DIFC Company Working Capital: Unlock Cash Flow 2026

Your sales are up. New customers are coming in. More stock is moving. Yet the finance team is watching cash get tighter, not looser.

That’s a common DIFC growth problem. A company can look healthy on paper and still feel squeezed day to day because cash is stuck between supplier payments, customer collections, and inventory that hasn’t converted back into bank balance yet. For operational businesses in DIFC, especially traders, distributors, and service-led SMEs, the issue usually isn’t profitability. It’s timing.

Traditional bank facilities can help in some cases, but they often move too slowly for businesses that need to pay now and collect later. That’s why practical DIFC company working capital strategy has shifted towards tools that release cash from actual trading activity instead of forcing every problem into a classic lending structure.

The Growth Paradox for DIFC Companies

DIFC is expanding fast, and that’s good news until growth starts consuming cash faster than the business collects it.

By the end of 2025, DIFC reached 8,844 active companies, up 28% year on year, according to the DIFC annual performance report summary. The same source notes a broader regional problem identified by PwC. Listed firms had $27.8 billion trapped in excess working capital, while Net Working Capital days deteriorated annually.

Growth creates pressure before it creates relief

A growing DIFC company usually feels pressure in three places at once:

- Receivables stretch out: Sales are booked, but cash hasn’t landed.

- Suppliers want certainty: Vendors still expect payment on agreed dates.

- Operations scale immediately: Payroll, marketing, logistics, and restocking don’t wait for your customers to settle.

This is why strong sales can coincide with cash stress. Every extra deal may require more stock, more fulfilment, and more time before the money comes back.

Practical rule: If revenue growth is forcing you to delay supplier payments or slow new orders, you don’t have a sales problem. You have a working capital structure problem.

DIFC advice often fits funds better than operators

DIFC has a well-developed ecosystem, but much of the public discussion around capital structures focuses on investment vehicles, asset holding, and regulatory frameworks designed for funds or wealth platforms. That’s useful for some businesses. It doesn’t solve next week’s supplier run for an importer, distributor, or B2B seller waiting on invoices to clear.

For those companies, DIFC company working capital needs to be managed closer to the trading cycle itself. The best solutions usually sit where the friction sits: invoices, payment terms, stock, and supplier relationships.

Why Traditional Working Capital Methods Fall Short

The default move is often to ask the bank for an overdraft increase or a term facility. That works when the business has time, collateral, and a clean story that fits the bank’s model. Many operational SMEs don’t have all three at the same moment.

UAE SMEs face average payment terms of 60 to 90 days, and that can tie up 25% to 35% of company capital in receivables, according to a 2025 SME Finance Forum reference discussed in this DIFC funds regime article. The same reference also highlights a practical gap. Standard DIFC guidance often focuses more on large investment structures than on day-to-day liquidity for operating SMEs.

Where banks lose fit

Banks usually prefer stability. Working capital pressure is rarely stable.

A distributor may need support because one large customer has moved from thirty days to ninety. An automotive trader may have cash locked in stock. A B2B seller may need to offer terms to win the order, but still pay suppliers quickly. Those situations don’t always fit fixed-limit products well.

Common friction points include:

- Collateral-led decisions: The focus can be on hard security rather than live trade flows.

- Slow approvals: By the time the facility is in place, the buying opportunity may be gone.

- Rigid structures: A fixed line doesn’t always expand and contract with invoices or order volume.

- Extra administration: Finance teams end up feeding paperwork into a process that doesn’t match the speed of operations.

A CFO shouldn’t have to choose between growth and liquidity. But with rigid facilities, that’s often the choice the business feels.

What this means in practice

If your business is healthy but cash is consistently late relative to obligations, traditional facilities can become a blunt instrument. They may support the balance sheet, yet still leave the trade cycle underfunded.

That’s why many finance leaders now separate two questions. First, what capital supports the company overall? Second, what tool best releases cash from receivables, stock, or customer payment terms right now?

