Technology Company Working Capital Middle East: 2026 Guide

Your sales pipeline looks healthy. New contracts are coming in. The product team needs more people, customer success is stretched, and your buyers still want payment terms. Yet the cash account feels tighter each month.

That tension sits at the centre of technology company working capital Middle East planning. On paper, growth says you're winning. In the bank, timing says something else. Many MENA tech firms, distributors, and auto businesses aren't dealing with a profitability problem first. They're dealing with a timing problem that grows as the business grows.

The Growth Paradox for MENA Tech Companies

A familiar pattern shows up across the region. A software company signs annual contracts but invoices on terms. An e-commerce operator sells fast but has to hold stock. A marketplace grows GMV while supplier payments, marketing spend, and payroll hit long before customer cash lands.

That's why working capital deserves board-level attention. PwC's 2025 Middle East Working Capital Study says regional companies recorded 6.3% revenue growth in 2024, yet could free up an additional $54.7 billion in liquidity through better working capital efficiency according to PwC's Middle East Working Capital Study 2025. The signal is clear. Revenue growth and cash health don't automatically move together.

Why growth can drain cash

Tech founders often assume the cash profile of a digital business should be lighter than a traditional business. Sometimes that's true. Often, it isn't.

Enterprise sales cycles are long. Buyers negotiate procurement steps, acceptance milestones, and internal sign-offs. Meanwhile, your company still pays salaries, cloud bills, implementation costs, partner commissions, and customer acquisition spend on time.

Three pressure points usually create the paradox:

- Customer terms stretch cash receipt. You book the sale now, but the money arrives later.

- Scaling costs arrive upfront. Hiring, onboarding, product delivery, and go-to-market spend can't wait for collections.

- Banks underwrite yesterday's statements. Fast-growing firms need decisions based on live trading activity, not only historical ratios.

Practical rule: If your sales team is accelerating faster than your collections process, growth will feel expensive.

What tends to work better

The strongest operators don't treat working capital as a back-office clean-up task. They build it into commercial design. That means aligning payment terms, invoice processing, procurement timing, and buyer onboarding before cash pressure becomes urgent.

It also means choosing tools that fit how modern firms sell. That's one reason more founders and finance teams are paying attention to embedded finance and fintech infrastructure in the region, especially as B2B buying shifts online. For a broader view of that shift, this overview of MENA fintech trends gives useful context.

