A Guide to Managing Outstanding Invoices for UAE SMEs

An outstanding invoice is a bill for completed work that has been sent to a customer but has not yet been paid. While it may still be within the agreed-upon payment window, it represents revenue you've earned but cannot yet use.

What Are Outstanding Invoices and Why They Matter

For most small and medium-sized businesses in the UAE, an invoice isn't just a document. It’s the culmination of a process: you’ve delivered the goods or finished the service, and that invoice acts as a formal promise that payment is forthcoming.

But here’s the crucial point: the time between sending that promise and the funds actually arriving in your bank account can create significant financial strain.

The Pipeline Blockage Problem

Think of your company's cash flow as a pipeline. In a healthy business, cash flows smoothly from clients to your accounts, providing the working capital needed for daily operations. This is the financial lifeblood that lets you pay salaries, buy inventory, and pursue new opportunities.

Outstanding invoices are like blockages in that pipeline. Every unpaid invoice traps earned revenue, slowing your cash flow to a trickle. A single blockage might not cause much trouble, but as more accumulate, the pressure builds. Suddenly, you may have healthy sales figures on paper but not enough cash in the bank to run the business effectively.

This isn't just a theoretical problem; it’s a daily reality for thousands of businesses. In the UAE's B2B sector, overdue invoices are a major issue, impacting a staggering 58% of all B2B sales. The challenge isn't always that customers can't pay—often, it’s due to administrative delays. With payment terms already averaging around 50 days, these delays can easily stretch the waiting period to 80 days or more, putting suppliers under immense pressure. To really grasp the scale of this, you can explore more data on B2B payment practices in the United Arab Emirates.

Managing outstanding invoices is not merely an administrative task. It is a core strategic function that directly influences your company's stability, agility, and capacity for growth in the competitive MENA market.

From Accounting Task to Business Strategy

Effectively managing these invoices is essential for survival and growth. When you ensure that cash is flowing consistently, you have the resources to operate without stress and seize new opportunities.

When your financial pipeline is clear, you can:

- Meet daily operational needs like paying salaries and rent on time without strain.

- Maintain strong relationships with your own suppliers by paying your bills promptly.

- Invest confidently in growth, whether it's a new marketing campaign or expanding your product line.

Ultimately, converting outstanding invoices into cash is fundamental to building a resilient and thriving business.

The Real Cost of Unpaid Invoices

Outstanding invoices are more than just numbers on a spreadsheet; they represent a direct drain on the lifeblood of your business. When revenue you've already earned is stuck in accounts receivable, the ripple effects can be felt across your entire operation, creating tangible problems that go far beyond a simple accounting entry.

Imagine trying to run a marathon with weights strapped to your ankles. You’re still moving, but every step is a struggle, and you’re constantly on the verge of exhaustion. Each unpaid invoice is another one of those weights, slowing you down and holding you back.

Growth Grinds to a Halt

One of the first and most painful consequences of late payments is stunted growth. Businesses thrive on their ability to be nimble and act on opportunities. But when your cash is tied up in someone else's accounts payable, your ability to make quick, decisive moves shrinks dramatically.

Imagine your top supplier offers a significant discount for buying inventory in bulk—a deal that could boost your profit margins for the entire quarter. Without cash on hand, you have to watch that opportunity slip away. The same goes for investing in a promising marketing campaign or upgrading critical equipment. It’s not a lack of ambition that holds you back; it’s a lack of liquidity. This is how outstanding invoices directly choke off the strategic investments that fuel expansion.

Your Business on the Hook: Credit Risk and Bad Debt

The longer an invoice remains unpaid, the less likely you are to ever see that money. This simple fact introduces a significant element of credit risk into your business. What starts as an "outstanding invoice" can quickly sour into bad debt—money you eventually have to recognize as uncollectible.

