Boost Resilience: Supply Chain Disruption Financing UAE

Your shipment hasn’t arrived. Your supplier wants payment. Your customer still expects delivery on time. Payroll, rent, customs charges, and freight bills don’t pause just because a route has slowed down.

That’s the cash flow trap many UAE SMEs are dealing with right now.

A supply chain disruption often looks like a logistics problem at first. In practice, it becomes a finance problem very quickly. Stock gets delayed, landed costs rise, invoices get paid later, and cash gets stuck in the wrong place at the wrong time. If you’re a wholesaler, distributor, dealer, or supplier, the pressure shows up in your bank balance long before it shows up in your annual accounts.

That’s why supply chain disruption financing UAE is no longer a niche topic. It’s a practical survival tool. The businesses that stay steady during disruption usually aren’t the ones with perfect forecasting. They’re the ones that can move cash faster than the disruption moves through the chain.

The New Reality for UAE Supply Chains

A Dubai SME owner orders stock as usual. The goods are ready. The buyer demand is still there. Then regional instability affects routes, carrier schedules, and delivery timing. Nothing is cancelled, but everything starts slipping.

That’s what makes these moments so difficult. The business still looks healthy on paper. Orders exist. Customers exist. Inventory exists somewhere in transit. But cash is suddenly unavailable when you need it most.

Why the UAE feels disruption quickly

The UAE sits at the centre of regional and global trade flows. That creates major opportunities, but it also means local SMEs feel external shocks quickly. A route issue, insurance change, cargo bottleneck, or customs delay elsewhere can land directly on a UAE company’s balance sheet.

The broader market is still expanding. The UAE Supply Chain Management market was valued at USD 5.22 billion in 2024 and is projected to reach USD 8.5 billion by 2031, with a 7.2% CAGR from 2025 to 2031, according to BlueWeave Consulting’s UAE supply chain management market outlook. Growth is good news, but it also means more businesses are relying on fast, connected, cash-sensitive supply chains.

Financing is now part of operations

Many SME owners still separate logistics from finance. In stable periods, that might work. In disrupted periods, it doesn’t.

If a blocked road stops your delivery van, you don’t solve it by looking only at the van. You look for another route, another vehicle, or another way to keep moving. Cash works the same way. When a disruption blocks inventory flow, you need a financial route around the blockage.

That can include:

- Invoice discounting to access cash tied up in issued invoices

- B2B Buy Now, Pay Later to help buyers keep ordering without immediate payment pressure

For a deeper overview of how these tools fit the local market, this guide to trade and supply chain finance in the UAE is a useful companion read.

Practical rule: If disruption delays goods by days or weeks, your finance process can’t take the same amount of time.

How Global Disruptions Create a Local Cash Flow Crisis

A disruption rarely arrives as one dramatic event. It usually arrives as a series of smaller blows. Freight costs rise. Capacity tightens. Goods sit longer in transit. Payment dates don’t move. Your margin gets squeezed from both sides.

That’s how a global event becomes a local cash flow crisis for a UAE SME.

The chain reaction behind the pressure

Here’s the typical pattern.

First, shipments slow down or become less predictable. Then the direct costs start stacking up. A business that expected a normal import cycle suddenly has to absorb extra transport charges, longer holding periods, and delayed sales. Meanwhile, suppliers still expect payment and staff still need to be paid on time.

The recent disruption pattern in the region shows how quickly this can happen. Oliver Wyman’s analysis of Middle East supply chain impacts notes that air cargo capacity initially dropped by 18%, while missile strikes contributed to more than 1,000 containers being stranded at a single port, with demurrage charges reaching four figures per container.

You don’t need to be directly importing through the affected route to feel this. Delays and capacity constraints travel across the network. Carriers reassign space. Timings shift. Prices reset. Stock planning becomes guesswork.

Where SME owners get caught out

Many businesses focus on whether the shipment will arrive. The bigger danger is whether the business can stay liquid while waiting.

Cash gets trapped in several places at once:

- In transit stock that has been paid for but can’t yet be sold

- Receivables from customers paying on long terms

- Higher insurance costs that reduce available operating cash

- Safety inventory held as a precaution, which ties up more funds

- Slow internal approvals that delay action even further

This is why logistics stress often turns into finance stress before owners fully realise what’s happening.

A blocked shipment doesn’t only delay revenue. It can force you to use cash reserves for expenses that were never meant to be funded that way.

