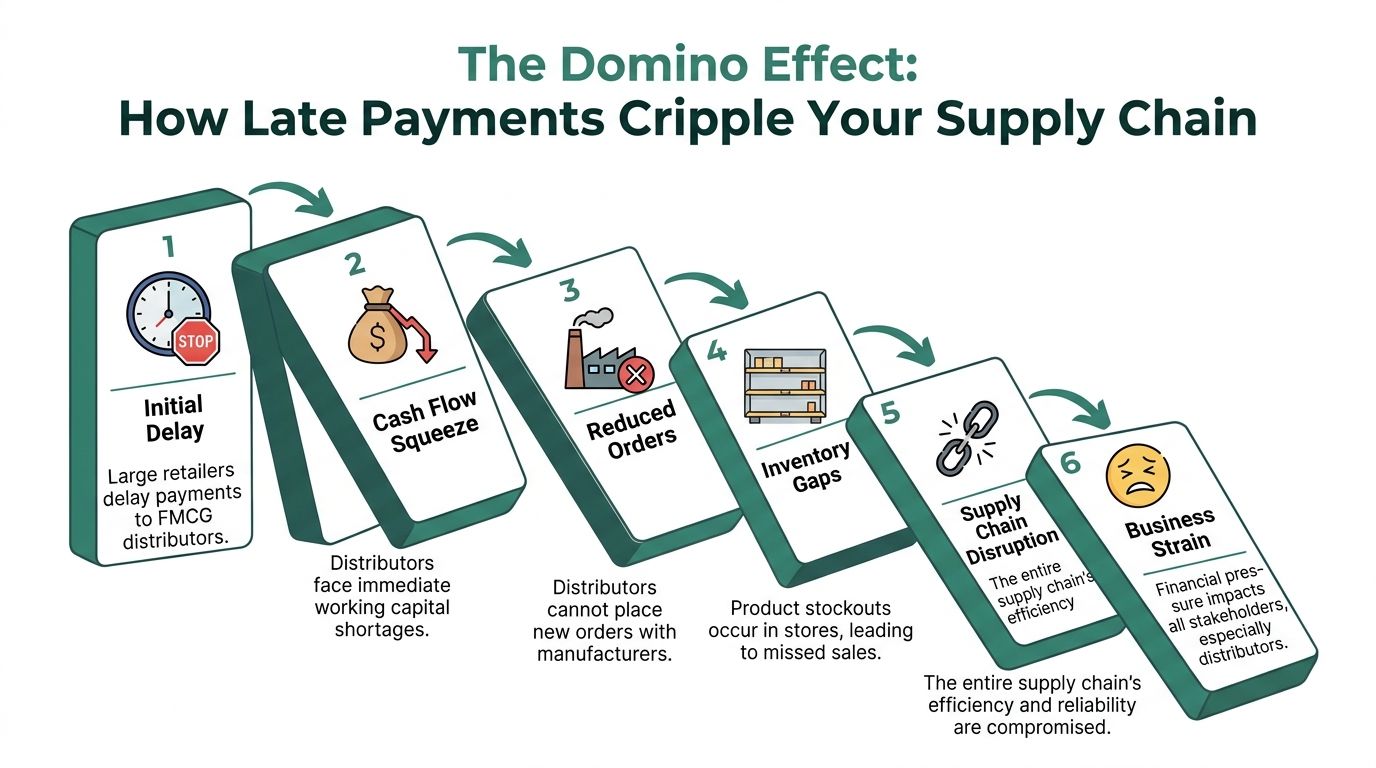

The Domino Effect How Late Payments Cripple Your Supply Chain

Late payment in FMCG is not a finance department irritation. It is a supply chain problem.

When the retailer delays settlement, the distributor does not just wait. The distributor starts making compromises. Purchase orders are delayed. Import schedules get pushed. Safety stock shrinks. Sales teams stop chasing new placements because the business cannot support more receivables.

Where the damage starts

Across the UAE B2B market, late payments affect 56% of invoices, bad debts account for 6% to 10% of sales, and average payment terms sit around 40 days, which puts heavy pressure on a supplier’s ability to manage its own payables (Atradius UAE B2B payment practices report).

That pressure often starts with ordinary operational issues, not dramatic defaults. A goods received note is not posted. A claim is left unresolved. A buyer asks for a statement reconciliation before releasing payment. The invoice ages while everyone says the account is “in process”.

What happens next

The damage is cumulative.

- Your import supplier tightens: They may ask for advance payment, shorter settlement, or hold the next shipment.