Writing off bad debt is a direct hit to your bottom line. In the UAE, this is a massive and growing challenge for B2B suppliers. Shockingly, bad debts now account for about 8% of the total value of B2B invoices in the country. For many SMEs, that means for every AED 100 they bill, AED 8 is lost forever. The problem is even worse in certain sectors, like pharmaceuticals, where bad debt can climb to a staggering 10% of all invoices. You can read the full research on rising bad debt in the UAE to get a clearer picture of the regional challenges.

Every day an invoice remains outstanding, it's not just a delayed payment; it's a growing risk to your financial stability. Proactively managing this risk is essential for long-term viability.

Measuring the Strain: The KPIs That Matter

To truly understand how unpaid invoices are affecting your business, you need to look beyond the total amount owed and start tracking specific metrics. These Key Performance Indicators (KPIs) act as a health check for your cash flow, turning vague concerns into concrete data you can act on.

Here are the essential KPIs every SME should be monitoring.

Key Metrics for Tracking Invoice Health

- Days Sales Outstanding (DSO): This measures the average number of days it takes you to collect payment after making a sale. A high DSO is a red flag, indicating that your cash is locked up for longer and signaling potential issues with your collections process or client creditworthiness.

- Cash Conversion Cycle (CCC): This tracks the time it takes to turn your investments (like inventory) into cash in the bank from sales. A long CCC puts a major strain on your working capital, as your money is tied up in the operational cycle, limiting your flexibility to pay bills or invest.

- Bad Debt Ratio: This is the percentage of your revenue that you have to write off as uncollectible. It directly measures your losses from non-payment. A rising ratio is a clear sign that your credit policies or collections efforts need a serious overhaul.

- Collection Effectiveness Index (CEI): This metric assesses how effective you are at collecting receivables during a specific period, compared to the total amount that was available to be collected. The CEI provides a precise score on your collections team's performance, helping you identify what's working and what isn't, so you can make targeted improvements.

By keeping a close eye on these numbers, you can spot trouble long before it becomes a full-blown crisis. If your DSO starts creeping up, for instance, you know it’s time to adopt a more assertive collections strategy. This is about shifting from reactive problem-solving to proactive financial management.

For a deeper dive, check out our guide on how to calculate and interpret Days Sales Outstanding. It’s a great starting point for turning raw data into a powerful tool for financial stability.

Best Practices for Managing and Reducing Outstanding Invoices

Effectively managing outstanding invoices isn't just about chasing down late payments. It’s about building a smart, systematic approach from the beginning that prevents them from becoming late in the first place. When you get this right, you spend less time playing detective and more time focusing on activities that actually grow your business.

The entire process can be broken down into three stages: setting clear expectations before the invoice is sent, actively monitoring during the payment period, and having a clear plan for when payments become overdue. Mastering these three stages provides a rock-solid framework for maintaining healthy cash flow.

Proactive Measures Before the Invoice Is Sent

The best way to deal with a late payment is to prevent it from happening. This foundational work begins long before an invoice is created, by establishing clear, professional ground rules with every client.

Think of it as building a strong foundation on three key pillars:

- Establish Crystal-Clear Payment Terms: Leave no room for ambiguity. Your payment terms must be clearly defined and agreed upon before any work begins. Specify the due date (Net 30, Net 60, etc.), accepted payment methods, and any penalties for late payments. This information shouldn't be hidden in the fine print; it should be front and center on every quote, contract, and invoice.

- Conduct Thorough Client Vetting: Not all clients have the same payment habits. Before entering a new partnership, do your homework. A quick credit check or requesting trade references can reveal a lot about a potential client's financial health and payment history.

- Offer Multiple Payment Options: Make it as easy as possible for clients to pay you. The more options you provide—bank transfers, credit cards, online payment gateways—the fewer excuses they have for delays. This simple step removes friction and accelerates cash collection.

Active Management During the Payment Period

The moment you send an invoice, the clock starts ticking. This is where active management becomes critical. Consistent communication and systematic tracking are your best tools, keeping your invoice top-of-mind without being intrusive.

A well-organized system prevents invoices from falling through the cracks. It's about sending the right message at the right time to keep the payment process moving forward.