High-risk sectors tend to share the same traits

Some sectors are more exposed because they depend on timely imports, thin margins, or fast stock rotation.

Common examples include:

- Automotive parts and vehicle distribution because inventory values are high and replacement timing matters

- Electronics distribution because products are often imported, time-sensitive, and margin-sensitive

- Fast-moving consumer goods because delays can disrupt replenishment and shelf availability

- Food and beverage supply chains because timing and continuity matter more than perfect pricing

- Healthcare-related distribution because shortages can create both operational and cash pressure

These sectors aren’t risky because they’re poorly run. They’re risky because disruption hits their operating model directly.

When freight gets slower and more expensive, the primary issue isn’t just delivery. It’s whether your cash cycle can survive the delay.

A lot of SME owners only review financing after the pressure becomes painful. That’s late. During volatile periods, your liquidity plan should sit beside your purchasing plan.

If you want a practical foundation for tightening collections, timing payments better, and smoothing inflows, this guide on how to improve cash flow helps frame the basics.

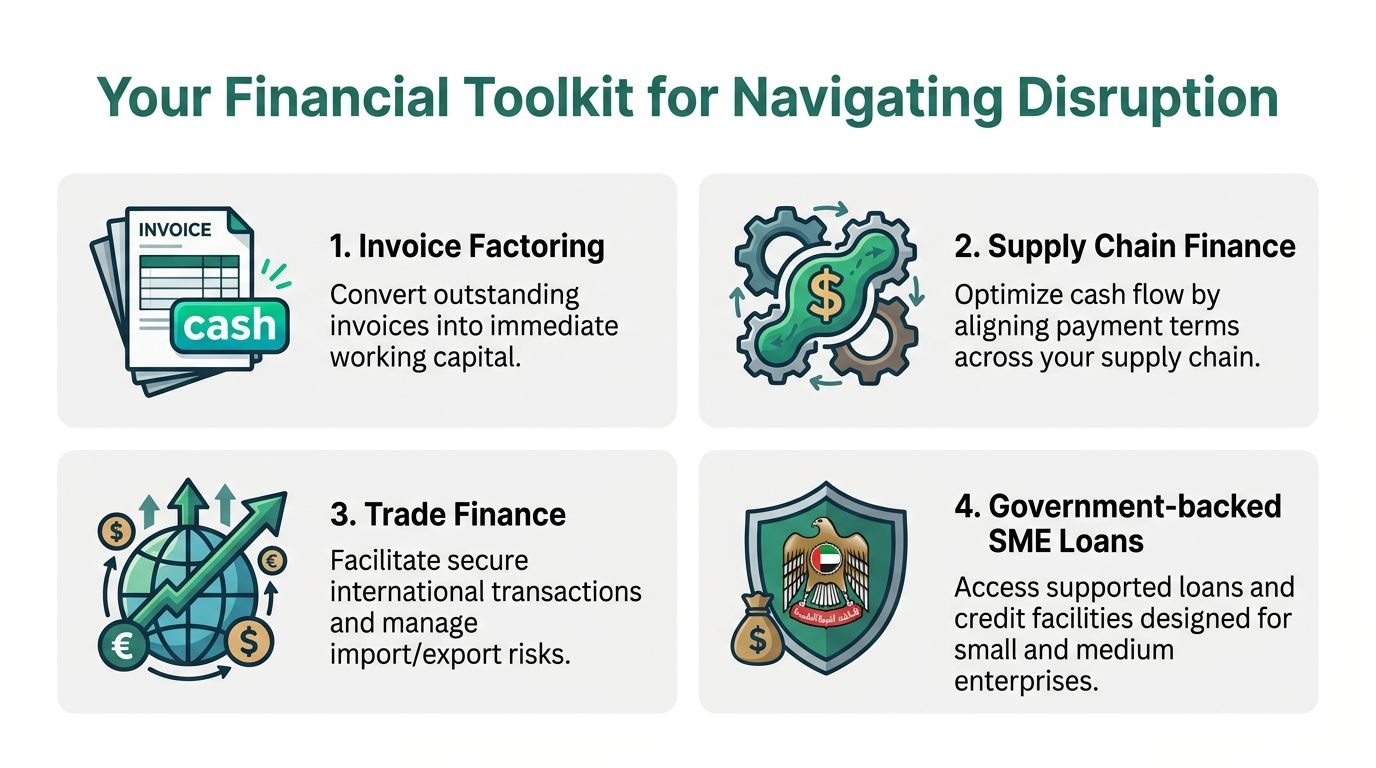

Your Financial Toolkit for Navigating Disruption

Once disruption starts, most SMEs ask the same question. “What can I do this week?”

