A Practical Guide to Managing Bad Debt and Cash Flow

In business, not all money owed to you is created equal. Some of it, unfortunately, is destined to disappear. This is known as bad debt, an uncollectible payment owed to your business, officially written off as a loss after all reasonable collection efforts have failed. It's a promised payment that never arrives, taking a direct hit on your bottom line.

What Bad Debt Really Means for Your Business

For any small or medium-sized enterprise (SME), an invoice isn't just a piece of paper; it’s the cash you're counting on to run the show. When that invoice becomes uncollectible, it flips from being a valuable asset on your balance sheet to a painful liability. This isn't just about lower profits. It actively drains resources from your company.

Think of your business like a chain. Every expected payment is a critical link holding things together. A single unpaid invoice is like a link snapping. Suddenly, the entire flow of cash can grind to a halt, causing disruptions for everything that follows.

For a growing business in the UAE, this kind of disruption has real, tangible consequences that can snowball fast.

The Real-World Impact on SMEs

The ripple effects of bad debt are serious and they spread quickly. What starts with one missed payment can set off a chain reaction of financial headaches that can stifle growth and threaten the stability you've worked so hard to build. For many SMEs, this means the day-to-day essentials become a struggle.

When unpaid invoices choke your cash flow, you’ll find it much harder to handle the basics:

- Meeting Payroll: Paying your team on time becomes a major source of stress. This can crush morale and you risk losing your best people.

- Paying Suppliers: Good supplier relationships are everything. Bad debt can force you to pay them late, damaging your reputation and putting your own supply chain at risk.

- Covering Operating Costs: The essentials like rent, utilities, and marketing suddenly become difficult to manage, putting a huge strain on your daily operations.

- Missing Growth Opportunities: You might have to say no to new contracts, put expansion plans on hold, or delay buying new inventory, all because the cash you need is locked up in invoices you can't collect.

Distinguishing Bad Debt from Doubtful Debt

To maintain accurate financial records, it is crucial to understand the difference between bad debt and doubtful debt. They sound similar, but they represent two very different stages in the lifecycle of an overdue payment.

A doubtful debt is an invoice that's overdue, and you have a good reason to suspect it might not get paid. Perhaps the customer is consistently late or you've heard they're facing financial trouble. At this point, there’s still a chance you’ll receive the money, but the risk has increased.

Bad debt, on the other hand, is the final stage. It’s an amount you are now almost certain you will never collect. This could be because a customer went bankrupt, can no longer be contacted, or you've exhausted every collection attempt over a long period.

This isn't just accounting jargon. Correctly classifying these debts gives you a realistic picture of your company's financial health. Moving an account from doubtful to bad debt is an admission that the money is gone. It allows you to clean up your books and make smarter strategic decisions based on the actual cash you have, not the cash you hope to have.

How Bad Debt Silently Damages Your Financial Health

The real danger of bad debt isn’t just the final loss; it’s the quiet, corrosive damage it does long before you officially write it off. On paper, your accounts receivable might look fantastic, showing strong sales and healthy revenue growth. But if those invoices are never actually paid, that revenue is a phantom, painting a dangerously misleading picture of your company’s financial stability.

This gap between what your books say you’ve earned and the cash that’s actually in the bank is where poor business decisions are often made. You might invest in new stock, hire more staff, or launch a new product line based on profits that don't really exist. When that cash fails to materialize, the fallout can be severe, freezing operations and straining relationships with your own suppliers.

Dealing with this discrepancy demands a clear accounting strategy. There are two main ways to account for bad debt, and your choice directly impacts how accurately your financial statements reflect reality.

Choosing Your Accounting Method

How you record bad debt is a critical decision. One approach offers simplicity, while the other provides a much more honest—and proactive—view of your company's financial health.

- The Direct Write-Off Method: This is the straightforward approach. You wait until you're absolutely certain an invoice is a lost cause, then you directly record it as a bad debt expense. While it’s easy, its major flaw is that it violates the matching principle of accounting. You end up recognizing the expense in a different period from the revenue, which can seriously distort your profitability reports.

- The Allowance Method: This is the preferred and far more realistic method under Generally Accepted Accounting Principles (GAAP). Instead of waiting for a client to default, you proactively estimate and set aside an "allowance for doubtful accounts" based on historical data and current economic conditions. This creates a buffer, matching potential bad debt expenses to the same period the revenue was earned.