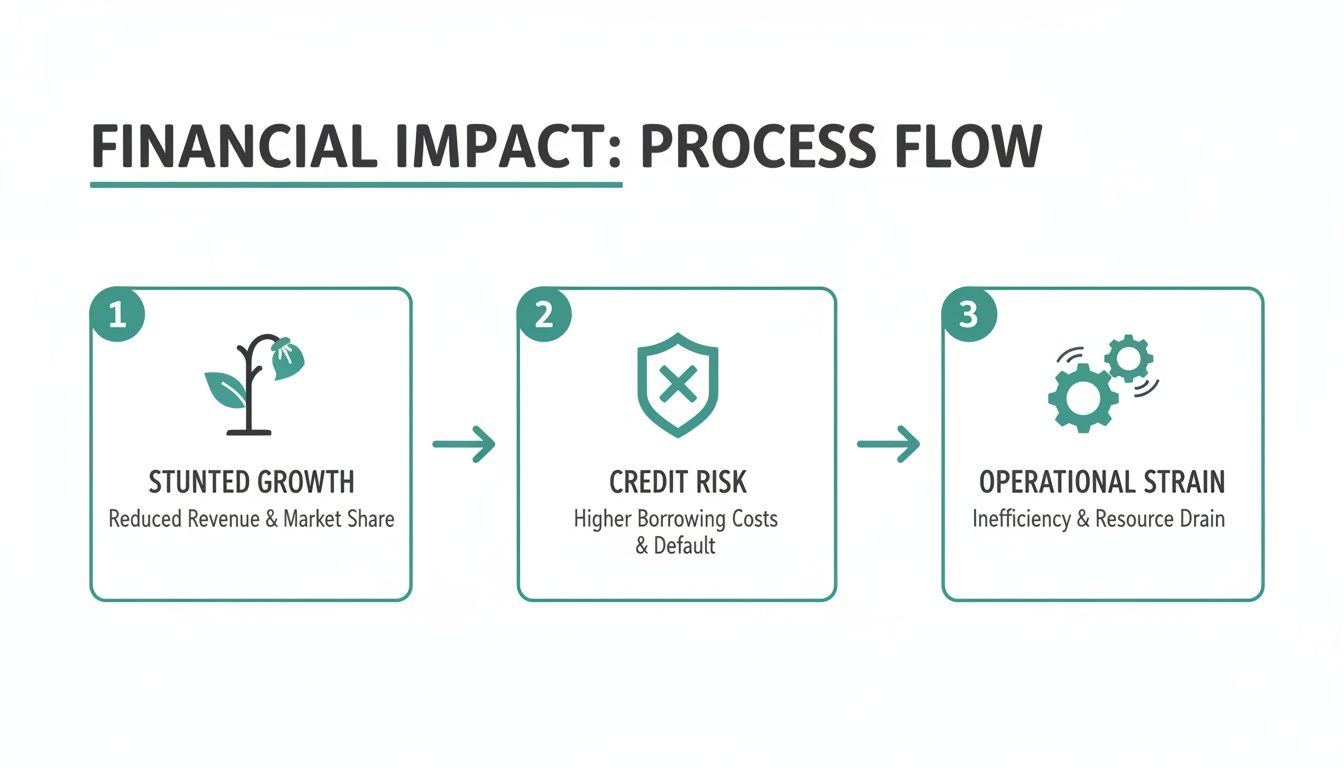

Failure to manage this stage can lead to serious roadblocks, such as stunted growth, rising credit risk, and significant operational strain.

As illustrated, these problems can feed into each other, creating a domino effect that can destabilize a business from multiple angles.

One of the most effective tools for this stage are automated payment reminders. These systems send polite, automatic follow-ups as the due date approaches, saving you significant manual effort while ensuring consistent communication. For a deeper look, explore our guide on creating an https://comfi.ai/blog/automated-invoice-system to get your entire workflow running on autopilot.