The right answer usually isn’t one giant facility or one perfect product. It’s a toolkit. Different cash flow problems need different instruments.

Invoice discounting

If you’ve already delivered goods or completed a service and issued an invoice, that invoice represents money you’ve earned but haven’t received yet.

Invoice discounting is the simplest tool to understand. It works a bit like accessing part of your salary before payday. The work is done. The payment is due. You just need the cash sooner.

This matters in the UAE because many SMEs don’t deal with a single large buyer. Many manage fragmented payment flows across 5 to 50 concurrent buyers with different terms, according to Finverity’s analysis of the UAE supply chain finance market. That creates a portfolio problem, not just a collection problem.

A useful way to think about invoice discounting:

- Best for businesses with issued invoices and delayed customer payment terms

- Useful when stock has arrived, sales have happened, but cash is still sitting in receivables

- Less useful when the issue is pre-shipment purchasing rather than post-sale collections

B2B Buy Now, Pay Later

Some disruptions don’t stop demand. They stop your buyers’ ability to pay immediately.

B2B Buy Now, Pay Later helps by letting a buyer purchase now and settle on agreed terms later. For the seller, this can reduce friction at the point of sale and help maintain order volume during uncertain periods.

This is especially useful when your buyers are also under pressure. A distributor may still want to place the order, but hesitate because freight volatility or delayed downstream collections have made cash tight. Flexible terms can keep the transaction moving.

B2B BNPL works well for:

- Wholesale and distribution where repeat orders matter

- B2B ecommerce where checkout friction reduces conversion

- Business sellers that want to offer terms without building a large collections operation internally

Trade finance and supply chain finance tools

These are broader categories, and they often confuse SME owners because the labels sound more complex than the actual use cases.

In plain terms:

- Trade finance helps businesses manage import and export transactions more securely and smoothly

- Supply chain finance helps align payment timing across buyers and suppliers so one side isn’t carrying all the strain

The main value during disruption is coordination. If suppliers need faster payment while buyers want longer terms, digital supply chain tools can bridge that timing mismatch better than email chains and manual spreadsheets.

This is one area where wider financial services digital transformation really matters. Faster onboarding, cleaner data flows, and system integration aren’t nice extras. They determine whether a finance tool is usable during a live disruption or too slow to help.

Dealer financing for automotive industry

For vehicle dealers, the problem often isn’t a lack of demand. It’s that too much cash is parked in stock already sitting on the floor.

Dealer financing structures help release cash from vehicles already in the showroom. The business doesn’t need to wait for every current unit to sell before acting on the next opportunity. That improves stock rotation and reduces the feeling of being trapped by inventory.

Why digital-first matters more than the product label

Many owners spend too much time comparing product names and too little time comparing execution.

When disruption is active, the winning features are often operational:

- Paperless onboarding so the process starts quickly

- Instant or fast eligibility checks so you know where you stand

- Dashboard visibility across invoices, buyers, and status

- System integration with accounting or ERP tools

- Clear turnaround times instead of open-ended approvals

A digital option won’t solve a weak business model. But it can remove the drag caused by manual processing, fragmented communication, and slow approvals.

For a grounded look at how invoice-based tools work in the local market, this explainer on invoice discounting in the UAE is worth reading.

The most useful finance tool during disruption is the one that matches the exact point where your cash gets stuck.

Choosing the Right Digital Solution for Your Business

Not every business needs the same type of support. A distributor waiting on customer payments has a different problem from a dealer holding expensive stock. A wholesaler trying to preserve order volume has a different need from an importer trying to cover a timing gap.

That’s why choosing well matters.

Start with the cash flow blockage

Before comparing providers, define the blockage clearly.

Ask yourself:

- Receivables problem. Have you already invoiced, but payment is coming too late?

- Buyer conversion problem. Are customers delaying purchases because they need more flexible terms?

- Inventory lock-up problem. Is too much cash trapped in stock that hasn’t sold yet?

- Import timing problem. Are costs landing before revenue arrives?

The answer will usually point you toward invoice discounting, B2B BNPL, dealer financing, or a broader supply chain finance setup.