The allowance method gives you a much truer picture of your net realizable receivables—the actual amount of cash you can realistically expect to collect. To get a handle on how bad debt eats into your bottom line, it’s worth using a robust Profit and Loss Analyzer to keep a close watch on your financial health.

By anticipating potential losses, the allowance method prevents the sudden financial shock of a large write-off. It’s a strategic move that acknowledges the inherent risk in credit sales and prepares the business for it.

From Paper Profits to Real-World Problems

Let's walk through how this plays out in the real world. Imagine a mid-sized electronics distributor in Dubai that lands a huge order from a new retail client. The sale is worth AED 300,000, and the invoice is sent with 60-day payment terms.

On the books, the distributor immediately records this as revenue. The profit and loss statement looks amazing. Based on this rosy picture, the finance manager approves a large inventory purchase from an overseas supplier to meet expected demand.

But then the 60-day mark passes with no payment. The distributor’s team follows up, but the retailer has gone radio silent. At 90 days, it’s painfully clear the money isn't coming. The distributor is now forced to classify the AED 300,000 as bad debt.

The damage, however, is already done:

- Frozen Working Capital: The cash they were counting on was earmarked to pay for the new inventory. Now, the distributor can't pay its own supplier, badly damaging a crucial business relationship.

- Inflated Performance: The company made strategic decisions based on revenue that never existed, triggering a full-blown cash flow crisis.

- Operational Halt: Without cash to pay suppliers, the distributor can't get new products. This brings sales operations to a grinding halt, hurting their ability to serve other, more reliable customers.

This kind of scenario is all too common in the region. The UAE has a non-performing loans (NPL) rate that highlights these challenges. As of 2022, the UAE's NPL ratio was 6.55%, which sits above the world average of 5.49%. This elevated level of bad debt in the financial system makes it tougher for SMEs to get traditional support, as financial institutions become more cautious. This makes proactive bad debt management not just good practice, but absolutely essential for survival.