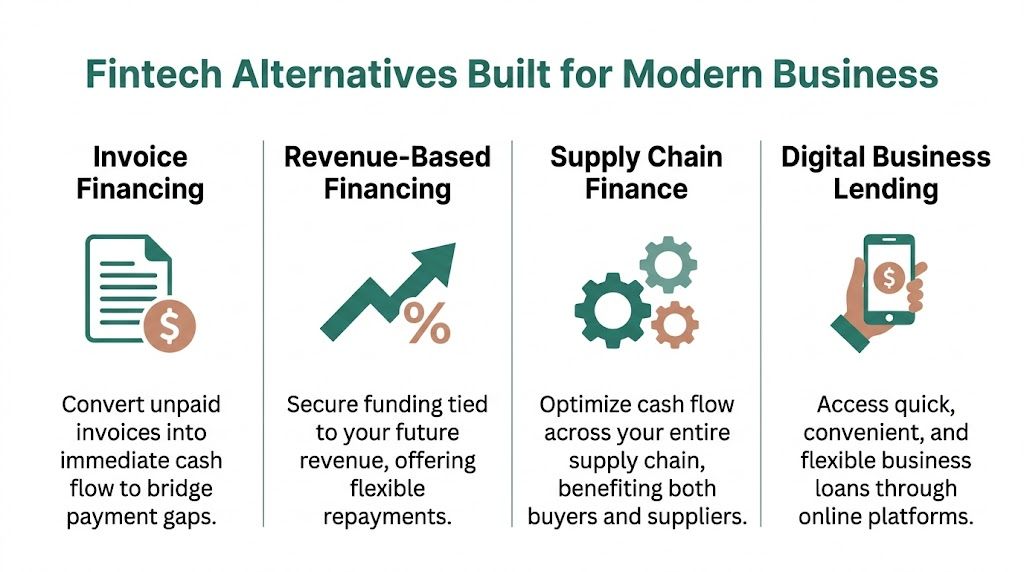

Fintech Alternatives Built for Modern Business

Modern fintech tools work best when they are tied to a real commercial event. An invoice has been issued. A buyer wants terms. A dealer has stock on hand. That’s why they can feel more practical than broad facilities that try to cover every scenario with one product.

Invoice discounting

Invoice discounting is the most direct answer when cash is stuck in receivables. You’ve done the work, raised the invoice, and now you’re waiting. Instead of waiting through the full payment cycle, the business can access cash against that invoice and use it immediately for supplier payments, payroll, or fresh stock.

This is why process matters. If your invoicing is slow, inconsistent, or full of manual follow-up, you create avoidable delays before any funding decision can even happen. A finance team reviewing options should first tighten the workflow with better billing controls and, where needed, tools such as Automated Invoice Processing Software, because faster clean invoices usually mean faster access to cash.

B2B buy now pay later

B2B Buy Now, Pay Later works from the opposite side of the transaction. Instead of asking how the seller gets paid sooner, it asks how the buyer gets time to pay without forcing the seller to absorb the delay.

For DIFC companies, this can be a commercial tool as much as a finance tool. A buyer may be ready to place the order but wants room in its own cash cycle. Flexible terms can remove that friction and help the seller close business that would otherwise stall.

A practical overview of how these models are evolving across the region is covered in fintech trends for MENA businesses.