Compare digital options by operating reality

The pressure on routes and freight has made efficiency more important than ever. Tive’s review of Middle East supply chain risks notes that VLCC charter rates on the Middle East to China route nearly doubled to over $400,000 per day, while overall freight rates surged by more than 4.5x year-to-date. When transport costs move like that, the cost and speed of your financing choice become strategic, not administrative.

Use these criteria.

Speed of access

This is often the first filter.

- Traditional bank processes can suit planned, slower-moving funding needs where documentation is already organised.

- Digital fintech platforms are often better for urgent liquidity decisions, especially when delays are unfolding in real time.

If your stock issue is today’s problem, a long approval journey can be as unhelpful as no solution at all.

Documentation burden

Some businesses can support heavier document requests. Others can’t spare the time.

Look for:

- Paperless application flow

- Simple invoice or transaction upload

- Clear eligibility checks early in the process

- Minimal back-and-forth for routine cases

If your finance manager has to chase ten missing documents before even knowing whether you qualify, that process may create more stress than relief.

Cost structure

Don’t just ask whether a solution is “cheap”. Ask whether it is predictable and proportionate to the value it creates.

Good questions include:

- Is the pricing easy to understand?

- Does the cost fit the urgency of the problem being solved?

- Will it protect margin by preventing a larger disruption cost?

Sometimes a faster digital option is worth more because it prevents a missed sale, supplier strain, or delayed restock.

Integration and control

A useful digital tool should fit your workflow, not force your team into a second manual process.

Consider whether it can:

- Connect with your accounting or ERP setup

- Give your team one dashboard for visibility

- Handle multiple buyer relationships cleanly

- Scale as order volume changes

If your business deals with many buyers and mixed payment terms, visibility becomes as important as funding itself.

Choose the tool that removes friction from your actual bottleneck, not the one with the most impressive label.

High-risk sectors should be extra selective

If you operate in a high-risk category such as automotive, electronics, FMCG, or parts distribution, your timing exposure is higher. That means your tolerance for slow onboarding, vague pricing, or poor platform visibility should be lower.

In those sectors, the right digital solution usually has three traits. It moves quickly, it handles repeat transactions well, and it gives the finance team confidence about what happens next.

How to Secure an Advance on Your Invoices

For many SMEs, invoice-based funding is the fastest route to breathing room because it starts with value you’ve already created. You’ve delivered the goods. You’ve issued the invoice. You’re waiting to be paid.

The process is usually more straightforward than owners expect.

Step 1 Identify the gap, not just the stress

Start by naming the exact cash gap.

Is the problem payroll next week, supplier payment this month, customs clearance, or the ability to reorder fast-moving stock? Defining this is important, as you don’t need to submit every invoice. You need to select the invoices that best solve the pressure point.

Choose invoices that are clear, issued, and tied to completed delivery or accepted work.

Step 2 Use a digital platform with paperless onboarding

A modern platform should let you begin without printing forms, scheduling multiple branch visits, or rebuilding your financial history from scratch.

Look for a process that asks for core business details, supporting documents, and invoice data in a digital flow. If you’re busy managing operations, speed and clarity matter more than fancy terminology.

Step 3 Upload invoices or connect your system

Some businesses prefer manual upload. Others want system integration.

Either can work. What matters is that the invoice information is accurate and easy for the platform to assess. If your business issues many invoices across several customers, integration can save time and reduce errors.

Step 4 Review eligibility and the offer carefully

You should know quickly whether the invoice is eligible and what the commercial terms look like.

Read the details with a practical eye:

- Funding timing matters

- Customer or invoice criteria matter

- Process after approval matters

- Repayment or settlement mechanics matter

If the provider can’t explain these clearly, pause.

Step 5 Use the funds for movement, not drift

Once cash lands, treat it as a tool for restoring flow.

That may mean:

- Paying a supplier to release stock

- Covering an import-related timing gap

- Restocking a fast-selling line

- Preserving payroll and operating continuity

- Avoiding expensive delays elsewhere in the chain

The biggest mistake is using quick-access funds without linking them to a specific operational outcome.

Step 6 Repeat only when it fits your cycle

Invoice-based funding works best when it supports a repeatable pattern, not panic borrowing behaviour.

If your business regularly sells on terms, this can become part of your cash flow rhythm. If the issue is more occasional, use it selectively around known bottlenecks such as seasonal stock build-up, route volatility, or slower-paying customers.