- Your replenishment slows: Fast-moving SKUs run short because you cannot reorder with confidence.

- Your shelf presence weakens: Empty facings hurt sales and damage your standing with the retailer.

- Your margins get hit: You may accept rush freight, smaller order sizes, or unfavourable buying terms just to keep stock flowing.

A delayed payment from one supermarket can affect customers who never paid late at all. That is why I call it a domino effect. One blocked receivable can distort your entire buying plan.

Why international suppliers feel this first

Imported brands add another layer of stress. Overseas manufacturers usually care less about your local retail collection problems than they care about their shipment release conditions. If they want funds before dispatch, your local receivable timing becomes irrelevant to them.

Practical view: Retailers buy time with their payment terms. Import suppliers often sell certainty, not time. That mismatch is where many distributors get trapped.

The result is a business that looks busy but becomes defensive. Instead of planning expansion, finance starts planning survival.

How to Negotiate Better Payment Terms and Manage Credit Risk

You cannot eliminate payment pressure in FMCG, but you can stop making it worse through weak contracts and loose credit discipline.

The first mistake new suppliers make is treating a retailer’s first draft as standard. It is standard for the buyer, not for your cash flow. The second mistake is offering generous credit without matching controls.

Build terms before you build volume

For high-volume wholesaler relationships, Net 60 is common, but agreements should also include late fees such as 1.5% monthly and credit limits capped at 20% to 30% of annual sales to control default risk (distribution agreements in the UAE).

Those clauses matter because they set boundaries before the account becomes politically difficult to manage.

A strong agreement should cover more than the headline term:

- Payment trigger: Is payment based on invoice date, delivery date, or acceptance date?

- Required documents: PO, delivery note, stamped invoice, proof of receipt.

- Dispute window: How long does the buyer have to raise a claim?

- Deduction rules: Which deductions are allowed, and what approval is required?

- Late payment consequences: Fees, credit hold, or escalation path.

What usually works in negotiation

Ask for structure, not just speed

A buyer may reject a shorter term but accept a safer structure. Examples include:

- Part upfront, balance later: Useful for imported, promotional, or customised stock.

- Limit by account age: Credit increases only after clean payment history.

- Term extensions tied to safeguards: Bank guarantees, letters of credit, or stronger documentation.

Control exposure account by account

Do not give every customer the same limit. A disciplined smaller retailer may deserve more flexibility than a large buyer with chronic admin delays.

Use a simple internal rule set:

- green accounts get normal release

- amber accounts require finance review

- red accounts move to hold or partial prepayment

For teams building their controls, this guide on payment risk is a useful starting point.

Tip: Sales should negotiate volume. Finance should decide exposure. When one team does both, payment discipline usually slips.

What does not work

Chasing overdue invoices without fixing root causes does not work. Neither does relying on verbal promises. If your team keeps hearing “payment next run” but deductions and mismatches remain unresolved, the account is not under control.

Good credit management is not aggressive. It is organized.

Unlock Your Working Capital with Modern B2B Payment Solutions

A common UAE FMCG squeeze looks like this. Stock has landed, shelves are moving, and sales reports look healthy. But cash is still tied up in 45, 60, or 90-day receivables, while your overseas supplier wants settlement on the agreed date. That gap is where growth starts to hurt.

Modern B2B payment tools address that mismatch by turning approved invoices into usable cash before the buyer pays in full. For FMCG suppliers, that matters because one delayed supermarket payment can hold up your distributor, then your freight booking, then your next supplier remittance. The problem is not only slow collection. It is the chain reaction that follows.

Two tools usually matter most. The first is invoice discounting in the UAE, where you receive early payment against approved invoices instead of waiting for the full credit term to run. The second is B2B Buy Now Pay Later (BNPL), which gives buyers structured time to pay without forcing the supplier to carry the whole financing burden on its own balance sheet.

Used properly, these tools do not replace credit control. They support it.

A finance team still needs clean invoicing, proof of delivery, deduction management, and buyer approval discipline. But once those basics are in place, fintech funding can smooth the gap between selling locally and paying internationally. That gives suppliers room to reorder faster, protect supplier relationships, and avoid the scramble for emergency cash each time a key account pays late.

Related Reading

- How Comfi’s B2B Buy Now Pay Later Solution Enhances Cash Flow for Businesses in the UAE

- Deferred Payment for Business Purchases UAE: A Guide 2026

- Software Reseller Payment Terms UAE: A Practical Guide

- Unlock Cash Flow: How to Get Extended Payment Terms From Suppliers in the UAE

Ready to improve your business cash flow? Get started with Comfi today.