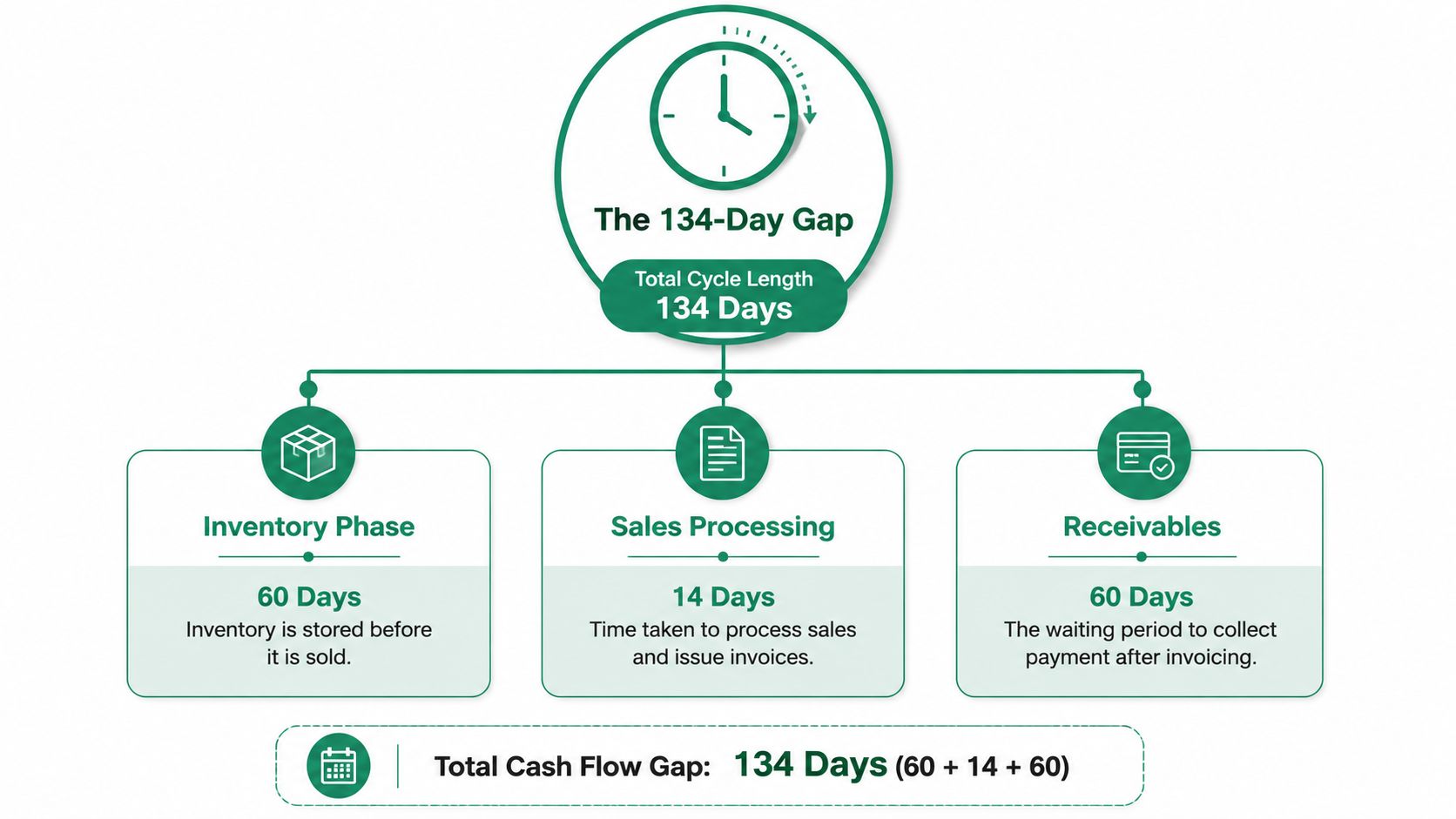

The 134-Day Cash Flow Gap in the UAE

For many UAE SMEs, the working capital problem isn't abstract. It's measurable. SMEs in the UAE face a net working capital cycle of roughly 134 days, made up of 112 days of inventory, 47 days of accounts receivable, and 25 days of accounts payable, based on UAE SME working capital benchmarks.

That's a long time to fund operations before cash returns.

What those numbers mean in practice

Think of the cycle as three clocks running at once.

First, inventory sits in the system. For a distributor, that means goods in storage. For a hardware-enabled tech business, it can mean devices, components, or returned stock waiting to move again.

Then comes receivables. You've delivered the product or service, sent the invoice, and now you wait. Your buyer may pay on standard terms, later than agreed, or only after internal approvals clear.

Payables move in the opposite direction. Your suppliers usually won't wait as long as your customers do. That gap creates the funding strain.

Why tech SMEs still feel this pressure

People hear “technology company” and assume no stock, no friction, no working capital issue. That misses the way many UAE tech firms operate.

A regional software reseller may carry implementation costs before payment. A B2B commerce platform may need to pay suppliers quickly to keep supply reliable. An electronics seller may look like a software business on the front end but still carry inventory risk in the background.

Good finance teams don't ask only, “Are we growing?” They ask, “How many days are we financing that growth ourselves?”

What owners should inspect first

Start with a short internal review:

- Map the invoice journey. Check how long it takes from delivery to invoice issuance. Delays here are self-inflicted and common.

- Separate customer types. Enterprise, government-linked, and SME buyers behave differently. Don't manage them as one receivables bucket.

- Review supplier pressure points. If suppliers demand quick payment, that needs to be reflected in pricing and deal structure.

- Check the tax layer too. Cash planning is tighter when tax obligations and working capital stress hit together. For owners preparing ahead, this guide on UAE corporate tax relief for SMEs is a useful operational read.