Proactive Strategies to Prevent Bad Debt

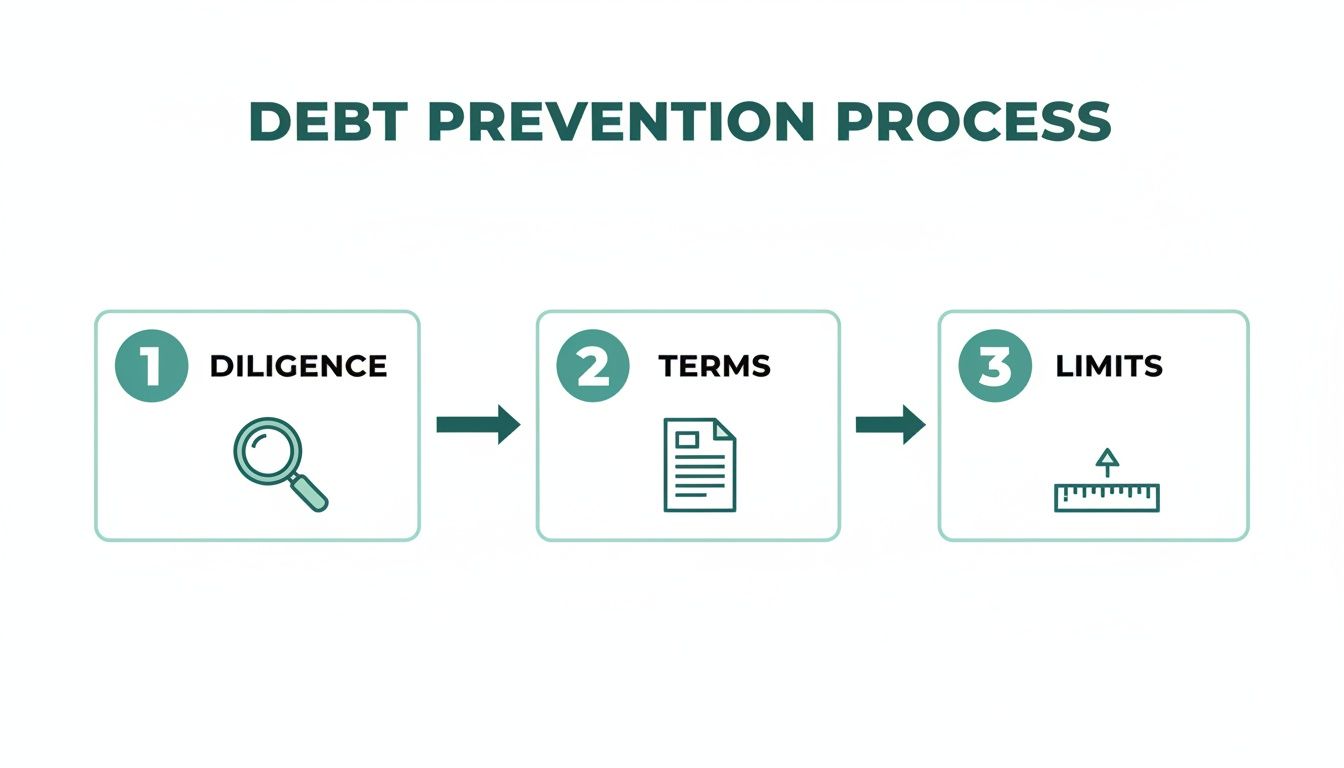

The most effective way to deal with bad debt is to prevent it from happening in the first place. While you can't eliminate the risk completely, taking a proactive stance will drastically lower the chances of an invoice becoming a write-off. It’s all about building a strong defense system that kicks in long before a payment is even late.

By putting a few smart strategies in place, you can shield your cash flow and attract a more reliable customer base. It's about being selective, crystal clear, and vigilant from day one. These practices don't have to slow you down; instead, they blend right into your operations, creating a more financially secure business.

Perform Smart Customer Due Diligence

Before you even think about extending credit to a new customer, you must know who you’re dealing with. A quick but solid due diligence process can save you a world of financial pain down the road. This isn’t about being suspicious; it’s about making smart business decisions.

Your goal is to get a clear picture of a potential client's financial stability and payment history. You can start by:

- Checking Trade References: Ask for references from other suppliers they’ve worked with. A quick phone call or email can tell you a lot about their payment habits.

- Reviewing Credit Reports: For larger contracts, it’s worth using a reputable credit reporting agency in the UAE to get a proper look at their creditworthiness.

- Analyzing Their Digital Footprint: Check out their company website, social media pages, and any online reviews. A professional, active online presence is usually a good sign.

This initial screening helps you spot potential red flags before you’re locked into a business relationship, letting you sidestep high-risk accounts from the get-go.

Establish Crystal-Clear Payment Terms

Ambiguity is the enemy of getting paid on time. If your payment terms are buried in the fine print or are confusing, you’re practically asking for delays and disputes. Your terms need to be simple, communicated clearly, and agreed upon before any work starts or goods are delivered.

Every invoice should be a clear, concise instruction manual for payment. It must explicitly state the total amount due, the due date, and the accepted payment methods. This removes any guesswork for the client.

On top of that, make sure your policy for late payments is spelled out directly in your service agreement. Be upfront about any late fees or interest that will be charged on overdue invoices. Setting clear consequences from the beginning shows you’re serious about timely payments. If your business is struggling with chaotic payment cycles, you can learn more about how an automated invoice system can enforce these terms and bring stability to your cash flow.

Set Sensible Credit Limits

Not every customer should get the same line of credit. A classic mistake that leads straight to bad debt is extending too much credit to a brand-new or unproven client. The smarter move is to use a tiered system for credit limits that’s based on risk.

Start new customers off with a lower, more conservative credit limit. As they build a solid track record of paying you on time, every time, you can gradually increase that limit. This approach lets you build trust while keeping your initial financial exposure to a minimum.

You should also review these limits regularly, especially for your biggest accounts. If a customer is constantly bumping up against their limit or their payment behavior suddenly changes, it might be time to rethink their terms. This dynamic approach to credit management helps you adapt to changing situations and protect your business. Using automations for overdue payments can also be a huge help in keeping your cash flow healthy.

A Step-by-Step Guide to Recovering Overdue Payments

When a payment deadline passes, it’s tempting to either panic or ignore it. Both are mistakes. Reacting without a clear plan can burn bridges with good customers, and doing nothing just hurts your cash flow. The most effective approach is a structured, professional process that escalates calmly and logically.