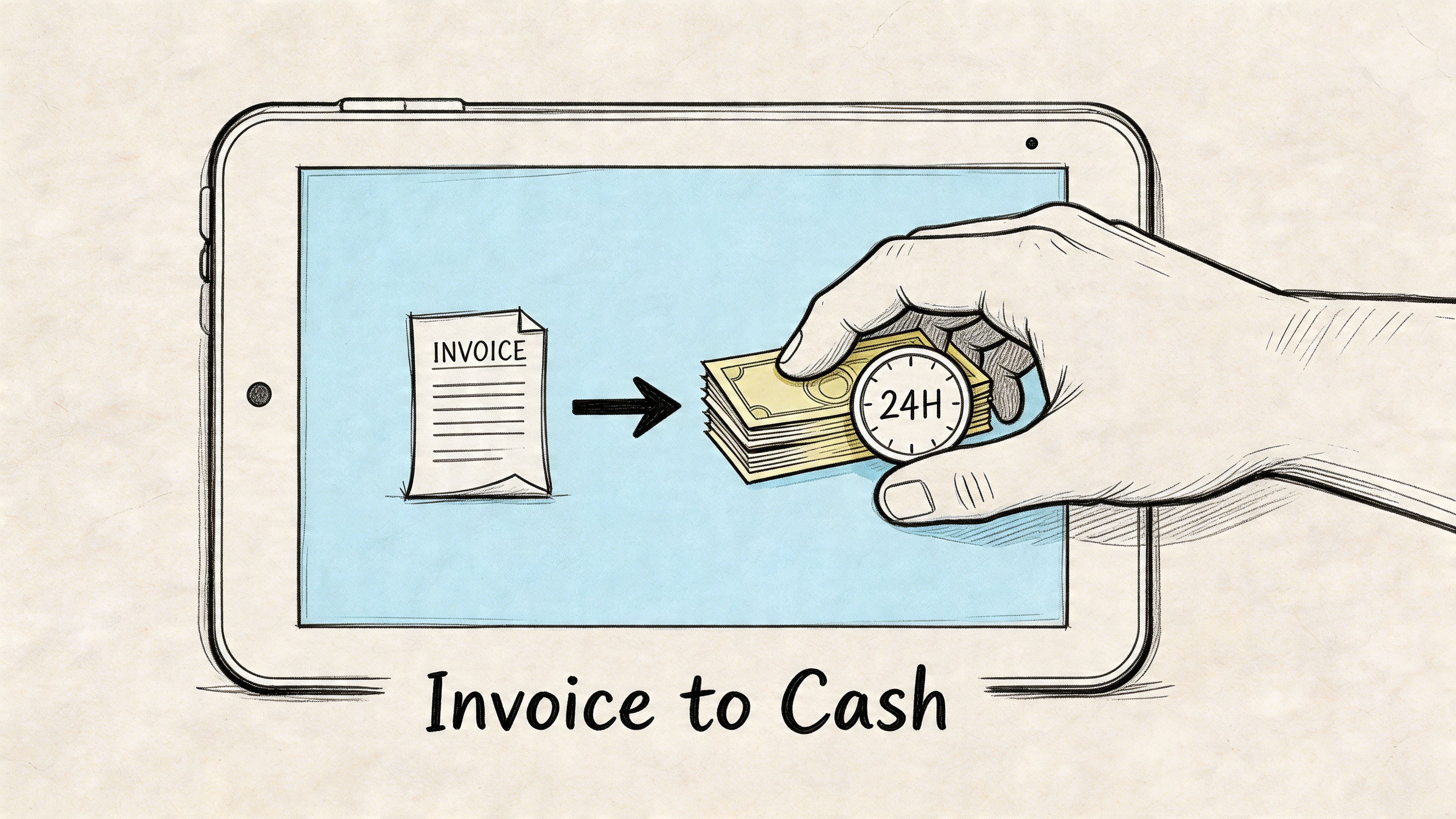

Unlock Cash from Invoices in 24 Hours

When invoice discounting is set up well, it’s one of the cleanest ways to improve DIFC company working capital because it follows a transaction that has already happened. You’re not funding a forecast. You’re releasing value from a completed sale.

According to analysis referencing DIFC VCC structures and fintech benchmarks, platforms like Comfi deliver an 85% approval rate and 24-hour funding, in an environment aligned with the pace expected by DIFC’s 50,200+ financial professionals.

How the process usually works

The practical workflow is straightforward:

- Issue a valid invoice to a business customer for goods or services already delivered.

- Submit the invoice digitally through the provider’s platform or integration.

- Complete the review process, which typically looks at the business transaction, customer quality, and supporting documentation.

- Receive funds quickly once approved, which can give the finance team room to operate without waiting for the full payment term to expire.

This matters most when the business has immediate uses for that cash.

- Supplier payments: Paying on time protects supply continuity and negotiating power.

- Inventory top-ups: Fast-moving businesses can restock before they lose momentum.

- Payroll and operating costs: Cash timing becomes less dependent on one or two slow-paying customers.

Why speed changes the finance function

Fast release of invoice cash does more than solve a temporary gap. It changes how the finance team plans.

Instead of treating receivables as a static balance that will eventually convert, the CFO can treat selected invoices as a near-term liquidity tool. That can reduce pressure on cash reserves and make monthly planning less defensive.

It also fits digital operating models. Teams that already care about collections, reconciliation, and treasury speed should pay attention to adjacent infrastructure such as real-time money transfer solutions, because cash released quickly still needs to move through the business efficiently.

For readers comparing operating models, invoice discounting options for business cash flow show how these platforms are typically positioned around speed and simplicity.

What works: Selective use on strong invoices with clear documentation.

What doesn’t: Treating every overdue or disputed invoice as if it should unlock cash.

The key discipline

Invoice discounting works best when the finance team is selective. Clean invoices, credible buyers, and completed delivery create the best fit. If your billing process is messy, fix that first. If customer disputes are common, address root causes before expecting smooth cash release.

Used properly, invoice discounting doesn’t replace treasury discipline. It gives the treasury team another lever.

Boost Sales with B2B Buy Now Pay Later

B2B Buy Now, Pay Later is often misunderstood as a payment convenience feature. In practice, it can be a sales tool.