The key lesson is simple. A long cash cycle doesn't only slow expansion. It changes what growth costs you.

Unlocking Growth with Modern Capital Solutions

A lot of finance leaders still approach this problem with old tools. They push collections harder, delay supplier payments, or ask founders for another equity round. Sometimes those moves help. Often, they just move stress from one part of the business to another.

That's why newer solutions matter. Regional analysis still lacks good benchmarks for tech companies, especially those with SaaS, e-commerce, and platform cash cycles, as noted by Middle East Briefing's analysis of working capital gaps. When the sector data is thin, products that understand transaction flow become more useful than generic bank structures.

Invoice discounting in plain English

Invoice discounting is simple when explained properly. You've already done the work, delivered the goods, or completed the milestone. Instead of waiting through the full payment term, you access cash from that issued invoice earlier.

It's like converting a dated promise into usable operating cash.

This is especially useful when:

- Your buyers are strong but slow. The issue isn't willingness to pay. It's timing.

- Your sales team is landing larger contracts. Bigger invoices can create bigger cash gaps before settlement.

- You need continuity in payroll or supplier payments. The invoice exists, but the business can't pause while waiting.

One practical reference point is this guide to invoice financing for UAE IT companies, which helps connect the product mechanics to software and services businesses.

Embedded payment terms for B2B sales

The second tool is embedded payment terms, often framed as B2B Buy Now Pay Later. This matters when your buyer wants time, but you don't want your own cash cycle to stretch with every deal.

The easiest analogy is this. Your buyer gets breathing room. Your operations don't lose oxygen.

That can help in several ways:

- Commercial teams close more smoothly because payment flexibility removes one buying objection.

- Order values often become easier to justify when buyers can spread payment over agreed terms.

- Supplier relationships stay cleaner because your business doesn't have to choose between customer friendliness and internal liquidity.

For founders comparing the wider funding picture, including equity and debt alternatives, this roundup of UAE startup funding options in 2025 is a useful companion read.

What usually does not work

Some fixes create fresh problems:

- Using founder capital for recurring working capital gaps. That's expensive and distracting.

- Discounting too heavily just to get early payment. Margin disappears quickly.

- Relying only on overdrafts. Traditional facilities can be rigid when your trading profile changes month to month.

One option in this category is Comfi, which supports invoice discounting, embedded payment terms, and dealer financing through digital workflows. The useful distinction isn't branding. It's the operating model. The tools sit closer to invoices, orders, and buyer transactions than a conventional paper-heavy facility does.

How to Qualify and Integrate Fast Capital Solutions

Most owners still assume these solutions require the same process as a bank line. Long forms, static statements, weeks of back-and-forth, then a decision based mostly on last year's numbers.

Modern platforms work differently. Fintech platforms using API-driven invoice data can achieve 20 to 50% higher approval rates for SMEs than legacy banks, while also cutting average time-to-funding from several days to under 24 hours, based on regional fintech platform analysis.

What the platform actually checks

Instead of relying mainly on a broad financial snapshot, digital underwriting looks closer to live trading data. That includes invoice behaviour, order flow, payment history, buyer concentration, and the consistency of commercial activity.

In practical terms, the platform wants to understand whether your receivables are observable, trackable, and tied to real business activity.

What you need ready

Preparation matters more than paperwork volume. The cleanest onboarding usually comes from businesses that organise their trading data before applying.

A sensible checklist looks like this:

- Invoice records. Issued invoices should be current, readable, and easy to reconcile.

- Buyer information. You need clarity on who pays, how they pay, and whether payment behaviour is stable.

- Process ownership. Someone in finance should own the integration and document flow, even if setup is light.

How integration fits into daily workflow

Good integrations don't ask the business to work twice. They pull from tools teams already use, then route invoice and payment information into a decision engine.

That matters for two reasons. First, eligibility can be assessed faster when data arrives directly from source systems. Second, finance teams spend less time producing one-off packs for every review.

For UAE IT services firms thinking through the operational side, this guide on how to improve working capital for a UAE IT services business gives a useful workflow lens.