This isn’t just about demanding money; it's about understanding why a payment is late and preserving the relationship when you can. A consistent, prompt follow-up process shows you’re serious about your finances and sets clear expectations for the future.

Of course, the best way to handle overdue payments is to prevent them from happening in the first place. This process kicks in after your first lines of defense—proper diligence, clear terms, and sensible credit limits—have been established.

Think of these preventative steps as the foundation. What follows is the playbook for when a crack appears.

Phase 1: The Gentle Nudge (1-30 Days Overdue)

The second an invoice ticks past its due date, your system should kick in. Don’t wait. The first phase is all about friendly, professional reminders. The reality is, most late payments are simple oversights, not a refusal to pay.

Start with automated, low-touch communication. A polite email or a system-generated SMS is often all it takes to jog a customer's memory without creating any awkwardness.

- Action 1 (1-7 Days Overdue): Send a friendly automated email. The tone should be helpful ("Just a quick reminder...") and assume it was an honest mistake.

- Action 2 (15 Days Overdue): If you haven't heard back, it's time for a slightly more direct follow-up. Send another email and make a quick, courteous phone call to confirm they received the invoice and see if there are any issues.

- Action 3 (30 Days Overdue): At the one-month mark, a senior team member, like an accounts manager, should make contact via both phone and email. The goal now is to get a clear answer: is there a problem holding up payment?

Throughout this entire phase, document everything. Log every email sent, every call made, and a note about every conversation. This paper trail is invaluable if things need to escalate later.

Phase 2: Direct and Clear Escalation (31-60 Days Overdue)

If the gentle nudges are ignored, it’s time to dial up the urgency while staying completely professional. The conversation shifts from a simple reminder to a direct request for payment.

This is the critical point where you need to clearly reference the consequences of non-payment you laid out in your initial terms and conditions, like late fees. Following through on your own policies is the only way customers will take them seriously.

Now is the time for a more formal letter or email that summarizes all your previous attempts to get in touch and clearly states the outstanding balance. A call from someone more senior, like a finance manager, also adds weight and signals that this is becoming a serious issue.

This direct approach is often what it takes to get a response. And remember, every day an invoice goes unpaid, it impacts your own finances. Keeping a close eye on your collection timeline is key, and you can learn more about how to reduce your Days Sales Outstanding (DSO) to get a better handle on your overall cash flow.

Phase 3: Final Demands and Calling for Backup (61+ Days Overdue)

Once an invoice is more than two months late, the chances of you collecting that money on your own start to drop off a cliff. Your focus has to shift from polite follow-ups to decisive action. It’s time for a final demand and to seriously consider bringing in outside help.

Your next step is to send a formal "Letter of Demand." This isn’t just another email. It’s a formal document that lays out the total amount due, gives one final, firm deadline for payment, and explains what will happen next if that deadline is missed. This could mean involving a collection agency or seeking legal advice.

At this stage, you have to make a tough call and weigh the costs versus the benefits of taking further action:

- Collection Agencies: In the UAE, there are reputable agencies that can take over the collection process for you. They usually work on commission, taking a cut of whatever they recover. This can be effective, but it almost always means the business relationship is over.

- Legal Action: For larger debts, a consultation with a legal expert is a must. They can tell you if it’s worth pursuing the debt through the courts, but be prepared for a process that can be both long and expensive.

Engaging a third party is a major step. It should be reserved for those situations where you’ve tried everything else and the size of the debt justifies the extra cost and finality of the decision.

To give this structure, here is a simple escalation plan you can adapt.

Bad Debt Recovery Escalation Plan

This timeline provides a clear path for escalating collection efforts, helping you stay systematic while balancing the need to get paid with the desire to maintain customer relationships.

Here are the recommended actions based on how overdue an invoice is:

- 1-7 Days Overdue: Send an initial automated reminder via email or SMS. The goal is a gentle nudge, assuming an oversight.

- 15 Days Overdue: Send a second reminder and make a brief follow-up call. The goal is to make personal contact and confirm invoice receipt.

- 30 Days Overdue: Have a senior staff member follow-up by phone and email. The goal is to understand the root cause of the delay.

- 45 Days Overdue: Send a formal letter stating the overdue status and applying late fees as per your terms. This increases urgency.

- 60 Days Overdue: Send a final Letter of Demand with a firm payment deadline, stating the final terms before third-party involvement.