A buyer wants the goods. The budget may exist. The hesitation is timing. If the supplier can offer structured payment terms without carrying the full burden internally, the deal moves forward faster. That matters in DIFC sectors where procurement decisions are commercial first and administrative second.

Why commercial teams like it

Sales leaders like B2B BNPL because it removes a common objection without forcing a blanket discount.

Instead of cutting price to win the order, the seller can improve terms. For many buyers, preserving cash is more valuable than shaving a small amount off the invoice. That’s especially true when they are balancing multiple suppliers at once.

Typical benefits include:

- Larger baskets: Buyers may place fuller orders when immediate cash pressure is reduced.

- Faster conversion: Deals don’t sit in approval loops waiting for internal budget release.

- Stronger buyer relationships: Flexible terms can make a supplier easier to buy from.

Why finance teams should still control it

Not every customer should receive the same terms. That’s where good process matters. BNPL should support margin and turnover, not create loose discipline around collections.

A sensible approach is to ask:

- Which buyers regularly delay orders because of payment timing?

- Which product lines benefit most from easier purchasing?

- Where does payment flexibility improve retention without harming collections quality?

For businesses assessing the commercial side of this model, B2B Buy Now Pay Later for trade purchases gives a useful product reference point.

If a buyer is good for the business but constrained by timing, better payment design often works better than another round of discounting.

Done properly, BNPL helps both sides. The buyer protects cash. The seller keeps momentum.

DIFC Onboarding The Fintech Way

Many CFOs hesitate at the same point. The product sounds useful, but they assume onboarding will be slow, document-heavy, or awkward inside a DIFC compliance environment.

That assumption is often outdated. Fintech onboarding usually starts with core business documents, recent operating information, and transaction-level evidence. The process is designed around verifying a live business and the quality of underlying trade, rather than forcing every applicant through the same collateral-based path banks often use.

Why this is more practical than structural solutions

There’s ongoing discussion around VCCs and other advanced structures in DIFC. They may suit investment or asset-holding purposes. They are not the first answer for an operating SME that needs immediate liquidity from invoices or stock.

That gap is reflected in broader SME conditions. A Q4 2025 KPMG survey, cited in this note on the proposed DIFC VCC regime, found that 40% of UAE SMEs cite inventory financing gaps. The same discussion points to a simple reality. Accessible fintech platforms often address these operating needs more directly than complex corporate structures.

What a finance team should prepare

The smoothest onboarding usually comes from preparation, not improvisation.

- Corporate records: Trade licence and core company documents should be current and consistent.

- Banking visibility: Recent statements should support the transaction story the business is presenting.

- Invoice discipline: Approved invoices, proof of delivery, and buyer details should be easy to retrieve.

- Internal ownership: One person in finance should manage the full submission process end to end.

Fintech often excels in usability. The process is closer to operational due diligence than a long-form facility negotiation.

A CFOs Checklist for Unlocking Working Capital

If you’re reviewing DIFC company working capital options, start with the blockage, not the product.

- Map the cash delay: Identify whether cash is mainly trapped in receivables, inventory, or customer demand for longer terms.

- Segment your invoices: Separate clean, undisputed invoices from weak or delayed ones. Only the first group is useful for fast cash release.

- Review supplier pressure points: Note which vendors affect continuity if payment slips. Those are the relationships working capital tools should protect first.

- Test B2B BNPL selectively: Use it where payment flexibility helps close higher-quality orders, not where it merely masks weak demand.

- Tighten invoice operations: Billing speed, proof of delivery, and reconciliation quality directly affect how quickly receivables can turn into usable cash.

- Prepare onboarding documents early: Keep licences, statements, and trade evidence organised before liquidity pressure becomes urgent.

- Measure outcome properly: Track whether the tool improves stock turns, supplier reliability, collections timing, and sales conversion. Don’t judge it only by cost.

- Avoid false solutions: If the problem is operational cash timing, don’t default to complex structures designed for fund or holding use.

The best working capital strategy is rarely the most complicated one. It’s the one your team can use quickly, repeatedly, and with control.

If your business is dealing with slow collections, supplier pressure, or buyers asking for longer terms, Comfi is worth a look. It offers practical tools built around invoices, payment terms, and dealer inventory, so DIFC-based SMEs can free up cash already tied up in normal trading activity without relying on rigid traditional banking processes.

Related Reading

- How Can MENA SMEs Master Working Capital?

- Staffing Agency Payroll Financing UAE: Boost Cash Flow 2026

- SME Cash Flow Management: A Guide for MENA Businesses

- Improve Working Capital for UAE IT Services Business

Ready to improve your business cash flow? Get started with Comfi today.