Where businesses get stuck

The biggest failures usually aren't technical. They're internal.

Some companies apply before tightening invoice controls. Others ask for flexible buyer terms without a clear collections policy. A few treat fast capital as a substitute for discipline, when it works better as an extension of discipline.

The strongest setup combines three things: clean data, repeatable invoicing, and a clear commercial reason for using the product.

The Real-World ROI of Improved Working Capital

Return on working capital usually shows up in day-to-day operating decisions, not in a single headline metric.

A software reseller can commit to a larger deployment without building payroll risk into the project plan. A B2B distributor can approve buyer terms that help win the order, while still keeping its own cash cycle under control. An auto dealer can rotate slower stock out and bring in fresher inventory before the forecourt starts working against margins.

That is where the payoff becomes visible. Teams stop treating every growth decision as a cash gamble.

Where the benefit appears first

For MENA SMEs, the first gains tend to land in a few practical areas:

- Sales execution. Commercial teams can offer structured payment terms without sending every deal into a finance bottleneck.

- Procurement timing. Stock, parts, licences, or subcontracted capacity can be secured when demand is there, not weeks later when cash finally clears.

- Collections stability. Finance gets a more even inflow profile and spends less time patching shortfalls between due dates.

In practice, predictability matters more than a lower funding cost on paper. A facility that fits the invoicing cycle, buyer approval process, or dealer stock turn can save more money operationally than a cheaper product that creates delays or admin overhead.

What improves inside the business

The effect is usually indirect, but it is measurable in how the business behaves.

Hiring decisions get easier because payroll is no longer tied so tightly to one or two customer receipts. Management can approve sensible growth spend, such as implementation staff, sales coverage, or stock purchases, without protecting cash by default. Supplier conversations also change. Terms become part of planning, not a last-minute negotiation triggered by a tight bank balance.

For tech and auto SMEs in the Middle East, that operational fit matters. The strongest working capital setup is the one that sits inside existing order flow, invoicing, and repayment habits, then reduces timing pressure across the cycle.

Better working capital does not fix a weak business model. It gives management more room to make disciplined decisions at the right time.

That is the commercial return. Better control over the timing of growth, with fewer forced pauses in between.

Your Next Steps to Secure Predictable Cash Flow

If your business is growing but cash still feels tight, don't reduce the issue to collections alone. Look at the full operating cycle. A core constraint is often the time lag between paying out and getting paid in.

That's why working capital strategy belongs inside sales, procurement, and finance together. If those teams work in silos, your business ends up funding avoidable delays.

A quick self-check for SME owners and finance leads

Review these questions thoroughly:

- Do you know your current cash conversion cycle well enough to explain where the delay sits?

- Are invoices issued immediately after delivery or milestone completion, or do they wait for internal admin?

- Have you lost deals because buyers wanted payment flexibility you couldn't offer?

- Are your supplier terms shorter than your customer terms, leaving you to fund the gap?

- Does your team rely on overdrafts, founder cash, or ad hoc fixes every time growth accelerates?

- Can your systems show live receivables and buyer behaviour, or are you still working from static reports?

What to do next

If several of those questions made you pause, the next move isn't complicated. Review your invoicing flow, clean up receivables data, and assess whether invoice discounting, embedded payment terms, or dealer-focused structures fit your trading model.

The businesses that manage cash best in MENA don't always grow slower. Usually, they grow with more control. That makes expansion less stressful, supplier relationships steadier, and planning much more realistic.

If you want to see how a digital SME capital platform can fit into your existing workflow, take a look at Comfi. It supports invoice discounting, B2B payment terms, and dealer financing through a paperless setup that connects with normal operating systems, helping businesses access working capital without forcing a full process rebuild.

Related Reading

- How Can MENA SMEs Master Working Capital?

- Staffing Agency Payroll Financing UAE: Boost Cash Flow 2026

- SME Cash Flow Management: A Guide for MENA Businesses

- Technology Company Working Capital Middle East

Looking to improve your cash flow? Explore Comfi's Invoice Discounting solutions. Get started today.