- 75+ Days Overdue: Review the case internally to decide on the cost-effectiveness of handing it off to a collection agency or legal counsel.

Having a clear, documented plan like this takes the emotion out of the process. It ensures every overdue account is handled consistently and professionally, maximizing your chances of recovery while protecting your business.

Using Fintech to Secure Cash Flow and Reduce Risk

Chasing down overdue payments feels like a grim, unavoidable part of running a business. The traditional cycle involves long waits, endless follow-up emails, and a mountain of administrative stress. But modern financial technology offers a much smarter way forward, with tools designed to tackle the root cause of the problem: the painful delay between doing the work and getting the cash.

These solutions are built to disconnect your service delivery from your cash flow. Instead of holding your breath for 30, 60, or even 90 days, you can tap into the value of your invoices almost instantly. This isn't just a small tweak; it's a fundamental shift in how you manage your finances, turning unpredictable receivables into reliable cash flow you can access on demand.

By bringing these tools into your business, you're not just getting paid faster—you're building a more resilient, agile operation. It’s a proactive strategy that shields you from the crippling domino effect of bad debt and late payments.

Unlocking Your Capital with Invoice Discounting

One of the most direct ways to shut down bad debt risk is through invoice discounting. Think of it as hitting the fast-forward button on your payments. Instead of waiting for your customer’s payment cycle to crawl to a finish, you can submit your approved invoices to a fintech platform and get a huge chunk of their value upfront, often within 24 hours.

This simple move solves the cash flow gaps that leave your business vulnerable. Those long waiting periods—where you're exposed to the risk of a customer defaulting—are completely wiped out. You get the money you've earned right when you need it, empowering you to pay your own suppliers, cover payroll, and jump on growth opportunities. With this approach, many clients find they are able to unlock their working capital.

By converting your accounts receivable into immediate cash, invoice discounting ensures your business runs on actual funds, not on promises. It is a strategic move that directly reduces your exposure to potential bad debt by shortening the collection cycle to a single day.

This approach also adds a vital layer of security. The headache of actually collecting the payment from your customer often shifts to the fintech platform, lifting a massive administrative burden off your team. This frees you up to focus on what you're actually good at: running and growing your business.

Streamlining B2B Payments for Mutual Growth

Beyond just speeding up your own payments, fintech platforms are redesigning the entire B2B transaction landscape. Solutions from companies like Comfi create a win-win for both suppliers and their buyers, building healthier business relationships while cutting risk for everyone involved.

Here’s a practical look at how it works:

- Suppliers Get Paid Instantly: As the supplier, you get paid for your goods or services immediately by the platform. This completely removes the risk of late payments or defaults, shielding you from bad debt.

- Buyers Receive Flexible Terms: Your customer gets flexible payment terms (like 30, 60, or 90 days) from the platform. This lets them manage their own cash flow without holding up your money.

This model gives you the confidence to chase bigger sales and take on larger orders without the fear of wrecking your own finances. When clients know they can get better payment terms by working with you through a platform like Comfi, it can drive a serious sales uplift—some businesses report increases of up to 30%. You secure your operations and build stronger customer loyalty at the same time.

The Practical Benefits of a Fintech Partnership

Bringing these payment solutions into your business gives you more than just quick cash. It delivers a strategic edge that strengthens your entire financial foundation and positions you for real, sustainable growth. The benefits go far beyond just dodging bad debt.

A modern payments platform helps you nail several key goals:

- Improved Cash Flow Predictability: When funds arrive quickly and consistently, your financial planning becomes far more accurate. You can create budgets with confidence, knowing exactly when your cash will hit the bank.

- Reduced Administrative Overhead: Your team can finally stop wasting countless hours chasing invoices. The platform handles the collections, freeing up your people for more valuable work.

- Stronger Supplier Relationships: By making sure you can always pay your own suppliers on time, you earn a reputation as a reliable partner, which can unlock better terms and stronger partnerships for you.

- Accelerated Business Growth: With reliable cash flow, you can invest in more inventory, launch new marketing campaigns, or expand into new markets without waiting for customer payments to slowly trickle in.

Ultimately, using fintech to manage your B2B payments is a proactive way to de-risk your business. It transforms the uncertain and often stressful process of managing receivables into a predictable, secure, and efficient part of your operation. It turns bad debt into a problem you prevent, not one you have to recover from.