Good invoice funding should feel like a clean operational workflow, not a rescue mission.

Real-World Examples from UAE SMEs

The mechanics are easier to understand through real business situations. These examples are fictional, but they reflect the kinds of pressure UAE SMEs face every day.

Electronics distributor in Jebel Ali

An electronics distributor sells to multiple retail buyers across the UAE. Demand is steady, but customer terms vary widely. Some buyers pay faster. Others take much longer. At the same time, imported stock has become less predictable.

The company’s problem isn’t a lack of sales. It’s fragmented cash timing.

When one shipment arrives late, the business still has to pay operating expenses and prepare for the next order cycle. Invoice discounting helps the distributor turn selected issued invoices into immediate liquidity instead of waiting for every buyer to settle on their own schedule.

That gives the company room to keep stock moving without pushing supplier relationships to breaking point.

Automotive dealer in Al Quoz

An auto dealer has several vehicles in stock, but too much cash is tied up in that inventory. This isn’t unusual. In the automotive trade, capital can be tied up in stock for up to 180 days, and holding more safety inventory across locations after disruption makes the cash strain even sharper, as discussed in GTR’s Middle East and Africa disruption roundtable.

The dealer spots an opportunity to acquire in-demand vehicles, but can’t move quickly because too much money is parked in existing units.

A dealer financing structure helps make cash available from vehicles already in the showroom. The business doesn’t need to wait for every current unit to sell before acting on the next opportunity. That improves stock rotation and reduces the feeling of being trapped by inventory.

FMCG wholesaler serving regional buyers

A wholesaler serving food and household goods buyers faces another kind of stress. Customers still want product, but many ask for more flexibility on payment timing because their own downstream cash collections have become uneven.

If the wholesaler says no to terms, some orders may shrink or disappear. If it says yes without a proper structure, the business may take on too much cash risk.

B2B BNPL gives the wholesaler a way to keep orders moving while preserving cleaner cash flow. The sales team can support buyers without turning every transaction into an internal credit decision.

What these examples have in common

These businesses are in different sectors, but the pattern is the same:

- The disruption begins in operations

- The pain appears in cash flow

- The solution works best when it matches the blockage

- Digital tools matter because timing matters

None of these businesses need vague resilience language. They need practical options that help them keep buying, selling, and collecting while conditions stay uneven.

Building a Financially Resilient Business

Disruption isn’t a temporary side issue anymore. For many UAE SMEs, it’s part of the operating environment.

That changes how a smart business thinks about finance. The goal isn’t only to survive the next delay. It’s to build a company that can keep functioning when routes shift, lead times stretch, and buyers start asking for more flexibility.

Resilience starts with financial agility

Operational resilience gets a lot of attention. Supplier diversification, buffer stock, alternate routes, and better forecasting all matter.

But without financial agility, those plans can stall. You may know exactly what to do operationally and still be unable to act because the cash is trapped in invoices, inventory, or slow customer payments.

That’s why digital funding tools are best treated as part of normal operating design, not emergency-only fixes.

A practical resilience mindset

A resilient SME usually does a few things well:

- Maps its cash bottlenecks before they become crises

- Chooses digital tools in advance rather than under pressure

- Matches the product to the problem instead of using one tool for everything

- Reviews payment terms actively across buyers and suppliers

- Keeps finance close to operations so purchasing and liquidity decisions support each other

If you want a broader owner-level perspective beyond finance alone, these strategies for building a resilient business are a helpful complement.

The key message is simple. You can’t control geopolitical shocks. You can control how quickly your business responds when cash gets squeezed.

The SMEs that stay steady aren’t always the biggest. They’re often the ones that prepared a faster financial route around the blockage.

If your business needs a faster way to make cash available from invoices, offer flexible B2B payment terms, or free up funds tied in automotive inventory, Comfi offers digital tools built for UAE and MENA SMEs. The platform supports invoice discounting, Buy Now Pay Later, and dealer financing through a paperless workflow, helping businesses access funds quickly and keep sales moving during disruption.

Related Reading

- What Is Trade Finance and How Does It Work for SMEs

- A Guide to Trade Credit for Modern MENA Businesses

- What Is Trade Finance and How Does It Work for SMEs

- What is Trade Credit: A Practical Guide to Boost Cash Flow

Looking to improve your cash flow? Explore Comfi's Invoice Discounting solutions. Get started today.