Reactive Collections for Overdue Invoices

No matter how perfect your system is, some invoices will inevitably go past their due date. When that happens, you need a structured, professional collections process that gets you paid without damaging the client relationship. The key is to escalate your efforts gradually and calmly.

A respectful but firm follow-up process is essential in the MENA region. Your communication should reflect an understanding of business culture while clearly stating your expectation of prompt payment.

Your collections strategy should follow a clear, step-by-step timeline:

- The Gentle Reminder (1-3 Days Past Due): Start with a polite email. The goal is to assume the delay is an oversight. A friendly nudge is often all it takes. For example: "Hi [Client Name], this is just a friendly reminder that invoice #[Invoice Number] was due on [Due Date]. Please let us know if you have any questions."

- The Direct Phone Call (7 Days Past Due): If the email receives no response, it's time to pick up the phone. Contact your counterpart in the accounts payable department. The mission is simple: confirm they have the invoice and get a specific date for when payment will be made.

- The Formal Escalation (15-30 Days Past Due): If payment is still missing, send a more formal email. This message should clearly state that the account is overdue and mention any applicable late fees as per your terms. It's also a good practice to copy a more senior contact at their company.

- The Final Demand (45+ Days Past Due): This is your last step before considering external assistance. Send a final demand letter that outlines all invoice details, the total amount now owed (including any fees), and a firm, final deadline for payment.

By systemizing these proactive, active, and reactive stages, you can transform invoice management from a chaotic, stressful task into a predictable and efficient part of your business operations.

How Outstanding Invoices Show Up on Your Books

When you send an invoice, you've done more than just request payment—you've created recognized value that is legally owed to you. In accounting, this value must be officially recorded on your company’s financial statements, long before the cash actually hits your bank account. This isn't just a formality; it’s a critical practice for maintaining an accurate picture of your financial health.

An outstanding invoice is recorded in an account called Accounts Receivable (AR). The easiest way to think of AR is as a holding area for all the money your customers owe you for goods or services they've already received. It is a crucial component of your balance sheet.

Accounts Receivable Is a Current Asset

On your balance sheet, Accounts Receivable is classified as a current asset. This is an important distinction, as it signifies resources you expect to convert into cash within one year. In essence, your outstanding invoices are treated as money that is just around the corner, and they directly contribute to your company's total asset value.

This is precisely why sharp AR management is so vital. A well-organized AR ledger provides a clear, optimistic view of incoming revenue, which is essential for financial planning and forecasting. Using robust cloud-based accounting software is fundamental for keeping your invoices, payroll, and ledgers in order, all of which ties back to how you track these outstanding payments.

Facing Reality: The Allowance for Doubtful Accounts

However, every experienced business owner knows that optimism must be balanced with a dose of reality. Unfortunately, not every invoice you issue will be paid. To account for this without distorting your financials, accountants use a clever tool called the Allowance for Doubtful Accounts.

This is what’s known as a contra-asset account, which is a technical way of saying it works against your Accounts Receivable. Its sole purpose is to hold an estimate of the AR you likely won't be able to collect. By subtracting this allowance from your total AR, you arrive at a much more realistic figure for the actual value of your receivables.

Your financial statements should tell the true story of your business. The Allowance for Doubtful Accounts ensures that your asset value isn't inflated by invoices that have little chance of ever being collected.

A Practical Example: Following the Journal Entries

Let’s walk through how this plays out with a couple of simple journal entries. Imagine your company, "Dubai Designs," makes a sale of AED 10,000 on credit to a client.

- Step 1: Recording the SaleFirst, you’d record the revenue and the corresponding receivable. This entry increases both your sales figures and your AR asset.

- Debit (Increase) Accounts Receivable: AED 10,000

- Credit (Increase) Sales Revenue: AED 10,000

This entry officially shows you’ve earned the money and are now awaiting collection.