Understanding the UAE Debt Landscape

Think of the UAE’s fiscal health as the bedrock beneath your business. When the government keeps its own debt in check, it ripples out confidence across the market—making capital more available and commercial activity more predictable.

That sturdy backdrop matters for SMEs. It means you can plan investments, manage receivables and work with modern payment solutions without fearing sudden policy shifts or funding crunches.

Dubai’s Progress And Market Stability

Dubai offers a striking illustration of this principle in action. By tackling its public debt head-on, the emirate has reduced gross government debt from about 70% of GDP in 2021 to roughly 38% at the close of 2023, according to S&P Global. That’s a dramatic turnaround—one that underscores a commitment to easing fiscal pressures over the long haul.

For the full breakdown, visit the official DMO profile: https://dmo.dof.gov.ae/en/debt-profile/.

This drop in public debt isn’t just a statistic; it’s a signpost pointing to a more reliable, business-friendly environment.

As an SME leader, you gain real advantages from this stability:

- Sharper cash-flow forecasts, since you’re not bracing for abrupt rate hikes.

- Better access to capital, thanks to a market with lower perceived risk.

- Reduced default risk, when your customers operate in a healthier economy.

It also explains why solutions like invoice discounting services available in the UAE are so effective. They plug into a fundamentally sound economy, offering a dependable safety net when you need to improve cash flow. By aligning your internal credit controls with these broader economic trends, you’re setting the stage for steady, sustainable growth.

Bad Debt: Your Questions Answered

When you're dealing with overdue payments, a lot of questions pop up. Knowing the answers helps you make smart decisions that protect your company’s bottom line. Here are the most common things business owners and finance teams ask about handling bad debt.

When Is the Right Time to Write Off a Debt?

Deciding to write off a debt isn't giving up; it’s a calculated accounting move. It should only happen after you’ve tried every reasonable way to collect. Typically, this is when an invoice is 90 to 120 days overdue and your follow-ups have gone unanswered.

The one exception? If you get concrete news that a customer has gone bankrupt, write off the debt immediately. The key is to have a consistent internal policy so your financial records stay clean and accurate. This is where using the allowance method for accounting really pays off, as it helps you plan for these losses before they happen.

A bad debt write-off isn't a surrender. It's a strategic accounting move to clean up your balance sheet and reflect a more realistic financial position. You're simply acknowledging that chasing the debt any further would cost more than it's worth.

Can I Still Recover a Debt After Writing It Off?

Absolutely. It’s a great outcome when a customer pays an invoice you’ve already written off your books. In accounting, this is called a bad debt recovery, and you need to record it properly to keep your financial statements accurate.

To account for it, you first reverse the original write-off entry. Then, you record the cash payment just like any other. This makes sure your revenue and expense records for the period are correct and reflect the unexpected win.

How Does Invoice Discounting Help with Slow-Paying Customers?

Invoice discounting is a direct solution to the cash flow crunch caused by customers who drag their feet on payments. Instead of waiting around and worrying if the money will ever come, you can use a fintech platform to unlock the cash tied up in those outstanding invoices.

Here’s how it helps you sidestep the risk of bad debt:

- Get Your Cash Now: You submit your approved invoices and get a huge chunk of their value almost instantly, often within 24 hours.

- Shift the Risk: The platform takes on the job of collecting from your customer. This lifts the administrative headache and the collection risk right off your team’s shoulders.

- Create Predictable Cash Flow: This gives your business a steady stream of cash it needs to pay suppliers, cover payroll, and invest in growth—without being held hostage by your customers' payment habits.

It’s a proactive strategy that turns your unpredictable accounts receivable into a reliable source of cash, shielding your operations from the damage of slow payers and potential bad debt.

By transforming your receivables into predictable cash flow, Comfi helps you secure your operations and focus on growth. Discover how you can eliminate payment delays and de-risk your business at https://comfi.ai.

Related Reading

- How Can MENA SMEs Master Working Capital?

- Staffing Agency Payroll Financing UAE: Boost Cash Flow 2026

- SME Cash Flow Management: A Guide for MENA Businesses

- Improve Working Capital for UAE IT Services Business

Looking to improve your cash flow? Explore Comfi's Invoice Discounting solutions. Get started today.