- Debit (Decrease) Allowance for Doubtful Accounts: AED 10,000

- Credit (Decrease) Accounts Receivable: AED 10,000

Notice what this entry doesn't do—it doesn't affect your revenue at this point. The expense of the bad debt was already accounted for when you periodically set aside funds in the Allowance account. This write-off is simply a housekeeping task. It cleans up your books by removing the uncollectible invoice from your AR and drawing down the allowance you had reserved for it. This disciplined approach is what keeps your financial reporting accurate and trustworthy.

Modern Solutions to Unlock Capital from Your Invoices

Even with the most efficient internal processes, a 60 or 90-day payment term creates a fundamental challenge: your earned revenue is locked away, unable to fuel your daily operations or your next strategic move. Good financial discipline is essential, but it doesn't change the reality that you're stuck waiting.

This is where modern financial technology can completely change the game. Instead of passively waiting for payment terms to expire, businesses can now actively convert their accounts receivable into immediate cash. It’s about closing the painful cash flow gap that holds so many great SMEs back.

Turning Receivables into Ready Capital

The core idea is simple but powerful: your outstanding invoices aren't just a promise of future payment; they're an asset you can leverage today. Two of the most effective ways for B2B companies to do this are invoice discounting and Buy Now, Pay Later (BNPL) arrangements for business clients.

These tools allow a business to receive a significant portion of an invoice’s value upfront, often within 24 to 48 hours. This injection of cash provides the liquidity to pay suppliers, fund new inventory, or cover payroll without waiting weeks or months for customer settlement.

The goal is to transform your balance sheet from a static record of assets into a dynamic source of working capital. This empowers you to operate with more agility and far greater financial predictability.

How Invoice Discounting Works

Invoice discounting is a straightforward method to access the money you've already earned, but sooner. It is not a loan. Think of it as fast-forwarding your payment cycle.

The process typically unfolds in a few simple steps:

- You issue an invoice to your customer as you normally would, with your standard payment terms.

- You submit that invoice to a platform offering discounting services.

- You receive an advance for a large percentage of the invoice’s value, often within a day or two.

- Your customer pays the invoice on its original due date.

- You receive the remaining balance, minus a small, agreed-upon service fee.

This model is a valuable tool for businesses with reliable customers that need to smooth out their cash flow between payments. You can learn more about how invoice discounting empowers SMEs to take control of their cash flow and accelerate their growth.

The Role of a Facilitator Like Comfi

In this new financial ecosystem, companies like Comfi act as facilitators. Our platform is designed to connect businesses with the capital that's already sitting in their outstanding invoices. For suppliers in the UAE and the wider MENA region, this means you can upload an approved invoice and get it paid, fast.

This allows clients to unlock their working capital on their own terms. Instead of being stuck in a 30, 60, or 90-day holding pattern, you can access your cash and put it right back to work. This newfound liquidity means you can jump on growth opportunities—like buying inventory in bulk or launching a new marketing campaign—without delay.

The rapid digitization of commerce in the region is making these solutions more accessible than ever. The UAE e-invoicing market, valued at USD 76.72 million in 2024, is projected to grow to USD 311.58 million by 2033. This expansion, fueled by digital transformation and updated VAT regulations, is creating the perfect environment for platforms that turn digital invoices into instant cash flow.

Turn Your Invoices into Fuel for Growth

Let's be honest: managing outstanding invoices can feel like a chore. It’s an administrative headache that often gets pushed to the bottom of the to-do list. But what if we started looking at it differently? What if those unpaid invoices weren't a problem to be solved, but a powerful asset just waiting to be unlocked?

That simple shift in perspective is the key. It's about moving from a reactive collections mindset—chasing down late payments—to a proactive capital strategy.

This transformation begins with getting your own house in order. Strong internal processes are the foundation. When you set crystal-clear payment terms, stay on top of your receivables, and keep your accounting records spotless, you're not just being organized. You're building a system that dramatically reduces overdue payments and gives you a brutally honest picture of your financial health.

Building a More Resilient Business

Ultimately, taking control of your outstanding invoices is about making your cash flow predictable. When you know when and how you’re getting paid, you can plan for the future with confidence. This stability is the bedrock of any real, sustainable growth. It means you can seize opportunities when they appear, not just when you happen to have cash in the bank.

To build a business that’s not just surviving but is ready to scale, here are a few practical next steps:

- Take a Hard Look at Your Current Process: Map out your entire invoicing and collections workflow. Where are the delays? Where do things get stuck? Pinpoint those bottlenecks and put the proactive strategies we've discussed into action.

- Embrace Modern Tools: Explore how platforms like Comfi can turn your receivables into immediate cash. By accessing the funds already tied up in your invoices, clients have been able to unlock their working capital to put right back into the business.

- Make Financial Visibility a Priority: Keep a close eye on the KPIs we covered, like DSO and your bad debt ratio. This data is your early warning system, allowing you to make smart decisions before small issues snowball into big problems.

Your accounts receivable ledger isn't just a list of money you're owed; it’s a reservoir of earned capital. The faster you can tap into it, the faster you can grow.

When you pair disciplined internal management with the right modern tools, you can turn your outstanding invoices from a constant source of stress into a catalyst for growth. The path forward is clear: get a handle on your receivables, stabilize your cash flow, and build a much stronger financial future for your company.

Answers to Your Top Questions About Outstanding Invoices

When you're running a business, managing money often brings up the same questions. Let's cut through the noise and provide clear, practical answers for handling outstanding invoices.

What’s the Difference Between an Outstanding Invoice and Bad Debt?

This is a critical distinction, as it tracks how an unpaid bill transitions from a simple delay to an actual loss for your business.

Think of it this way: an outstanding invoice is a bill you've sent that is still within its payment window. It is considered an asset on your books because you fully expect that cash to come in.

Bad debt, on the other hand, is what happens when that invoice has been ignored for so long that you've given up hope of ever collecting it. At that point, it’s no longer an asset. You must write it off as an expense, which directly reduces your profits.

So, every bad debt starts as an outstanding invoice, but with the right processes, you can ensure very few of your outstanding invoices ever reach that stage.

How Long Should I Wait Before Following Up on an Invoice?

There isn't a single magic number, but the golden rule is to be proactive. If you wait too long, you send the message that timely payment isn't a high priority for you. It’s far better to have a clear, structured timeline.

- A few days before it's due: Send a friendly, automated reminder. This one simple step can prevent a large number of late payments.

- The day after it's due: Your first real follow-up should go out. Often, a customer simply forgot, and this is all it takes to get things moving.

- Weekly check-ins: If the invoice is still unpaid after a week, it's time to follow up consistently via email and phone. Your tone can become slightly more firm, but always remain professional.

Letting an invoice sit for more than a week past its due date without any action is a recipe for a slow collection cycle.

Will Using Invoice Discounting Hurt My Customer Relationships?

This is a perfectly valid concern. The last thing you want is for your customers to think you're in financial trouble or feel like you're being aggressive by bringing in a third party.

Thankfully, with modern platforms, that’s largely a misconception.

These services are designed to be completely seamless and professional. In many situations, your customer may not even be aware you're using a discounting service because you remain their main point of contact. The arrangement is a private one between your business and the platform.

Modern invoice discounting is built to protect your client relationships. The goal is to get you the cash you need to run your business smoothly, not to change how your customers see or interact with you.

At the end of the day, these are simply tools to improve your cash flow so you can continue delivering the great service your customers expect.

Ready to stop waiting and turn your outstanding invoices into cash in the bank? Comfi offers fast, flexible ways to take back control of your cash flow. Unlock the capital tied up in your receivables and start growing your business today. See how Comfi can put your working capital back to work.

Related Reading

- A Practical Guide to Invoice Discounting in the UAE

- 8 Best Accounts Receivable Software for SMEs in 2026

- Inventory Financing vs Invoice Discounting for UAE SMEs

- What Is Accounts Receivable: Your 2026 Guide for UAE SMEs

Ready to improve your business cash flow? Get started with Comfi today.